XPRO - Expro Group: International Offshore Projects Present Upside

2023-12-12 17:38:45 ET

Summary

- Expro Group Holdings has seen a sharp turnaround in international offshore deepwater activities, evidenced by a four-year contract in Norway and the acquisition of PRT Offshore.

- The energy services industry is expected to strengthen in 2024, with increased demand for XPRO's subsea interventions and vessel-deployed LWI solutions in various regions.

- XPRO faced challenges in Q3, including reduced activity and weaker pricing for onshore tubular running services, as well as an accident in its vessel-deployed LWI system in Australia.

XPRO Rests On Offshore Gains

I discussed Expro Group Holdings N.V. ( XPRO ) strategies in my previous article . In the past few quarters, we have witnessed a sharp turnaround in the international offshore deepwater activities. Its four-year contract related to well-flow management and production optimization in Norway is evidence of the current momentum. Recently, it acquired PRT Offshore, which will provide it access to the wellbore safely, increase efficiency, and reduce costs. It also extended the credit maturity following the recent acquisition, bringing stability to its balance sheet.

The primary challenge in Q3 was reduced activity and weaker pricing for onshore tubular running services. Increased LWI-related cost is another challenge. The stock appears to be slightly undervalued versus its peers. The current momentum should more than offset the headwinds. So, I continue to extend my medium-term "buy."

Industry Outlook

The energy services will likely strengthen in 2024. On the demand side, economic data points to a resilient condition in China, the US, and Europe, although robust storage of natural gas in Europe and slower demand growth in Asia can be a concern. On the supply side, long cycle development in deepwater development and increased project sanctioning in 2023 can lead to higher supply in 2024. The growth momentum is visible in various regions, including Norway, Angola, India, Indonesia, Brazil, and Guyana. In this scenario, XPRO's subsea interventions and vessel-deployed LWI solutions will see increased demand.

In November, XPRO inked a four-year contract to provide well-flow management and production optimization services to Equinor in the Norwegian Continental Shelf. The contract is considered to be one of Norway's largest surface well testing operations and will use the company's CoilHose Light Well Circulation System.

Key Challenges

{kind=link}

In Q3, XPRO faced a stiff challenge related to an accident in one of Expro's vessel-deployed light well intervention (or LWI) systems in Australia. Following this, the company suspended the vessel-deployed LWI operations. The company has not yet determined the time and cost required to return the system to operational status. In this context, investors may note that the expected annual revenue from the vessel-deployed LWI business ranges between $50 million and $75 million.

In North and Latin America, not only did the LWI-related costs increase, but activity also went down in the recent slowdown. In Q3, revenues from the US onshore tubular running services (or TRS) business declined by 10% due to the sustained reduction in activity and weaker pricing. The quarterly margin from this operation also fell in Q3. I think TRS capacity exceeds demand in the US onshore, which has prompted many service providers to lower pricing in view of securing a higher market share.

Response To The Challenges

XPRO has rationalized its TRS operating footprint in the US land market to overcome the issues in the TRS market. It has also redeployed equipment to select U.S. and international basins for better utilization, pricing, and returns. The drilling-related softness in the US and Latin America offshore markets also affected the company's business. However, its management anticipates a rebound in offshore activity in Q4.

The other strategy for the company was to take the acquisition route to accelerate growth. In October, it acquired PRT Offshore, which provides well completions, interventions, and decommissioning services onshore and offshore. The acquisition will provide XPRO's customers access to the wellbore safely, increase efficiency, and reduce costs.

New Projects And Backlog

XPRO has strengthened its cementing following the acquisition of DeltaTek. The acquisition supplements its low-risk, open-water cementing solutions, including pure technology. In Q3, XPRO delivered a well-cementing project in the U.S. Gulf of Mexico. In other projects, it designed and constructed an onshore LNG pretreatment facility in the Eni Congo project. The first production is scheduled for 1H 2024 here. In the Middle East and North Africa, Expro completed the installation of the Kinley check valves.

During Q3, XPRO captured $235 million in new work orders. This includes a $30 million award in an integrated service contract in Norway. The company will provide drilling, well testing, subsea, and coil host services. Its backlog increased from $2 billion in the previous quarter to $2.4 billion.

The Q3 Drivers

{kind=link}

From Q2 to Q3, the company's revenue decreased by 7%. Geographically, the North and Latin America (or NLA) division registered the steepest fall (22% down) during this period. Meanwhile, the Europe and Sub-Saharan Africa (or ESSA) and Middle East regions remained relatively steady. Asia Pacific (or APAC), on the other hand, moved impressively (10% up). The company's adjusted EBITDA margin decreased sharply (510 basis points down) sequentially in Q3 despite the LWI-related margin headwinds.

Short-term softness and structural challenges for tubular running services within the well construction in the US Gulf of Mexico contributed to the fall. Partially mitigating the fall was the Strong demand for subsea interventions and vessel-deployed light well solutions in the APAC region.

Cash Flows And Liquidity

In 9M 2023, led by a rise in revenues, XPRO's cash flow from operations turned remarkably positive compared to negative CFO a year ago. Its free cash flow also turned positive despite the increase in capex.

As of September 30, XPRO had $50 million debt related to closing the PRT Offshore transaction, although it has repaid $35 million since then. Its liquidity was approximately $350 million on September 30. It has recently amended its revolving credit facility and extended the maturity by three years.

What Does The Relative Valuation Imply?

Author Created and Seeking Alpha

{kind=link}

XPRO's forward EV/EBITDA multiple (7.8x) is expected to contract versus the current EV/EBITDA multiple (6.4x). The rate of contraction is steeper than its peers' average fall (NOV, RES, FTI), implying a higher EBITDA growth, which should translate to a higher EV/EBITDA multiple. The stock's current multiple is marginally lower than its peers' average. So, the stock is undervalued versus its peers.

The stock is trading at a significant discount to its past average. Given the recessionary fear in the US, I do not see the stock improving much in the short term. However, if the multiple expands in the medium term anywhere close to the past, it can climb sharply from the current level.

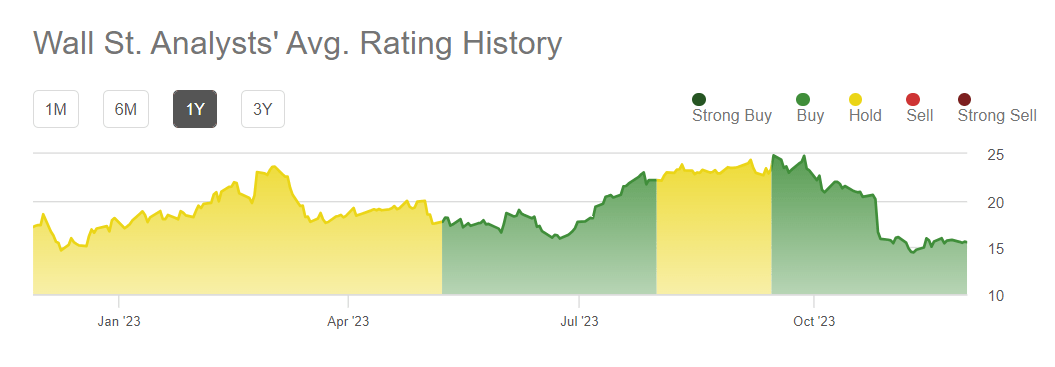

Target Price And Analyst Rating

{kind=link}

In the past 90 days, four Wall Street analysts rated XPRO a "Buy." Two analysts rated it a "Hold," while none recommended a "Sell." The consensus target price is $22.3, which has a 48% upside potential at the current price.

Why Do I Keep My Call Unchanged?

I considered XPRO a "buy" in my previous article. In Q2, the LWI system sales declined. Also, customer budget constraints were hanging over its outlook. However, well flow management, well intervention, and the integrity of product lines kept its volume steady. I wrote:

With higher approvals of the number of offshore projects, I expect the project sanctions will increase until 2030. It has also forayed into carbon capture operations. In Q2, its revenues and adjusted EBITDA increased significantly, especially in the APAC region, which shows the momentum on its side.

Given the improving dynamics in the offshore energy market, I expect subsea interventions and vessel-deployed light well intervention solutions to see increased demand. In November, XPRO inked a four-year contract to provide well-flow management and production optimization services in Norway. Cash flows can continue to improve in 2024. So, despite the lower drilling activity in the US onshore, I repeat my "buy" take on the stock.

What's The Take on XPRO?

{kind=link}

In 2024, I expect long-cycle development in deepwater and increased project sanctioning to benefit XPRO's outlook. However, XPRO suffered a setback in September when an accident occurred in Australia, and the company suspended vessel-deployed LWI operations in that region. Also, the company's onshore tubular running services came under pressure. So, the stock underperformed the VanEck Oil Services ETF ( OIH ) in the past year.

However, the energy industry balance appears to be shifting as the offshore drilling market rejuvenates. Also, the company's recent acquisitions can give it a boost. It won several new projects in Q3, which can push the topline higher in Q4 and into 2024. Given the relative valuation, I reiterate my "buy" call for healthy returns in the medium-to-long term.

For further details see:

Expro Group: International Offshore Projects Present Upside