OIS - Expect Oil States International To Turn Around (Rating Upgrade)

2024-01-17 07:18:43 ET

Summary

- Oil States International is transitioning to subsea minerals, renewable, and clean tech energy systems.

- The company's operating margin improved in Q3 and it has a strong backlog in the Offshore/Manufactured Products segment.

- OIS's stock is undervalued compared to its peers and has the potential for significant returns.

OIS Is On A Steady Trajectory

I have been discussing Oil States International (OIS) in the past, and you can read the latest article here . The company has been gearing up to transition to subsea minerals, renewable, and clean tech energy systems for the past few quarters. It has also strengthened its position in the traditional subsea market through new product introductions, primarily through increased project activity in Brazil and Guyana. The onshore market should recover in 2024, as the early indicators show. The company's operating margin also made gains in Q3.

However, it will continue facing a slowdown in the completion market. The company's cash flows improved remarkably in 9M 2023 while maintaining low leverage. The stock is relatively undervalued versus its peers. Based on the growth factors and the valuation multiples, I see an impressive return possibility from the stock. I suggest investors "buy" it.

Company Outlook

The legacy operations that OIS excelled in the past are the subsea, floating, and fixed production operations. However, it has started pursuing deep-sea minerals gathering, offshore wind developments, carbon capture, and other renewable and clean tech energy opportunities.

Offshore, it has introduced new products, including Merlin Deep Sea Mineral Riser System and Active Seat Gate Valve Technology. The company sees growth opportunities in an offshore-focused investment cycle over the next two years as energy prices recover in 2024. The company pinpoints its focus on the international growth markets, particularly offshore. However, it will continue to serve the US markets with enhanced product offerings.

In the Offshore/Manufactured Products segment, revenues should grow in 2024 due to a strong backlog. Also, the achievement of the project milestones will help it accelerate. However, its Well Site Services and Downhole Technologies segments can relatively underperform. In Q3, these segments saw headwinds following softer US onshore activities. Based on the lag before the rig count or drilling activity takes before it follows the energy price's recovery, I expect these services are close to a bottom and will likely bounce back in 2024.

Industry Outlook

{kind=link}

The company estimates that the global crude oil and natural gas inventories are normalizing. However, natural gas prices are still under the pump and can decline further. Therefore, it can partially mitigate the overall growth of drilling and completion spending.

On the other hand, the earlier investments in long lead time projects in international offshore projects have started materializing. The consolidation in energy prices' long-term outlook points to a multiyear upcycle. Considering everything, I think the company's offshore and international operations will propel its revenues, adjusted EBITDA, and free cash flow to grow in 2024.

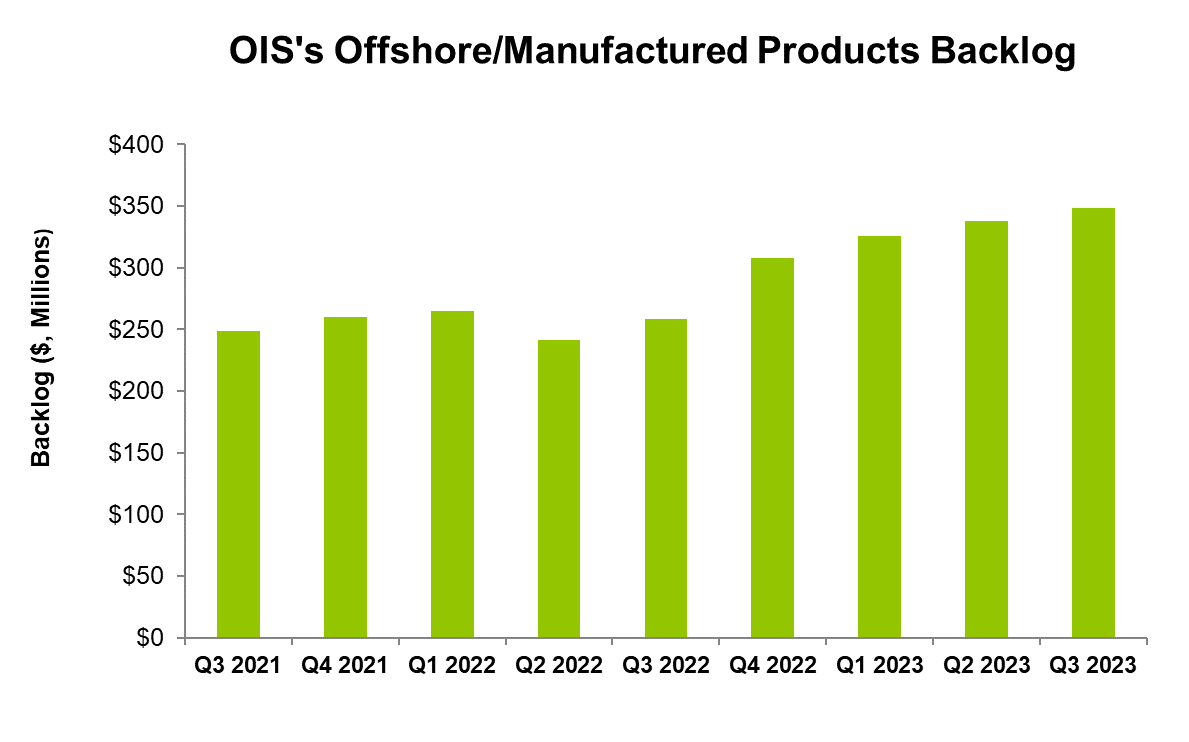

Projects And Backlog

{kind=link}

In Q3, OIS's Offshore/Manufactured Products segment backlog increased by 3% sequentially and 35% year-over-year. Its book-to-bill ratio also increased from 1.1x to 1.2x in Q3. Among the major orders were a Merlin Deepsea Mineral Riser System and a production facility equipment order for Brazil.

The company has seen increased project activity in Brazil and Guyana, led by improved subsea technology tied to production infrastructure. Quarter-over-quarter, the segment saw five consecutive increases in backlog due to new product introductions like its MPD (managed pressure drilling) systems. Although making a call precisely at this point will not be accurate, I think a book-to-bill ratio above one indicates the segment's strong revenue visibility in the medium term.

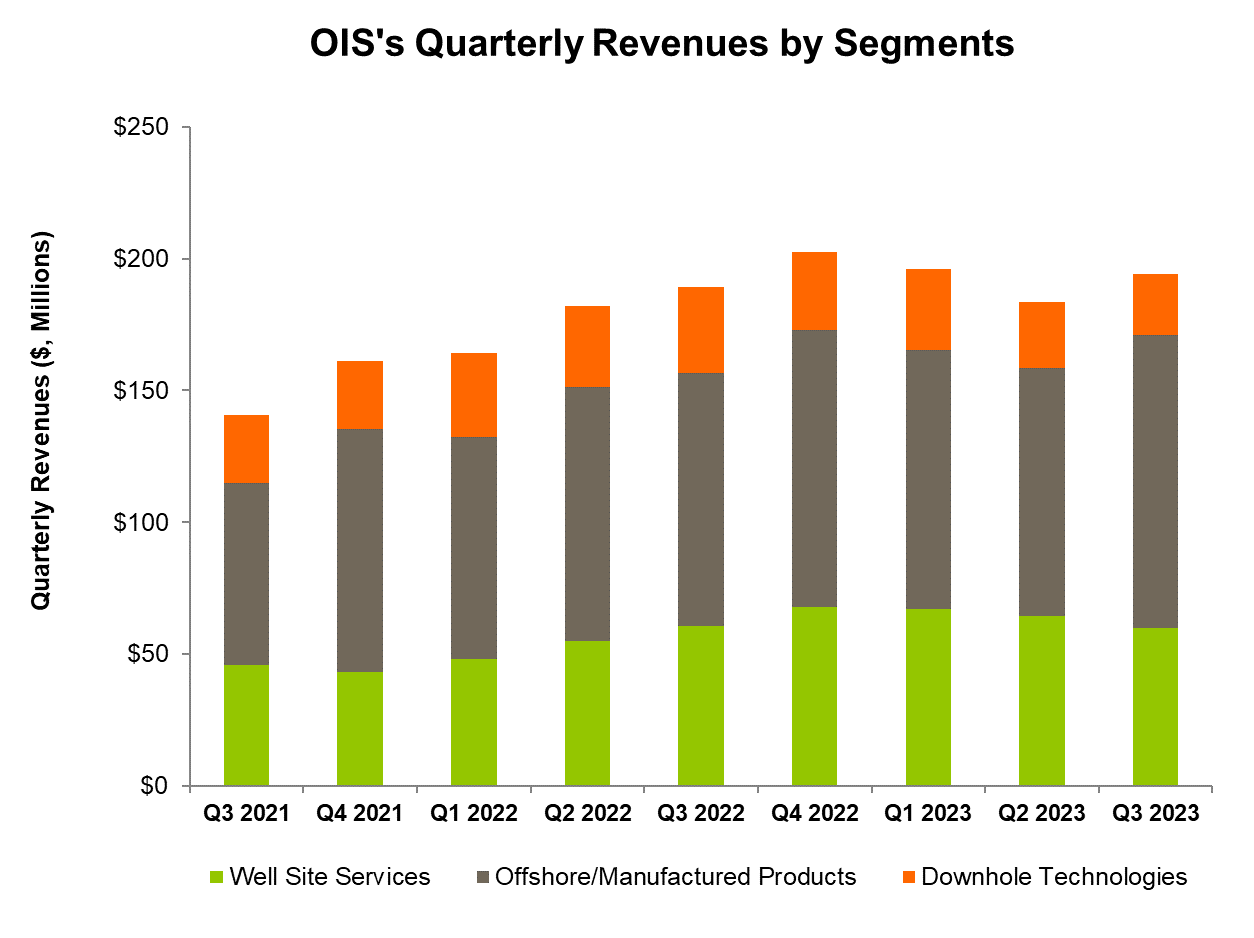

Analyzing Q3 Performance

{kind=link}

In Q3 2023, the Offshore Manufactured Products segment revenues increased by 18% quarter-over-quarter. As a result of higher revenues, the adjusted EBITDA margin expanded by 500 basis points in Q3. On the other hand, the Well Site Services segment witnessed a 7% lower revenue in Q3, while its adjusted EBITDA margin declined by 150 basis points during this period. The Downhole Technologies segment saw a similar sequential revenue fall (by 20%) in Q2 2023, while its adjusted EBITDA margin turned negative in Q3.

As I have discussed in the article, customer demand for completion products shrank in Q3. Also, a reduction in frac spreads led to lower manufacturing volumes. Competition, however, remained intense in the oilfield services industry. All these factors diminished performance in the Well Site Services and Downhole Technologies segments in Q3.

A Margin Analysis

In Q3, OIS's adjusted EBITDA margin expanded by 170 basis points to 12% from a quarter earlier. The company believes it can hold or improve the EBITDA margin to "high teens" EBITDA margins based on strong project work and contributions from higher service revenues. So, a higher revenue base, better cost absorption, and better product mix - all contributed to improved margins in Q3.

Key Challenges

In Q3, several frac spreads were retired or went offline. In the first nine months of 2023, 19% of frac spread counts decreased. As a result, the demand for the downhole tools also went down. The pressure pumpers have relatively long contracts and, therefore, get hit more than product-sell businesses (e.g., wireline), which rely more on spot market rates. These factors adversely affected OIS's Downhole Business segment.

In 2024, the company plans to transform some of its operations to spot-based activity and introduce new technology to improve its domestic business. Plus, it works on expanding its international operations. The management is optimistic about a profitable turnaround in 2024.

Cash Flows And Debt

In 9M 2023, OIS's cash flow from operations increased by 1.7x from a year ago. Its capex also increased by 76% during this period. Consolidation and relocation of certain facilities in the US and other geographies caused capex to rise. Despite higher capex, free cash flows (or FCF) improved handsomely in 9M 2023.

OIS's debt-to-equity ratio was 0.19x as of September 30, 2023. It had $188 million in liquidity as of that date. The company expects to invest ~$35 million in capex in FY2023.

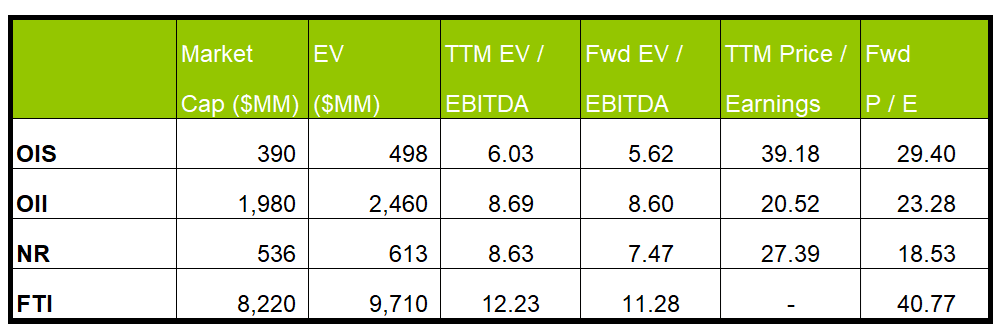

Relative Valuation

Author Created and Seeking Alpha

{kind=link}

OIS's forward EV/EBITDA multiple contraction versus the adjusted EV/EBITDA is as steep as its peers because its EBITDA is expected to rise as sharply as its peers in the next year. This typically results in a similar EV/EBITDA compared to its peers. The company's EV/EBITDA multiple (6x) is lower than its peers' (OII, NR, and FTI) average. So, the stock is undervalued at this level compared to its peers.

The stock is trading at a discount to its past five-year average EV/EBITDA of 12.2x. I do not see the stock returning to trading at the past multiple in the short term. However, if it trades at the industry average in the medium term, it can climb 90% from the current level.

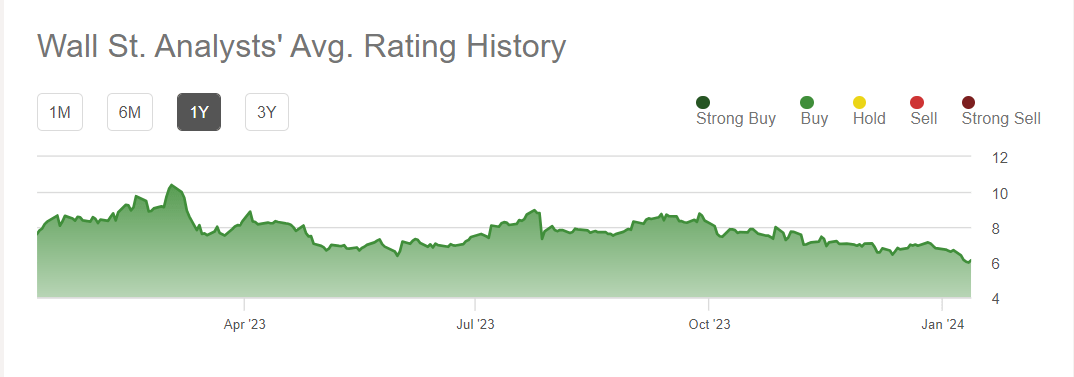

Analyst Target Price And Rating

{kind=link}

Three sell-side analysts rated OIS a "buy" in the past 90 days (including "Strong Buy"), while two recommended a "hold." None ranked it as a "sell." The consensus target price is $9.2, which yields 51% returns at the current price. Based on the value drivers and comparing my relative valuation analysis, I think the Wall Street analysts have fairly reasonable expectations from the stock.

Why Do I Change My Call?

I did several iterations on OIS in the past. While the company benefited mostly from the shorter-cycle onshore projects in the past, the US market has become relatively unsteady. The backlog stability has remained, though. In the past, it suffered from cash flow deficiencies.

In my previous article, I noted that drilling and completion spending lowered in the US. Cash flows turned around in 1H 2023. The company embraced new techs like offshore wind developments, subsea minerals gathering, and other renewable energy systems. I wrote :

I see a multiyear upcycle in the global energy business, which will benefit the long lead-time projects. Although the US rig and frac counts declined in 1H 2023, they can potentially see an uplift in 2H 2023. With more than half of its revenues coming from international and offshore markets, OIS's recent orders strengthen its strategy of diversifying into subsea minerals and renewable and clean tech energy systems.

After Q3, OIS will invest in new product developments, seeing the growth opportunities offshore. Its steady backlog provides a strong backbone for the topline growth. The near-term US energy market volatility and the slowdown in downhole technology can mitigate rapid recovery. But, given the undervaluation, I upgrade the stock to a "buy."

What's The Call On OIS?

{kind=link}

In the recent past, OIS invested in new technologies, including Merlin Deep Sea Mineral Riser System and Active Seat Gate Valve Technology. The offshore investments should start yielding results soon because long lead time projects in international offshore projects have materialized. Although the US frac counts declined in 9M 2023, drilling activity will likely recover in 2024, and completion activity will follow suit. OIS's recent order backlog is a robust signal in that direction.

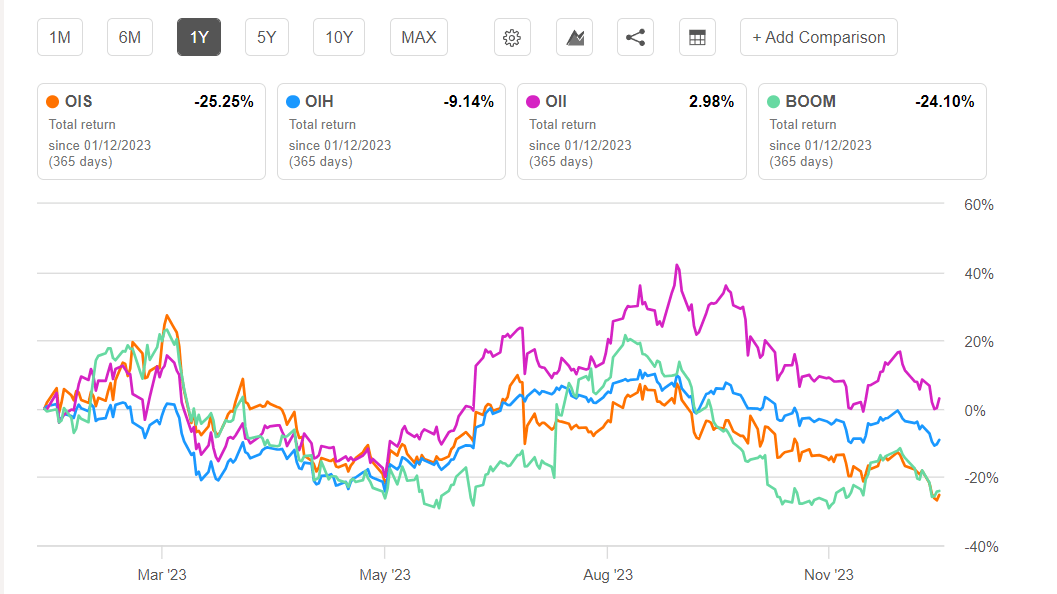

However, the slowdown in completion activity continues to cast doubt over the company's rapid recovery. So, the stock underperformed VanEck Vectors Oil Services ETF ( OIH ) in the past year. The company improved its cash flows considerably. Given the steep drop in its stock prices in the past six months and its relative undervaluation, I think investors have an opportunity to "buy" it at this price range.

For further details see:

Expect Oil States International To Turn Around (Rating Upgrade)