EXPO - Exponent: Time To Lower Expectations - High Growth Is Likely Over

Summary

- Shareholders that got in when the price was low have enjoyed some solid returns from EXPO, but the valuation of the company is now extremely high.

- If I already had a position in the company, I would probably keep it, although taking some profits off the table at this time would reduce downside risk.

- Being a thinly traded stock, when a little more volume comes in, it can have a disproportionate impact on the firm.

- While I think the company will probably generate incremental growth going forward, there are a lot better stocks that will deliver better growth and income.

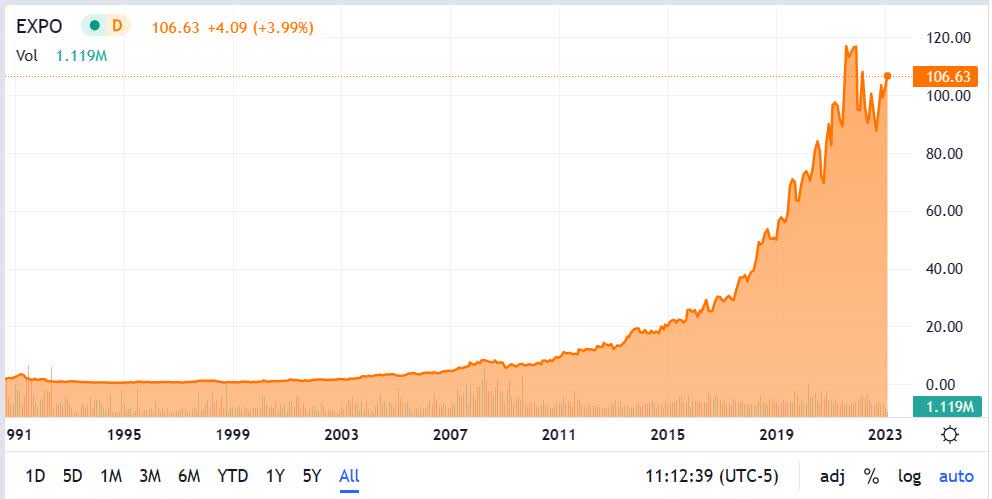

Exponent, Inc. ( EXPO ), a company that competes as a science and engineering consulting company on a global basis, has generated extraordinary returns for long-term investors, if you want to go back to around the turn of the century.

Even if looking at a 10-year chart, the company has done very well for shareholders, being up over 9x since February 2013, when it traded at approximately $11.50 per share.

The company has been growing at a steady pace while generating consistent, positive net income, but I see the company approaching the top end of its valuation for now, with not a lot of room for long-term growth that would come close to matching some of its past performance.

Since reaching a 2-year high of about $127.50 on November 22, 2021, the stock has traded very volatile, with the company struggling to break out in any sustainable manner.

{kind=link}

I think shareholders have started to take profits on the stock, and with the share price still trading very high, I don't see any reason for investors to take a position at this time, as the risk/reward is not favorable for those opening a position in the company.

The bottom line for this stock is its best days are over in regard to growth, and the one thing that it still has going for it is consistent earnings and cash generation, which I think should start being applied even more to the dividend in order to make it worth taking a position in.

In this article, we'll look at its recent numbers, valuation, and what is likely to happen in the future with the stock.

Some of the recent numbers

Total revenue in the fourth quarter of 2022 was $127.4 million, up 12.2 percent from $113.5 million in revenue generated in the fourth quarter of 2021, beating by $15.93 million. Net revenue (before reimbursements) in the fourth quarter of 2022 came in at $112.6 million, compared to net revenue of $104.3 million in the fourth quarter of 2021.

Net income in the reporting period was $22.5 million, or $0.44 per diluted share, compared to net income of $20.4 million or $0.38 per diluted share in the fourth quarter of 2021.

EBITDA in the fourth quarter was $31.1 million, or 27.6 percent of revenue before reimbursements, compared to EBITDA of $30.2 million, or 28.9 percent of revenue before reimbursements in the fourth quarter of 2021.

Total revenue for full year 2022 was $513.3 million, up 10.1 percent year-over-year, and net revenue was $463.8 million, an increase of 6.7 percent over last year in the same reporting period.

Net income for full year 2022 was $102.3 million, or $1.96 per diluted share, slightly up from $101.2 million, or $1.90 per diluted share for full year 2021.EBITDA for all of 2022 climbed to $137.2 million, or 29.6 percent of revenue before reimbursements, compared to $132.3 million, or 30.4 percent of revenue before reimbursements, for full year 2021.

For full-year 2023, the company guides for revenue before reimbursements to grow by the high-single to low-double digits level, with EBITDA to be in a range of 27.5 percent to 28.2 percent of revenue before reimbursements.

At the end of 2022, the company had cash and cash equivalents of $161.5 million.

Performance by segment

The bulk of revenue in the reporting period, as usual, came from its Engineering and Other scientific segments, which generated 83 percent of net revenue in the fourth quarter and full year 2022. Net revenue in this segment was up 10 percent sequentially, and up eight percent year-over-year.

Categories driving growth in the segment for the quarter were automotive, consumer products, electronics, and life sciences.

In its Environmental and Health segment accounted for the remaining 17 percent of revenue in the fourth quarter and full year of 2022. Net revenue in the fourth quarter was down 2 percent from the fourth quarter of 2021. Not including the impact of FX on the segment, revenue was up two percent in the fourth quarter, and up four percent year-over-year.

The primary driver in Environmental and Health for the fourth quarter was work associated with human health and environmental safety.

Increase dividends or share repurchases?

When looking at most companies, if the question is asked concerning whether a company should focus on boosting dividends or repurchasing share, most investors would probably reply - do both.

While that's probably the best way to look at it in most situations, I think in the case of EXPO, management may need to rethink how it returns cash to investors.

For example, over the last year, the company repurchased $155.9 million in stock while paying out $49.2 million in dividends. With its share price struggling to gain traction over the last couple of years, this was an attempt to shore it up, yet it has achieved little in the way of results in response to the repurchases.

My view is the company would do better to allocate more capital toward boosting its low-yield dividend, rather than repurchase shares. My reasoning behind that is, at this time, the company's upward growth trajectory is now far behind it. For that reason, I think investors would prefer to see more income than potential incremental growth in its share price.

The company can no longer compete with other growth companies, and I think the best way to create shareholder value is to transition primarily to an income stock, as its high growth days are behind it.

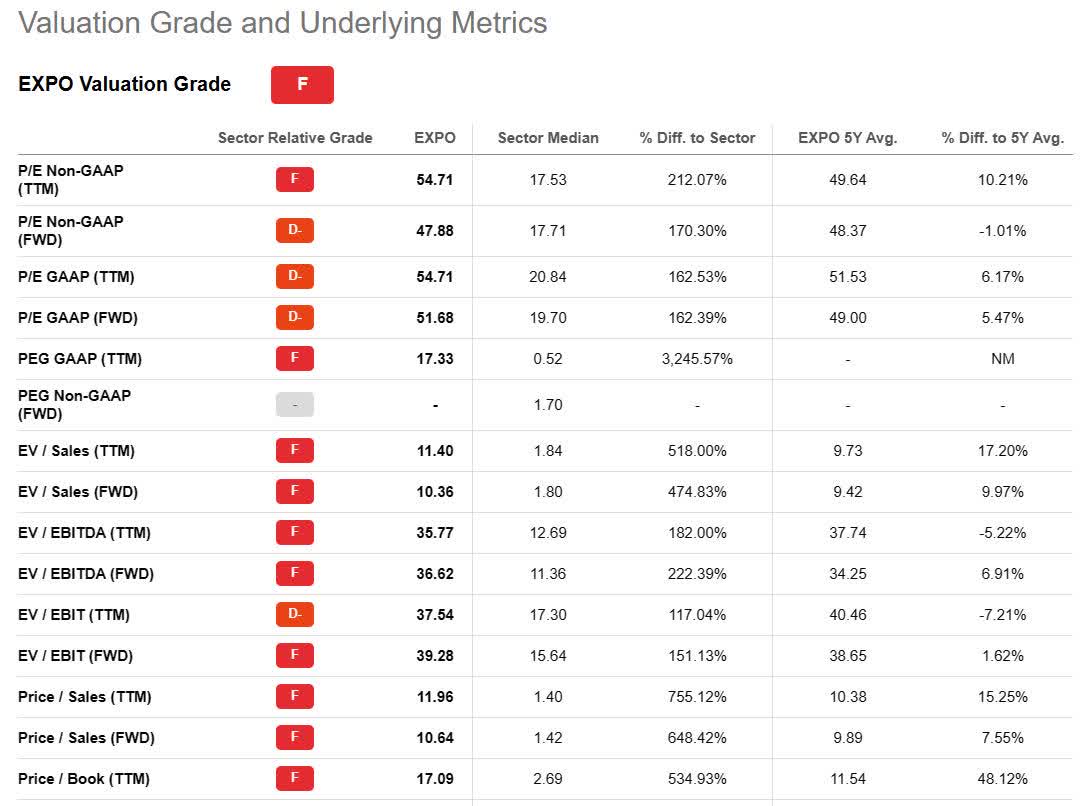

Valuation

As for valuation, I'll let the data below speak for itself. By every metric, the company is highly overvalued, and no amount of moderate earnings growth changes that reality.

{kind=link}

Conclusion

When taking EXPO into consideration, it should be understood that its high-growth days are in the past, and going forward, the focus should be on returning capital to its shareholders; especially in regard to boosting dividends.

That doesn't mean the company won't have any growth left in it, but whatever growth it does have will be incremental growth, and when considering its high valuation, it could be primed for a major correction if shareholders start taking profits at a high rate.

Where the company stands today, it doesn't offer a favorable risk/reward setup, and those taking a position at these price levels could find themselves underwater for a prolonged period of time. And with a dividend-yielding less than one percent as I write, there's no real compelling reason to take a position in EXPO.

For further details see:

Exponent: Time To Lower Expectations - High Growth Is Likely Over