CVX - Expectations For ConocoPhillips' Q2 Earnings

2023-07-21 11:32:52 ET

Summary

- ConocoPhillips' stock has risen by around 10% over the past month due to firming oil prices and anticipation of a solid Q2 report.

- The company's earnings are primarily dictated by the price of oil, with Q2 earnings expected to be lower compared to Q1 due to a drop in petroleum prices.

- ConocoPhillips has been criticized for prioritizing share buybacks over dividends, with the company allocating $9.3 billion on share buybacks compared to $5.7 billion on dividends in 2023.

- Meantime, risks are growing as COP has yet to embrace the EV and renewable energy transition in any meaningful way.

ConocoPhillips' ( COP ) stock is up ~10% over the past month (see chart below) as oil prices have recently firmed a bit and investors anticipate another solid quarterly report - Q2 results are due out on Aug. 3. Today I will review what investors should expect from COP's Q2, discuss the company's return of capital plan (i.e., stock buybacks and dividends), and touch on the rising risks to shareholders due to the company's failure to embrace the EV and clean-energy transition in any significant fashion. Indeed, COP's over-emphasis on share buybacks over the dividend effectively forces shareholders to double down on the future of oil and gas as the planet desperately needs to ween itself off fossil fuels and as the EV and renewables transition accelerates.

Oil Price

Being the largest independent O&G company in the world, Conoco's earnings are primarily dictated by the price of oil and, to a lesser extent, the price of LNG (for which the majority of COP's production is contractually linked to the price of Brent), natural gas, and NGLs.

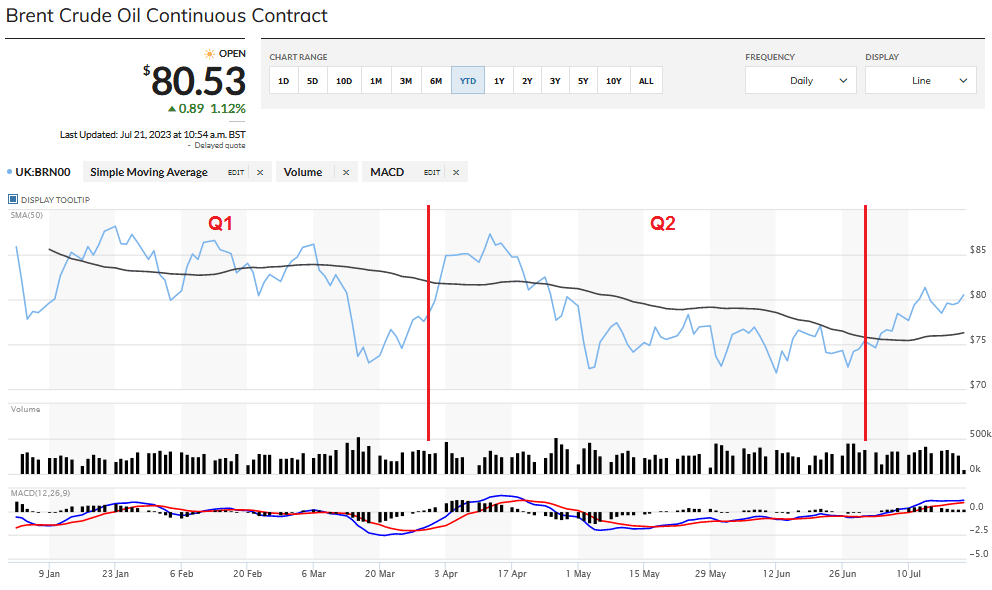

The chart below shows the price of Brent crude since the beginning of the year:

{kind=link}

As can be seen in the graphic, the price of Brent had been on a downward drift throughout 2023 until just recently when the simple moving average bottomed and moved ever so slightly higher (far right of the graphic). That being the case, and all else being equal (but realizing it seldom is…), investors should expect COP's overall realized price in Q2 - and its earnings - to be lower as compared to Q1. I estimate COP's realized Brent price to average roughly $6/bbl lower in Q2 as compared to Q1.

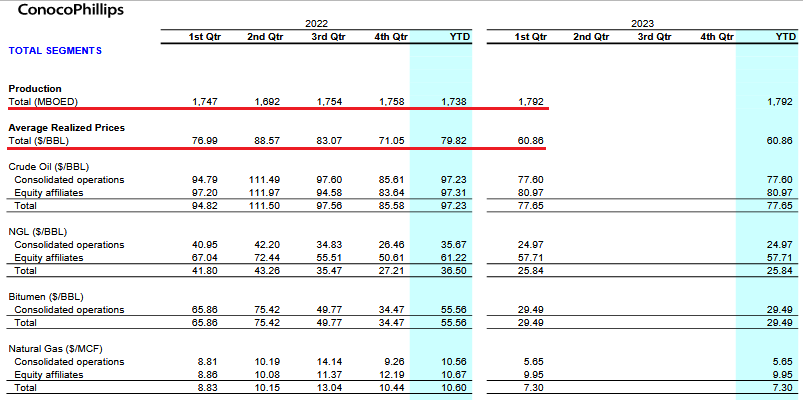

The graphic below was taken from COP's Q1 Supplemental Report. It clearly shows that realized prices across the entire petroleum complex (i.e., crude oil, NGLs, bitumen, natural gas) are not only likely to be lower sequentially, but also significantly lower on a year-over-year basis as well:

{kind=link}

All in, my estimate is that COP's total average realized price could come in ~$10/bbl lower as compared to Q1, or an estimated $50/bbl. Given that, a straight read-across from the $2.28/share earned in Q1 would be an estimated $1.96/share for Q2:

| ConocoPhillips |

| Q1 |

| Q2 (Estimated) |

| Average Realized Price |

| $60.86/bbl |

| $50/bbl |

| EPS |

| $2.38/share |

| $1.96/share |

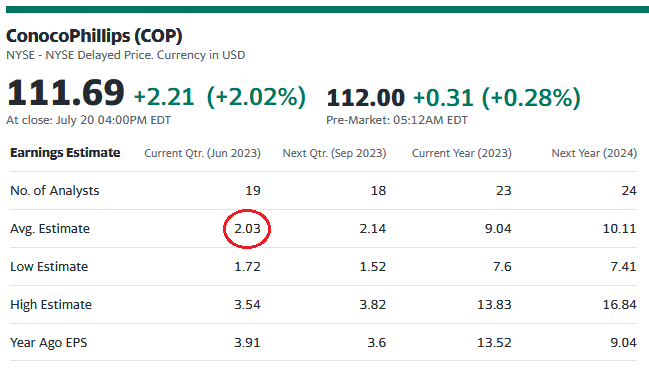

And my estimate is roughly in line with what is reflected in current consensus estimates (courtesy of Yahoo Finance ):

{kind=link}

My straight-across Q2 earnings estimate of $1.96/share did not take into account the fact that the midpoint of COP's previous Q2 production guidance (1.79 million boe/d) would be ~90,000 boe/d above Q1.

In addition, COP's interest expense should be falling as the company continued to reduce its debt load during the quarter by announcing it would tender up to $1.1 billion in Notes (some with rates as high as 6.5% and 7.8%).

In addition, my $1.96/share EPS estimate did not take into account the reduction in outstanding shares as a result of COP's massive share buyback program. So, let's take a closer look at that.

Stock Buybacks

As my followers know, I have been quite critical of COP's CEO and board of directors decision to significantly over-emphasize share buybacks (at the top of the commodity price cycle) as compared to dividends directly to shareholders. I also have pointed out that COP's return of capital strategy is drastically different from that of peers EOG Resources ( EOG ) and Pioneer Natural Resources ( PXD ), both of which prioritize dividends over share buybacks (see PXD Could Pay $30/share In FY22 Dividends ).

Indeed, for all of FY2022 COP allocated $9.3 billion on share buybacks as compared to only $5.7 billion on dividends. Thankfully, that over-emphasis narrowed somewhat in Q1 with $1.7 billion allocated to share repurchases and $1.5 billion for dividends.

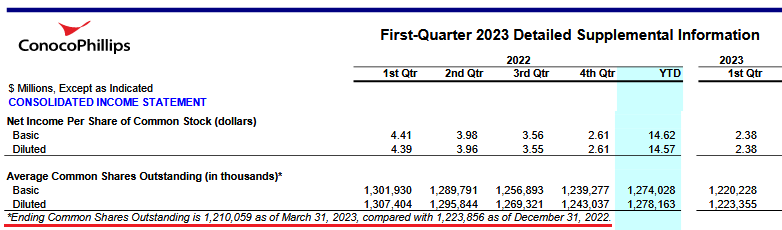

As the note in the table below shows, the result is that COP's outstanding share count fell to 1.210 billion shares at the end of Q1 - down from 1.224 billion shares at the end of 2022 (or down an estimated 13.8 million shares, or -1.13%, during the quarter):

{kind=link}

Investors will be interested to see how much COP allocated to buybacks during Q2 and what was the net impact on the outstanding share count and the resulting EPS. Remember, in the Q3 report last year, COP increased its existing share buyback authorization by a whopping $20 billion. To put that into perspective, note that COP's current market cap is $132.5 billion.

Dividends

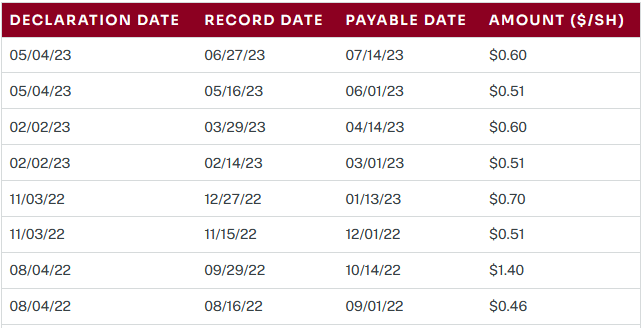

The table below was taken directly from COP's dividend history webpage and shows the company's base plus variable dividend declarations for the last four quarters:

{kind=link}

In aggregate, COP's total TTM dividends equate to $5.29/share. Given the stock closed Thursday at $111.69, that works out to a yield of 4.7%. I have previously alerted investors to the fact that the TTM yield as reported by most financial websites (such as Yahoo Finance and Seeking Alpha) typically only report the yield based on the base dividend, and are - as a result - way off. Currently, Yahoo Finance reports COP's yield as 2.19% while Seeking Alpha says it is 1.86%. Both are, obviously, way off base.

Risks

The following table shows COP's current P/E valuation relative to some of its shale peers:

| Company |

| TTM P/E |

| Forward P/E |

| ConocoPhillips |

| 8.72x |

| 12.2x |

| EOG Resources |

| 7.65x |

| 11.3x |

| Pioneer Natural Resources |

| 7.58x |

| 11.0x |

| Diamondback Energy ( FANG ) |

| 5.80x |

| 8.1x |

NOTE: TTM P/Es are per Yahoo Finance; Forward P/E's per Seeking Alpha.

As you can see, COP trades at a premium to its shale centric peers, which is rational given that COP arguably has a superior portfolio (i.e., non-shale assets like Alaska and LNG) and a massive shale drilling inventory in the Permian after buying Concho Resources and Shell's assets.

In my opinion, the biggest risk COP faces is the transition to renewable energy and EVs. I know I won't be popular mentioning what Al Gore said in an article being read by O&G investors, but sometimes investors need to hear what they don't like. Regardless, in a recent New York Times article , and with the planet literally on fire - with smoke from Canadian fires reaching Atlanta, extreme temperatures all across the U.S., and with seawater off the coast of Florida reaching near hot tub temperatures - what Gore said rang true to me. After pointing out that 80% of all the energy in the world today still comes from fossil fuels, Gore said:

Fossil fuel companies are desperately trying to use their political and economic networks and their successful capture of policy in too many countries to slow down this transition. They don't disclose their emissions. They don't have any phase-out plan. They're not committed to a real net zero pathway. They're greenwashing. They're performing anti-climate plotting. The climate crisis is in the main a fossil fuel crisis.

I agree. Gore goes on to point out that if the world is not permitted to discuss the phasing down of fossil fuels because the fossil fuel companies don't want the world to discuss it, that's indicative of "a very flawed process." And that is what has been happening.

However, Gore also pointed out how quickly renewable energy and EV adoption is growing and quoted the economist Rudiger Dornbusch :

Sometimes things take longer to happen than you think they will, and then they happen faster than you thought they could.

And I think that could be exactly the case with a company like ConocoPhillips, which has, at least to date, refused to allocate significant capital to solar, wind, and battery backup capacity. The same is true of big international oil companies like Chevron ( CVX ) and Exxon Mobil ( XOM ) as well. Both companies have given a lot of lip service to "sustainability," but are doing very little to actually position their companies to become sustainable (i.e., no capital allocation to wind, solar, and battery backup). That said, I was happy and excited to see reporting that Exxon is "planning to build one of the world's largest lithium processing facilities in Arkansas, with a capacity to produce 75K-100K metric tons/year of lithium. At that scale, the plant's production would equate to ~15% of all finished lithium produced globally last year." Now that would actually be a move in the right direction.

Summary and Conclusion

COP's low cost-of-supply portfolio will be solidly profitable in Q2 despite the general slide in commodity prices across the petroleum space on both a qoq and yoy basis. However, it will be very interesting to see how the company allocates capital to share buybacks vs. dividends directly to shareholders. Note that an over-emphasis on share buybacks effectively forces shareholders to double down on the future of oil and gas. As you can tell from the above "risks" section of this article, my opinion is that the allocation strategy is risky for shareholders given that COP has allocated no significant capital to position the company for the transition to EVs and renewable energy.

Regardless, I rate COP a hold based on an attractive yield, significantly discounted valuation level as compared to the S&P 500, its strong position in Alaska and global LNG, and the prospects for rising petroleum prices in the second half of this year.

I'll end with a five-year total returns chart of COP as compared to some of its O&G peers as well as to the S&P 500 and Nasdaq-100 as represented by the Vanguard S&P 500 ETF ( VOO ) and the Invesco Nasdaq Trust ( QQQ ), respectively:

Investors may be surprised to see that COP has returned more than all those listed except for the triple Qs.

For further details see:

Expectations For ConocoPhillips' Q2 Earnings