EXPO - Exponent: Largely Mixed With A Positive Bias

2023-12-19 14:40:42 ET

Summary

- Exponent Inc. is a 55-year-old company that provides engineering and scientific consulting services to global clients.

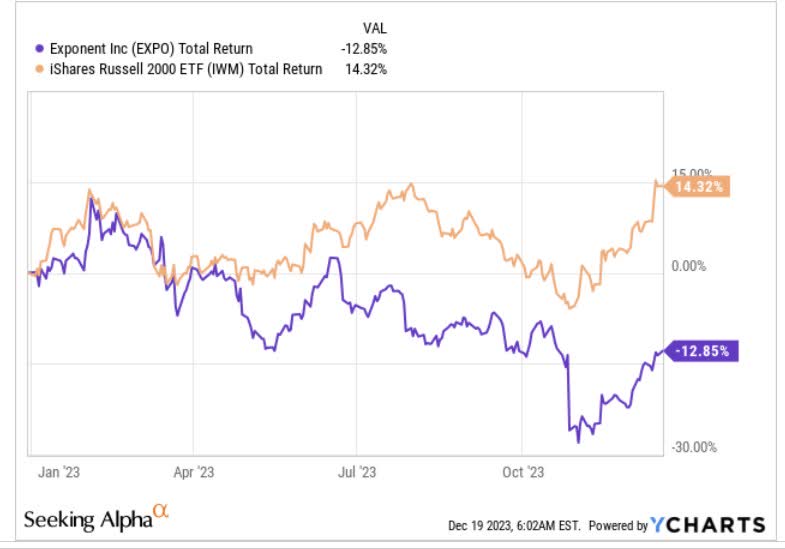

- The company has seen sub-par performance in 2023, with its stock slumping by 13% while its peers delivered 14% returns.

- Weak conditions in the consumer electronics segment could continue to impact sales, but cost adjustments are expected to improve its EBITDA profile with potential margin improvement of 100bps till FY25.

- We like the dividend theme and the valuation on offer.

- The charts are not too compelling or distressing, implying fair risk-reward.

Company Snapshot

Exponent, Inc. ( EXPO ), is a 55-year-old company that has been providing premium engineering and scientific consulting services for global clients, which it renders via 950+ consulting staff which include scientists, engineers, physicians, and business consultants. Even though EXPO’s advisory services are tapped by a plethora of industries, it is predominantly utilized by industries such as consumer products, energy, utilities, transportation and chemicals. The company reports under two divisions; Engineering and other scientific which account for 83% of group sales, and environmental and health which account for 17% of group sales.

Sub-Par Performance This Year

2023 has been a rather forgetful year for EXPO; on a YTD basis, the stock has slumped by 13% whilst its peers from the Russell 2000 have ended up delivering 14% returns during the same period.

{kind=link}

Conditions In The Consumer Electronics Segment Could Weigh Heavily

Even though EXPO offers some useful exposure to a range of industries, one shouldn’t dismiss the impact of subdued conditions in the consumer electronics space, as revenue from this segment accounted for the largest chunk of total revenue last year ( 31% ). As long as conditions here remain weak, EXPO may struggle to gain meaningful traction.

In the recently concluded Q3, note that consumer electronics was a -$8m drag on the topline; in percentage terms, that translated to an unfavorable 6-7% YoY hit. The CFO warned that investors ought to expect a similar percentage impact in Q4 as well, although once we get 2023 out of the way, you may see a tenuous return of services such as product development consulting, as management also implied that the pipeline was showing signs of convalescing and some projects that were pushed back could come to the table.

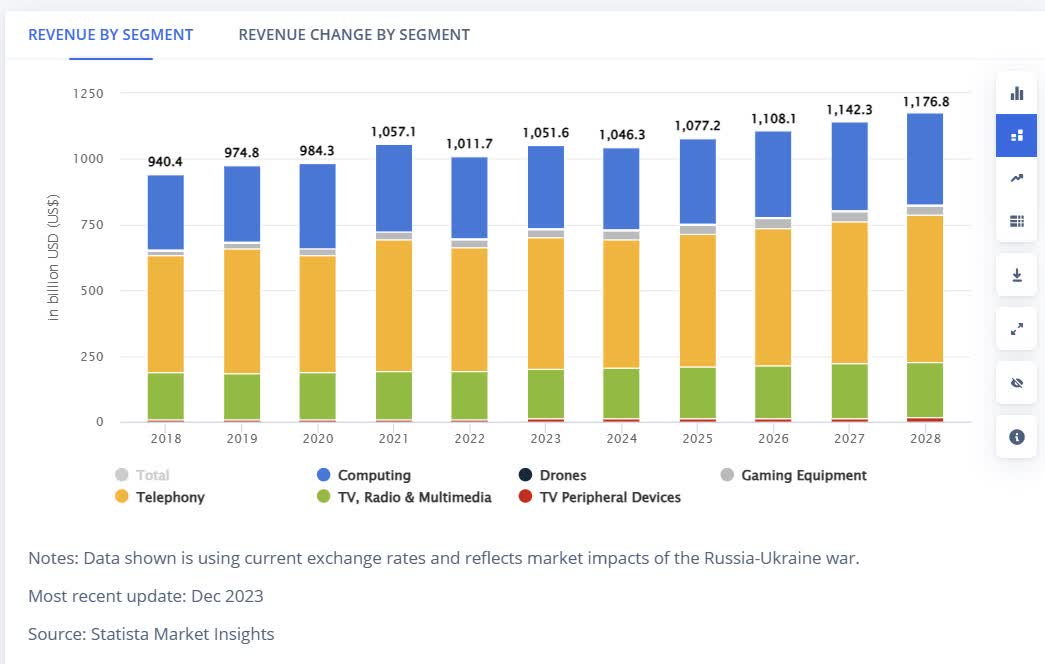

Nonetheless, it’s also worth noting that a study by Statista suggests that the global consumer electronics market which hit peak levels of sales of $1.057bn will likely only top that level in FY25, so don’t expect any fireworks in FY24. Rather it could just be steady progress at least through H1 before the low base kicks into effect in H2.

{kind=link}

Alternatively, EXPO would also be hoping for sustained resilience in terrains such as transportation (13% of group sales last year) where enquiries around EVs and ADAS-related litigation work remains quite active.

Even otherwise, EXPO deserves some credit in that even though its largest market is in a slump, it has still managed to increase its total billable hours by 4% for the first nine months of the year. This reflects the importance of its expertise in some of the other sub-markets (including transportation) such as utilities, energy, chemicals, etc.

Cost Adjustments Are Poised To Reflect Well on The EBITDA Profile Going Forward

Whilst the revenue profile may not necessarily be in fine fettle, EXPO’s investment case is somewhat abetted by what it's doing on the cost front. Since this is a consulting business, the primary focus ought to be on the employee front, and here we’ve seen EXPO management trim its FTE (Full-time equivalent) employees by 2.5% in Q3 (on a sequential basis).

The expectations are now for another 2% sequential cut in Q4 as well, as management seeks to ensure their headcount is in close alignment with the subdued demand environment. Ongoing actions on this front should help boost the utilization rate which had dropped to 70% as of September 2023 (versus 75% a year ago).

To get a sense of how this pans out in the years ahead, one may consider looking at the texture of sell-side estimates for EXPO through FY25. From FY23 to FY25, YCharts suggest that EXPO’s topline will likely grow at 8.2% CAGR, but because of the cost actions and improving utilization, the EBITDA runway for the same period is expected to be over 200bps better, translating to a CAGR of 10.3%! Meanwhile, the company's EBITDA margins too are poised to increase by 100bps over the next two years.

YCharts

Valuation Considerations

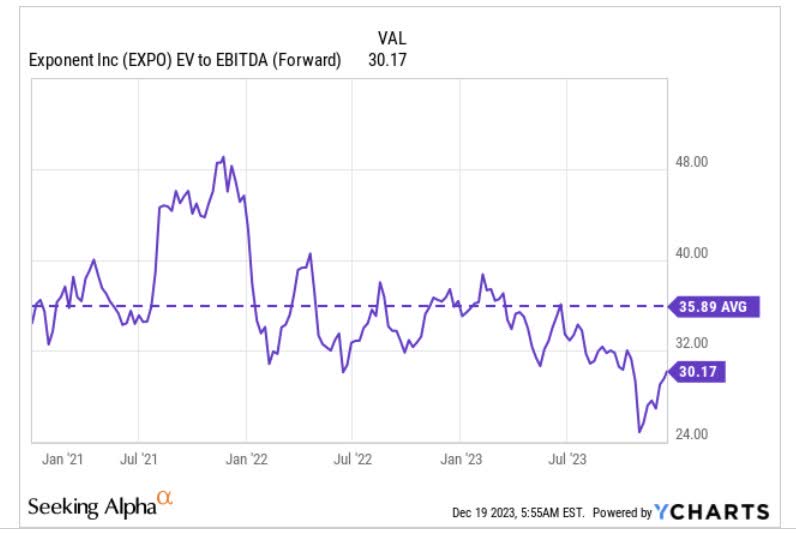

Prima facie, if you pass a cursory glance at Exponent’s valuation multiple in isolation, one may be inclined to think that it’s too exorbitant; basically, you're looking at a business priced at an EV/EBITDA of 30x, even after considering that this is a business with a net cash position of over $100m (in effect, the lack of financial leverage is compressing the EV even further).

Nonetheless, we think a 30x EV/EBITDA business such as EXPO should not be dismissed as its EBITDA profile is rather compelling. Compared to the average EBITDA margin of a little less than 10% for the research and consulting services industry, EXPO’s EBITDA profile stands quite tall at 25-30%, and is one of the best in this business.

Crucially also note that the current multiple actually translates to a -16% discount to the stock’s long-term average of 35.89x!

{kind=link}

Useful Distribution Theme

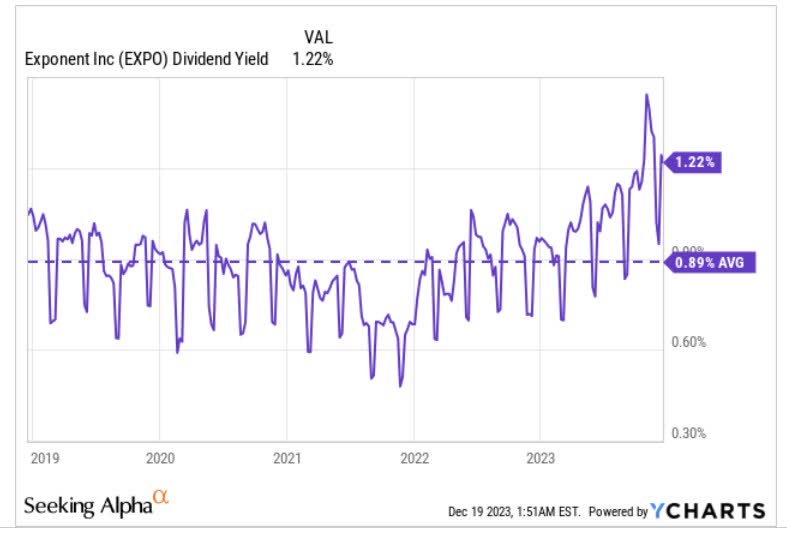

The EV/EBITDA reading may also be supplemented with what the dividend yield is suggesting, as after all, this is a business that has been growing its dividends for 10 straight years since 2013. Typically, over the last five years, the stock has yielded an average of 0.89%, but if you enter at current levels you could be locking in a superior figure of 1.22%.

{kind=link}

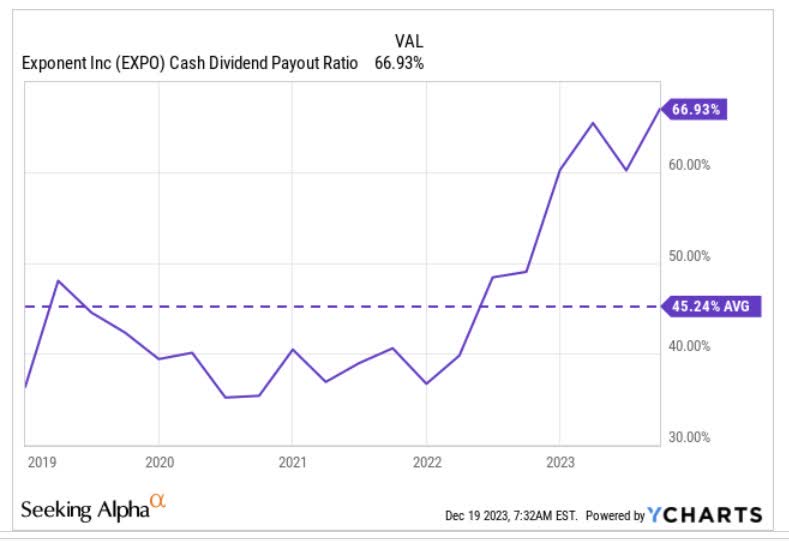

It’s also heartening to note that, EXPO has over time become increasingly generous in doling out a larger chunk of its free cash flow as dividends. This is captured by the cash dividend payout ratio which has averaged around 45% over the past five years, but currently is at 5-year highs of 67%!

{kind=link}

Closing Thoughts- Technical Considerations

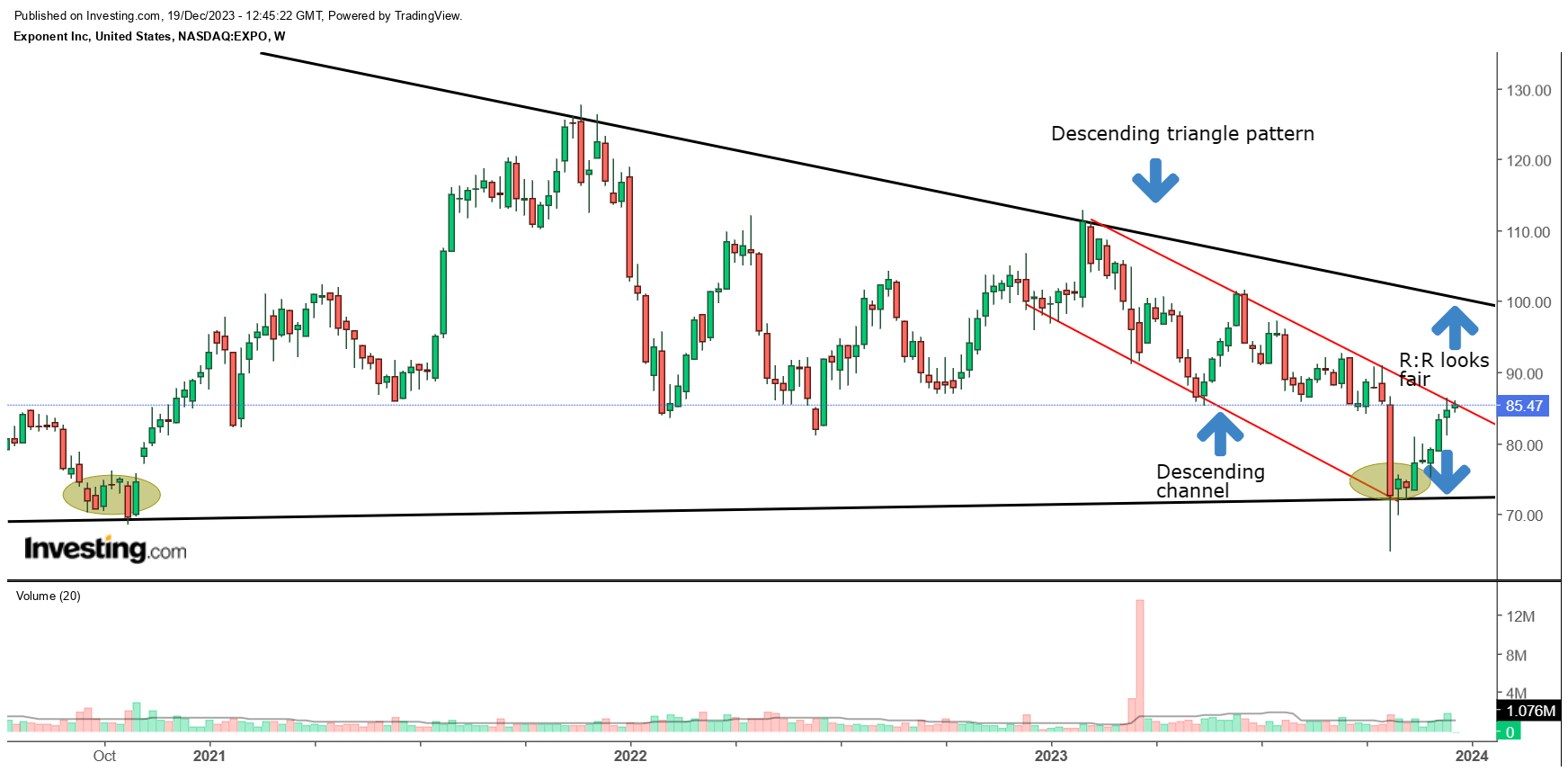

Switching focus to the charts, we first start with EXPO's weekly price patterns for the last 40-odd months. Basically what we can see is that the price has trended in the shape of an approximate descending triangle pattern with a rather flattish support, and a downward-sloping resistance.

{kind=link}

In October and November, it was heartening to see the stock take support at levels last seen during September-November 2020, but after a decent enough comeback to the +85 levels, it now looks like we have equidistant spaces between the price and the triangle boundaries (the two black lines), implying fair risk-reward.

Separately within the triangle, you also have an intermediate descending channel pattern (red lines), and it is not too ideal to see the stock perched right around the upper boundary of the channel.

Finally, if you’re someone who’s looking for suitable rotational opportunities within the industrial space, we are not sure EXPO represents the best bet as it relative strength ratio versus the Vanguard Industrials ETF is now on par with the mid-point of its long-term range.

{kind=link}

For further details see:

Exponent: Largely Mixed, With A Positive Bias