EXLS - ExlService: A Bet On Great AI Execution

2023-10-12 01:37:05 ET

Summary

- ExlService Holdings provides analytics and digital operations solutions to businesses in numerous industries.

- The company's AI investments present opportunities for further growth and cost efficiencies as the data analytics models could be streamlined with the technology.

- EXLS has a fantastic long-term track of profitable growth, but the growth seems to already be priced into the stock - I have a hold rating for the stock.

ExlService Holdings (EXLS) provides analytics and digital operations solutions. The company has a fantastic long-term track record of profitable growth both organically and through select acquisitions. As AI models become better at interpreting data, the company could face further tailwinds for growth - the future seems exciting for ExlService. Although the company seems promising, I can't constitute a buy rating as the stock already seems to be priced for significant growth - for the time being, I have a hold rating.

The Company & Stock

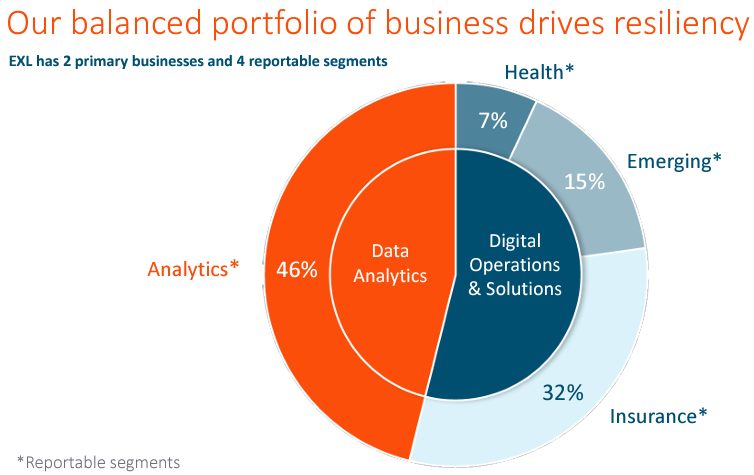

ExlService splits its business into two primary distinct parts representing quite similar amounts in revenue - Data Analytics and Digital Operations & Solutions. The latter business part is further divided into separate segments:

ExlService's Business Parts (EXLS October Investor Presentation)

{kind=link}

The Data Analytics part of ExlService focuses on providing value for businesses in insurance, banking, healthcare, retail, media, and sports among other industries, through proprietary analytical models that process businesses' data into insights that can be used to improve operations. The company has a large amount of data scientists to process the data and to improve Exl Analytics' models.

Although the word is too often used as a buzzword, I do believe that AI represents a good opportunity for ExlService, as the company communicates in its October investor presentation . As AI becomes better at recognizing patterns in massive amounts of data and interpreting the findings, artificial intelligence could be used to both improve the offering through a more refined model, as well as improve the company's cost structure through efficiencies that an AI could provide; the Data Analytics business part seems very interesting.

The Digital Operations & Solutions part provides solutions for businesses that help in claims management, client acquisition, finance and accounting, and customer service. This part of the business seems good in the fact that it is very stable - contracts are made on a multi-year basis with a very high renewal rate.

The company's stock has performed very well on the stock market in its history - from the IPO in 2006, the stock has returned a 617% return to investors, representing a CAGR of around 12.3%:

Stock Chart From IPO (2006) (Seeking Alpha)

{kind=link}

Financials

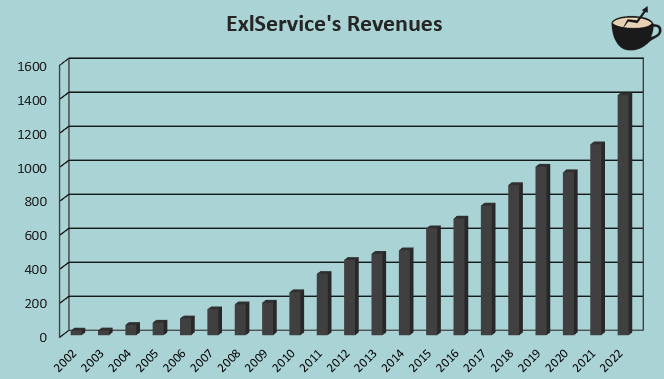

ExlService's growth has been phenomenal - from 2002 to 2022, the company has achieved a compounded annual growth of 21.8%:

Author's Calculation Using TIKR Data

{kind=link}

Although ExlService does have some acquisitions, the growth seems to be mostly due to organic efforts - from 2013 to 2022, the company's cash acquisitions add up to less than half a billion, representing quite a small amount of the current market capitalization of around $4.9 billion - in the same period, the company's revenues have risen by 195%. The growth doesn't seem to show signs of slowing down - in the first half of 2023, ExlService's growth was 19.2%.

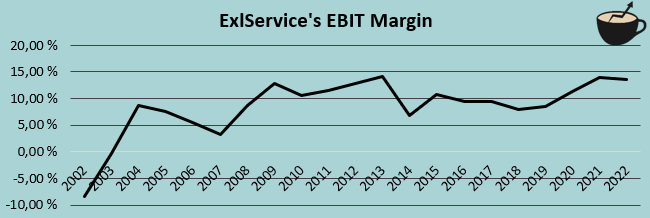

The company has achieved an average EBIT margin of 8.5% from 2002 to 2022. The margin has had some variance, but overall has stayed on a good level.

Author's Calculation Using TIKR Data

{kind=link}

Currently, ExlService's trailing EBIT margin stands at 14.6%; the company has achieved a very good amount of growth in the past couple of years, creating a good amount of operating leverage. The margin could see some further expansion in the medium- to long-term future, too - as AI models become a more valuable part of ExlService, the company's cost structure could be improved further.

Valuation

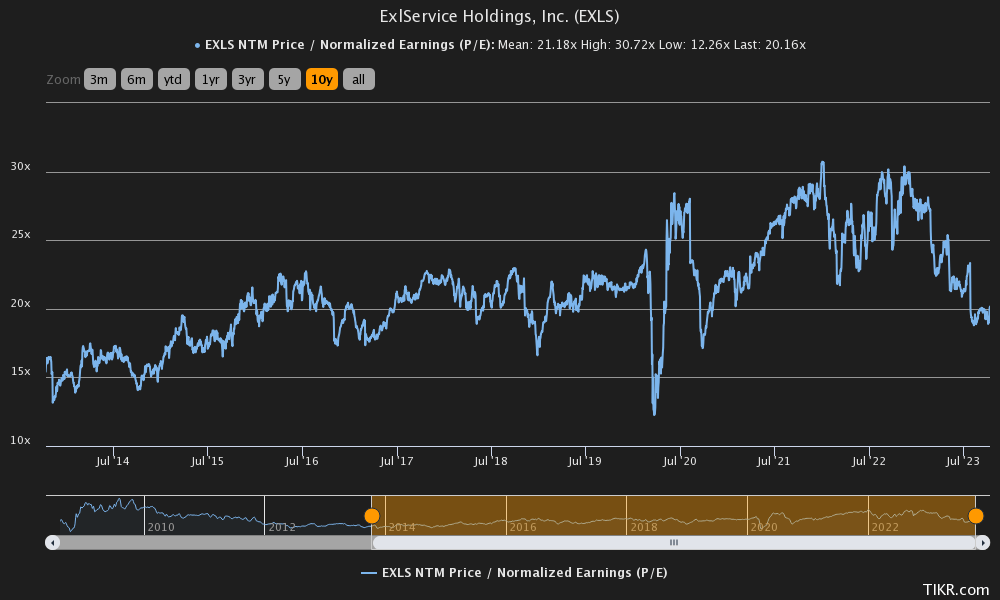

ExlService's P/E ratio is currently near the ten-year average of 21.2 - the ratio currently stands at 20.2:

{kind=link}

The P/E ratio seems quite reasonable at first glance as ExlService has had a good amount of organic growth in its history. To further analyze the valuation, I constructed a discounted cash flow model as usual to estimate a rough fair value for the stock.

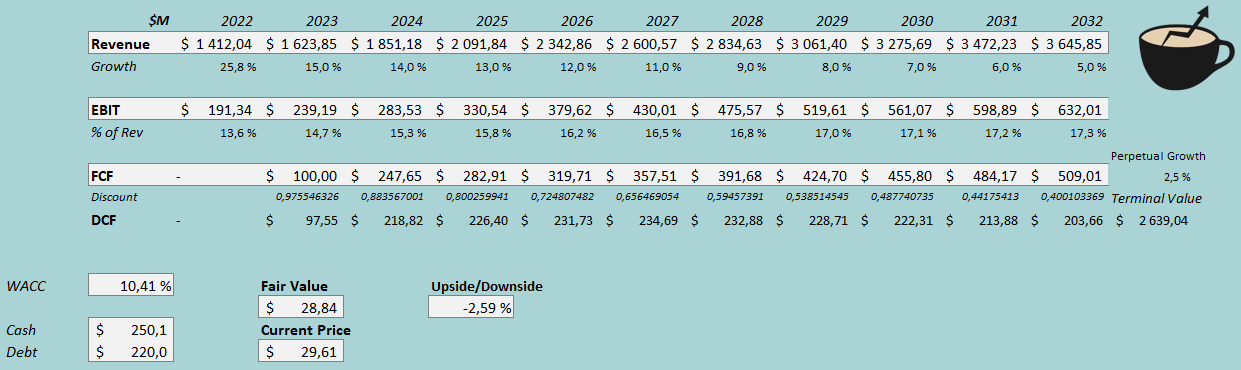

In the model, I estimate a growth of 15% for the current year, in line with ExlService's tight revenue guidance. Going forward, I estimate quite similar growth - for 2024, I have a growth estimate of 14%. Beyond the year, I estimate growth to slow down in very slow steps - in 2032, the growth is still at 5%, and the CAGR from 2022 to 2032 is 10.0% in the estimates. After 2032, I estimate a perpetual growth rate of 2.5%, slightly above my usual estimate of 2% as I see ExlService's long-term growth opportunity as very good.

For the company's EBIT margin, I estimate some further operating leverage as a result of a larger scale of operations as well as the utilization of artificial intelligence - I estimate a margin of 14.7% for 2023, 1.1 above the level achieved in 2022. Beyond the year, I estimate ExlService's margin to grow by 2.6 percentage points in slow steps into a margin of 17.3% in 2032. The company has a very good cash flow conversion as the CapEx level seems quite moderate and the company doesn't tie very much working capital with the growth.

The mentioned estimates along with a cost of capital of 10.41% craft the following DCF model with a fair value estimate of $28.84, around 3% below the current price:

DCF Model (Author's Calculation)

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, ExlService had $3.24 million in interest expenses. With the company's interest-bearing debt amount, the company's interest rate comes up to 5.89%. It is important to note that the company's amount of debt is quite low - the derived interest rate could vary largely if the company is to draw more debt, although I do think that the estimate is fairly representative of a good long-term estimate. As ExlService uses debt very conservatively, which is why I estimate a very low long-term debt-to-equity ratio of only 5%.

The risk-free rate of 4.58% is the United States' 10-year bond yield , which I think fairly represents a risk-free return on the cost of equity side. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate made in July. Yahoo Finance estimates ExlService's beta at 0.98 . Finally, I add a small liquidity premium of 0.35% into the cost of equity, crafting the figure at 10.72% and the WACC at 10.41%, used in the DCF model.

Takeaway

ExlService should be facing good times ahead as the AI boom continues and the company continues its long-term track of growth. Although I believe that the company should grow its revenues significantly along with some operating leverage, I don't think the current price necessarily represents a good buying price - my DCF model estimates the stock to be roughly fairly valued. As it stands, I believe a hold rating is constituted.

For further details see:

ExlService: A Bet On Great AI Execution