EXFY - Expensify: Downside Is Limited Considering Valuations And Buybacks

2023-05-15 12:13:18 ET

Summary

- Expensify's Q1 2023 financial performance didn't meet the market's expectations, and I don't expect EXFY to deliver a good set of results in Q2 2023 as well.

- But EXFY is fairly valued with its current EV/EBITDA multiple of 10.5 times, and its shares should find support from the company's buyback plan.

- A Hold rating for Expensify is justified, taking into account both its near-term outlook and valuation metrics.

Elevator Pitch

I assign a Hold investment rating to Expensify, Inc.'s ( EXFY ) shares. I think there is limited downside for EXFY's stock, even though the company's short-term outlook is unfavorable. Expensify is fairly valued based on my analysis, and the company has initiated share repurchases which will provide support for its stock price. But a positive re-rating of EXFY's valuations in the near future is unlikely, considering the company's prospects for Q2 2023. This explains my Neutral view and Hold rating for EXFY.

Company Description

Expensify refers to itself as "a payments superapp" which makes it easier to "manage money across expenses, corporate cards, and bills" in the company's media releases .

The Expensify SuperApp's Key Features

EXFY's Investor Relations Website

{kind=link}

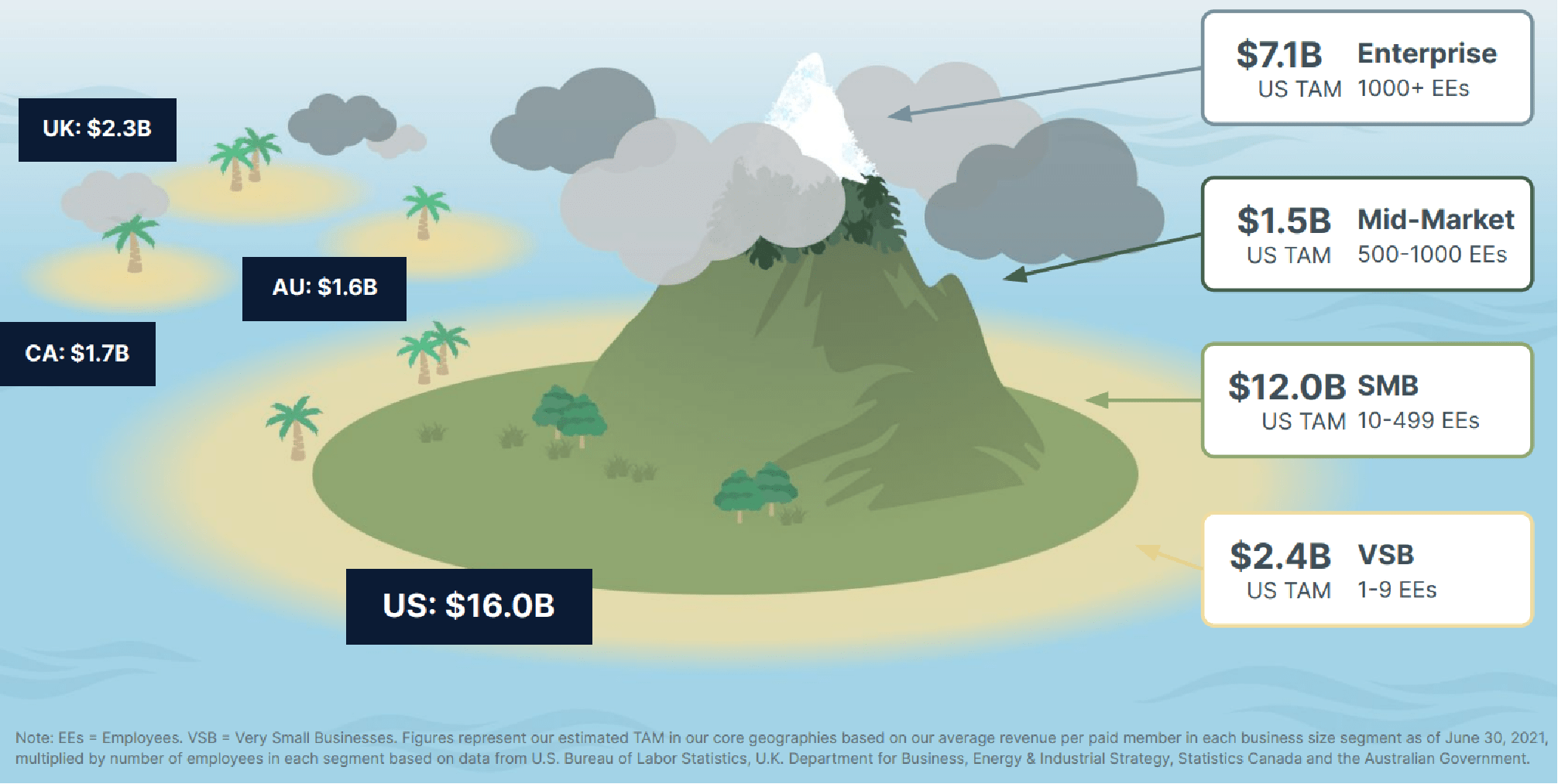

The TAMs Of The Key Geographic Markets And Client Segments That Expensify Is Targeting

EXFY's Q1 2023 Results Presentation

{kind=link}

EXFY's home market, the US, accounted for 91% of the company's revenue for full-year fiscal 2022, as per its 10-K filing . Foreign markets outside of the US contributed the remaining 9% of Expensify's top line in the previous year. As highlighted in the chart above, Expensify has the intention to expand its presence in international markets such as the UK, Australia, and Canada.

Disappointing Quarterly Results For Expensify

EXFY issued a press release last Tuesday after trading hours disclosing its financial performance for Q1 2023. Expensify's most recent quarterly financial results were a disappointment, as both the company's revenue and earnings failed to meet the market's expectations.

The company's actual first quarter top line of $40.1 million was -8% below the sell-side analysts' consensus sales projection of $43.7 million . Q1 2023 is the first quarter that Expensify had registered a revenue contraction (-0.7%) since the company's public listing in November 2021 . EXFY's top-line growth has already been slowing down significantly in the past few quarters. Expensify's revenue expansion rates for Q1 2022, Q2 2022, Q3 2022, and Q4 2022 were +35.8%, +22.3%, +13.5%, and +7.7%, respectively in YoY terms.

In its Q1 2023 earnings presentation slides , Expensify highlighted that "activity across all customers is down" due to weak "economic conditions" which drove "a net decrease in paid members." EXFY disclosed at its recent first quarter earnings call that the number of paid members per client for the company declined from approximately 14.0 in Q4 2022 to 13.3 for Q1 2023.

Separately, Expensify's normalized earnings per share or EPS of $0.05 for the first quarter of this year missed the market's consensus bottom line estimate of $0.08 by -37% , and this was equivalent to a -45% YoY drop

The non-GAAP adjusted EBITDA margin for EXFY decreased from 27.2% in Q1 2022 and 25.7% in Q4 2022 to 21.7% for Q1 2023. It is reasonable to conclude that Expensify's EBITDA margin contraction was the result of negative operating leverage. On its investors' FAQs page , Expensify stressed that it "avoids the high marginal costs of the competition" thanks to its "word of mouth, self-service business model." This implies that EXFY has a high proportion of fixed costs and a high degree of operating leverage embedded with its business operations. As such, when Expensify's revenue growth slows or even turns negative, the company's bottom line takes an even bigger hit.

A Turnaround In The Near Term Is Unlikely

The probability of Expensify delivering a positive surprise with its Q2 2023 results is pretty low.

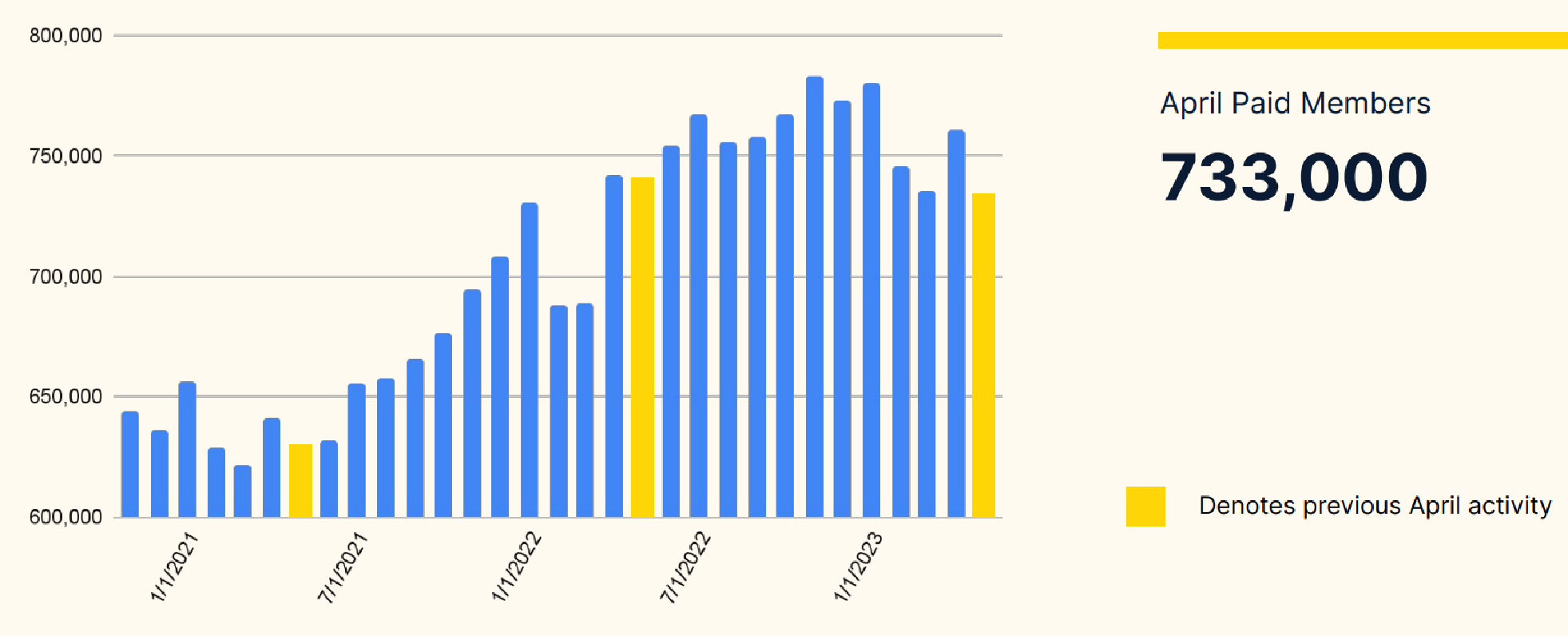

The Number Of Paid Members For EXFY Tracked On A Monthly Basis

{kind=link}

As per the chart presented above, Expensify's number of paid members has declined MoM (Month-on-Month) and YoY in April 2023. Therefore, it is highly probable that EXFY's revenue will continue to contract in April and Q2 2023 based on the paid members' growth trend. At its Q1 2023 earnings briefing, Expensify acknowledged that it is "not through the woods yet on the volatility" relating to the economy and the change in paid member numbers.

EXFY's profitability outlook for Q2 FY 2023 isn't encouraging too. The company guided at the most recent quarterly results call that its selling and marketing expenses should see an uptick in the current quarter. Expensify added 100 new sales representatives in the first quarter of this year, and the negative impact on staff costs wasn't fully reflected in Q1 2023 due to timing differences in expense recognition. EXFY will be also organizing a conference known as "ExpensiCon" between May 18 and May 2023, which will incur additional costs for the company.

In consideration of the factors mentioned above, I see Expensify reporting lower top line and earnings for Q2 FY 2023.

EXFY's Valuations And Share Repurchases

Expensify's stock is fairly valued, and share buybacks will help to limit the downside for EXFY's shares in the short term.

As per S&P Capital IQ's valuation data, EXFY is currently trading at 10.5 times consensus forward next twelve months' EV/EBITDA. The sell-side's consensus EBITDA CAGR projection for Expensify is 10.6%. Although the weak economic conditions have hurt EXFY's financial performance in the near term, the company's long-term growth runway is unaffected. As mentioned earlier in this article, less than 10% of Expensify's revenue is generated from foreign markets, and there is room for EXFY to expand in overseas markets like the UK in the long run.

In my view, Expensify's shares are at a fair valuation now, as the company's expected EBITDA growth is roughly aligned with its EV/EBITDA valuation metric.

Moreover, Expensify revealed in its Q1 2023 results press release that it will execute on "$3.0 million of near-term share repurchases in the open market starting May 10th." The company's recent share buybacks have helped to stabilize EXFY's share price. Expensify's stock price fell by -18% to $5.91 on May 10, 2023, after reporting below expectations Q1 results. Subsequently, EXFY's shares rose to $5.96 at the end of the May 11 trading day, before closing slightly lower at $5.86 on May 12.

Closing Thoughts

A Hold rating for Expensify is reasonably fair. Q2 2023 is expected to be another tough quarter for EXFY in terms of revenue growth and operating profitability. On the flip side, EXFY's valuations aren't expensive, and its share price should be supported at current levels with ongoing share buybacks.

For further details see:

Expensify: Downside Is Limited Considering Valuations And Buybacks