EXPO - Exponent: Highly Profitable Business With A Wide Moat

2023-09-29 11:35:04 ET

Summary

- Exponent’s revenue has grown at a CAGR of 6% while EBITDA has at 8%. This has been driven by its fantastic business model and industry tailwinds.

- Exponent provides highly complex consulting services to its clients, leveraging decades of experience and data. Further, it has developed deep expertise within specific high-value, robust industries, such as healthcare.

- Global megatrends such as technological development and growing investment in healthcare and chemicals have the potential to maintain or enhance Exponent’s growth trajectory.

- Exponent is an expensive investment but we believe it can maintain its current trajectory, contributing to greater scale with a FCF-M of >18%.

Investment thesis

Our current investment thesis is:

- Exponent, Inc. ( EXPO ) has developed a wide moat through a number of factors, all of which are built on providing an exceptional service. It is a leader in its market and has shown an ability to grow scale without diluting capabilities. Exponent’s exceptional margins and lack of erosion are a financial reflection of its competitive positioning.

- The company services industries that are highly resilient while also benefiting from growth, allowing the company to enjoy an upward growth trajectory with limited volatility. With megatrends positioned to at least maintain the status quo, Exponent should have healthy growth ahead.

- The business is performing extremely well relative to its peers, particularly due to its margin superiority. It may not have comparable growth but this appears to be a “tortoise and the hare” situation given the level of competition in “mainstream” consulting.

- Exponent is expensive and we do not like to see its FCF yield decline. Despite this, it's hard to argue against its fantastic fundamentals.

Company description

Exponent is a multidisciplinary scientific and engineering consulting firm headquartered in Menlo Park, California. Founded in 1967, Exponent provides a range of technical expertise and analytical services to clients across various industries, including automotive, healthcare, environmental, and consumer products. The company is known for its team of experts, including scientists, engineers, and consultants, who tackle complex challenges and offer solutions based on rigorous research and analysis.

Share price

Exponent’s share price performance has been exceptional, returning over 350% to shareholders and noticeably exceeding the wider market. This has been driven by incremental financial improvement alongside commercial development.

Financial analysis

Exponent's financials (Capital IQ)

{kind=link}

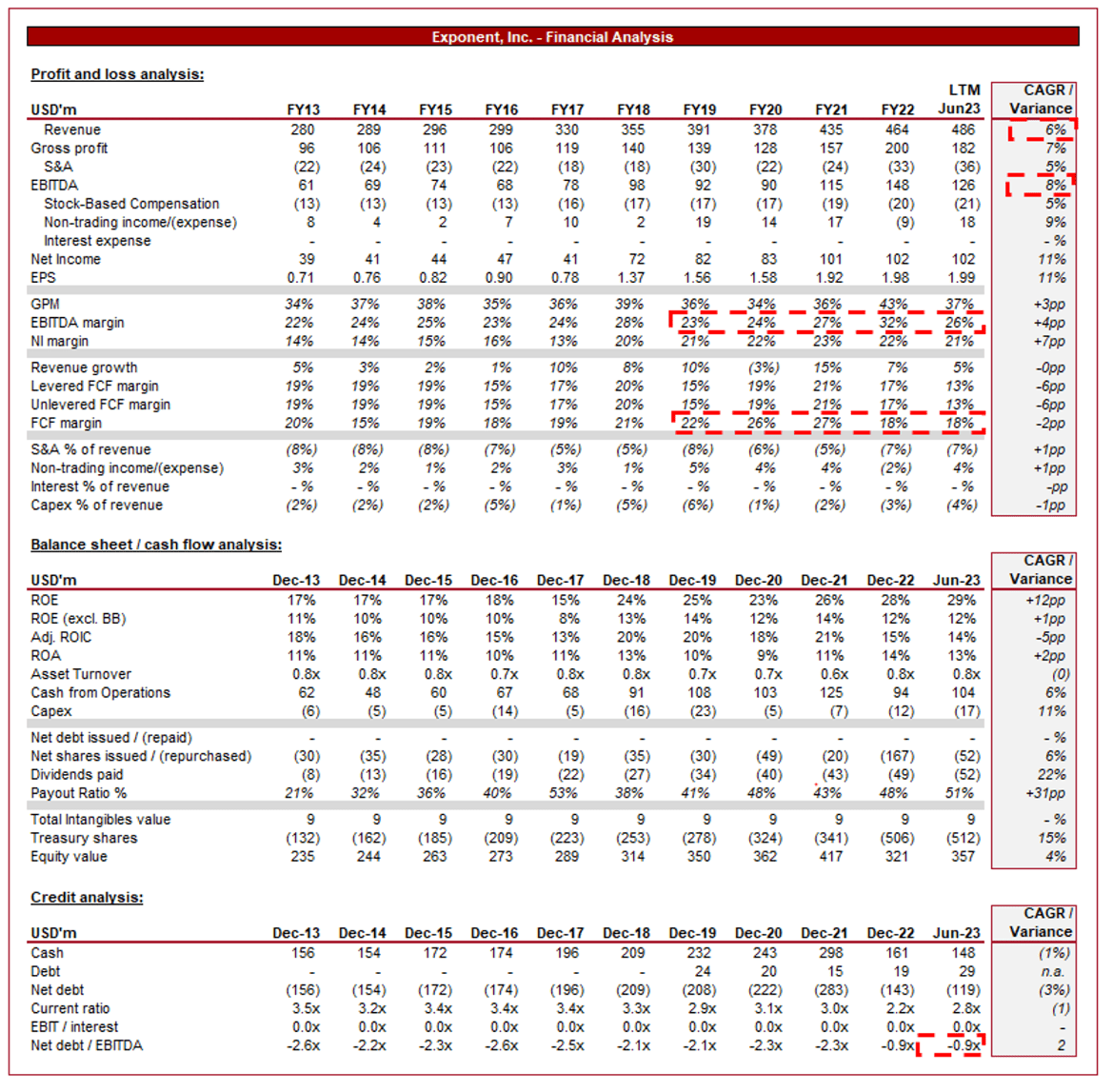

Presented above are Exponent's financial results.

Revenue & Commercial Factors

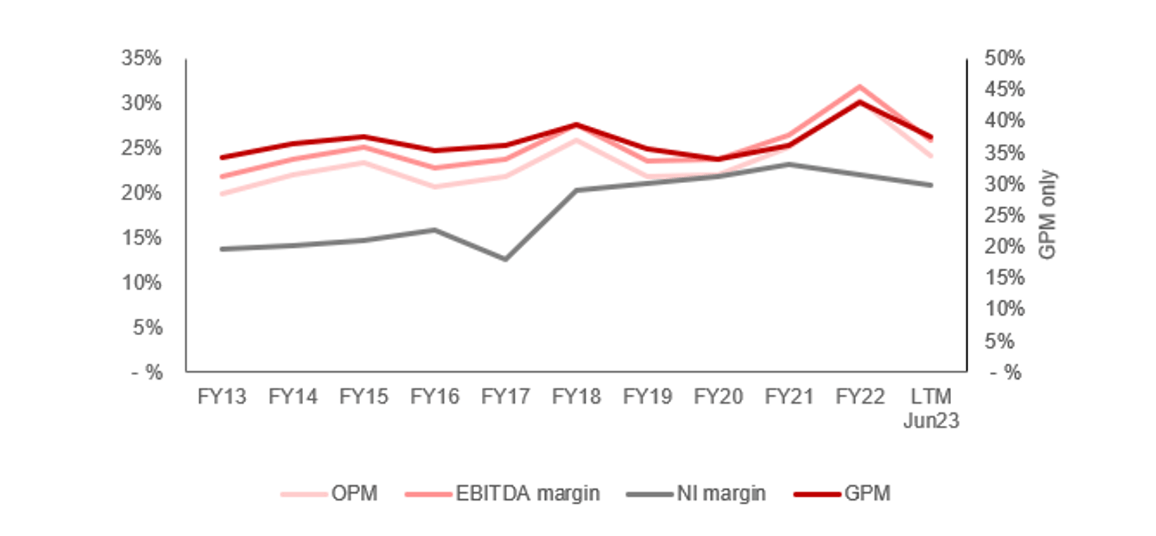

Exponent’s revenue has grown at a CAGR of +6%, with broadly consistent gains YoY. There has been a clear improvement in growth following FY17, with the only disruption being the pandemic-impacted year. The most impressive achievement is EBITDA growth, which has exceeded revenue by 2ppts, with moderate margin improvement.

Business Model

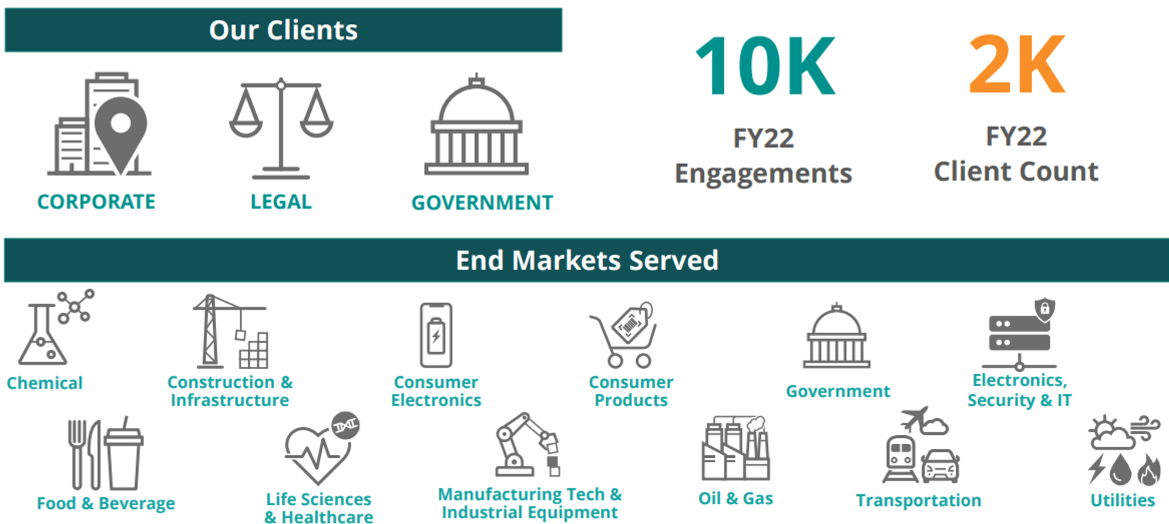

Exponents offers consulting services to a broad client base, including corporations, law firms, government agencies, and insurance companies. These services involve analyzing, investigating, and providing expert opinions on technical and scientific matters, with a focus on areas of high complexity. The company currently boasts c.2k clients and c.10k engagements across a range of industries.

{kind=link}

Exponent is expected to solve technical problems, investigate accidents, assess product failures, and offer expert opinions in legal disputes. Their work helps clients make informed decisions and resolve complex issues, contributing to lucrative contracts. Exponent is positioned well to consistently win project as clients seek consultants who have a strong track record of beneficial solutions in the specific area in question.

The firm conducts research and in-depth analysis to understand the root causes of incidents, failures, or technical challenges. This involves extensive data collection, experimentation, and modeling. This has allowed the company to develop a repository of proprietary knowledge and experience, positioning the business well to pitch for high-value projects and deliver leading results.

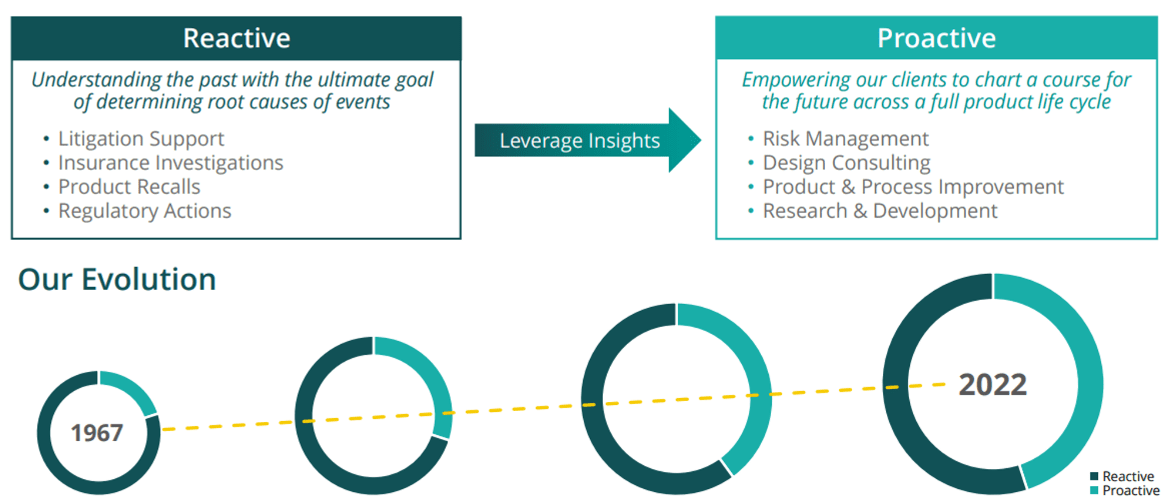

The company has leveraged its deep expertise and knowledge/experience from historic projects to develop its business model toward Proactive services. These have allowed the company to deepen its relationship with clients through progressive support, contributing to a greater proportion of recurring revenue and more consistent revenue YoY.

{kind=link}

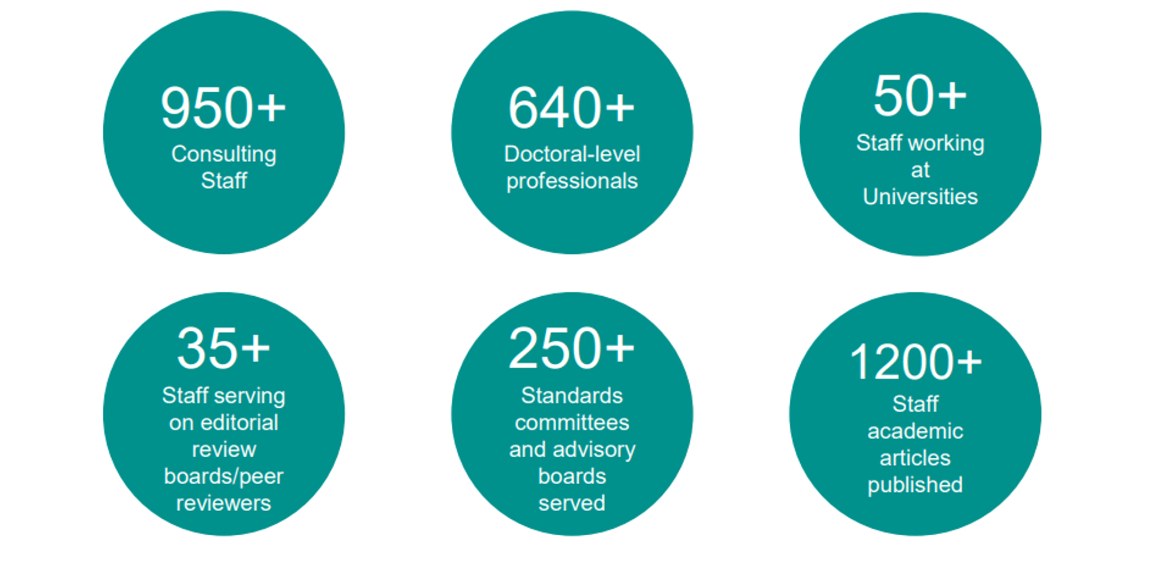

Exponent employs a diverse team of experts, including engineers, scientists, statisticians, and consultants with specialized knowledge in various fields. Exponent is highly selective with recruitment, talent identification, and invests heavily in continuous training. All of which are to ensure they have a highly competitive workforce in what is a industry of human capital.

{kind=link}

Exponent has expanded its global presence, allowing it to serve clients internationally and tap into a broader market. This has increased its revenue potential and also further enhanced its reputation. Finally, this is a critical requirement to win large contracts, as many projects will involve cross-border dynamics.

{kind=link}

The combination of these factors has allowed Exponent to earn high margins and achieve consistent growth. The key to the business model is its expertise and experience, both of which have been developed over a significant period of time, and are a combination of internal capabilities and attracting high-quality talent. In conjunction with this, the business has a strong reputation.

Consulting Industry

The consulting industry is highly competitive, although the rapid increase in consultant usage globally has contributed to healthy demand shared among a number of leading global brands and boutiques. Exponent, however, operates within a niche, particularly when considering its industry focus (acknowledging that it does broadly service a large number of industries).

Exponent competes with other consulting firms that offer technical and scientific expertise. Key competitors include Ramboll Group, RPS Group, and Golder Associates.

We believe the following megatrends will be key value drivers in the years to come:

- Life Sciences, Healthcare, and Chemicals - This is an important set of industries for Exponent, with a unifying range of trends driving these very different industries. Investment in development has accelerated during the last decade, driven by economic development and growing wealth. This creates the scope for greater litigation, regulatory consulting, and product design consulting. These are highly protected and extremely complex industries, with little scope for error. This is where Exponent thrives.

- Electrification and Automation - With technological development contributing to fundamental changes in industries such as the Automotive market, the demand for Battery performance and safety studies will grow. There is also scope for increased litigation, both at a corporate level and by consumers.

- Consumer Electronics - Technological development in the consumer segment continues to be high, with economic growth globally contributing to strong incentives to create new products. The scope for litigation and user experiences will continue to be high.

- Infrastructure and Utilities - Western nations have underinvested in infrastructure for an extended period. When considered in conjunction with the energy revolution, the scope for increased client and risk studies is high.

From these trends, there is a clear overarching point that continues to be repeated. Development. As society becomes more complex, and invests more in finding new solutions, Exponent is positioned to benefit through supporting its clients. The company’s focus on robust industries where development is constant means its long-term runway for growth is high.

Margins

{kind=link}

Exponent’s margins have trended up during the last decade, although is below its all-time high. The margin improvement is a reflection of operating cost leverage, with S&A spending declining as a % of revenue. This is a simplistic reason, however, as GPM has also improved. Exponent has been able to charge clients more for its solutions, in part due to the development of Proactive services. We suspect there is still further scope for margin improvement, although we conservatively suggest the current levels are maintainable into the medium term.

Quarterly results

Exponent has continued its strong financial performance, with top-line revenue growth of +6.2%, +7.9%, +9.2%, and +9.7% during the last 4 quarters. This is an impressive result given the current economic conditions, reflecting the resilience of its business model.

The key takeaways from its most recent quarter are:

- Growth was driven by robust demand for its reactive services, including product safety engagements and disputes-related work spanning multiple industries.

- The proactive segment benefited from increased demand in the chemicals and life sciences industries. This is a reflection of the benefits of diversification, as the company has faced some weakness in the electronic sector but this has been wholly offset.

- The company had accelerated its recruiting during the last year. This has been combined with lower-than-expected staff turnover, contributing to a 15% increase in headcount. Given the quality training and thorough recruitment, we believe this will support improved growth in the coming years.

Overall, this is another quarter of “business as usual”. The company continues to perform exceptionally well, with little volatility.

Balance sheet & Cash Flows

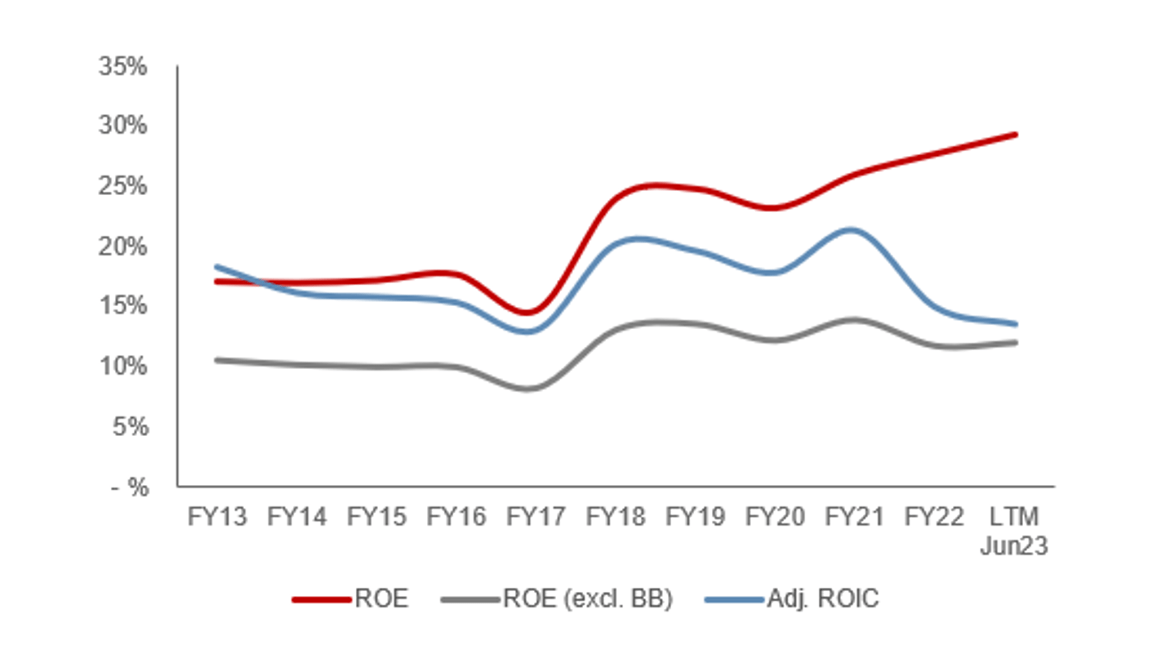

Exponent’s balance sheet is broadly clean. The company utilizes no debt due to its impressive FCF-M, which has consistently exceeded 18% since FY16. This is a remarkable feat and a primary reason why its share price has performed this well. These cash flows have been reinvested within the business, as well as distributed to shareholders, through both dividends (growth at an average 22% rate) and buybacks.

This consistency is also accretive, with the company’s ROE broadly improving over the historical period. Even when excluding the impact of buybacks, ROE has stepped up. All metric remains well above the COE.

{kind=link}

Outlook

{kind=link}

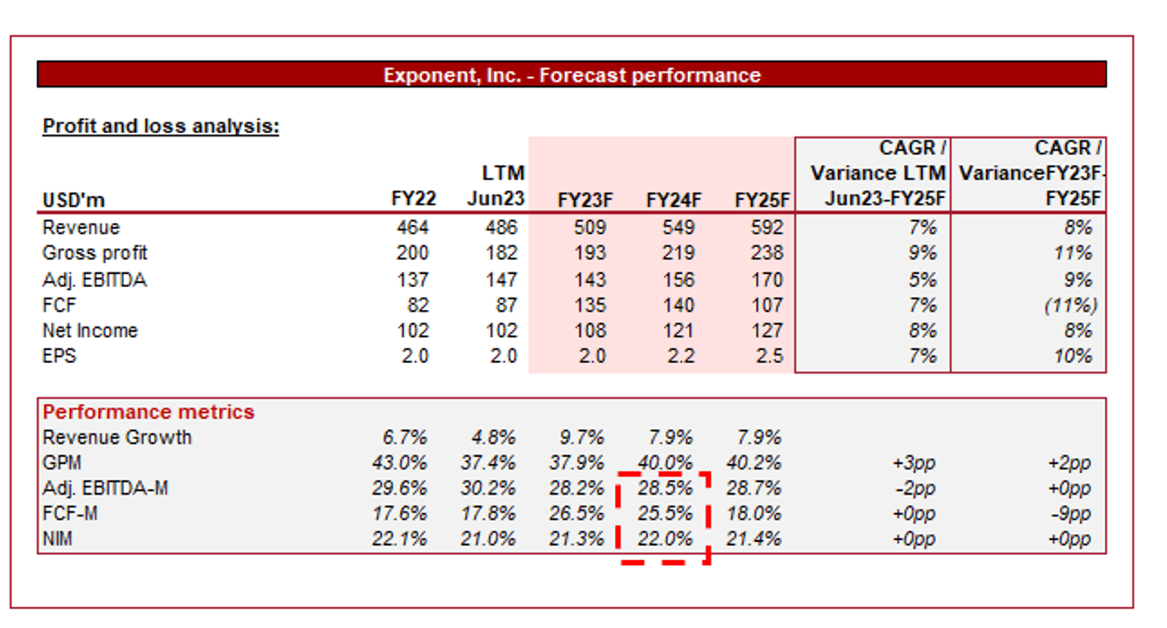

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of the company’s growth trajectory, with a CAGR of 7% into FY25F. In conjunction with this, margins are expected to remain broadly flat.

We consider both assumptions reasonable. Revenue growth is showing no evidence of slowing, and if anything, is accelerating. Further, the commercial strength of the business and industry tailwinds are broadly at the same level.

Margin assumptions are more difficult to conclude on given Exponent has seen some variability. Analysts are likely taking a conservative view that the normalized level is in line with the current year, rather than expecting further improvement. We concur with this given the steep drop between FY22 and LTM on a definitional basis.

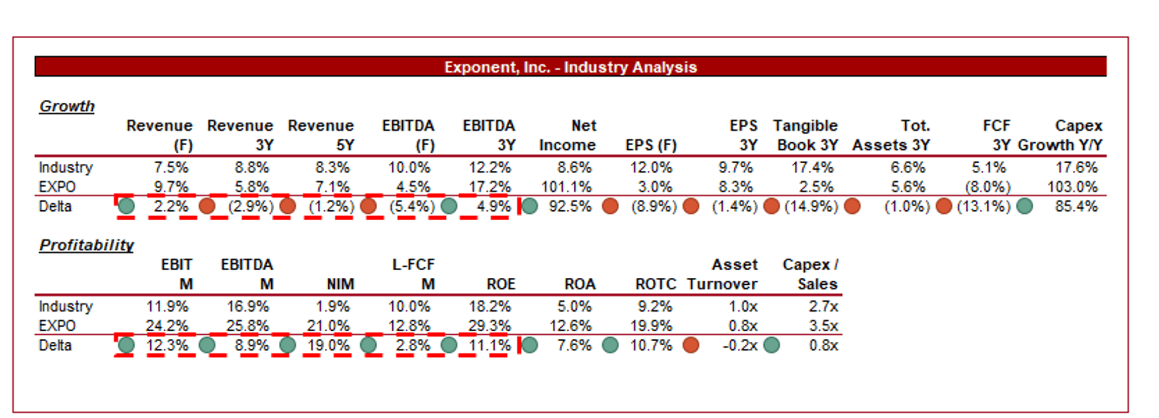

Industry analysis

Research and Consulting Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Exponent's growth and profitability to the average of its industry, as defined by Seeking Alpha (29 companies).

Exponent performs moderately well, without being a definitive standout. The company’s revenue growth has lagged the market, as has many of the profitability growth metrics, illustrating the relative growth rates of the industries it targets compared to its peers. We do not consider this below-average rate an issue with Exponent but more so a reflection of the more specialized nature of the services it provides and the industries it targets.

Exponent’s area of strength is its margins, with a substantial premium relative to its peers. The company has an EBITDA-M positive delta of +9ppts, +19ppts at a NIM level, and +11ppts on a ROE basis. This is a reflection of its specialized services and deep expertise, allowing it to command a premium price. It should be stressed how impressive this performance is, given many of its peers operate a wholly recurring revenue profile based on research.

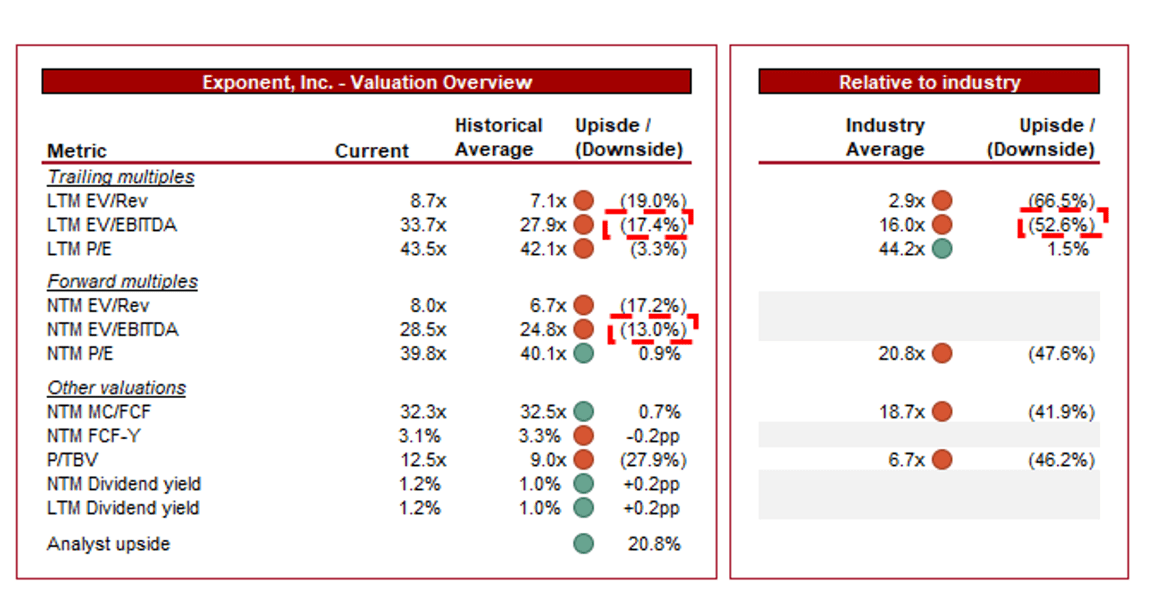

Valuation

{kind=link}

Exponent is currently trading at 34x LTM EBITDA and 29x NTM EBITDA. This is a premium to its historical average. With a valuation such as this, a material level of risk and judgment is based on the sustainability of its current growth trajectory. Based on our analysis of its industry and business model, we broadly concur with the view that Exponent can maintain its HSD growth.

A premium to its historical average is warranted in our view, owing to the improved margins achieved, enhanced growth trajectory, and ability to develop expertise at a greater scale.

Further, it is trading at a premium to its peer group on both an LTM EBITDA basis and a NTM P/E basis. We are supportive of this also, owing to its substantial margin superiority and also its resilient business model. The company is unlikely to see material fluctuations in revenue generation, while showing an ability to incrementally win new work.

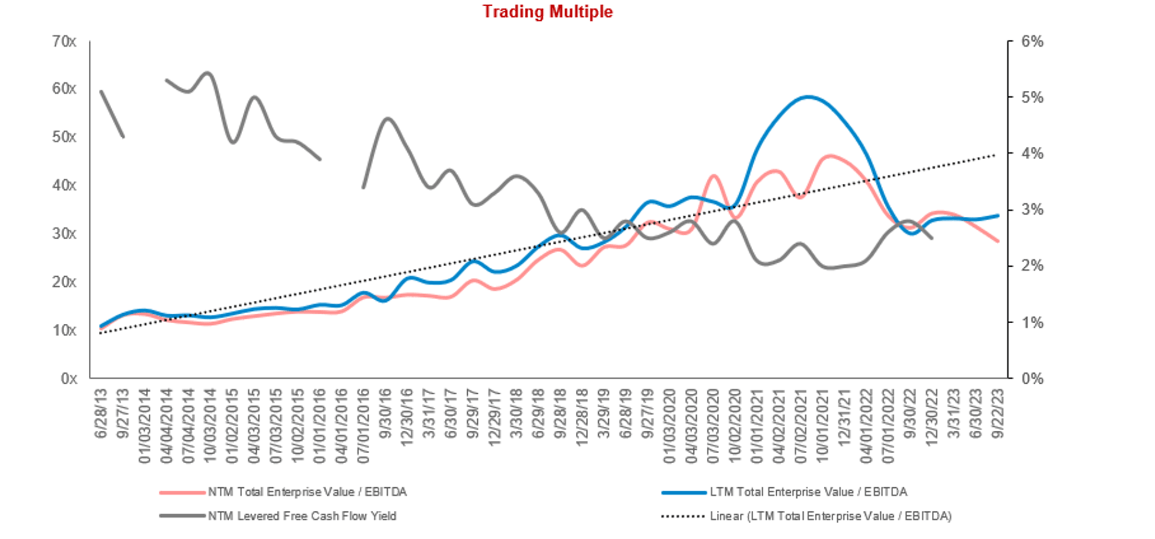

With this in mind, however, the degree to which the premium is present is key. As the following illustrates, its valuation trajectory has been monumental, although there has been a rerating following 2021/22, likely in conjunction with the market weakness. What makes us cautious is that its FCF yield has declined while multiples have increased, which is not an ideal trend.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Growth sustainability - Both risks identified center around Exponent’s ability to maintain the status quo. With high valuations come little margin for error while equally allowing for continued value by just doing what it has already done. We believe the industries it is targeting will sustain their current growth trajectory and so the onus is on Exponent to continually win work.

- Increased competition - With its substantial margins, market theory suggests new entrants are inevitable. Although the company has deep expertise and valuable processes/IP, it is inherently a business driven by human capital. This means the risk of staff being poached or even (v. unlikely), a team being carved out.

Final thoughts

Exponent is a fantastic company. Its competitive advantage is built on deep expertise, several decades of successful projects for high-profile clients, and a global brand. Beyond this, its financial performance is enhanced by its business model and industry, with a range of solutions servicing highly lucrative industries with robust demand.

In the years to come, we suspect continued internal investment and industry “megatrends” will ensure Exponent’s exceptional performance is maintained. Good companies are rarely cheap but fantastic companies never are.

For further details see:

Exponent: Highly Profitable Business With A Wide Moat