ABNB - Expedia: Currently More Attractive Than Peers (Rating Upgrade)

2023-12-08 04:02:49 ET

Summary

- Expedia's turnaround efforts are leading to accelerating growth and improving margins, creating a promising medium-term outlook.

- EXPE's Q3 earnings report showed record revenue and EBITDA, with growth in gross bookings and lodging revenue.

- I now believe we are at an inflection point in which it seems safe to assume growth will keep accelerating in the coming quarters.

- The involvement of activist investor ValueAct is seen as a positive, as they bring experience and are looking to work with management.

- From a current price level of $143, my calculations point to annual returns exceeding 20%, easily outperforming global benchmarks.

Introduction - Challenges remain, but fundamental improvements are appearing

I upgrade my rating on Expedia Group, Inc. ( EXPE ) from Hold to a Strong Buy despite a 25% share price gain since my last article on the company as I firmly believe the investor proposition has become meaningfully more attractive as management's turnaround efforts seem to materialize in accelerating growth and rapidly improving margins, leading to a very promising medium-term outlook.

I last covered Expedia in August. I rated shares a hold despite my enthusiasm for the company's fundamentals. It is a prominent player in the international travel sector, commanding a varied collection of robust brands that have gained the confidence of countless global travelers, resulting in a market share of 26.4% in the international digital travel market, only trailing Booking Holdings ( BKNG ) and a 42% market share in the US digital travel market, as pointed out in my August article.

The company's substantial market presence and consistent revenue expansion emphasize its position within the online travel agency domain. Despite encountering obstacles like changing market conditions and profit margin constraints, Expedia has demonstrated potential for future growth through recent initiatives like consolidating loyalty programs and tackling operational inefficiencies. Overall, these developments resulted in an excellent growth outlook of high-single-digit revenue growth and double-digit EPS growth.

And yet, I rated shares a hold. Why? This is mainly due to the company remaining inferior to industry leader Booking in terms of technology, customer experience, and long-term growth initiatives, significantly increasing the risk profile and making me wonder whether this will remain a drag on growth for Expedia. In the end, within the travel industry, the strong platform attracts the most customers, making it hard for Expedia to fight Booking without significant changes, creating uncertainties. Furthermore, management's track record of shareholder dilution and margin challenges requires some consideration.

As a result, I valued the company at quite a significant discount for the time being. I believe investors had to give the company and its management team more time to see recent positive developments reflected in its financials through margin improvements and a more efficient business model that allows the company to move forward and further strengthen its market position. If it does so, there is a lot of room for multiple expansions for sure.

Eventually, even as the company appeared undervalued based on conservative multiples, I rated shares a hold as the upside potential did not outweigh the fundamental struggles. Yet, since my prior article, shares are up 24% mainly in response to a strong Q3 earnings report. Crucially, while everything discussed in my prior article and above still holds up, there are first signs of fundamental improvements.

As a result, Expedia is poised for significant growth and margin improvement, which is evident in its Q3 record earnings. Despite challenges in the Vrbo platform, the completion of major migrations and the success of the One Key rewards program signal operational strength. Expedia's B2B business is thriving, particularly in China, while B2C, though facing industry changes, shows promising app adoption.

The company's financial health is robust, allowing for substantial share buybacks. In addition, ValueAct's involvement adds a positive dimension to operational enhancements. With a favorable outlook for FY24 and compelling valuation metrics, I upgraded Expedia to a "Strong Buy," anticipating attractive long-term returns.

Expedia is at an inflection point, with growth accelerating and margins improving

Expedia released its Q3 earnings report on November 2 and reported record revenue and EBITDA. Revenue growth accelerated from previous quarters and by 300 basis points sequentially to 9%, resulting in revenue of $3.9 billion. Across the board, Expedia continues to see steady demand for travel, with trends consistent with the last few months. North American and European demand remained stable, with more pronounced growth in APAC and Latin America. Inflation pressures are also easing.

Revenue growth was driven by a 7% growth in gross bookings to $25.7 billion, representing a sequential acceleration. Gross bookings growth mainly came from solid growth in lodging as this was up 8% YoY, driven by 9.5% growth in nights booked. This led to lodging revenue growth of 12%, driven by especially strong booking numbers in the hotel business.

This is especially strong considering the company continued to face headwinds on its Vrbo platform as it was still plagued by the migration of the platform, the recent Maui fires, and the continued softness from the demand shift towards more urban areas.

Positively, these headwinds are expected to ease in upcoming quarters, most importantly driven by the Vrbo migration having been completed last quarter. Despite Expedia completing the acquisition a few years ago, the platform never got adequately integrated into the front-end stack. With this migration now complete, Expedia has completed all significant migrations as part of its multi-year transformation. The company has faced headwinds from these transitions and transformations in the last couple of years. Still, it is now well-positioned to keep accelerating growth without the drag of transformation work that forced the company to go backward in order to go forward.

A crucial aspect of these transformations has been the introduction of One Key. The company introduced its One Key rewards program to increase the platform's attractiveness compared to rival Booking Holdings. This is what I wrote previously:

It unifies all the company's key brands under one loyalty program and allows customers to use "One Key Cash," earned through earlier bookings, across all its platforms and products, including flights, hotels, vacation rentals, car rentals, cruises, and activities. Eventually, this should drive improved customer loyalty as customers can now benefit from the activity in one app through another from the Expedia brands.

This new "One Key" is vital to the company's focus on attracting more customers to their loyalty membership and increasing app usage, boosting their value. Generally, these loyal customers drive higher profits per transaction and higher repeat rates, ultimately leading to higher lifetime value. I believe this is key to the growth prospects of Expedia.

As of Q3, Expedia has already migrated over 82 million members to the program and saw 34% growth in new members over the last year, although the addition of Vrbo supported this. In the travel industry, there is very little brand loyalty. Travelers typically go for the best platform with the broadest offering, focusing on convenience and, crucially, price.

Therefore, the introduction of a loyalty program that includes multiple popular travel brands like Expedia, Hotels.com, and Vrbo, leading to improved convenience and price savings, is the best way to win over customers and fight the competition. Therefore, this move should not be understated, and it should quite quickly be able to add to Expedia's revenue growth.

These are the sorts of financial developments and signs I indicated in the prior article I was looking for. I must admit, I did not expect to see these positive signals this quickly, but I now believe we are at an inflection point in which it seems safe to assume growth will keep accelerating in the coming quarters. We could see the company catching up to Booking, although this will remain challenging.

According to management, it has given up many short-term opportunities over the last few years to get to where it is now, in an operationally much stronger position. Furthermore, management strongly believes it is in a better spot technologically than anyone else, allowing it to return on the offense in the coming years.

Returning to the Q3 result, the company saw incredible strength in its B2B business. For reference, B2B travel accounts for 25% of revenue. The company reported a 26% YoY growth as it continues winning new deals and increasing wallet share with existing partners. Demand from China, in particular, continues to pick up, with Q3 bookings from China Partners up over 150% YoY. Travel activity in this region is still recovering from COVID headwinds, and growth will most likely remain strong here for at least the next 3-4 quarters. This will drive continued strength in B2B overall.

Meanwhile, B2C revenues were up just 4% YoY in Q3. Nevertheless, this is still a growth acceleration of 400 basis points sequentially, including an offset by the softness the company has been facing in its insurance and car businesses due to industry-wide changes post-pandemic. Also worth mentioning is that Expedia, just like Booking, is seeing increased adoption of its apps, with this as a percentage of total bookings up 300 basis points in Q3, contributing to YoY marketing leverage in B2C.

Moving to the bottom line, we can see that the cost of sales was $409 million, down 10% YoY. This allowed for the gross margin to improve to 89.5%, up 210 basis points YoY. Direct sales and marketing expenses in the third quarter were $1.7 billion, up 11% versus the third quarter of 2022 due to increased commissions in the B2B business. Overhead expenses were $617 million, up 9% YoY, resulting from talent and technology investments. However, with Expedia finishing a lot of its technology work this year, these expenses are expected to fall going forward, allowing for margin improvements.

Overall, expense growth sat below revenue growth, leading to a record EBITDA of $1.2 billion, up 13% YoY and reflecting an EBITDA margin approaching 31%, up 110 bps YoY. Adjusted net income was $778 million, up 21% YoY as the margin expanded by 210 basis points to 19.8%. This led to an EPS of $5.41, up 33% YoY.

Finally, Expedia generated a strong $2.3 billion in FCF YTD, and even after taking into account record levels of share buybacks, this still allowed the company to strengthen its balance sheet. It ended the quarter with total cash of $7.6 billion and debt of $6.3 billion, leading to a solid $1.2 billion net cash position and leaving it in excellent financial health with a gross leverage ratio of 2.4x, closing in on management's 2x target. However, with EBITDA expected to grow and improving cash flows allowing for early debt retirements, this goal should be achieved before the end of 2024.

As a result of this excellent financial position, management announced a new $5 billion share repurchase authorization after already buying back stock at record levels YTD. So far this year, management has repurchased $1.8 billion worth of shares, or approximately 17 million shares, leading to a share count reduction of around 10%, which is incredible.

However, this is just the company catching up to significant dilution in recent years. For reference, the share count reached new highs as recently as 2022. Luckily, management is now turning this around with it offsetting COVID-era dilution, bringing the share count back to below 2015 levels. Moreover, as it continues to believe shares remain undervalued, it plans to keep buying back stock opportunistically going forward, using this new authorization, able to reduce another staggering 26% of shares outstanding. This once again confirms the turnaround of this business operationally and confirms an inflection point is here, making me more opportunistic in the company's future.

The involvement of ValueAct is a mentionable positive

The news of activist investor ValueAct now holding a stake in Expedia gave the Expedia share price an additional boost in recent months. In their report, ValueAct speaks of investors seeing an acceleration in growth and margins climbing to their highest levels in a decade for Expedia as a reason for the investment. However, more importantly, unlike most investment firms, ValueAct prefers to work with management behind the scenes to improve operations.

In the past, the company has worked with the likes of Salesforce ( CRM ) and Microsoft ( MSFT ), so the investment firm brings quite some experience to the table, creating enthusiasm among investors, and rightfully so. I have been quite critical of management in my August article, as the company has dropped the ball on many accessions over the last few years, resulting in the company falling further behind its leading peer. Management is now working on steering the ship around, and I remain optimistic. However, I view the addition of ValueAct to work with management as a meaningful positive to boost operational improvements, making the share price jump in response fully justified.

Outlook & Valuation - Is EXPE stock a Buy, Sell, or Hold?

Following the impressive Q3 performance, management reiterated its FY23 outlook and continues to guide for double-digit top-line growth with margin expansion. For Q4, management expects to report gross bookings growth relatively in line with Q3, which is why I believe growth of 8% YoY is a realistic scenario, potentially resulting in gross bookings of $22.15 billion. In addition, management expects revenue and EBITDA growth to accelerate modestly compared to the third quarter. Therefore, I now guide for Q4 revenue and EBITDA growth of 10.1% and 14.4%, respectively. This results in a Q4 guidance of $2.88 billion (revenue) and an EBITDA of $514 million, reflecting an EBITDA margin of 17.9%. As a result, I now guide for EPS of $1.74 in Q4. Note that Q4 has historically been a down quarter for Expedia and peers.

Looking ahead to FY24, management expects to accelerate growth while further improving its margins, which seems likely. According to Evercore analysts , this will be driven by the series of sustainable company initiatives and key developments I laid out in this article. Meanwhile, global leisure travel demand is expected to remain reasonably robust going into 2024, supporting these growth ambitions.

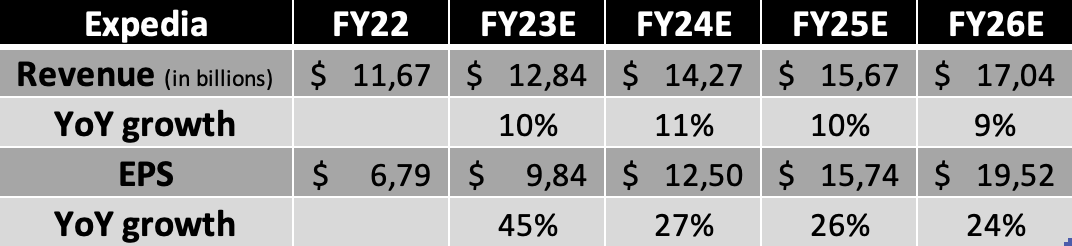

Considering this Q4 and FY24 guidance, the strong Q3 results, and underlying operational developments, I largely stick with my FY23 revenue guidance while upgrading my FY23 EPS expectation. Furthermore, with growth now ready to accelerate, driven by management's initiatives and the company's better competitive positioning, I foresee more robust revenue growth. On top of this, with massive migrations and technology investments now complete, I expect minimal cost growth over the next few years, potentially even some contraction in expenses, leading to significantly stronger margins. In response, I have meaningfully upgraded my EPS outlook, resulting in the following expectations.

Financial projections (Author)

{kind=link}

Based on these estimates, shares now trade at 14.5x this year's earnings, which is a significant discount to peers Booking Holdings and Airbnb ( ABNB ), which trade at 21x and 16x, respectively, reflecting an average discount of 27.5%. This discount becomes even more pronounced when looking at the FY25 earnings multiple, with Expedia trading at just 8.5x FY25 earnings compared to 15x and 27x for Booking and Airbnb, respectively, reflecting an even higher discount of 147%, which is just ridiculous at this point.

Valuation peer comparison (Seeking Alpha)

{kind=link}

However, we should still consider that Airbnb and Booking hold a much stronger market share in their respective travel categories and already report far more impressive margins. Simply put, these are lower-risk options fundamentally compared to Expedia, which still has to prove up to a point that its turnaround efforts will materialize.

However, even when taking this into consideration, the current discount is too much. Considering Expedia's current competitive positioning, its turnaround starting to materialize, and its incredible growth and margin expansion outlook, I believe a multiple of 16-18x much better represents the potential growth and risks involved.

For now, I will stay conservative and will use a 16x multiple combined with my FY24 EPS projection, calculating a target price of $200 per share, leaving an upside of 40% over the next 13 months. Furthermore, using a conservative 14x multiple and my FY25 EPS, I believe that from a current price level of $143, investors are well positioned for annual returns exceeding 20%, easily outperforming global benchmarks.

Therefore, I upgrade my rating on Expedia to a "Strong Buy" from "Hold" and recommend investors ignore the recent share price gains and position themselves for attractive long-term returns. At its current valuation, I believe Expedia is the most attractive travel stock on the market.

For further details see:

Expedia: Currently More Attractive Than Peers (Rating Upgrade)