ABNB - Expedia: Discounted For Good Reasons Yet Potentially Attractive

2023-08-14 13:41:47 ET

Summary

- Expedia Group is a leading global OTA with a diverse portfolio of strong travel brands and a significant market share in the online travel agency sector.

- The medium-term outlook for Expedia looks promising with solid revenue growth and impressive EPS growth.

- Despite its strong position in the travel industry and a discounted share price, I believe Expedia is a high-risk investment.

- Expedia looks to be valued below its fair value, but rightfully so. Despite the discount, I don't believe the risk-reward profile is attractive enough.

- Looking at the travel industry, I believe there are better options available to investors. Paying a premium for Booking or Airbnb makes more sense today.

Investment thesis

I initiate my coverage of Expedia Group, Inc. ( EXPE ) stock with a hold rating following my in-depth analysis of the company and the underlying industry. After my deep dive into the company, my thoughts on Expedia are best summarized as a mixed bag. While there are aspects to get excited over, there are also some serious risks.

Expedia stands as a formidable force in the global travel industry, wielding a diverse portfolio of strong brands that have earned the trust of millions of travelers worldwide. Its significant market share and steady revenue growth underscore its stature in the online travel agency sector. While Expedia has faced challenges, such as shifting market dynamics and margin pressures, its recent efforts to unify loyalty programs and address inefficiencies show promise for future growth.

The company's strategic initiatives, like the rollout of the "One Key" rewards program and technology enhancements, reflect a commitment to enhancing customer loyalty and engagement. Expedia's focus on cost savings and margin improvement is a positive step toward addressing its historical margin fluctuations, even though it faces competitive pressures from industry peers like Booking ( BKNG ) and Airbnb ( ABNB ).

The path ahead is not without obstacles. Intensified competition and the need for stronger leadership raises concerns about Expedia's ability to outpace its rivals. Furthermore, management's track record of shareholder dilution and margin challenges must be closely monitored.

In the dynamic world of online travel, Expedia's resilience and adaptability, coupled with its strategic initiatives, position it to capture a share of the growing market. While the road may be bumpy, the company's efforts to enhance customer loyalty, improve margins, and drive efficiencies may offer a path to sustained growth. With a cautiously optimistic outlook, investors should keep a watchful eye on Expedia's performance as it navigates both challenges and opportunities in the ever-evolving travel landscape.

In this article, I will take you through the company’s fundamentals, latest developments, and financial health to determine whether the company is an interesting investment today.

Expedia is an understated giant in travel with a strong service offering and strong brands

Expedia Group is a leading global OTA (Online Travel Agency) present in over 70 countries through 200 travel websites. The company operates a comprehensive portfolio of online travel brands, providing a wide range of services to millions of travelers worldwide. Expedia’s extensive brand portfolio includes some of the most recognized names in travel, such as Expedia, Hotels.com, Orbitz, Travelocity, Hotwire, Vrbo, and more. These brands collectively cater to a diverse spectrum of travelers and give the company a very strong foothold in the travel industry as it holds a significant market share in the global online travel booking industry of 26.4% and 42% in the US market (please note that this includes all brands from Expedia Group, including Expedia, Hotels.com, Vrbo, Trivago, etc).

This makes the company one of the leading players in the traveling industry, putting it only slightly behind Booking Holdings and ahead of Airbnb. Furthermore, the company has even been gaining share over the last year as it gained a 3% market share over the past year, primarily at the cost of rival Airbnb, which saw its market share fall by 3%.

{kind=link}

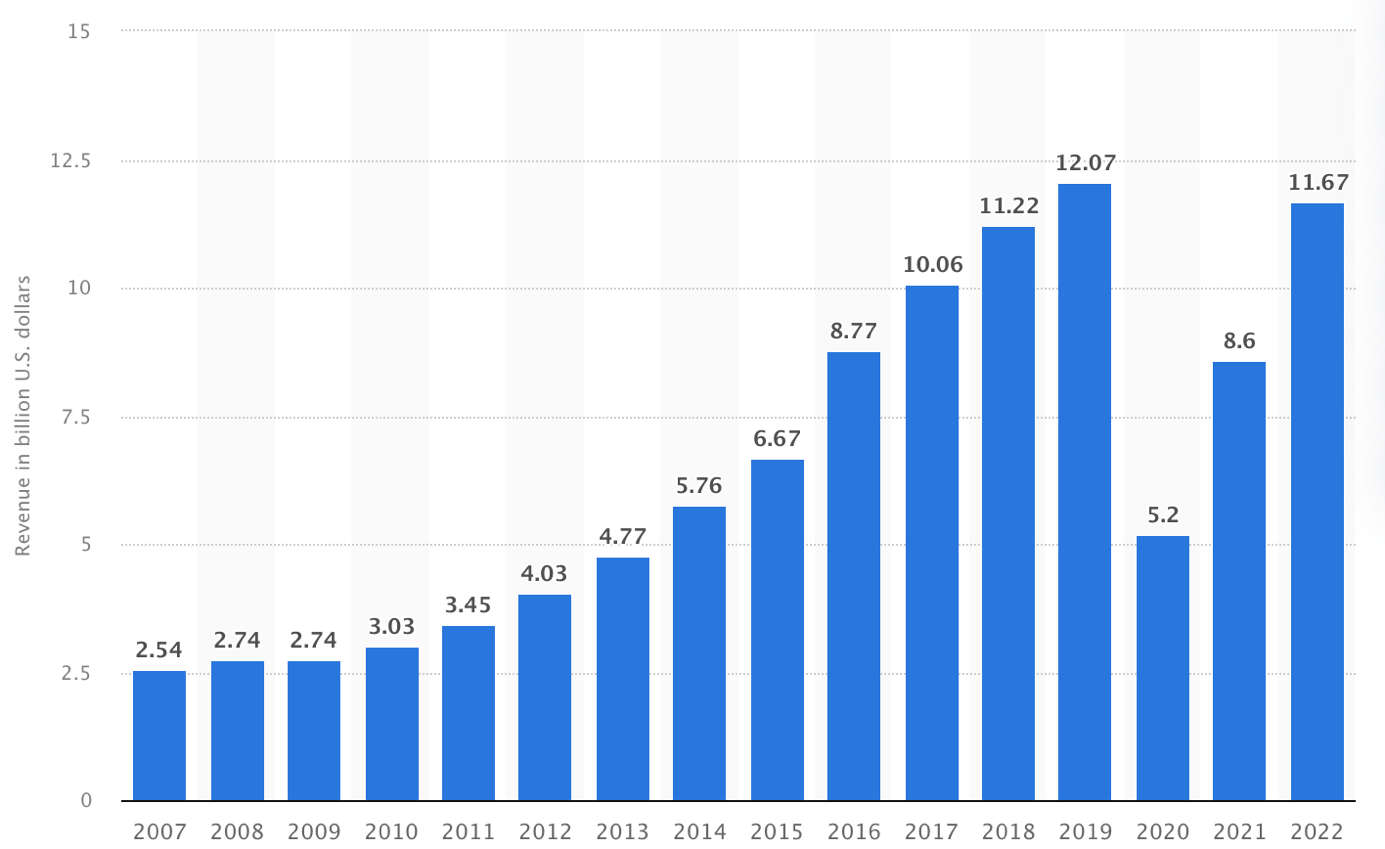

The strong market position of the company and its excellent travel services offerings have already massively benefitted the company over the last decade as well, with it growing its revenue at a stellar 11% CAGR from 2012 to 2022.

{kind=link}

Meanwhile, the online travel booking service industry is expected to keep growing at a 9% CAGR through 2030, driven by the growing influence of social media, increasing disposable income, and rising inclination toward adventure travel across the globe. For the US region, to which Expedia has the most exposure as highlighted earlier, the CAGR growth is expected to sit around 8.4%, which should drive meaningful growth for Expedia as well. The company should be well-positioned to benefit from this growth, although I am somewhat cautious regarding its growth outlook as, crucially, the CEO back in 2021 indicated that the company might start losing share in North America and appeared to blame this on the shift to lower-priced and lower-star hotels due to covid and record inflation levels. Expedia has historically been much less exposed to these lower-star hotels, and if this market grows faster, this could lead to market share losses for Expedia. So far this has not materialized, but it's important to keep a close eye on this.

On the contrary, investment firm B. Riley Securities recently stated that they see Expedia taking market share over the next several years as its service/product offering should position it favorably. Expedia has a solid portfolio of travel brands, which gives it good exposure to the broad travel industry and allows it to compete with Booking (primarily through Expedia and Hotels.com) and Airbnb (primarily through Vrbo). Also, these brands have a strong user base that will likely remain as the brands inspire confidence. From this standpoint, I can see where the B. Riley Securities analysts come from regarding the market share gains.

The company should be looking over the shoulder of Booking Holdings on how it could become the one-stop shop for everything that is travel. Currently, the company’s offering is spread out too much, and synergies are missing, creating a less practical customer experience. Yet, simultaneously, its over three million property listings , 220,000 unique activities, and 500+ cruise lines, airlines, and car rentals give it incredible exposure and an overall travel offering that is hard to match.

Expedia Group brands (Expedia)

{kind=link}

I can see Expedia gaining market share over the next several years, but this will be challenging with Airbnb and Booking also increasing their efforts and OTA’s barely having a moat at all. Apart from a convenient platform with a broad offering, there is not much an OTA can do to increase its competitive position. It is all about customer satisfaction and possibly driving customer savings through loyalty programs. The company owns no properties and entirely depends on suppliers offering their properties on the Expedia platforms, increasing overall risks. A company dependent on suppliers with a bunch of other platforms to supply to, is not ideal.

This should be considered as a very fragile moat or competitive advantage. Honestly, if I look for a hotel to stay in, there is very little between the leading platforms in the US. Therefore, I chose to take a neutral stance here and expect its market share to remain relatively stable. This should still ensure it to fully benefit from the strong industry outlook. Yet, there are several promising efforts by management that could boost future growth, which I will discuss later.

Margins are a problem, but this does not have to be structural

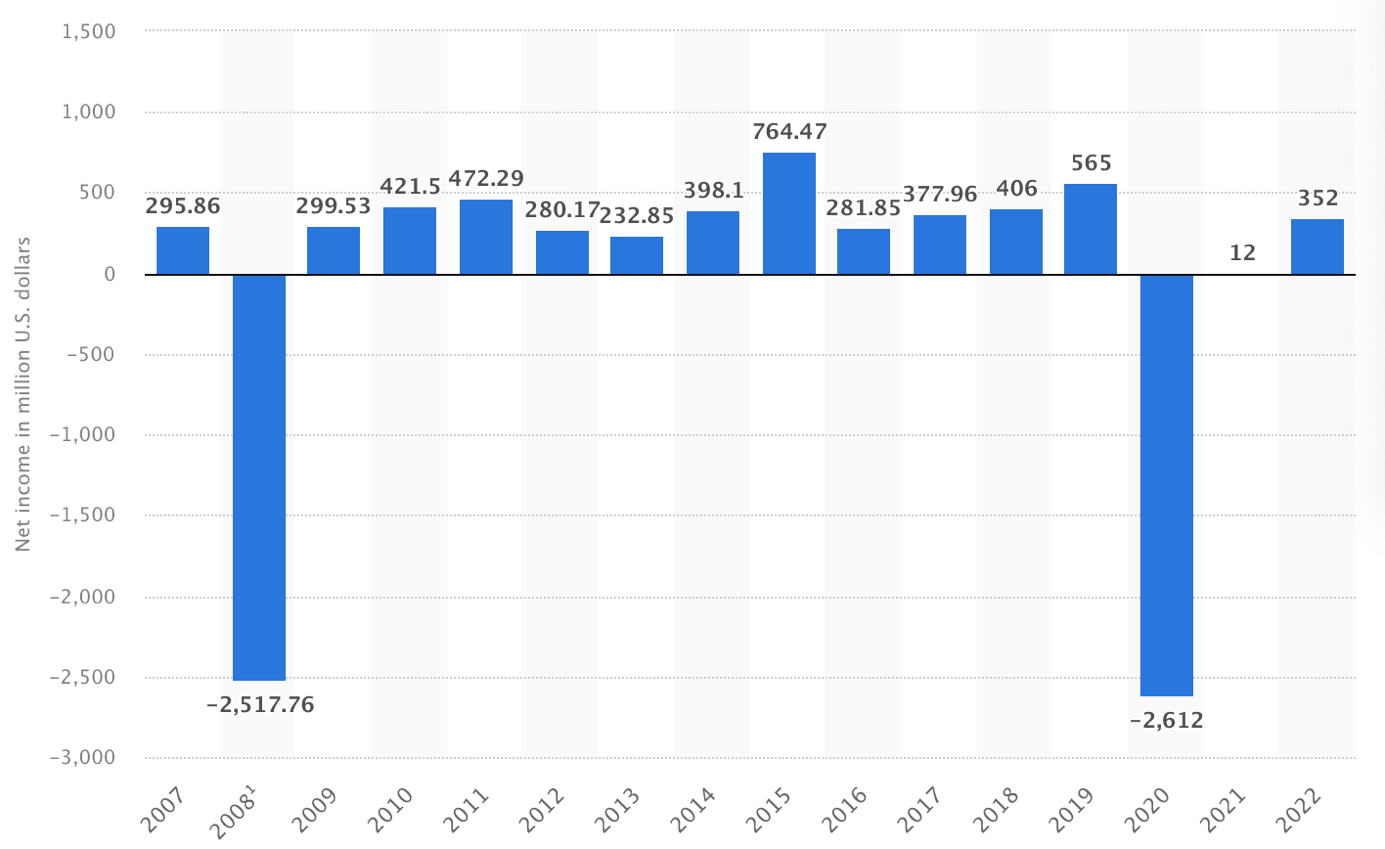

On a more negative note, while the company has been showing incredible growth over the past decade or so with this almost tripling, its share price has only risen by around 125% over the last decade, underperforming the SPY. The main reason is the company’s margin profile, which has not always been as stable and growing. Remarkably, over the 2012-2022 period, net income has grown at a very meager CAGR of 2.26%, far below its revenue growth. The graph below, which shows its net income development, is full of ups and downs, some of which can be easily explained, but the overall picture remains the same: the margins are far below its leading peers and are very inconsistent.

{kind=link}

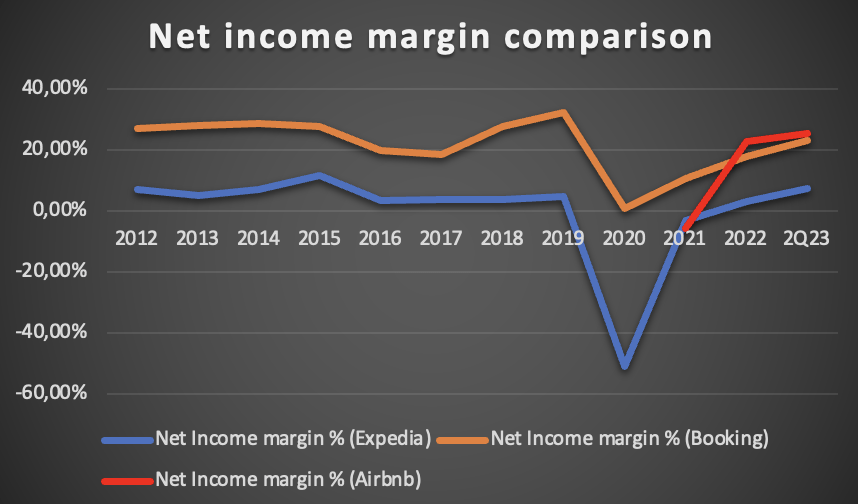

This is partly driven by the fact that the company has been unable to expand its margins over the last decade. Last quarter, the net income margin was approximately the same level as in 2012.

Net income margin peer comparison (By Author)

{kind=link}

This shows how the company has been struggling over the last decade. This can be attributed to the incredible cyclicality of the travel industry, which is highly correlated with the levels of consumer disposable income. The industry fluctuations, therefore, cause fluctuations in margins. This is also visible in the margins of Booking Holdings, which shows a very similar profile.

Yet, while these are industry-wide trends, this does not take away that Expedia’s margins sit structurally below that of its closest and larger peer, Booking Holdings, which reports margins closer to or above 20% compared to Expedia’s decade average of 3.5%. Several factors contributed to this margin gap, but I believe the most important is a management team that appears to lack conviction and has simply been sleeping on the margin problem for over a decade. As a result, a large part of the revenue gap between the two can be attributed to inefficiencies for Expedia. For example, while Expedia’s revenue sits at 68% of Booking’s 2022 revenue, its employee count as of the end of 2022 sat at 76%, indicating that revenue per employee for Booking is more favorable. Both companies offer similar services, but it seems Expedia still has some ground to gain here.

Furthermore, Expedia operates every single one of its travel brands as a separate platform. In contrast, Booking uses a “one-stack enterprise” strategy, meaning they primarily only need one tech platform to market hotels. This allowed for several cost savings and a more simplified marketing strategy, again allowing for improved efficiencies, something Expedia is unable to match.

That the company has been dropping the ball on the “one-stack enterprise” strategy is perfectly highlighted by the fact that its rental subsidiary, Vrbo, which it acquired a long time ago, has never been properly integrated into its travel offering and tech stack. The company has only recently started integrating the business properly, which could lead to further cost efficiencies but also brings with it several integration risks.

At the same time, factors that are more fundamental in nature drive these lower margins, like the fact that Expedia traditionally focused on offering lower-margin travel products like flights and business-to-business services, which negatively affected its margins. Now that Booking is expanding its offering to other travel verticals like flights, the margin gap is expected to close somewhat over the next few years. So, this explains part of the problem. Also part of the lower margins for Expedia is the lower take rates (11% versus 16% for Booking in pre-covid 2019), which are essentially the result of Expedia’s focus on the US market where take rates are lower compared to Booking’s largest region, Europe.

So, in short, the entire margin gap compared to Booking is definitely not due to “bad” management over the last decade as a part is due to fundamental business decisions and focus areas. With Booking now also increasing its efforts to create the one-stop shop for everything that is travel and focusing on the US market, the margin gap is expected to close somewhat, which could put Expedia in a better light, allowing it to trade at a slightly higher valuation. In addition, it has recently realized that it can and needs to address these margin issues and inefficiencies, which is positive and could bode well for the future. Of course, these issues discussed previously are not unsolvable problems.

The company has even started to address these issues as it has for a while been working on unifying all of its rewards programs under "One Key", which has been launched in the US recently and this should also lead to increased efficiencies and is a solid first step. Furthermore, Expedia has already lowered fixed costs by $700 to $750 million annually and a further $200 million in variable costs since the COVID-19 pandemic, showing that management is finally focusing on the margins and cost savings.

Besides driving more significant EPS growth and demanding a higher valuation, these potential margin improvements are also crucial to the long-term growth thesis. If the business is able to generate more cash like its peers Airbnb and Booking, it has more extensive financial capabilities to invest in growth, market share gains, and rewarding its shareholders. Enough reason for management to up its efforts and enough reason for shareholders to keep a close eye on this.

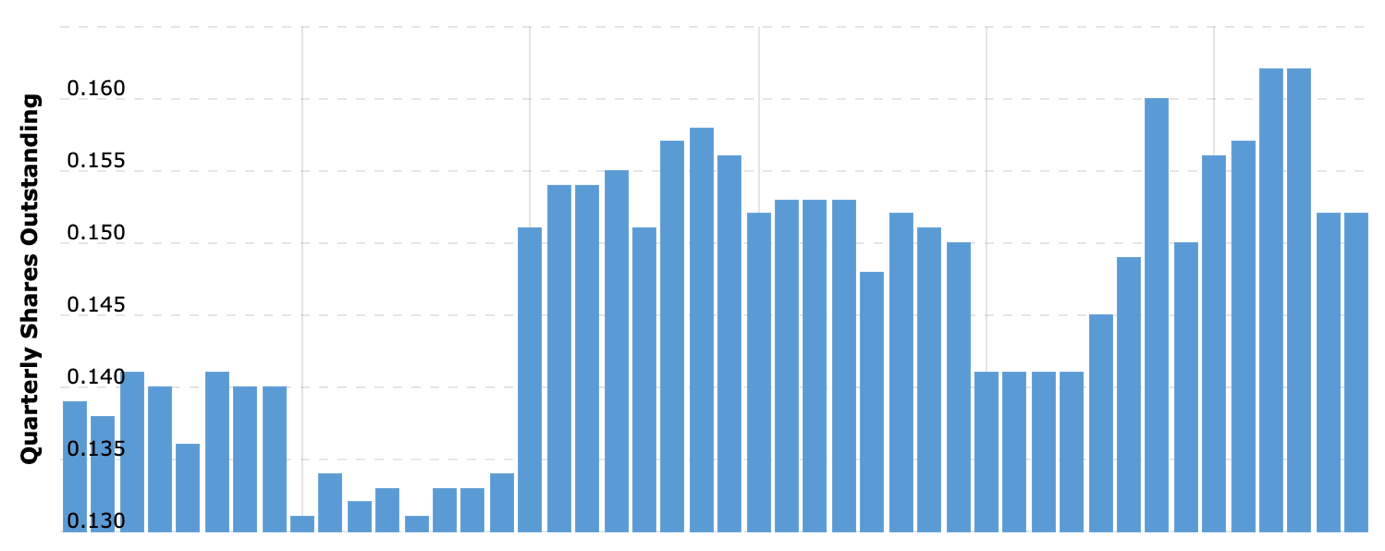

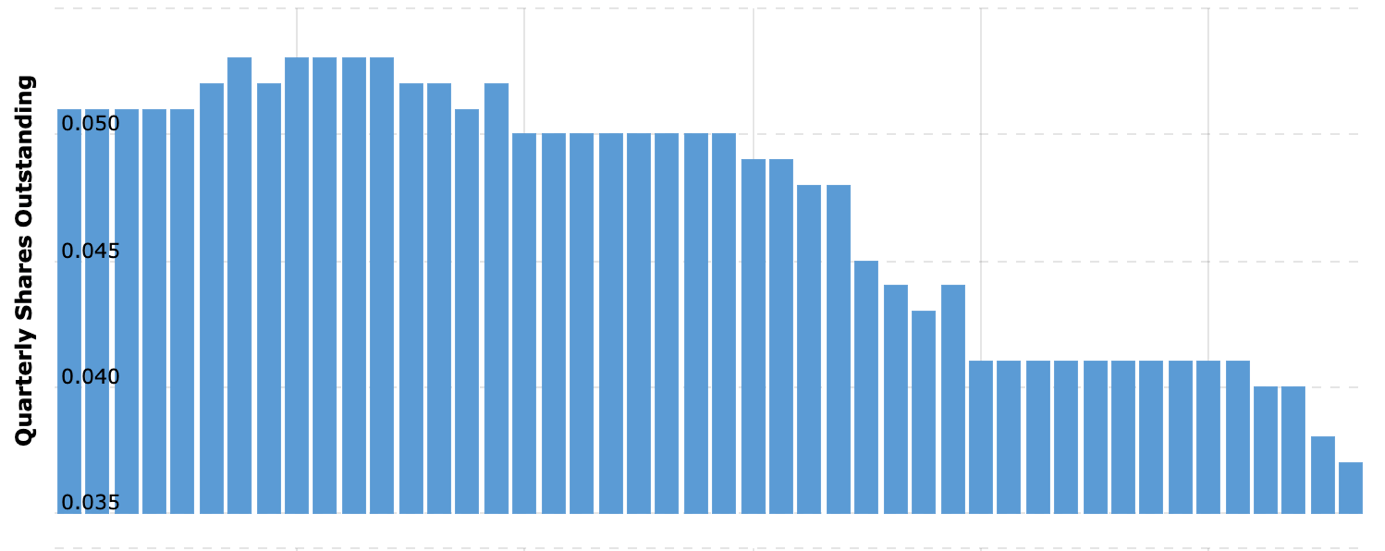

On the note of rewarding shareholders, the company has been attempting to do this over the last several years but has completely failed. It has been buying back shares but, at the same time, has consistently been diluting shareholders, resulting in a breakeven result. The number of outstanding shares is currently higher compared to the start of 2012 and while the company has repurchased $6.4 billion in shares, or around 40% of its current market cap, over the last 1.5 years, the number of outstanding shares has actually risen since.

Expedia share count (Macrotrends)

{kind=link}

This should give you an idea of how it is diluting its shareholders while draining its cash balance, cash that could be invested in technological development to boost long-term cost savings. For comparison, rival Booking has lowered its share count by over 27% over the same period of time, making it much more shareholder-friendly in my view. Which would you pick based on this? Easy decision, right?

Booking share count (Macrotrends)

{kind=link}

It is incredibly disappointing to see this kind of dilution from Expedia and a reason for shareholders to stay far away from the company. The company is solid, but the way it is managed is up for discussion, to say the least.

Luckily, the company remains in excellent financial health. It still holds a total cash position of $6.3 billion, up from $5.6 one year ago and roughly in line with its long-term debt of $6.3 billion.

There are also aspects and efforts to get excited over and the recently reported Q2 performance was solid

Earlier I mentioned that Expedia has started the roll-out of its “One Key” solution in the US, which is the company’s new rewards program. It unifies all the company’s key brands under one loyalty program and allows customers to use “One Key Cash”, earned through earlier bookings, across all its platforms and products, including flights, hotels, vacation rentals, car rentals, cruises, and activities. This eventually should drive improved customer loyalty as customers can now benefit from the activity in one app through another app from the Expedia brands

This new “One Key” is vital to the company’s focus on attracting more customers to their loyalty membership and increasing app usage, boosting their value. Generally, these loyalty customers drive higher profits per transaction and higher repeat rates, ultimately leading to higher lifetime value. I believe this is key to the growth prospects of Expedia.

The execution of this strategy has proven to be strong in Q2 as the number of loyalty members hit new highs, growing 15% YoY. Furthermore, the percentage of bookings made through the company’s apps also increased by 300 basis points sequentially. These developments are incredibly promising and are crucial to Booking maintaining its market share and boosting long-term growth stability. This solidifies my belief that Expedia should be able to maintain its market share over the longer term.

Expedia reported its Q2 earnings on August 3 and saw revenue come in roughly in line with the consensus, while EPS came in $0.53 or 22% above the average Wall Street estimate . Expedia continued to see robust travel demand as growth was driven by all regions, although growth in APAC and Latin America was much stronger due to an easier comparable quarter from last year when the US and Europe were already fully recovered from the COVID-19 lockdown effects.

Gross bookings in Q2 were up 5% to $27.3 billion, in line with management’s guidance but far below the growth reported by peers Booking and Airbnb, which reported gross bookings growth of 15% and 12%, respectively. For Expedia, this drove revenue up 6% YoY to $3.4 billion, driven by strength in the lodging business, which saw revenue grow by 12%. This revenue number does include a 170 basis points negative impact from FX.

Driven by cost-saving initiatives, Expedia delivered a record second-quarter EBITDA of $747 million, up 15% YoY and reflecting a margin of 22.2%, up 190 basis points YoY. While EBITDA came in at a record high, FX still impacted this, which resulted in a negative impact of 530 basis points. The improved cost efficiencies and higher revenue basis also led to an improvement in the net income margin from a negative number last year to 4.1% in the first half of this year. Of course, this is still not a level to cheer about but it does sit above the average percentage from the last decade. Also, the margin improved especially strongly in the second quarter, reaching 7.3%, driving the adjusted net income up 38% YoY. This caused a significant increase in adjusted EPS, which came in at $2.89, up 48% YoY. Finally, the improved EBITDA and net income margin also resulted in a strong free cash flow of $3.8 billion year-to-date. The company remains very well able to generate significant cash flows.

Outlook & EXPE stock valuation

Expedia is guiding for Q3 gross bookings growth to accelerate from Q2 and to show high single digits growth, driven by solid growth in hotel bookings but partially offset by Vrbo, which is still facing short-term headwinds from its integration and the lesser demand for longer-term and rural stays. Still, this should bring gross bookings to $26 billion, representing a growth rate of 8.5%.

Revenue growth in Q3 is expected to come in below the expected growth for gross bookings as reduced Vrbo bookings are converted to stays, which impacts the historically highest revenue quarter for the travel platform. Therefore, revenue is only expected to grow modestly sequentially. I expect Expedia to report revenue of $3.8 billion, up 5.6% YoY. Yet, it is crucial to note that this is largely driven by the Vrbo migration, so this should be fine for Expedia going forward.

Expedia reiterated the FY23 outlook from earlier this year and continues to expect double-digit top-line growth mostly driven by a strong second half of the year and particularly a strong acceleration in growth in Q4 as the Vrbo migration finishes and the impact of the One Key kicks in. Management also continues to expect margin expansion despite the EBITDA margin being expected to stay relatively in line with last year.

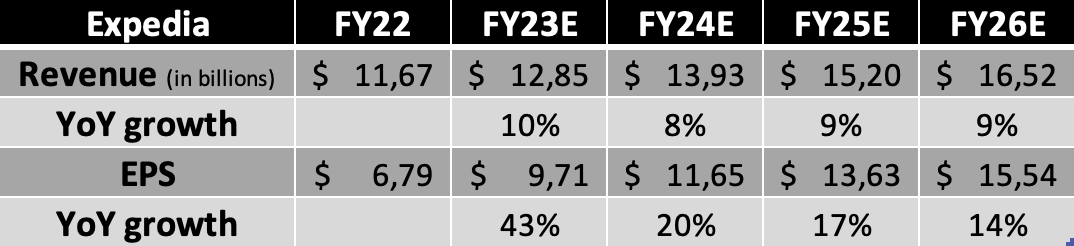

Following this guidance, the Q2 financial results, and my analysis of the company fundamentals, I now expect the following financial results through FY26.

Financial estimates (By Author)

{kind=link}

(These estimates include Q3 revenue of $3.8 billion and EPS of $5.08)

Shortly explaining these estimates, I expect Expedia to report FY23 revenue growth of 10%, driven by a growth acceleration in the second quarter, especially in Q4 as the Vrbo integration is expected to be completed by then, allowing for more pronounced revenue growth. Meanwhile, EPS should continue to grow rapidly YoY in the second half of the year due to an easy comparison to the negative EPS reported in FY22 and Expedia increasingly focusing on cost-savings and driving efficiencies in its business. I project FY23 EPS to grow 43% YoY.

For the following years, I expect Expedia to grow roughly in line with the projected growth for the online travel booking industry as I expect Expedia to keep its market share roughly flat overall. While there are several initiatives by management that could very well boost its attractiveness to consumers and the company remaining the leader in B2B travel services, I also see plenty of headwinds and increased competition from the likes of Airbnb and Booking Holdings, which, in my eyes are in a better position from a fundamental and industry growth standpoint. I believe that going with a neutral market share development is fair for the quality business of Expedia, which, as stated before, continues to have strong and broad exposure to the entire travel industry through its well-known travel brands.

As for my long-term EPS expectations, I believe Expedia will be able to grow this at an industry-leading pace as there is a lot of room for margin and efficiency improvements, which seems to finally be acknowledged by the management team. I expect Expedia to improve margins over the next several years, mainly by finding synergies between its businesses and brands. Continued share buybacks could also contribute to this, but only if the company stops diluting its shareholders. As this has so far not been the case, I have not included any benefits of a lower share count in these estimates. Still, the margin improvements will drive very strong EPS growth by itself.

Moving to the valuation, I believe this is quite a tough one for Expedia. While I like the company’s collection of travel brands and its broad exposure to the travel industry, which should ensure that it fully benefits from the expected growth in the industry over the remainder of the decade, there are several fundamental negatives that make me somewhat hesitant when it comes to determining its fair value. For example, Expedia’s management team really needed some changes to allow the company to move forward, in my humble opinion.

I believe the management team has shown over the last decade that it has been unable to develop the company in the right direction from a financial perspective. Positively, in the last several years under a new CEO and CFO (in their respective positions from 2020 and 2019, respectively) the company has been developing in the right direction, yet I need clear improvements in the company’s financial position to allow for an improved valuation multiple.

Furthermore, Booking Holdings and Airbnb are fundamentally better positioned to take market share and grow at a faster pace, making it hard to award Expedia a valuation multiple that suits its growth outlook. Right now, I see a large number of negatives that could very well be addressed over the next several years, but I will first need to see if these changes and policies have a positive effect on its reported financials before I will incorporate these into its valuation. Right now, the stronger competition, weak financial position (compared to peers), and questionable management (look at the shareholder dilution despite throwing large amounts of cash at share repurchases) demand a discounted valuation.

Considering the current valuations of its peers, Booking and Airbnb, which are valued at a forward P/E of 21x and 36x, respectively, I believe the current forward P/E of 11.5x is not far from its fair value. For now, I will award the company a P/E of 12x as this seems to allow for a sufficient margin of safety while ensuring solid long-term returns based on the current growth outlook.

Based on this belief and my FY24 EPS estimate, I calculate a target price of $140, leaving an upside of 25.44% from a current share price of around $111. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes).

Conclusion

My ideas on Expedia after my deep dive into the company are best summarized as a mixed bag. While there are aspects to get excited over, there are also clearly a number of serious risks. And while there have been some positive developments over the last couple of years, I believe investors have to give the company and its management team some more time to see this reflected in its financials through margin improvements and a more efficient business model that allows the company to move forward and strengthen its market position further.

Today, I view the company as inferior to its larger (in market cap) peers in terms of technology, customer experience, and long-term growth initiatives, significantly increasing the risk profile. Therefore, I chose to take a careful stance toward the company and value it at a significant discount to its peers to create a more pronounced margin of safety.

Based on my target price and going with an annual return of 10%, its current fair share price sits at around $121, leaving an upside of 8.42%. This means the company is currently valued below fair value, even when using very conservative valuation multiples.

And yet, I am still rating this one a hold for now. I simply see too many fundamental risks and am looking for significant improvements in its financial position and a successful migration of Vrbo by the end of the year. Considering all that I have discussed throughout this article, I believe investors are better off paying a premium for a higher-quality business like either Airbnb or Booking Holdings. Until the company is able to show steady and consistent improvements, I remain on the sidelines.

For further details see:

Expedia: Discounted For Good Reasons, Yet Potentially Attractive