ABNB - Expedia: New Initiatives Offer Growth Potential But Questions Still Remain

2023-09-20 04:02:30 ET

Summary

- Expedia maintains a strong market position with a diverse portfolio and customer-centric approach, but faces stiff competition from Booking.com and margin challenges.

- Expedia's "One Key" loyalty program aims to boost revenue and customer loyalty.

- Expedia's QoQ decline in units sold raises concerns, but strong summer 2023 and One Key launch could boost Q3 performance.

- Investing in Expedia could yield a strong return over five years, but questions still remain about margins and One Key's success.

Investment Thesis I believe Expedia Group Inc. ( EXPE ) stock is a hold at the moment, given the mixed signals in its performance and strategy. While the company has strong fundamentals and a promising new loyalty program in "One Key," there are still significant challenges to overcome. Booking.com (NASDAQ: BKNG ) continues to be a formidable competitor, outpacing Expedia in market share and margins. Additionally, the recent quarter-over-quarter decline in units sold is a concern, although the upcoming summer season and the launch of One Key could provide a boost. The projected 19.3% compound annual growth rate ((CAGR)) over the next five years is attractive, but the uncertainties surrounding margin improvement and the success of One Key cannot be ignored. Therefore, it would be prudent for investors to keep a close eye on Expedia's quarterly performance before making any long-term investment decisions.

Company Overview

Expedia Group, Inc. is a global travel technology company headquartered in Seattle, Washington. Founded in 1996, the company has evolved into a one-stop-shop for travel services, offering everything from hotel bookings and flight reservations to car rentals and vacation packages. Expedia operates through a variety of well-known brands, including Expedia.com, Hotels.com, Orbitz, and Trivago, among others. The company's business model primarily revolves around acting as an intermediary between travelers and service providers. Expedia earns money through commissions on bookings, advertising revenue, and service fees.

The travel industry is highly competitive, and Expedia faces stiff competition from both traditional travel agencies and other online platforms. Major competitors include Booking Holdings, which owns Booking.com and Priceline; Airbnb (NASDAQ: ABNB ), which has expanded into hotel bookings; and traditional travel agencies that have made a digital transition. Despite the competition, Expedia's wide range of services and global reach make it a significant player in the travel booking space.

Strong Market Position in the Face of Tough Competition

In my view, Expedia is a market leader in the online travel booking industry and has a strong market position which it has maintained for many years. I believe Expedia's strong market position is a result of its comprehensive and user-friendly product offerings that cater to a wide range of travel needs. The company operates through multiple brands like Expedia.com, Hotels.com, Orbitz, and Trivago, each with its unique value proposition. This diversified portfolio allows Expedia to capture various market segments, from budget travelers to luxury seekers.

What makes Expedia particularly attractive to consumers is its one-stop-shop nature. Customers can book flights, hotels, car rentals, and even vacation packages all in one place. This convenience is a draw for individuals who prefer not to scour multiple websites for the best deals. Additionally, their loyalty programs and partnerships, like the one with Walmart, add an extra layer of incentives for consumers to stick with Expedia for their travel needs.

In a crowded marketplace, Expedia's broad product range and customer-centric approach give it a competitive edge, making it a go-to platform for many travelers. In my opinion, the company has demonstrated this through its ability to maintain a 32% market share from 2018 to Q2 2023 and is a testament to its resilience and strategic acumen in a fiercely competitive and rapidly growing industry. The online travel booking sector is a tough industry to operate in, it’s a market where companies like Booking.com, Airbnb, and traditional travel agencies are vying for consumer attention and are continuing to innovate in order to distinguish themselves from the competition. Yet, Expedia has held its ground, which speaks volumes about its brand strength, customer loyalty, and diversified service offerings.

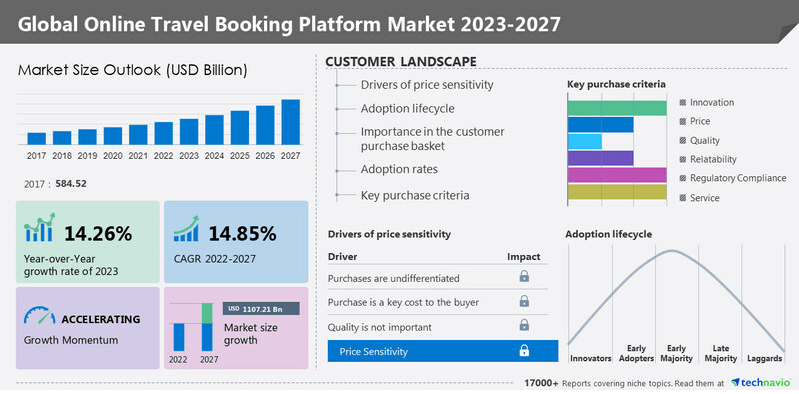

The online travel booking industry has seen significant growth in recent years particular since the reopening of the world since the pandemic, the industry is expected to grow at a CAGR of 14.85% from 2022 to 2027 . This presents a golden opportunity for Expedia. If the company can continue to maintain or even grow its market share, it stands to benefit immensely from the industry's overall expansion.

{kind=link}

Global Online Travel Booking Platform Market 2023-2027 (Technavio)

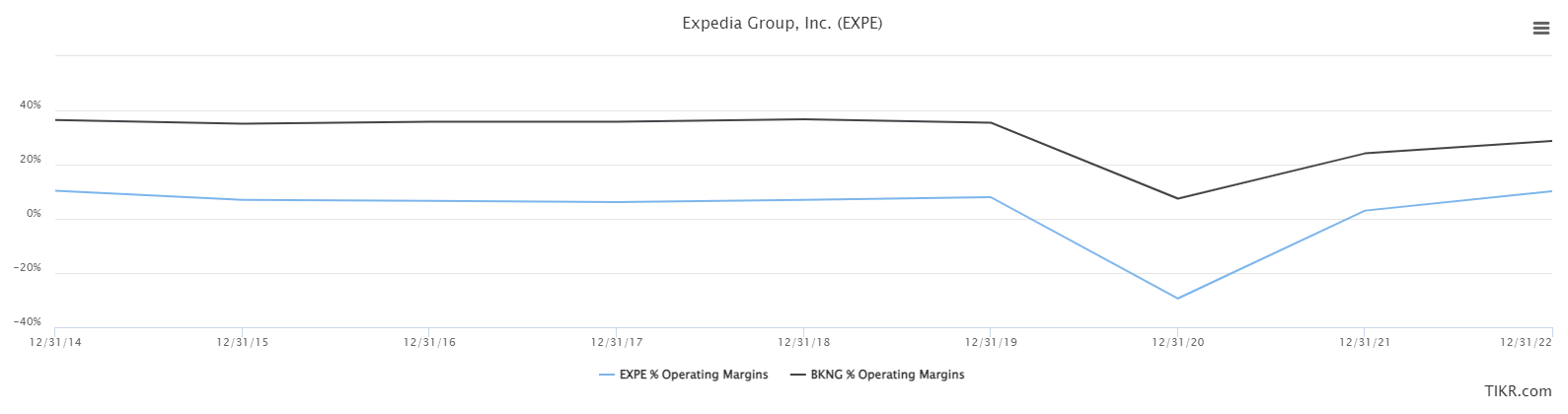

That being said, it’s worth noting the market share of its biggest competitor, Booking.com has expanded in that time from 41% to 50% . While both companies have a large network of product offerings, Booking.com has seen stronger growth in recent years and operates at higher margins compared to Expedia. I think the successful implementation of new initiatives such as ‘One Key’ and their continued progression to reduce costs and improve efficiency.

{kind=link}

Expedia vs Booking.com Margins (TIKR)

New Initiatives Aimed at Attracting and Retaining Customers

The launch of Expedia's "One Key" loyalty program is a significant strategic move that aims to consolidate the company's core brands under a single loyalty umbrella. It aims to offer unparalleled flexibility to travelers, allowing them to earn and spend rewards across a wide range of travel services, from hotels and vacation rentals to flights and cruises. The program is designed to accelerate demand by offering what travelers value most: flexibility. It also aims to attract high-value travelers who spend more and book more often. According to Expedia Group's data , members drove approximately 3x the gross bookings per customer and 2x the gross profit per customer compared to non-members. This could potentially lead to increased revenue and profitability for Expedia.

In my opinion, One Key is an exciting initiative, that, if implemented correctly, could be a game-changer for Expedia. It not only has the potential to increase customer loyalty but also to maximize revenue through its new rewards currency, OneKeyCash which would help the company in establishing a strong form of reoccurring revenue and may help to mitigate the seasonality the company experiences. The program also offers a suite of flexible tools, custom offers, and promotions that could boost bookings and get consumers spending more per visit to an Expedia site. The annual assessment of member eligibility, as opposed to lifetime membership, could keep the program dynamic and continually optimized for maximum profitability.

{kind=link}

Expedia's OneKey Launch (Expedia Group)

Management's confidence in the program is evident from their Q2 2023 earnings call , where they reported record revenue and EBITDA, attributing the strong performance to their strategic initiatives, including "One Key." The company also shifted some of its Q2 marketing spend to Q3 to better align with the program's launch, signalling its importance in their growth strategy for the latter half of the year. The loyalty program is expected to be a key driver in both top-line and bottom-line growth, especially as it starts to gain traction among consumers. I think with ‘One Key’, it’s important to note that it is an industry first and therefore I find it difficult to accurately gauge what kind of impact this will have on the business, while I do anticipate it will drive strong growth for the company, especially during the strong resurgence of the travel industry we are experiencing, the program's success is contingent on the Expedia’s ability to successfully deploy the product across all of its platforms.

Financial Analysis

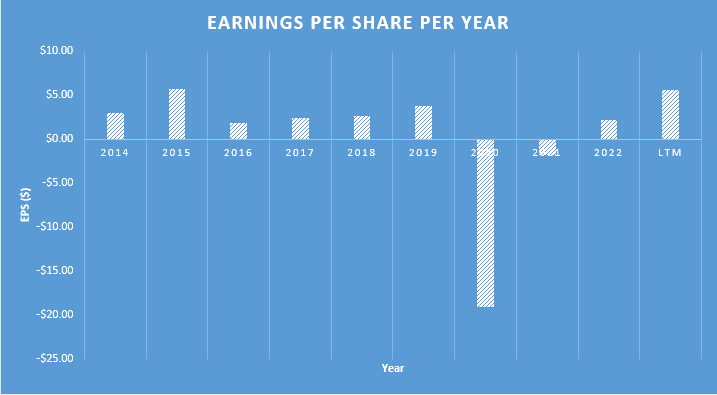

Over the past 5 years, the company has demonstrated mixed financial performance, much of which can be attributed to the COVID-19 pandemic which decimated the travel industry. Its revenue has shown a limited growth since 2018, increasing from $11.22 billion to $12.26 billion in the last 12 months LTM, but has seen an impressive revenue CAGR of 33.1% since 2020 where revenue dropped to $5.2 billion as a result of the pandemic. The earnings per share ((EPS)), has been more impressive, rising from $2.65 in 2018 to $5.59 LTM. I think this is good reflection on the company’s improving margins, which as I mentioned before, typically underperforms its online travel counterparts. When looking on a quarterly basis, the company has recorded some of their strongest operating margins in recent history and hopefully signals a turning point for the company, which has been dedicated to managing expenses and being disciplined with spending.

{kind=link}

EXPE's EPS Per Year (DJTF Investments)

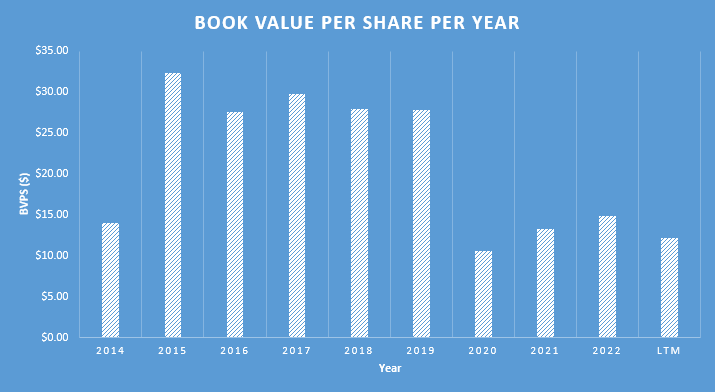

Expedia’s balance sheet is one of the weaker aspects of the business in my opinion. The book value per share has yet to recover to its 2018 level of $27.82 after falling substantially in 2020 to $10.52. Book value per share has slowly been recovering since 2020 to $12.18 LTM. I think is another indicator which demonstrates just how devastating the pandemic was to Expedia.

{kind=link}

EXPE's BVPS Per Year (DJTF Investments)

As of the most recent quarter, the company reported cash and cash equivalents of $6.27 billion. The company's total debt stands at $6.55 billion, with substantial portion of the debt being taken out during the pandemic. While the company does have a notable amount of debt, Expedia has cash and cash equivalents to cover this debt and therefore is not a concern in my opinion. Management have also demonstrated commitment to paying it off as the total debt held by the company has declined over the past 2 years.

I also want to briefly discuss Expedia’s recent performance and their slowdown in sales growth. In the last quarter, the company saw a quarter over quarter (QoQ) decline in units sold across their booked room nights and booked air tickets which is differs from 2021 and 2022 which both saw QoQ growth in Q2 for units sold. This resulted in a QoQ decline in gross bookings, yet the company still managed to grow, albeit at a slower rate than the previous 2 years. This isn’t necessarily a massive concern for me as I believe the company will have strong Q3 given that summer 2023 has been a record breaker and consciences with the launch of OneKey.

Looking beyond the next 12 months, assuming the travel industry maintains its strong post-pandemic recovery, the company should see solid growth accompanied by expanding margins and slow but steady improvement to the balance sheet. That being said, I believe that a lot of Expedia’s long-term growth will largely be dependent on their ability to implement initiatives such as OneKey which can attract consumers in an industry where there seems to be hundreds of different options.

Valuation

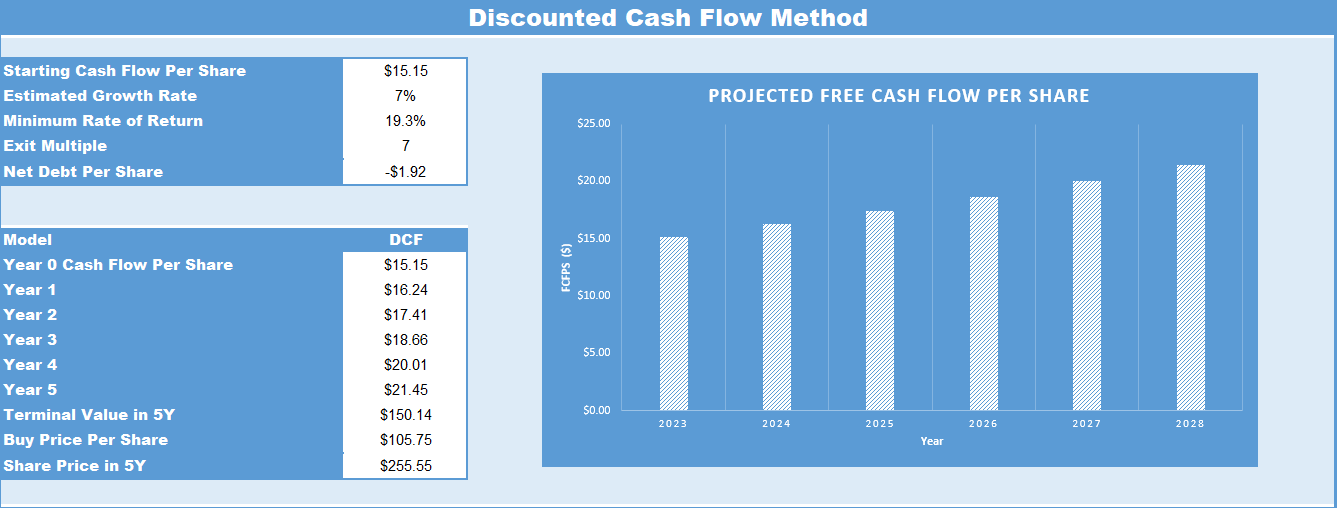

Expedia's current TTM free cash flow ((FCF)) per Share as of Q2 2023 is $15.15. Given the company's strategic initiatives and its focus on cost efficiencies as well as the continued growth of the online travel booking industry, I conservatively estimate that Expedia's TTM FCF per Share should grow at approximately 7% annually for the next five years which is below analysts’ estimates for growth of Expedia over the next 5 years and below the FCF growth rate of 9.35% CAGR the company has experienced over the past 10 years. Taking this growth rate into account, by Q2 2028, Expedia's FCF per share is projected to be $21.45. Using an exit multiple of 7, which is a price-to-free-cash-flow ratio that the company has been regularly trading at since the business returned to growth post-Covid, this would suggest a five-year price target of $255.55. Therefore, if you were to invest in Expedia at today's share price of $105.74, you could anticipate a CAGR of 19.3% over the next five years.

{kind=link}

EXPE's DCF Valuation Model (DJTF Investments)

This valuation assumes that the industry as a whole continues to grow strongly, and that Expedia is able to continue to attract and retain consumers. Personally, whilst this valuation is attractive, I still have reservations about Expedia's ability to sustainably improve its margins, which have historically lagged behind those of its peers like Booking Holdings. Additionally, while innovative initiatives like One Key are promising, it is still in its nascent stages and comes with its own set of integration risks and uncertainties about customer adoption rates. It's a step in the right direction, but it's up against well-established loyalty programs and brand loyalties in a fiercely competitive market. Because of this I believe that Expedia is a hold, although I will be continually assessing the company over the coming quarters to see if the situation changes.

Conclusion Expedia has long been a dominant player in the online travel booking industry, thanks to its diverse portfolio and customer-centric approach. However, it faces significant challenges, notably from Booking.com, which has been outperforming it in both market share and margins. The introduction of the "One Key" loyalty program is a strategic move aimed at boosting revenue and customer loyalty, offering a glimmer of hope for future growth. While the company experienced a quarter-over-quarter decline in units sold, the strong travel demand expected in summer 2023 and the launch of One Key could potentially uplift its Q3 performance. Investment in Expedia presents an attractive opportunity, with projections suggesting a 19.3% CAGR over the next five years. However, lingering questions about its ability to improve margins and the uncertain success of One Key make it a hold for now. Investors should keep a close eye on the company's performance in the coming quarters to reassess its potential.

For further details see:

Expedia: New Initiatives Offer Growth Potential, But Questions Still Remain