BKNG - Expedia Is A Better Buy Than Airbnb

2024-01-14 23:49:52 ET

Summary

- Airbnb's financials have shown robust growth despite the challenges of the pandemic, outpacing travel peers.

- Competitors like Expedia's VRBO are making moves to challenge Airbnb's dominance in the vacation rental market.

- VRBO enjoys a number of advantages, including EXPE's massive organic traffic network, ad budget, and One Key rewards program.

- For the potentially improved growth and margin profile possible from VRBO IRR, EXPE is well priced.

- We rate EXPE a "Strong Buy".

Airbnb ( ABNB ) is one of the most impressive companies that has gone public over the last few years.

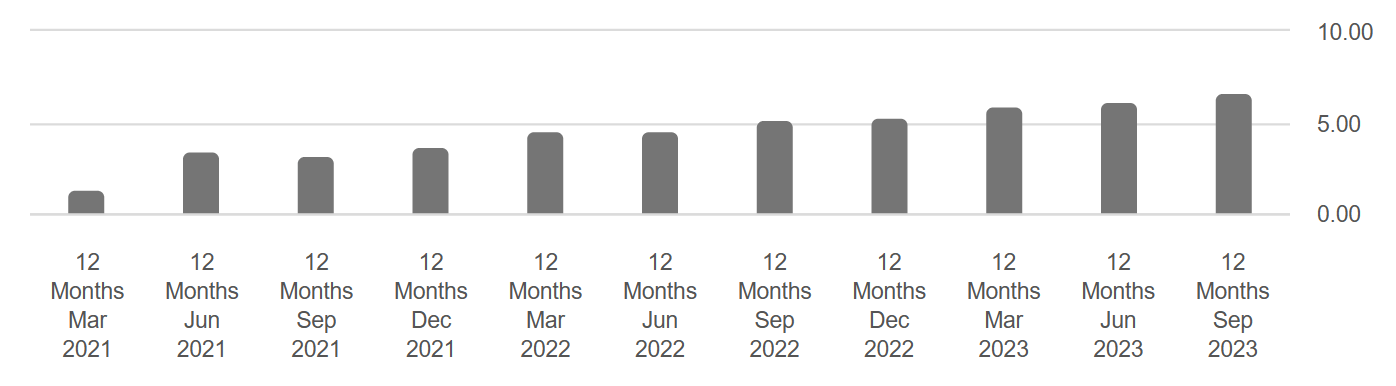

Financials have been robust, with top line sales growth of more than 3x since 2017, even when taking into account Covid, which acted as a massive headwind for the entire travel industry. TTM FCF per share has also kept pace, reaching new highs quarter after quarter like clockwork:

{kind=link}

However, despite this massive growth, the stock is mostly unchanged from its IPO price.

Strengthening financials have been offset by a falling multiple, and as a result, the stock has remained mostly rangebound, between $100 and $150 for the last year or so.

There's no question that the stock is a better 'deal' right now than when it first IPO'd in 2021.

However, competitors have begun to make moves against the company, attempting to take share away from Airbnb's massive lead in the 'vacation rental by owner' category.

Expedia ( EXPE ), with its growing VRBO brand, is one such competitor. As a more mature company with a much stronger organic traffic profile and a more well-diversified business model, is Airbnb really the name to own in the space?

Today, we'll be taking a look at Expedia - and its insurgent VRBO brand - to explain why the stock is well-positioned for future growth and margin expansion. Plus, most importantly, we'll highlight why the stock looks highly attractive at its current valuation.

Sound good?

Let's dive in.

Sizing Up The Incumbent

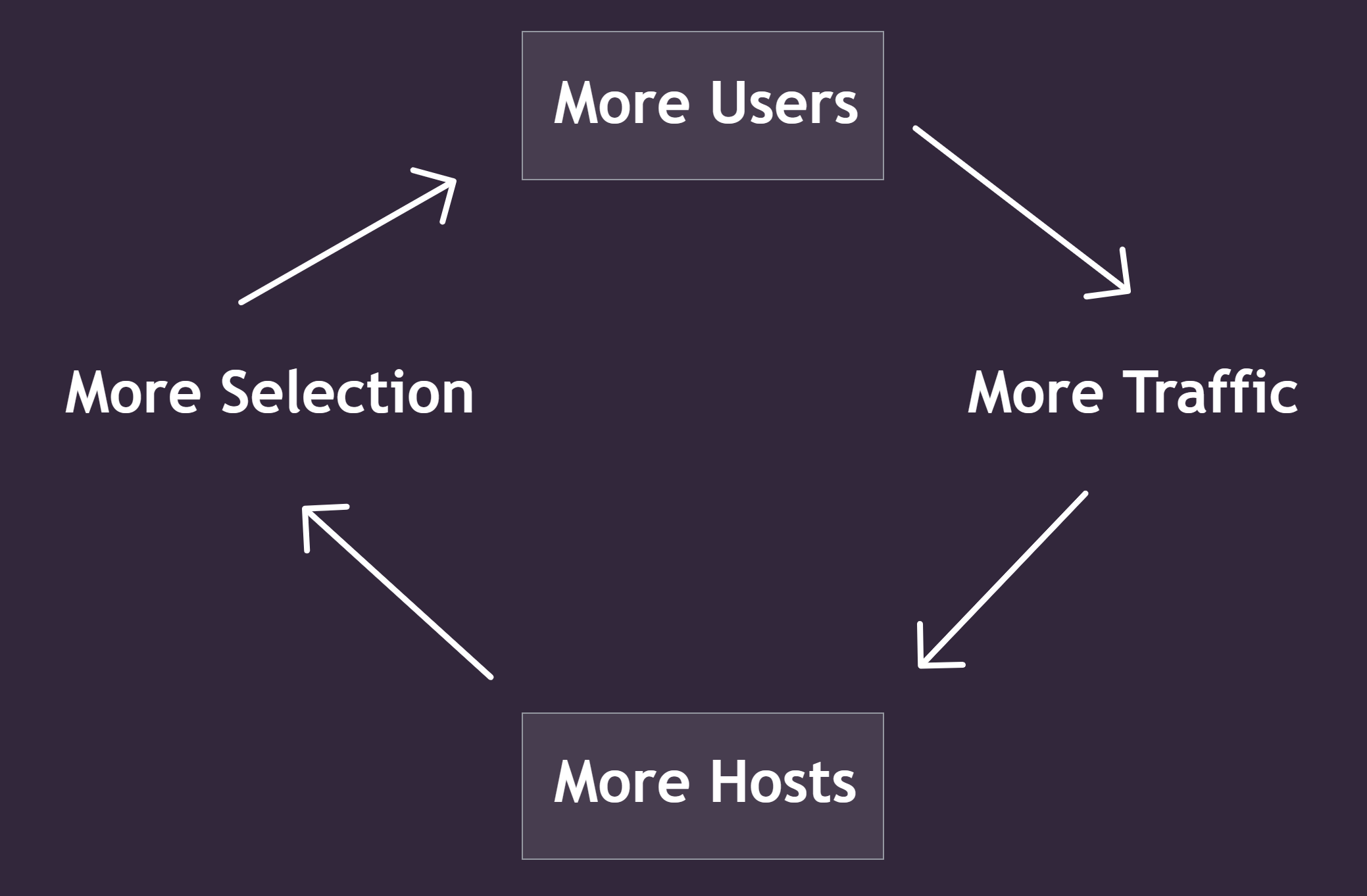

For its part, Airbnb is actually a fairly easy-to-understand company. At its core, ABNB is a technology firm that provides a platform where property owners can list their properties for short & mid-term rentals. It's a classic marketplace flywheel business, like Amazon ( AMZN ) or Etsy ( ETSY ):

{kind=link}

As users begin to browse the site, more hosts are attracted to the platform, and thus selection improves. Then, more users arrive in search of a better product, which attracts more hosts, and so on. The hard part about a business like this is getting it 'going', but once it's up and running, it can be hard to stop.

The platform has become so popular that it has attracted scrutiny from regulators, a hallmark of other disruptors like Uber ( UBER ).

But how does ABNB make any money off of this?

In short, it takes a cut from each transaction on the platform.

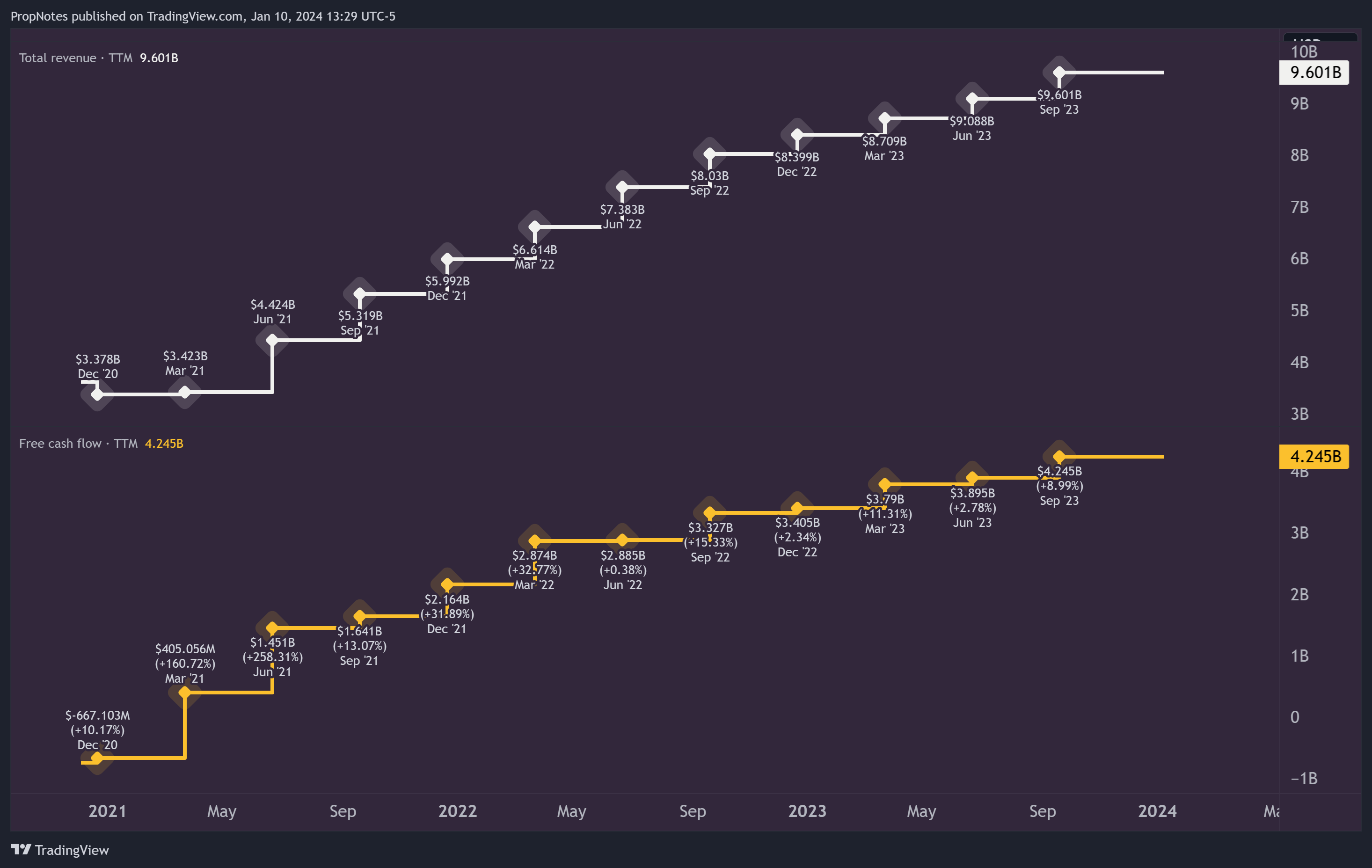

As more users and hosts have come to the platform, total gross bookings have risen, along with corporate revenues and profits:

{kind=link}

ABNB's business has a very high margin, as you can see above, which is highly attractive from an operational leverage standpoint. This is partially why the company did so well during Covid, when other travel operators were shutting down or going out of business due to a higher fixed cost base.

Additionally, the company earns a solid EBT, despite having high SBC numbers.

All in all, it's a well-run company.

But how can they grow from here? Right now, CEO Brian Chesky sees the majority of the issue on the supply side. There's significant demand from users who want to book on the site, but there are some supply limitations, as supply growth has lagged.

This is the equivalent of Uber not having enough drivers to service demand - it's a problem that reduces utility on one half of the flywheel.

Long term, management sees supply growth as a leading indicator for overall platform growth:

I'll just say that like this is my intuition having done this for almost 16 years of my life. I think that supply is even more important than it seems on the surface. Ultimately, when you're tiny and no one ever hears about you, one of the big levers is awareness. But once you're a brand like Airbnb that's known as really [indiscernible] used all over the world, so supply growth becomes a very important long-term leading indicator.

However, the company is keenly aware of this fact, and has been taking steps to address it:

We have added nearly 1 million active listings this year. Our supply grew 19% in Q3 compared to a year ago. We once again saw double-digit supply growth across all regions with the highest growth in regions with the highest demand.

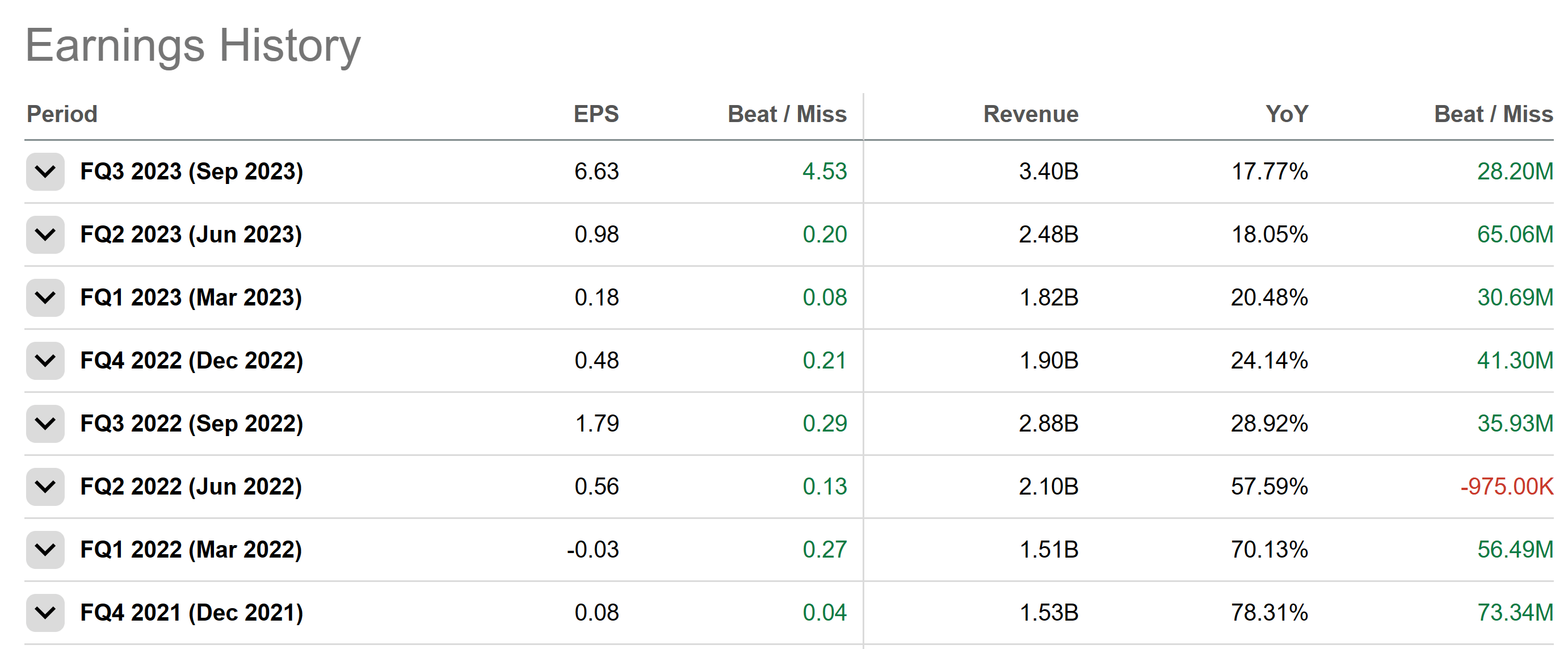

On the flip side, growth has been slowing when viewed from a more macro lens. From Q4 2021 through Q3 2023, top line YoY growth has slowed from 78% to a more modest 17%:

{kind=link}

While this is partially due to a bounce back from Covid, top line growth has slowed from Q3 2022 by more than 1000 basis points - YoY measurements that remain mostly unaffected by travel bans or restrictions.

The main takeaways here for Expedia are threefold:

- The rewards for owning a platform flywheel are robust, and very high margin.

- Promotion / awareness is the short-term growth driver, and supply growth is the long-term growth driver.

- Their main competitor, Airbnb, is seeing slowing growth as it scales.

{kind=link}

Add all these up, and EXPE has a serious opportunity with its VRBO brand.

Expedia's Advantage

While ABNB is a straightforward platform business, EXPE is a little more complicated.

The company operates a number of online travel media properties, like Expedia, Travelocity, Hotels.com, Trivago, and more.

Most of the properties function as essentially a traffic middleman, where they offer price aggregation services, rewards programs, and a cohesive booking experience to attract travelers to their sites.

In return for directing customers their way, Hotels, Airlines, Cruise lines, Car rental companies, and other travel services providers will pay EXPE a cut for the engaged leads.

This is in addition to VRBO, which is a more straightforward platform business, highly similar to Airbnb.

In our eyes, EXPE has some serious advantages worth considering.

First off, the company is a traffic machine, fully integrated into the 'top of funnel' search monopoly that is Google:

{kind=link}

On top of that, EXPE properties generate a tremendous amount of organic traffic from excellent SEO optimization over the years:

| Site |

| December 2023 Organic Traffic |

| Expedia.com |

| 35.3 million |

| Hotels.com |

| 47.7 million |

| VRBO.com |

| 8.1 million |

| Travelocity |

| 7.3 million |

| Hotwire |

| 1.7 million |

| Orbitz |

| 3.9 million |

| Trivago |

| 4.3 million |

| Total: |

| ~108 million |

| Source: Ahrefs |

This dwarfs Airbnb's organic SEO traffic of 19.6 million in December 2023.

To round it out, the company has a considerable marketing budget ($1.8 billion last quarter) that it uses to attract leads at the starting point of their travels/journeys.

To retain users, they also recently launched a "One Key" rewards program, which is valid across all of their properties and begins to introduce a solid moat effect. As EXPE attracts users once, they become the go-to option for customers the next time they're looking to travel, without the upfront acquisition cost.

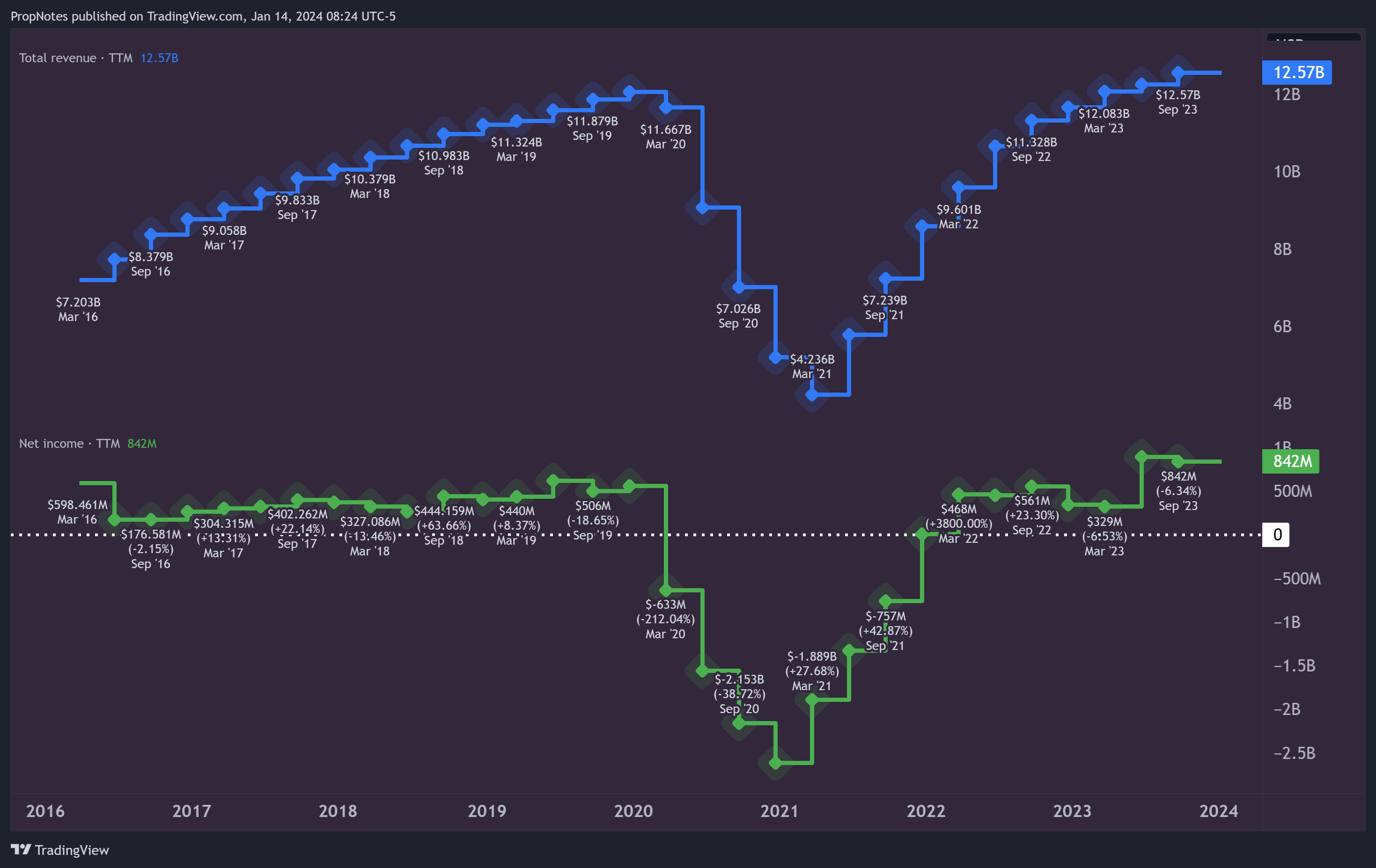

All of these efforts have built up EXPE into a travel industry behemoth, a company that does more than TTM $12.5 billion in sales:

{kind=link}

However, as you can see, the company has a much weaker margin profile than ABNB, keeping far less income for shareholders on a larger base of revenue.

Thus, the growth of VRBO has the ability here to materially improve financials, due to the inherent margin profile and growth opportunity present in that business.

Why do we think this is possible? In short, EXPE has an already-established traffic machine that it can use to boost the platform.

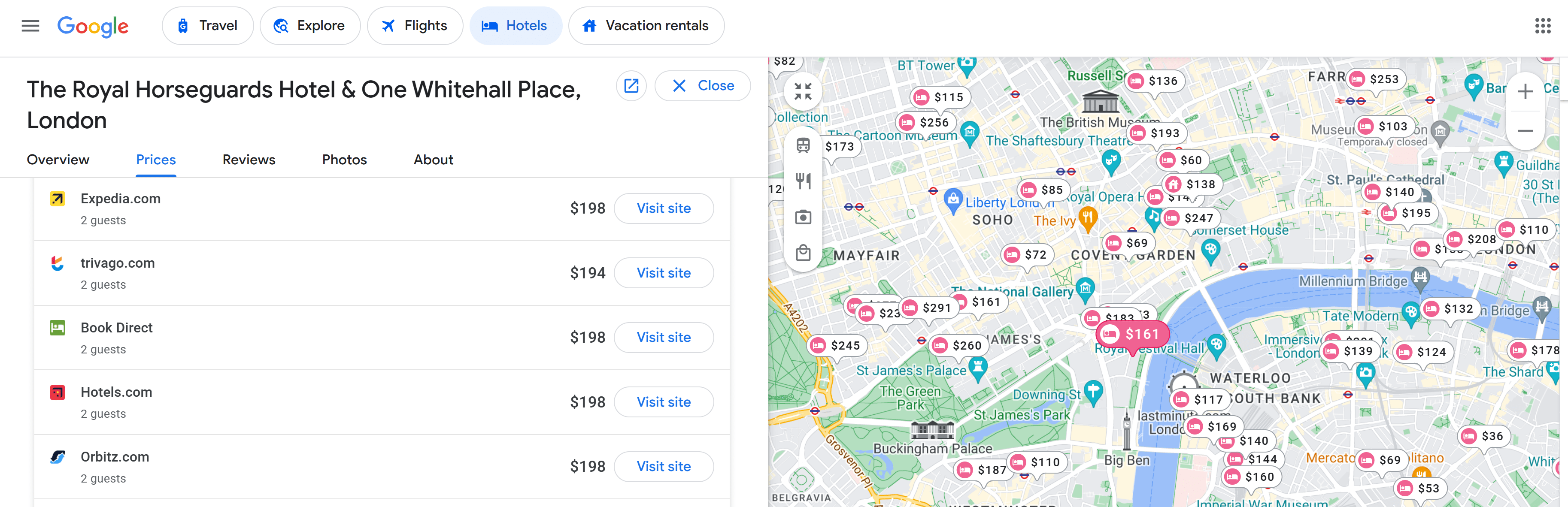

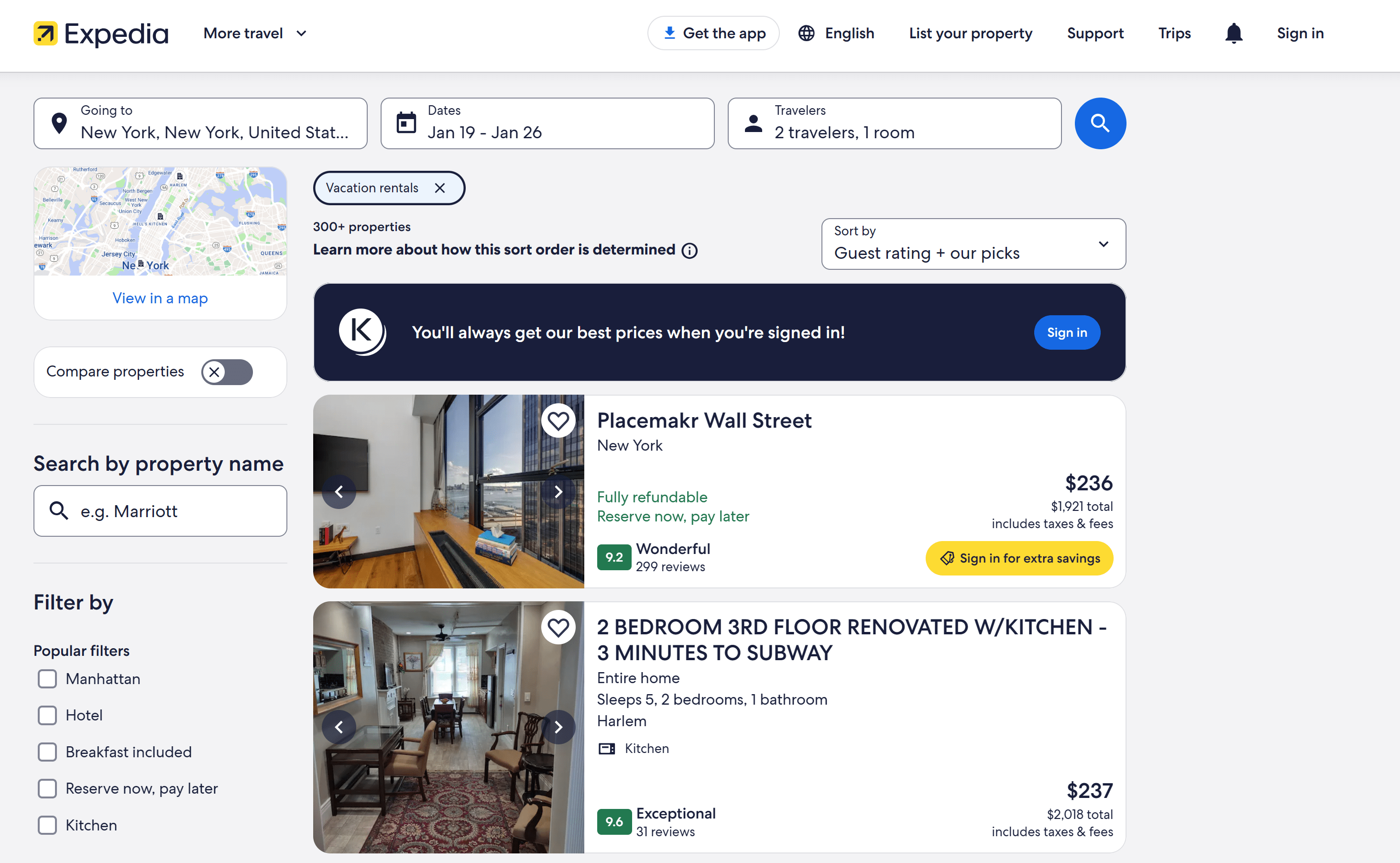

VRBO rentals are already findable in EXPE property 'stay' searches, and you can search for 'only' vacation rentals if you want:

{kind=link}

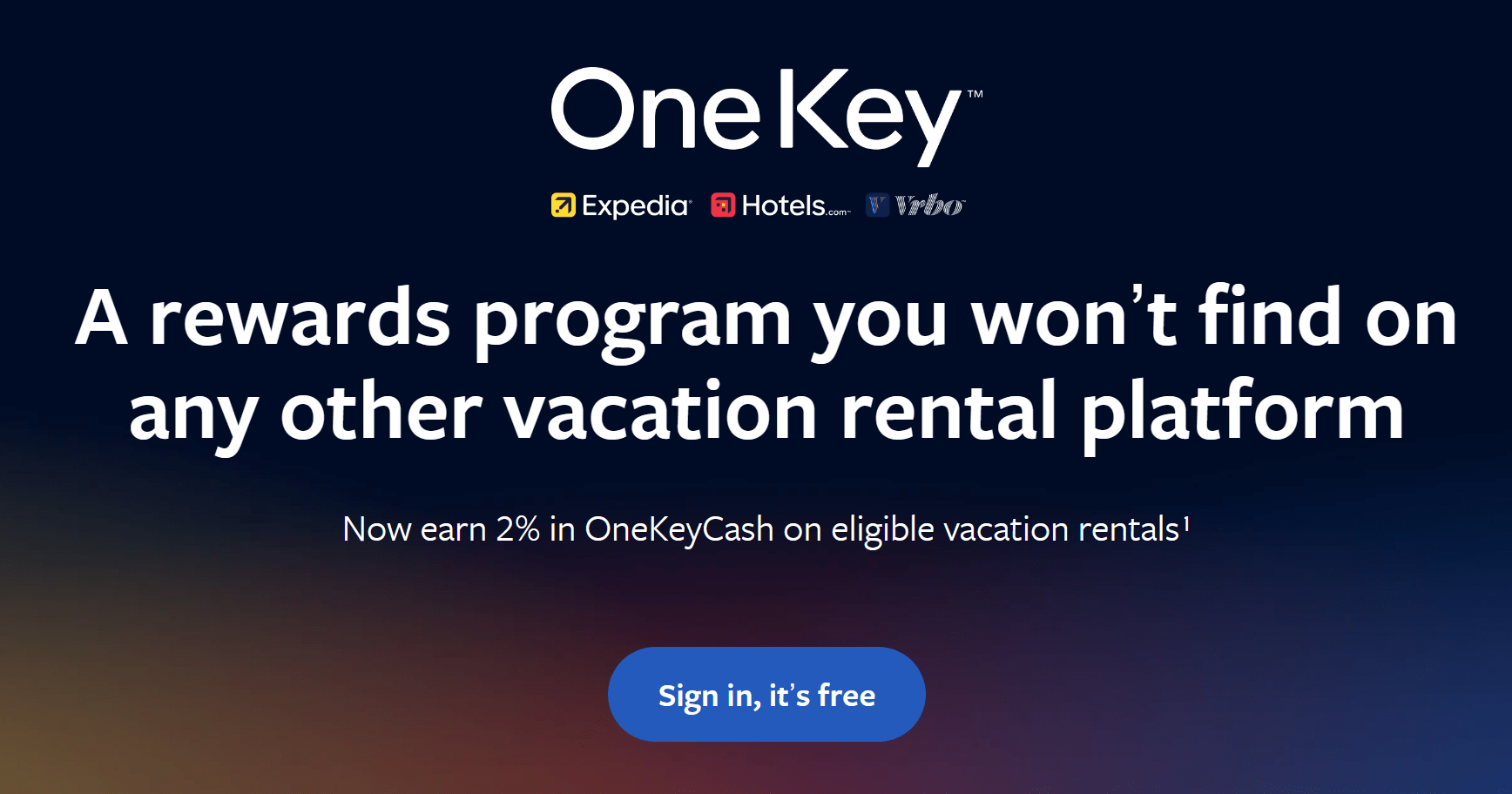

In addition, EXPE has made the smart decision to include VRBO in its OneKey rewards platform that spans its top sites, which should also encourage additional use and network effects:

{kind=link}

Finally, on a more anecdotal note, VRBO seems to have a better reputation among friends and family than Airbnb. Sure, Airbnb has a better selection across the globe of places to stay, but high cleaning fees, checkout procedures, and a generally uneven experience can complicate the experience.

Recent changes to ABNB's product haven't seemed to help this all that much.

VRBO, for its part, only lists 'entire' places, so you'll never be sharing your stay, and there are limited checklists and fees to contend with.

Additionally, considering how small of a market the 'rooms' feature is, focusing on 'entire place' stays seems to be a solid GTM strategy for VRBO.

If VRBO's growth continues, then it's possible that EXPE could see a serious lift in both revenue and margins.

Right now, Expedia doesn't break out financials on a per-site basis. However, if we were to estimate VRBO's contribution to financials based on traffic above, and grow it to ABNB's current size, then EXPE's financials would look more like:

- Revenue of ~$20 billion

- Net income of $2.9 billion

- Net margins of ~14.5%

This stands as an improvement to where things sit today:

- Revenue of $12.5 billion

- Net income of $840 million

- Net margins of 6.7%

Obviously, this isn't going to happen overnight. And, it may never happen. However, the growth of VRBO as a higher margin, internal business could provide tremendous organic lift here to EXPE over time.

Valuation

Thus - the question. What is EXPE currently worth, and what could it be worth?

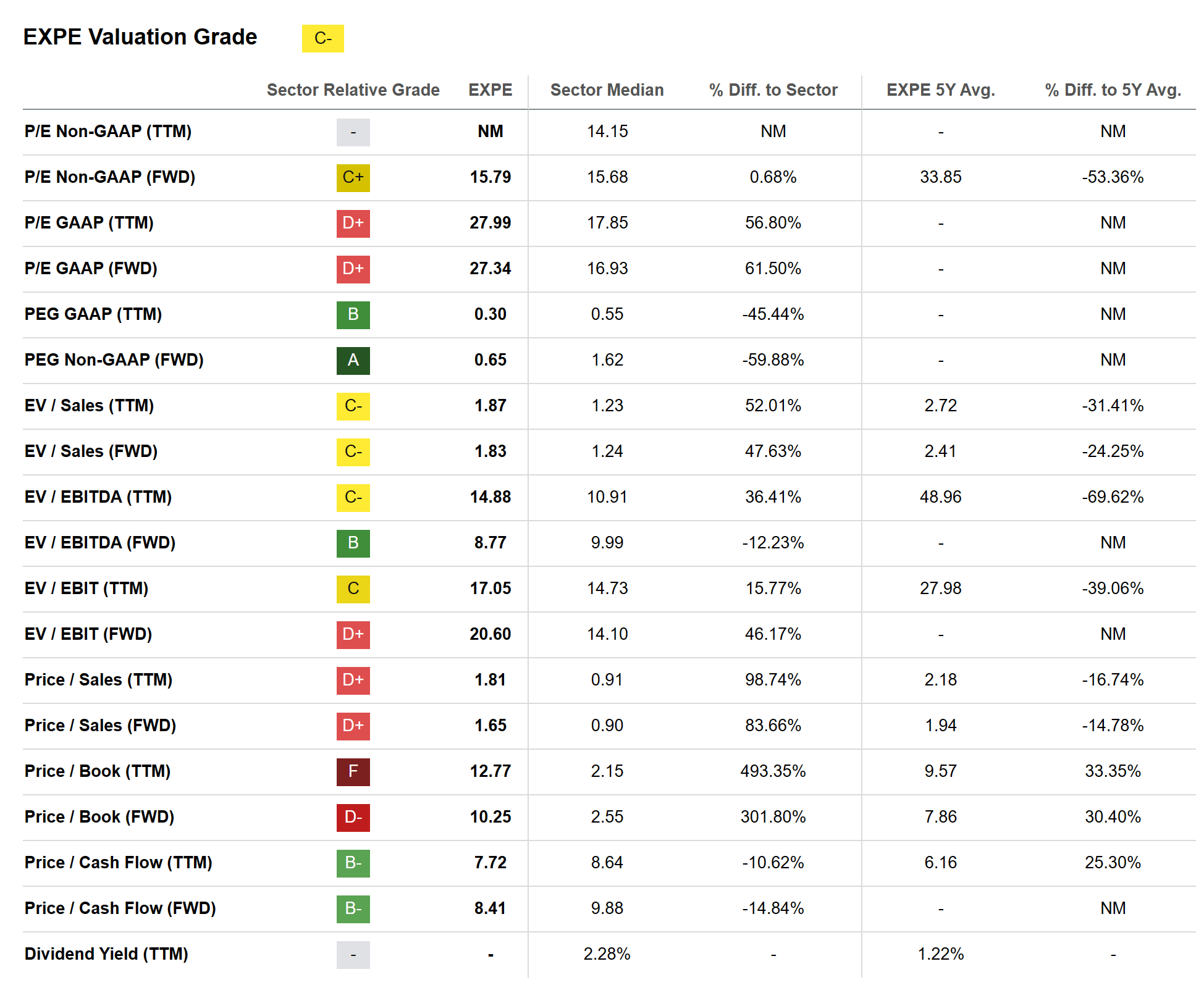

Right now, EXPE has a somewhat middle-of-the-road looking multiple set, which gets a 'C-' from the quant rating system:

{kind=link}

Some of the metrics look quite attractive, like the Price to Cash Flow multiple, which sits at only 7.7x. However, by some other metrics, EXPE looks expensive, especially on earnings (which sit at 27x FWD GAAP) and the book value of 12x.

As a highly solvent tech company, the book value here can be functionally ignored, but 27x FWD GAAP is something to consider.

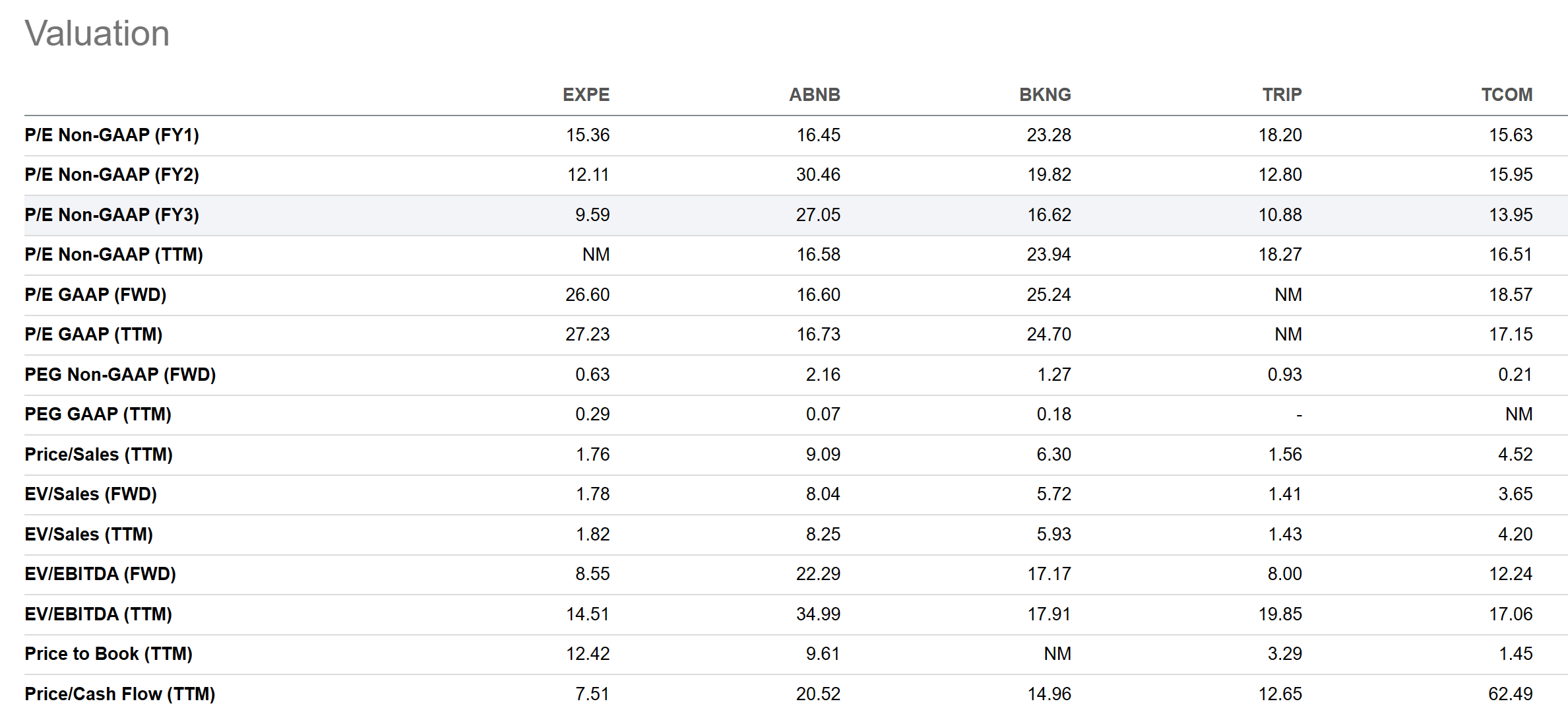

However, when compared to peers, EXPE begins to look more interesting:

{kind=link}

Zooming out into 2026, EXPE is actually trading at the cheapest multiple (only 9x) when compared to growth over that time.

In addition, EXPE sports the cheapest FWD PEG, of only 0.63x. This compares favorably with ABNB's 2.16 and BKNG's 1.27.

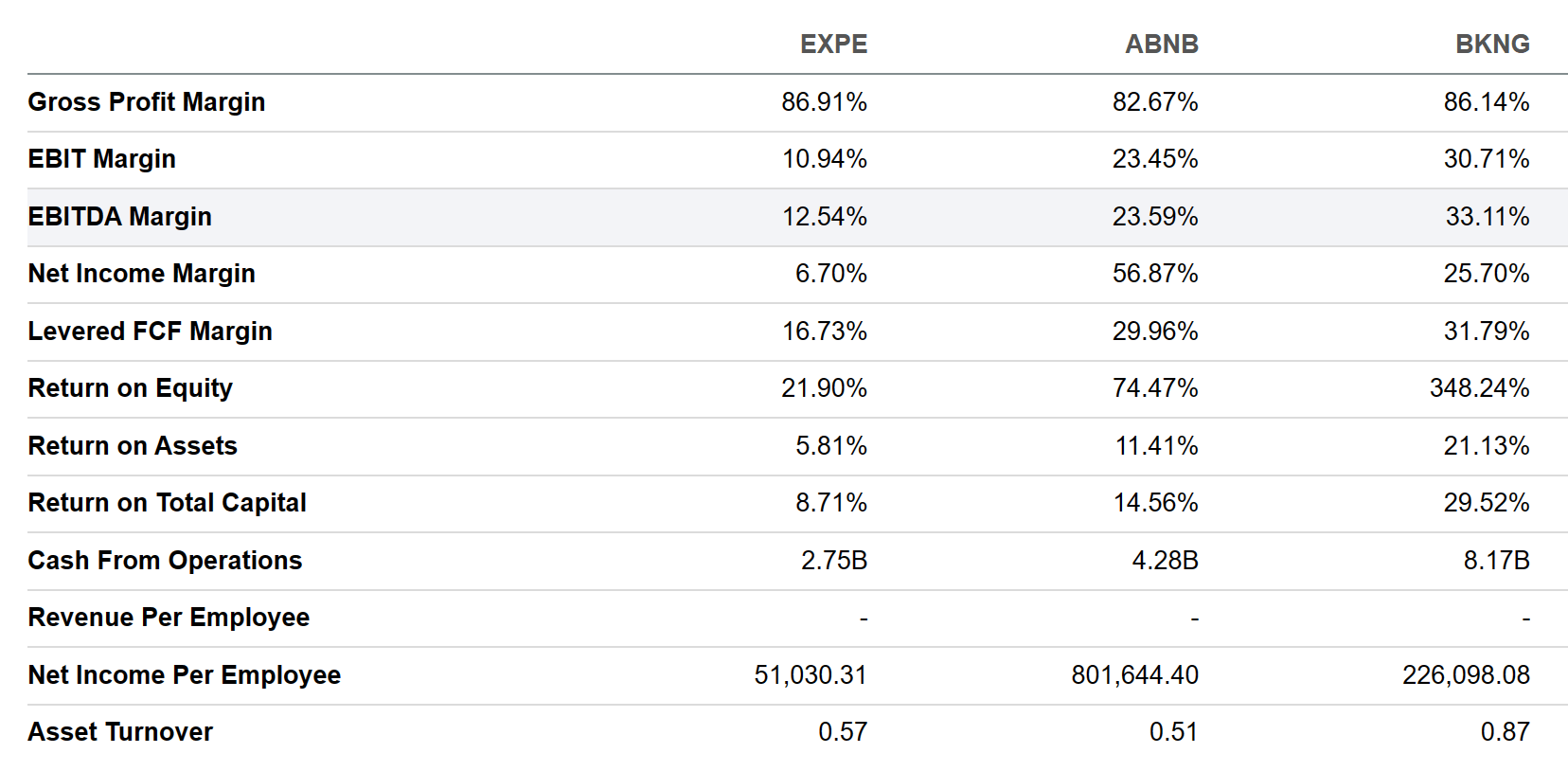

This discount makes sense when you understand EXPE's profitability profile, which is weaker than competitors, especially when looking at EBITDA margins:

{kind=link}

However, in light of the potential growth opportunities and margin lift that VRBO could make possible over time, it could make sense that EXPE's multiple would grow to come more in line with BKNG and ABNB - something closer to a 2.5x sales multiple.

This would put EXPE stock at ~$205 per share assuming a flat diluted share count, which is close to the all-time highs the stock traded at in early 2022. It also represents a 36% upside to Friday's close.

Clearly, there's some upside potential here as EXPE continues executing on its organic IRR opportunity set.

Risks

The key risk to our thesis is simply that VRBO fails to take off and squanders the advantages that EXPE management has given it. Building and growing a flywheel can be hard, especially if there's already an incumbent. We think it's possible that VRBO could fail to gain traction, but given that it's already reached somewhat of a critical mass, continued growth seems inevitable to some degree.

The good news is that a failure to materially grow VRBO over time should lead back to a multiple that is close to what the market has already priced the company at.

Thus, there's a large margin of safety baked into the VRBO 'hidden asset' thesis.

Summary

While Airbnb appears to be the king of the vacation rental by owner category at the moment, EXPE appears to be a well-positioned rival that could take share, re-accelerate growth, and improve margins with its upstart VRBO brand.

With a larger revenue base, more cash to spend on user acquisition, and a wider traffic network to take advantage of, we think VRBO could easily become a solid number 2 in a travel rental market that has no other clear competitors.

Plus, at a multiple that implies a large margin of safety, we think EXPE stock is highly attractive for investors at this point in time.

Thus, our "Strong Buy" rating.

Cheers!

For further details see:

Expedia Is A Better Buy Than Airbnb