EXPO - Exponent: Great Financial Health But Not A Good Time To Start A Position

2023-09-12 04:16:24 ET

Summary

- Exponent Inc. has a hold rating due to an unjustified PE ratio compared to revenue and EPS growth prospects.

- The company has strong financial health with no long-term debt and a current ratio within the desired range.

- Exponent has exceptional ROA, ROE, and ROIC, indicating efficient use of assets and shareholder capital. However, revenue growth is lower than expected for such a high PE ratio.

Investment Thesis

I wanted to take a look at Exponent Inc.'s ( EXPO ) financials because one of my friends was looking at opening a position. I offered to have a deeper look into the company before any transaction occurred. The current PE ratio doesn’t seem to be justified by the revenue growth and EPS growth prospects, therefore, I am giving the company a hold rating until these improve or the share price comes down.

Briefly on the Company

Exponent Inc. is a consulting company that specializes in engineering and science globally. The company has two reportable segments: Engineering and Other Scientific, which accounted for 83% of total revenues in FY22 , and Environmental and Health.

Financials

I like to look at full-year results for the big picture of where the company is heading rather than q/q results as these tend to fluctuate much more. I will include any necessary information from the most recent quarter for extra color, however, all graphs below will be as of FY22.

As of Q2 ’23 , the company had $148m in cash against zero long-term debt. This is always a great position to be in. It gives the company more freedom in how it can use its cash flow, whether that would be for growth initiatives or rewarding shareholders. I would prefer a company to reinvest in itself, but if there is no possible way of doing that anymore, rewarding shareholders through dividends or share buybacks is also acceptable, if those share buybacks are for a discount rather than an expensive company.

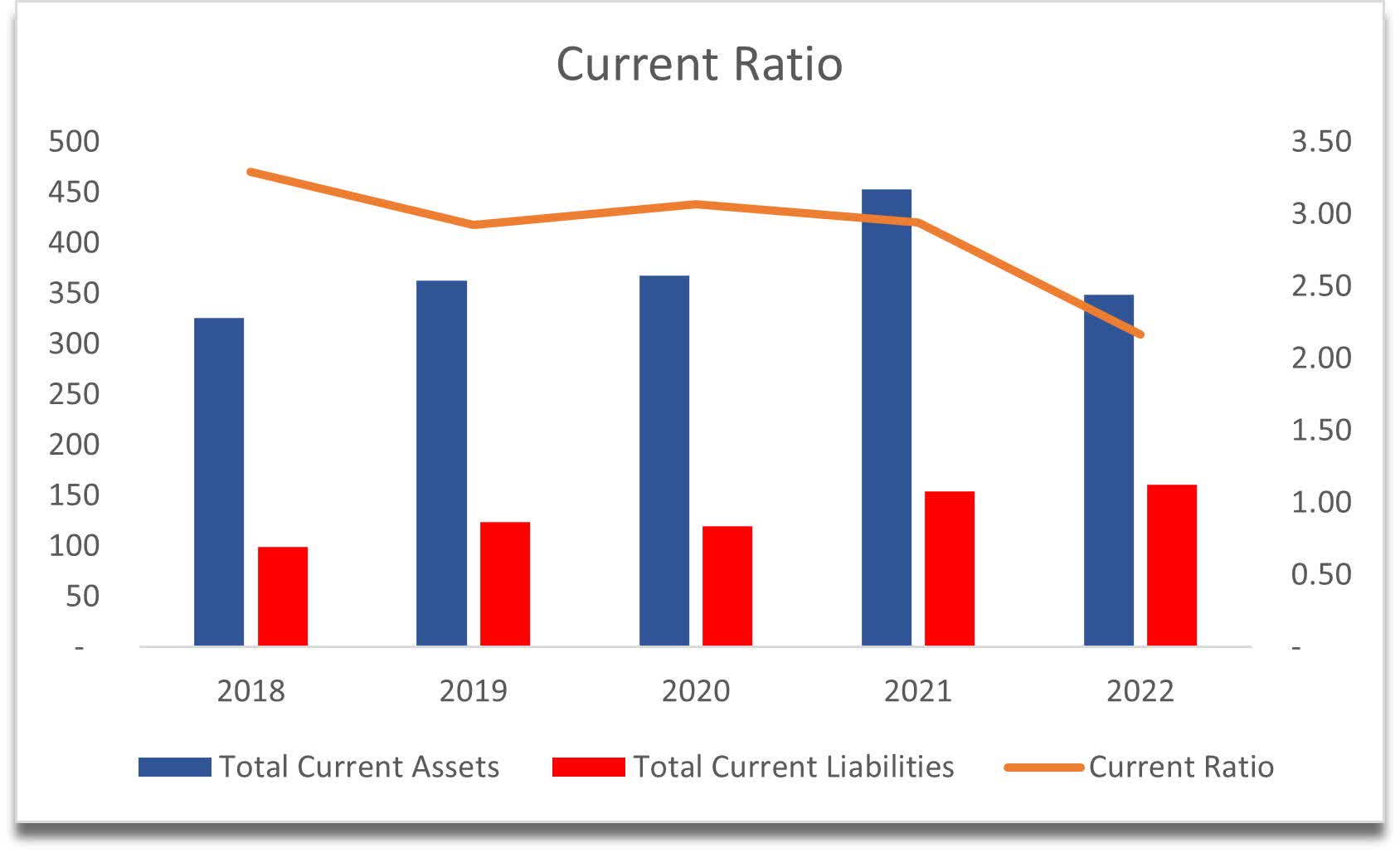

The company’s historic current ratio has been on the upper end of my desired range, or as I call it, efficient range. The efficient range is 1.5-2.0 in my opinion as this strikes a good balance between the ability to pay off the company’s short-term obligations and using assets like cash for further growth initiatives. As of FY22, the current ratio stood at around 2.1 which is about where I like it to be, however, as of Q2 ’23, this has gone up to around 2.7. It is not a bad thing, however, it’s not very efficient in my opinion either.

{kind=link}

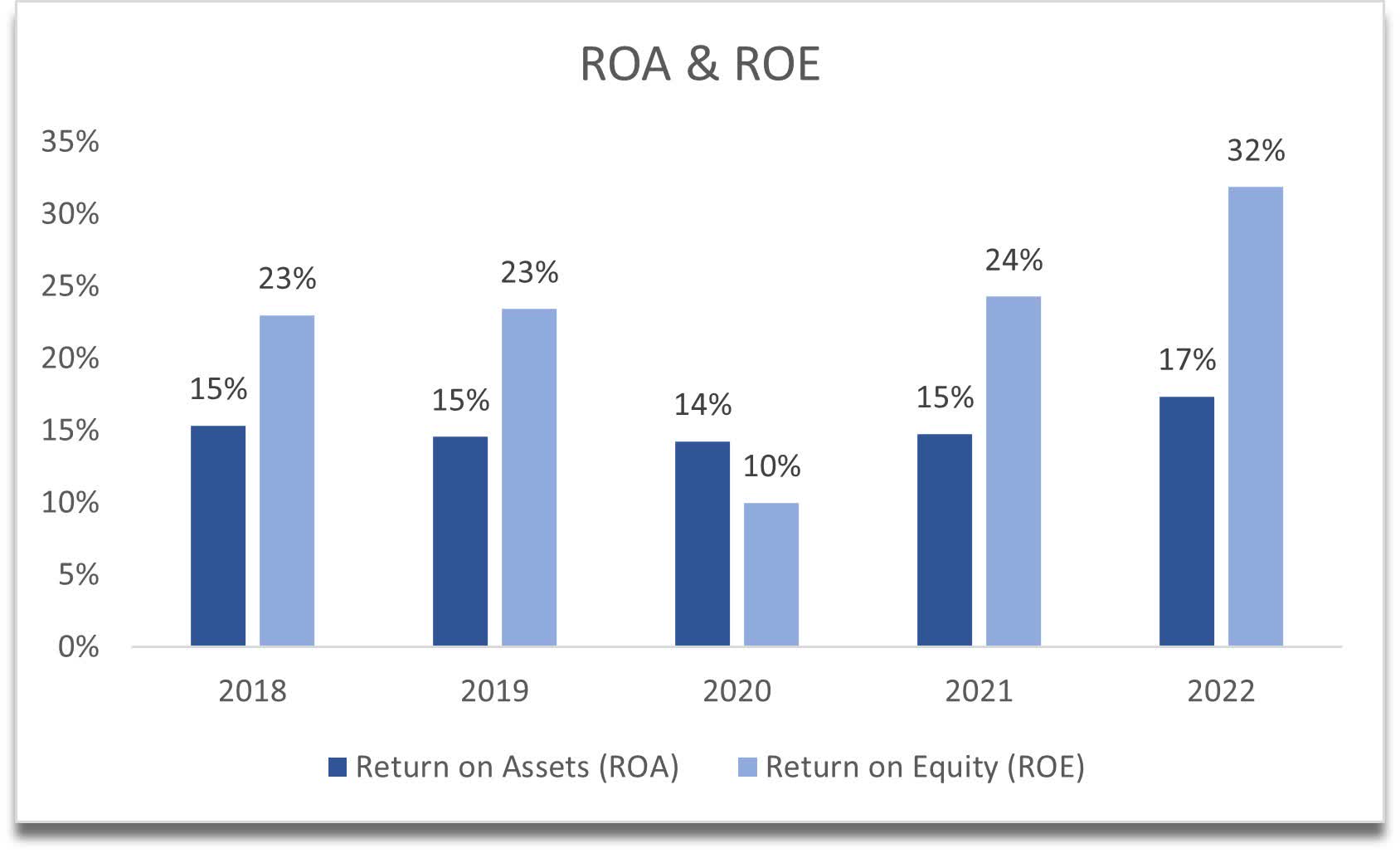

The company’s ROA and ROE have been exceptional over the last 5 years with clear improvements since FY20. The minimums I look for in these two metrics are 5% for ROA and 10% for ROE, which tells me that the management is utilizing the company’s assets and shareholder capital quite efficiently, thus creating value.

{kind=link}

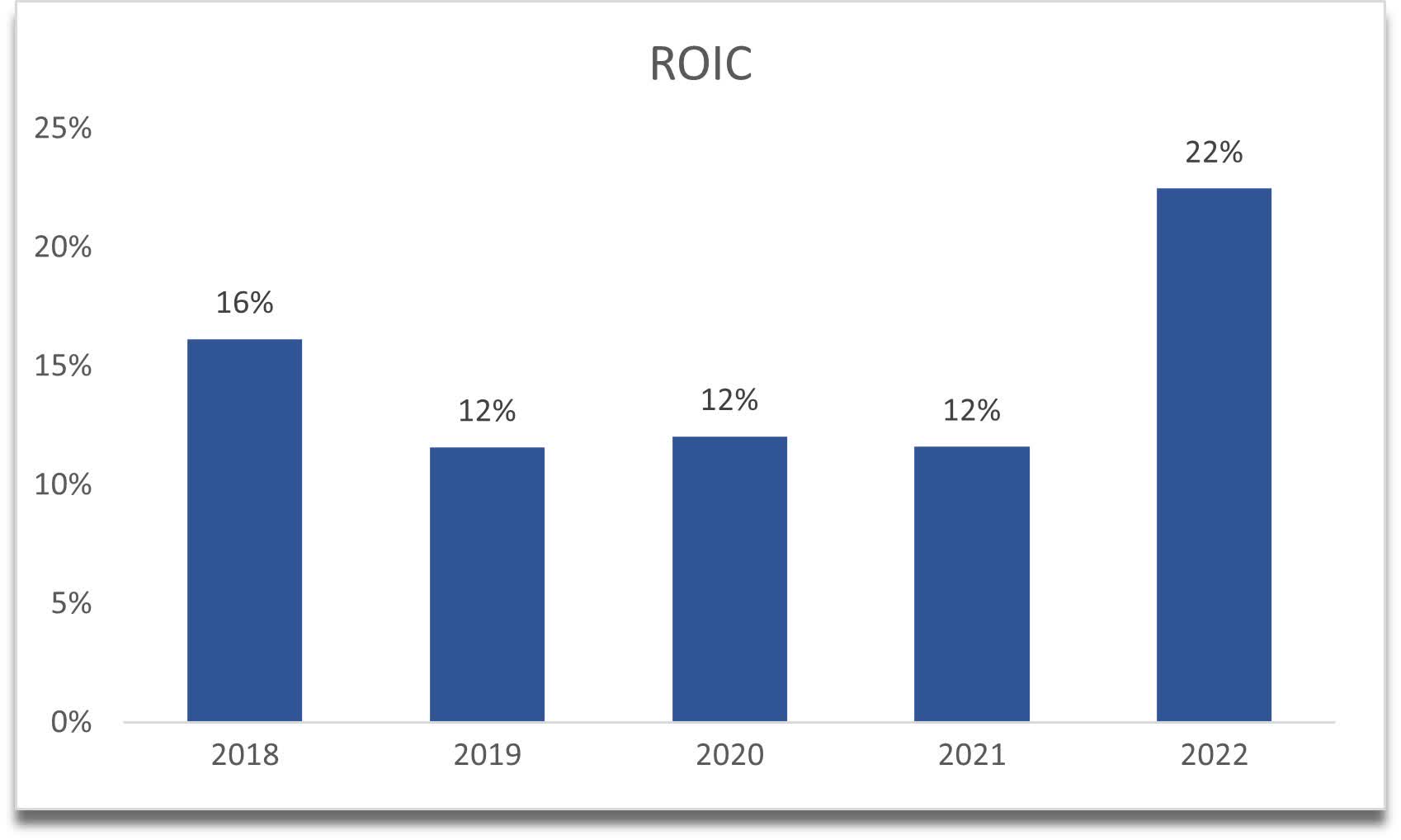

Another exceptional and very important metric for me is the return on invested capital. I aim for companies that can get at least 10% ROIC, which tells me the company has a decent competitive advantage and a moat. EXPO's ROIC as of FY22 has been 22%, which is fantastic. This tells me the company has a strong moat and a proper competitive edge. A little premium on shares wouldn't be out of the question.

{kind=link}

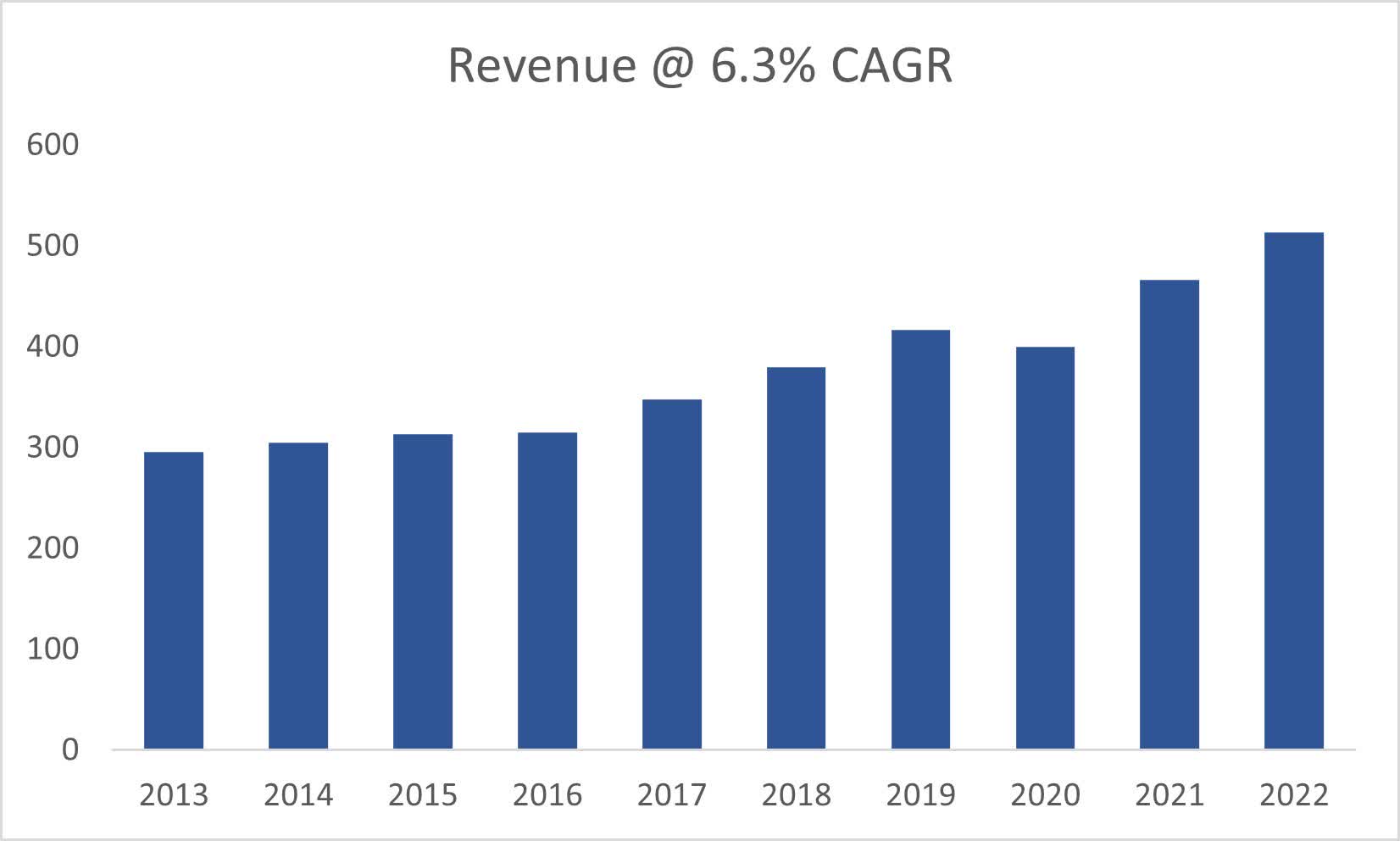

Revenue growth over the last decade is on the lower side in my opinion. Definitely doesn’t justify a TTM P/E ratio of 45. The company grew its revenues at a 6.3% CAGR, which gives me a baseline of where I will anchor my growth estimates for the model.

{kind=link}

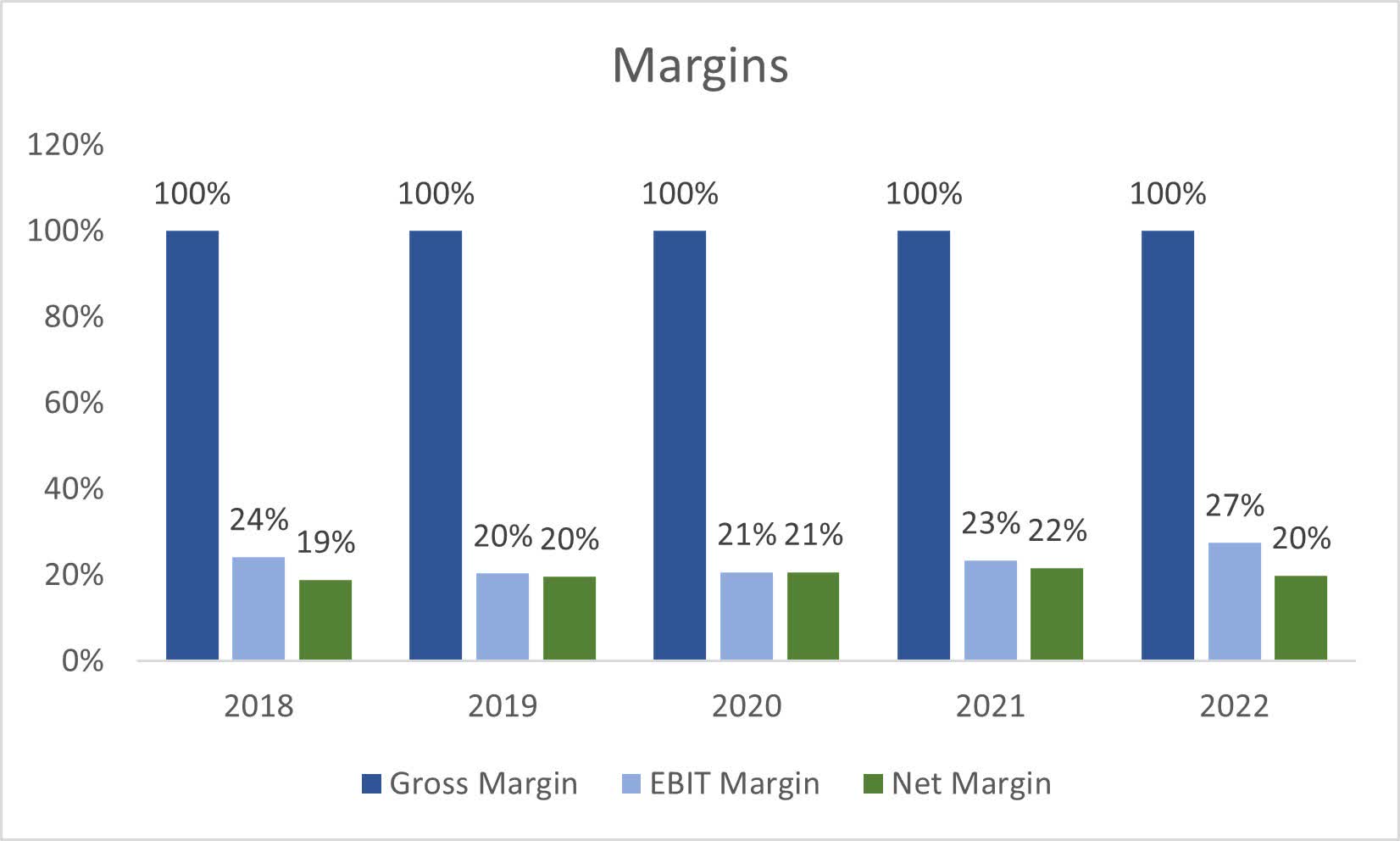

In terms of margins, these have been consistent over the years, and I don’t see much improvement happening any time soon, however, I do believe that over time, especially a decade, companies find ways to become more efficient and profitable, therefore, I will do some adjustments in my model in the next section.

{kind=link}

Overall, there is a lot to like in terms of the company’s profitability, efficiency, and financial health in general. The company has a lot of freedom because it is not burdened with debt and interest expenses, which frees up the cash flow for growth initiatives. The company seems to have quite a competitive advantage and a strong moat, which means I wouldn’t mind paying a slight premium for the shares. So, let’s look at what I would be willing to pay for the company’s revenue growth and earnings potential.

Valuation

As I mentioned earlier, the company’s revenue growth hasn’t been the strongest, some years saw low double-digit growth, and some low single-digit growth, and in the end it all averaged around 6.3% CAGR for the previous decade. Let's say the company manages to grow at around 7.2% for the next decade in the base case scenario, which is a slightly more optimistic take on growth. For the conservative case, I decided to go with a 5% CAGR, while for the optimistic case, I went with an 11% CAGR, to give myself a range of possible outcomes. Analysts predict around 9% growth for FY23, which comes down to around 7 for the next 2 years. After that, I had to go with hypotheticals to fill out the model.

Same for EPS, the company doesn't seem to be becoming more efficient very much, with less than 10% growth y/y for FY23 and FY24. This tells me that the company isn't improving its margins very much, however, as I mentioned in the previous section, companies tend to find ways of becoming more efficient, so for my model, I decided to improve operating margins by around 400 bps or 4% by the end of FY32 from the margins the company saw at the end of FY22.

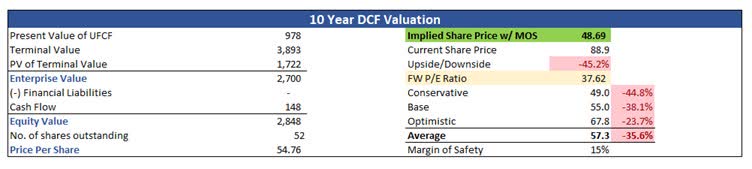

On top of these assumptions, I decided to add a 15% margin of safety to be on the safer and more conservative side. I usually give a 25% margin of safety to companies with great financial health; however, I made an exception here because I like the company's ROIC, ROA, and ROE numbers. With that said, Exponent’s intrinsic value is around $49 a share, which means the company is slightly overvalued currently.

{kind=link}

Closing Comments

I knew as soon as I saw the revenue outlook that a company with such a P/E ratio is probably trading a little on the rich side. My PT is almost half the current share price, however, that is where I would be willing to start a position, which would reflect a decent risk/reward for me. As you can see above, the company is currently trading at around 38x earnings, which is very high considering the revenue and earnings growth is in the high single digits. If it was trading at my PT, the company would be trading at around 20x earnings which is still quite high, to be honest, however, as I said earlier, such high ROIC deserves a slight premium, and I would be willing to pay 20x earnings if it comes down eventually.

The company’s share price has performed great over the last decade, going up 400%, while going up 7000% since ’98. It seems a little overpriced to me, so I wouldn't hop on the train now, however, I don't think selling your position at these prices is good either, since the company may continue to trade at a premium until earnings or revenue growth improves dramatically. I will have to be patient and follow how the company's performance develops over time and whether some time in the future would be a good time to jump in.

For further details see:

Exponent: Great Financial Health, But Not A Good Time To Start A Position