VNQ - Extra Space Storage: Opportune Time To Buy A Best-In-Class REIT

2023-07-21 08:24:32 ET

Summary

- Extra Space Storage is trading at a 5.8% implied cap rate, the lowest in five years, and is expected to see a total return of over 20% in the next year due to the acquisition of LSI and a well-protected dividend.

- Despite underperforming the Vanguard Real Estate Index Fund by 6.7% over the past year, EXR is still trading at a 7.9% discount to its Net Asset Value and a 13.9% discount to its intrinsic Discounted Cash Flow value.

- -6.7% relative performance vs. the Vanguard Real Estate Index Fund over the past year, leaves EXR trading at a -7.9% discount to its Net Asset Value (NAV).

Summary

- Extra Space Storage (EXR) currently trades at a 5.8% implied cap rate, which is the lowest valuation in the last five years, which includes its COVID valuation (2Q20 implied cap rate was 5.6%).

- EXR shareholders are poised to see a total return in excess of 20% over the next twelve months through a combination of accretion upside from the acquisition of [[LSI]], better than expected internal growth, and a well-protected dividend.

- -6.7% relative performance vs. the Vanguard Real Estate Index Fund (VNQ) over the past year, leaves EXR trading at a -7.9% discount to its Net Asset Value ((NAV)) and a -13.9% discount to its intrinsic Discounted Cash Flow ((DCF)) value despite having delivered the best shareholder returns among all public REITs over the last 10 years.

Investment Recommendation

I recommend a BUY rating for Extra Space Storage Inc with a price target of $176, representing a 21.6% total return over the next twelve months. EXR shareholders are poised to see ~15% low-risk total returns for the foreseeable future through a combination of: (1) dividends, (2) best in class internal growth, (3) reinvested retained cashflow, and (4) capital light accretive ventures (e.g. third party management).

Near term, positive catalysts for the stock include: (1) EXR is upgraded by rating agencies post the acquisition of peer Life Storage Inc. and (2) index rebalancing for funds that follow the S&P 500 to reflect EXR's post-acquisition size (forced demand for shares).

EXR has underperformed the Vanguard Real Estate Index Fund ETF by -6.7% over the past year as self-storage fundamentals have moderated from their pandemic highs, creating an opportune point of entry to purchase EXR shares at a price that is at a -7.9% discount to its Net Asset Value ((NAV)) and a -13.9% discount to its intrinsic Discounted Cash Flow ((DCF)) value despite having delivered the best shareholder returns among all public REITs over the last 10 years.

Google Finance, Public company filings.

{kind=link}

Potential Catalysts

- EXR is upgraded by ratings agencies to reflect its new larger enterprise value after the acquisition of LSI, resulting in a lower cost of capital for EXR going forward (positive).

- Index rebalancing (e.g. S&P 500) results in increased demand for EXR's stock after the acquisition of LSI (positive).

- Earnings guidance and accretion guidance from the acquisition of LSI surprise to the upside given management's track record of guiding conservatively (positive).

- Self-storage surprises to the upside as fundamentals stabilize at levels in line with pre-pandemic demand levels (positive).

- The Federal Reserve continues to raise rates resulting in increased interest expense to EXR given 29% of its debt is variable-rate (negative).

Company Background

Extra Space Storage is a fully integrated Real Estate Investment Trust ((REIT)) that was founded in 1977 and will be the largest self-storage operator by square footage in the US after it completes its announced acquisition of peer REIT Life Storage . The company invests in self-storage properties outright (1,457 stores as of 1Q23) and manages self-storage properties for third parties (931 stores as of 1Q23). Over the past 10 years, EXR has delivered cumulative return performance of 475%, which is the strongest shareholder return among all public REITs.

Company Investor Presentation.

EXR stands out not only among REITs in general, but also among self-storage REITs. EXR has a strong track record of being a best-in-class operator, which has allowed it to grow its core FFO per share by 720.4% since 2011, more than double the peer average of 275.5%.

Self-Storage REITs Love to Under Promise and Over Deliver

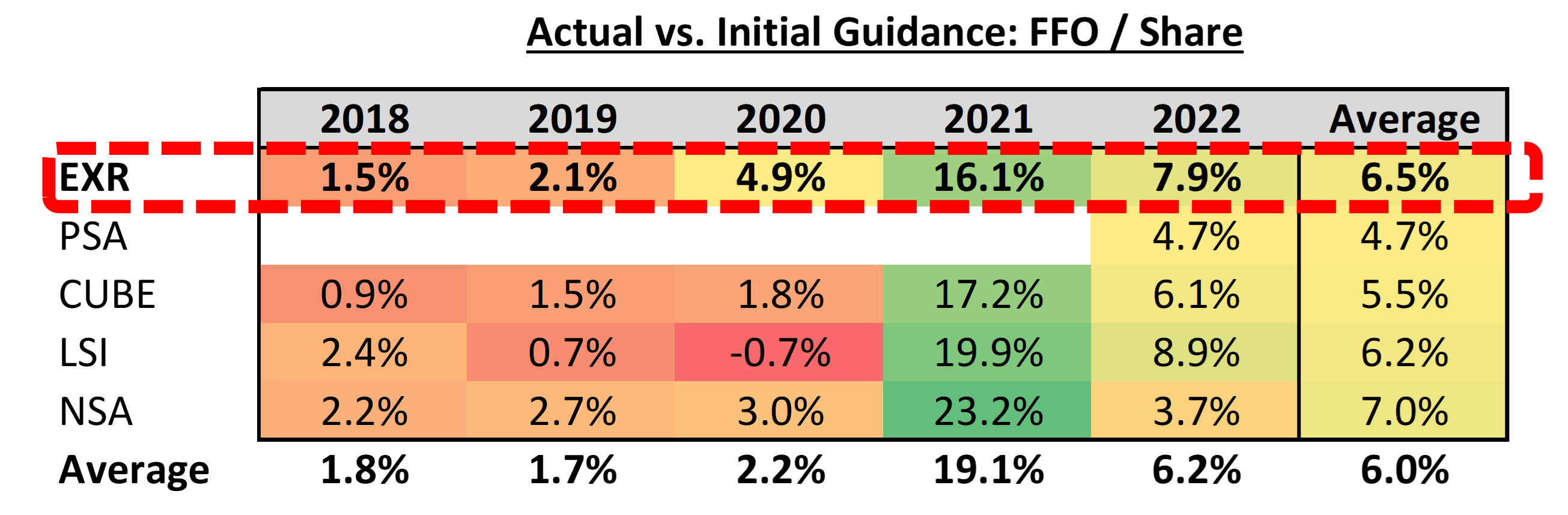

Comparing the mid-point of the initial FFO guidance range provided by management teams vs. achieved results, reveals that self-storage management teams tend to guide conservatively leading to an inevitable beat on earnings when actual results are reported.

Looking at the past five years reveals that EXR has beaten its initial FFO guidance by 6.5% on average compared to the self-storage REIT average of 6.0%. Even in FY2020, when the pandemic undoubtedly took every management team by surprise, EXR still managed to beat its initial FFO guidance by 4.9%, compared to a REIT peer average of 2.2%.

Company filings, Analyst estimates.

{kind=link}

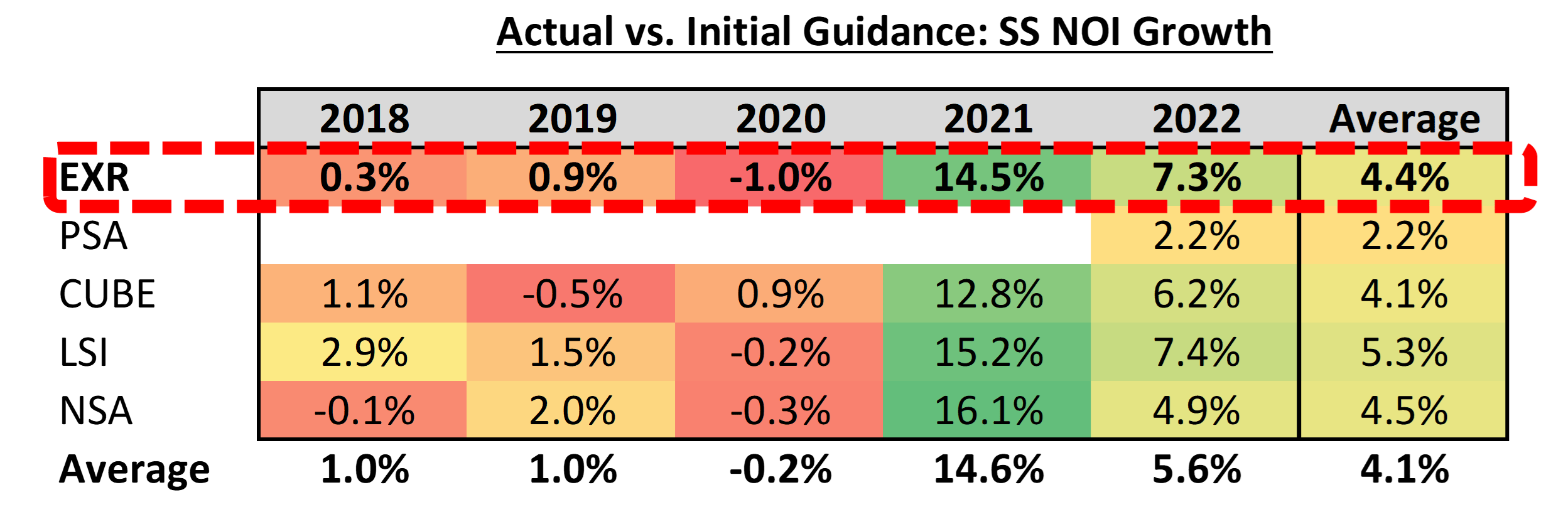

Comparing the midpoint of the initial Same-Store (SS) NOI growth guidance range provided by management teams vs. actual results over the past five years reveals a similar trend where EXR has beaten its initial SS NOI growth guidance by 4.4% on average relative to a self-storage REIT average of 4.1%. Given this trend, I think it is likely that EXR management is guiding conservatively not only in regards to its 2023 guidance estimates, but also in regards to its estimated synergies from the announced acquisition of LSI. I think 2023 is unique relative to other years in that EXR has multiple avenues in which management can surprise to the upside, which should bode well for share price performance.

Company filings, Analyst estimates.

{kind=link}

Why Public-to-Public REIT M&A Makes Sense

Given that real estate is a highly leveraged asset class, it is relatively well known that interest rates have a significant impact on real estate values. However, what might not be as apparent to the general public, is that moves in interest rates tend to be reflected in the values of publicly traded real estate securities much sooner than private real estate values. Given the unprecedented rapid hike in interest rates that we experienced in 2022, private market real estate transactions have come to a virtual standstill as potential sellers are unwilling to accept the new interest rate environment.

As publicly traded REITs have seen their share prices plunge, with a corresponding rise in capital costs, most REITs have been priced out of the private acquisition market. Funding acquisitions in private real estate markets with capital that is raised in the public market simply does not make sense from an accretion perspective. Given the unfavorable environment for one-off private real estate acquisitions, EXR, in my view, made the right decision by pursuing public-to-public M&A as it submitted a bid to acquire peer Life Storage.

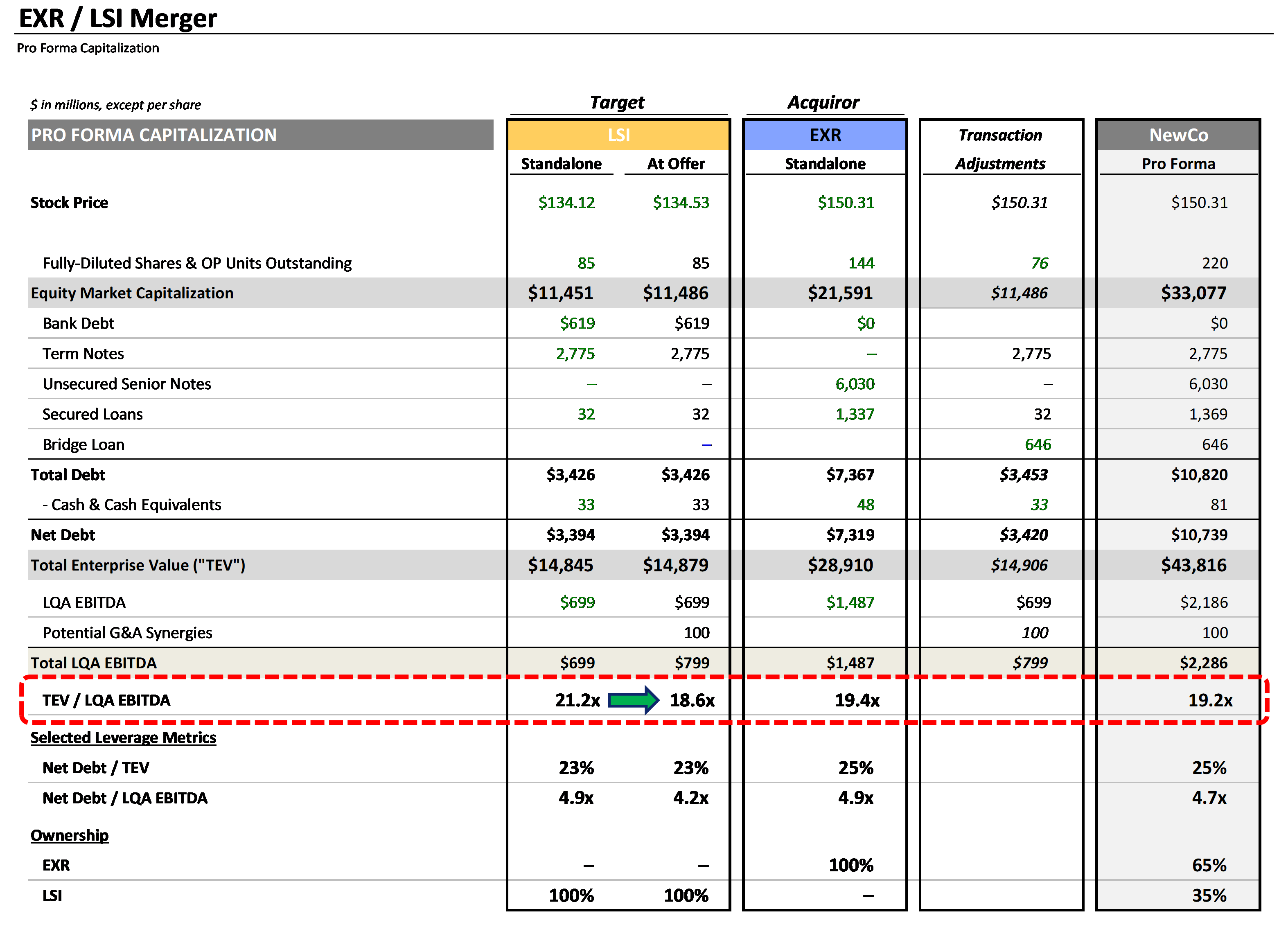

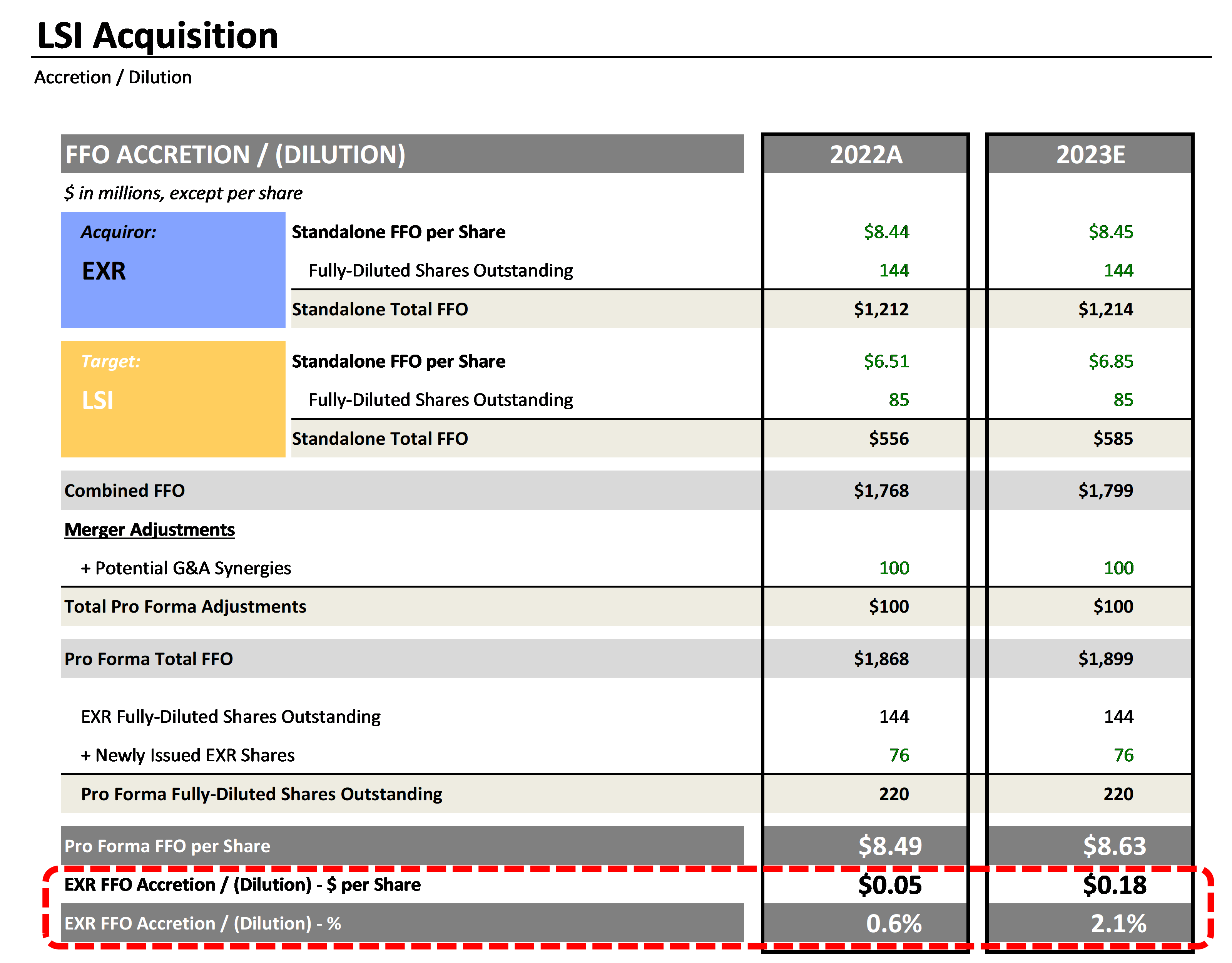

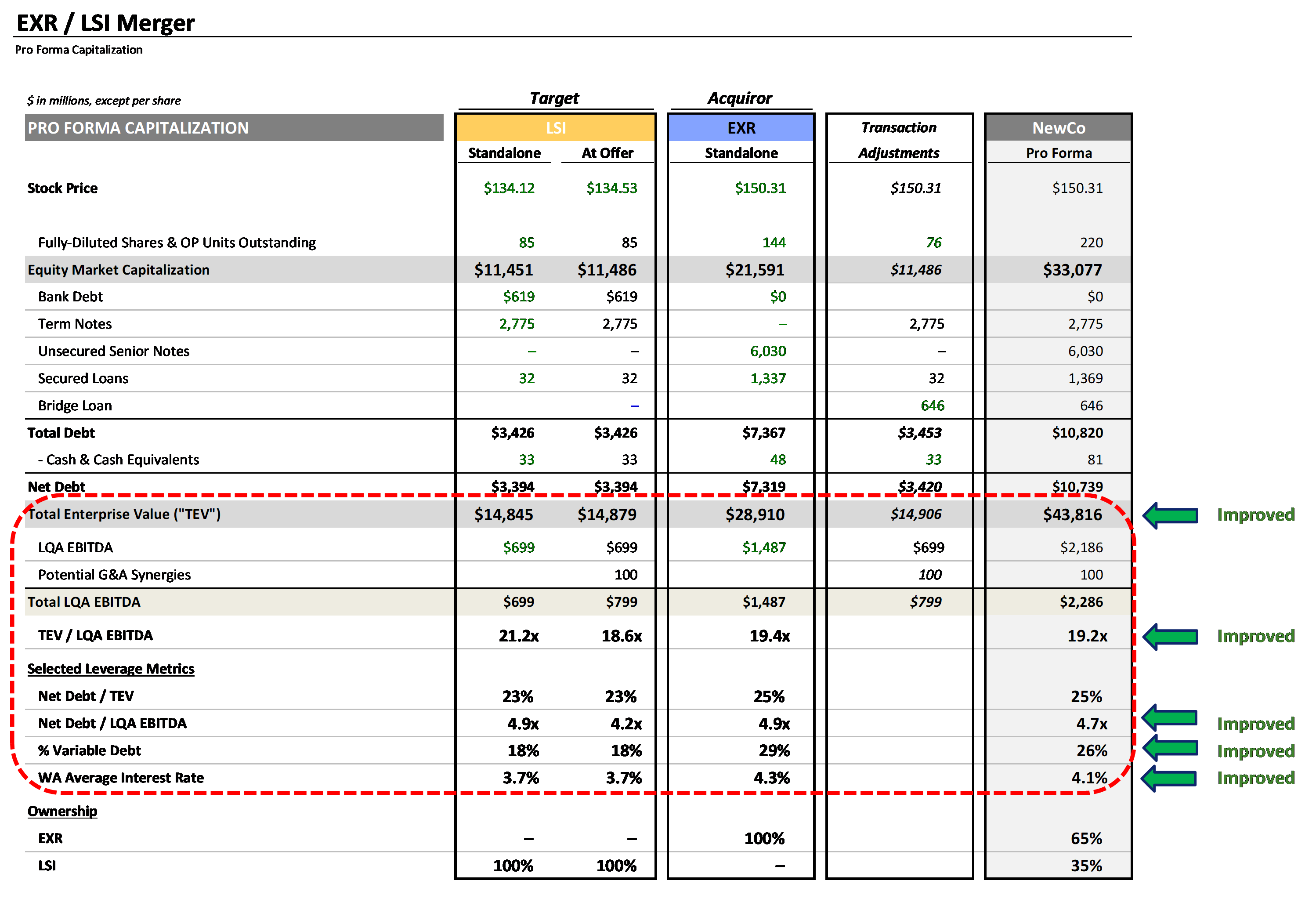

On April 3, 2023 , EXR and LSI announced that the two companies had entered into a definitive agreement by which EXR would acquire LSI in an all-stock tax-free transaction, with LSI shareholders receiving 0.895 EXR shares for every share of LSI owned. While on a standalone basis, the deal may appear dilutive given LSI currently trades at a 1.8x premium to EXR on an EV/EBITDA basis (LSI and EXR trade at EV/EBITDA multiples of 21.2x and 19.4x, respectively), after accounting for $100mn of expected synergies, the math makes more sense as LSI's EV/EBITDA multiple declines to 18.6x, representing a -0.8x discount to EXR.

Company filings, Analyst estimates.

{kind=link}

EXR management estimates 1% of FFO accretion from the deal based on $100mn of run-rate synergies. However, management's estimate of synergies assumes 100% of LSI's self-storage properties are rebranded under the Extra Space brand and banner. Given that the company plans to run both brands in markets where there is overlap and only rebrand if it makes economic sense, I think management's estimate of $100mn is likely conservative.

Additionally, on EXR's 1Q23 earnings call , management mentioned that when underwriting the LSI acquisition, they assumed they would need six regional offices, but later determined that they would only need four offices, which should further improve EXR's synergies recognized from the deal.

Given EXR management's track record of under guiding and over delivering, and despite management's estimate of 1% of FFO accretion, I think $0.18, representing 2.1% of FFO accretion is a more reasonable estimate of accretion and should serve as a positive catalyst to share price performance going forward if it is realized.

Company filings, Analyst estimates.

{kind=link}

EXR management has a reputation of acquiring portfolios of self-storage properties that are underperforming and then improving their performance once the portfolio is brought onto their best-in-class operating platform (e.g. acquisition of SmartStop ). In fact, many research analysts would accuse them of "juicing their SS NOI performance". While many may look at a large acquisition like LSI as creating a company too large too quickly and be worried about a denominator problem (i.e. its harder to grow a large company than a small company), unlike some real estate classes that have minimal opportunity to improve performance (i.e. net lease), EXR has the benefit of bringing a very large portfolio onto their operating platform, creating a significant opportunity to improve performance. Comparing LSI's per store performance to EXR's per store performance reveals that there is a significant opportunity to the upside for SS revenue performance once LSI's properties are added to the EXR SS pool.

Company investor presentation.

Self-Storage Fundamentals are Moderating, But They Are Not Falling off A Cliff

After an initial decline in demand for self-storage units at the beginning of the pandemic, consumer behavior shifted resulting in record demand for self-storage in the pandemic's later stages. Workers who fully embraced remote work and decided to move from expensive coastal markets to more affordable tertiary markets needed additional space to store their belongings during the moving process, while others de-cluttered their homes in order to make room for their Work From Home ((WFH)) office.

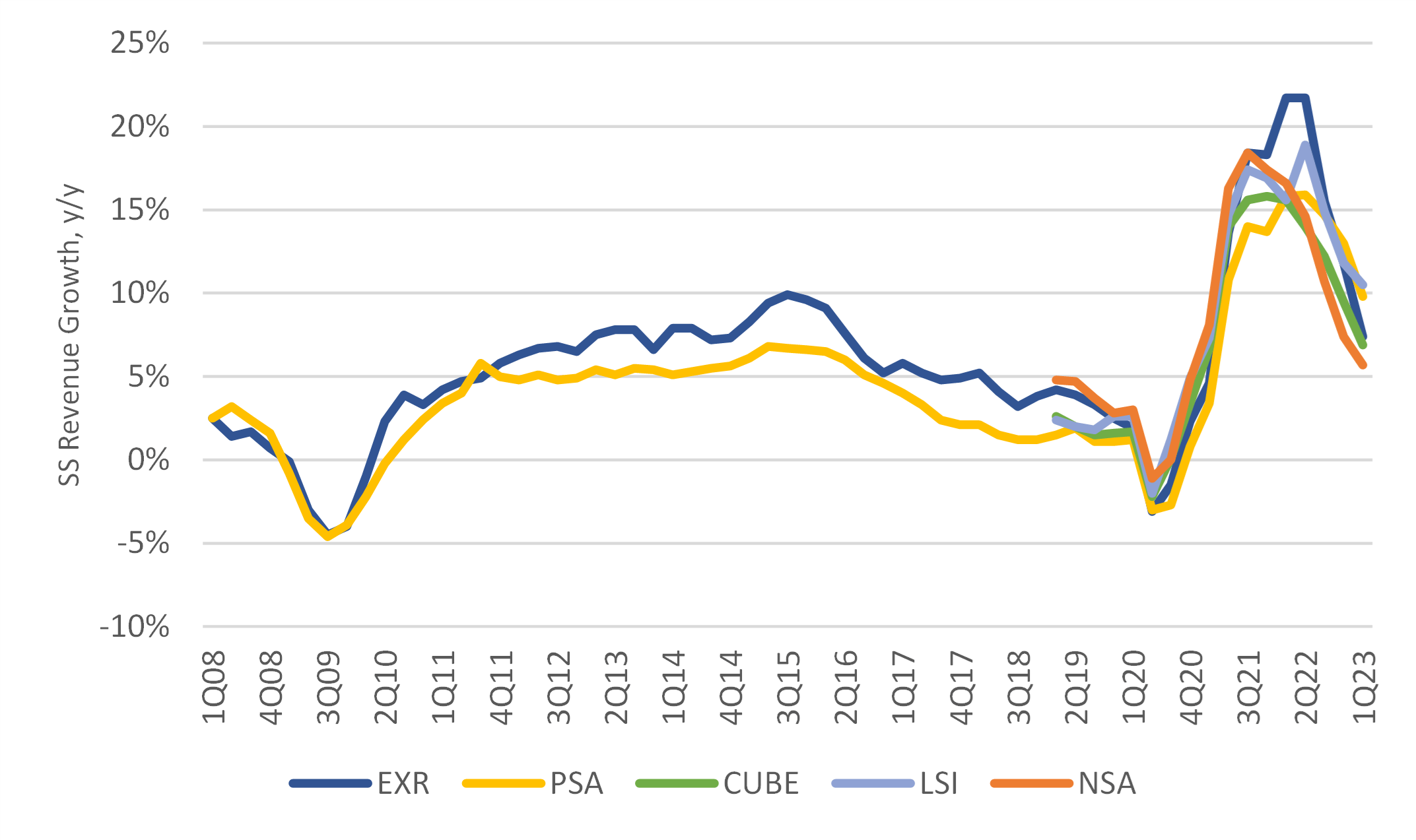

EXR reported SS revenue growth of 7.4% in 1Q23 , marking a stark deceleration from 2022 when the company reported annual SS revenue growth of 17.4%, the highest in the company's history. With difficult comps from 2022 and fading tailwinds as the pandemic is further in the rearview mirror, REIT management teams anticipate a return to pre-COVID demand trends. While this marks a stark deceleration from the record highs recently experienced, management teams are not seeing anything that would indicate that demand will settle at a level that is below pre-pandemic demand levels.

While optically the decline in storage fundamentals may be discouraging, it needs too be noted that the record high demand seen in 2021 and 2022 was not permanent and a return to more normal fundamentals is inevitable.

{kind=link}

On EXR's 4Q22 earnings call , management explained that Existing Customer Rate Increases (ECRI) were very constrained by government regulations in the early innings of the pandemic. As those regulations gradually dropped off state by state, there was a catch-up period of elevated ECRI's that further boosted SS revenue growth in 2021 and 2022 beyond the levels that would have been achieved by the previously cited shifts in consumer behavior alone. While concerned investors may interpret the rapid deceleration of SS revenue growth as something more serious like a secular decline in demand, I think what we are seeing is just an inevitable return to more normal demand levels that is being reflected in current SS revenue growth rates.

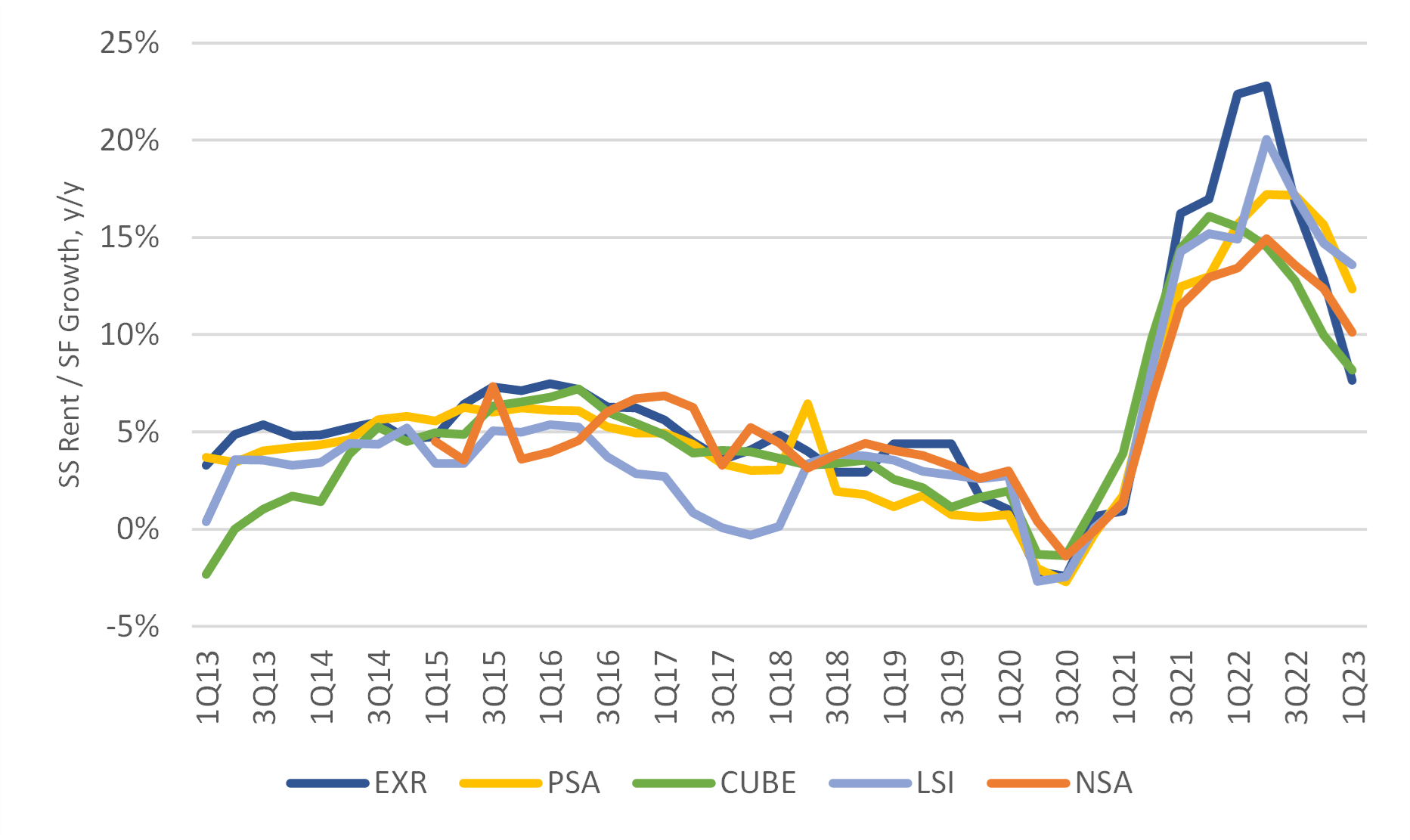

Self-storage SS revenue growth has two components: (1) change in rent/SF and (2) change in occupancy. Public self-storage REITs reported average SS revenue growth in 1Q23 of 8.1%, composed of 10.4% SS rent/SF growth offset by a -2.2% decline in occupancy. While an average SS revenue growth of 8.1% is a stark deceleration from 17.1% SS revenue growth in 1Q22, it is still significantly above the long-term average SS revenue growth of 5.1%.

{kind=link}

{kind=link}

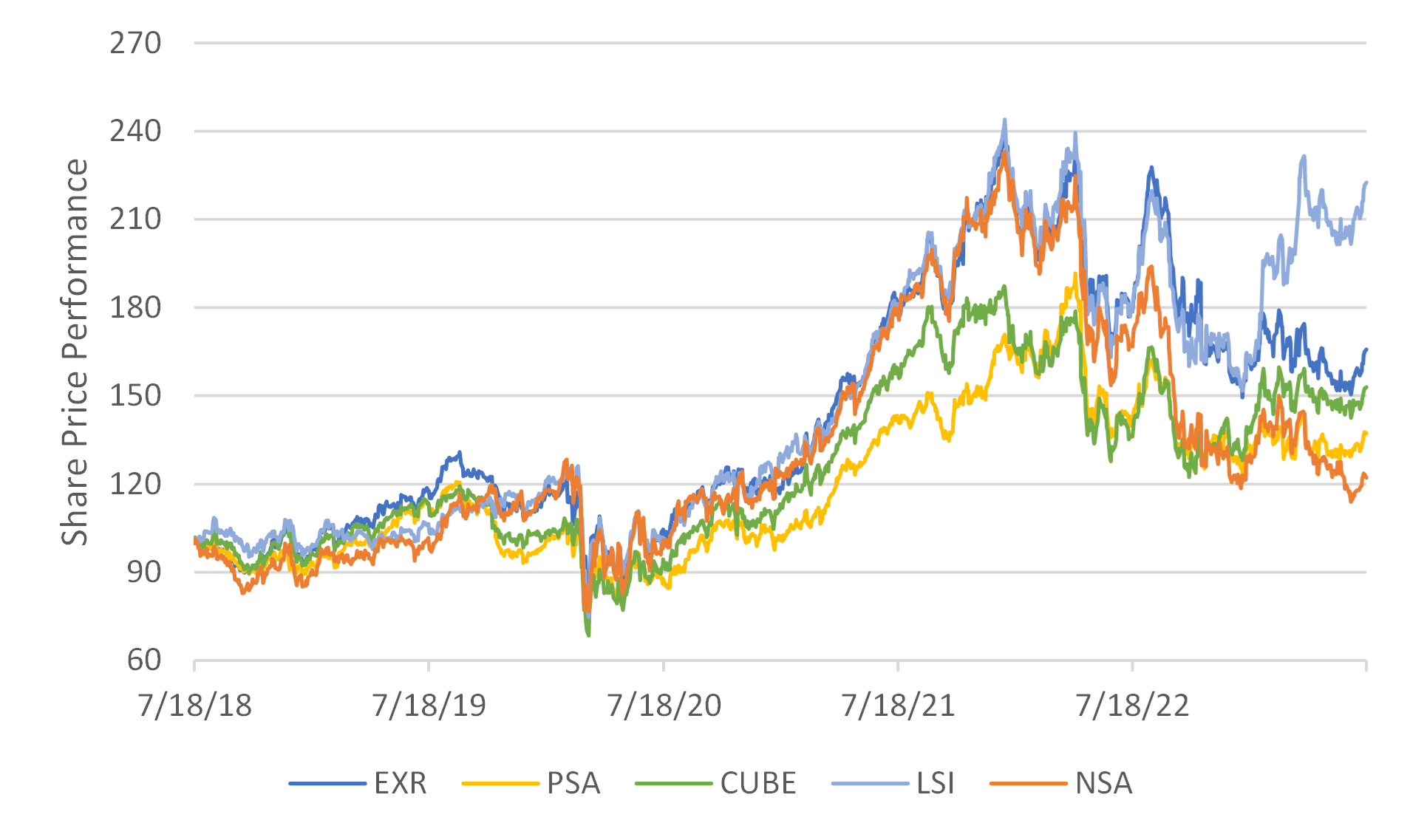

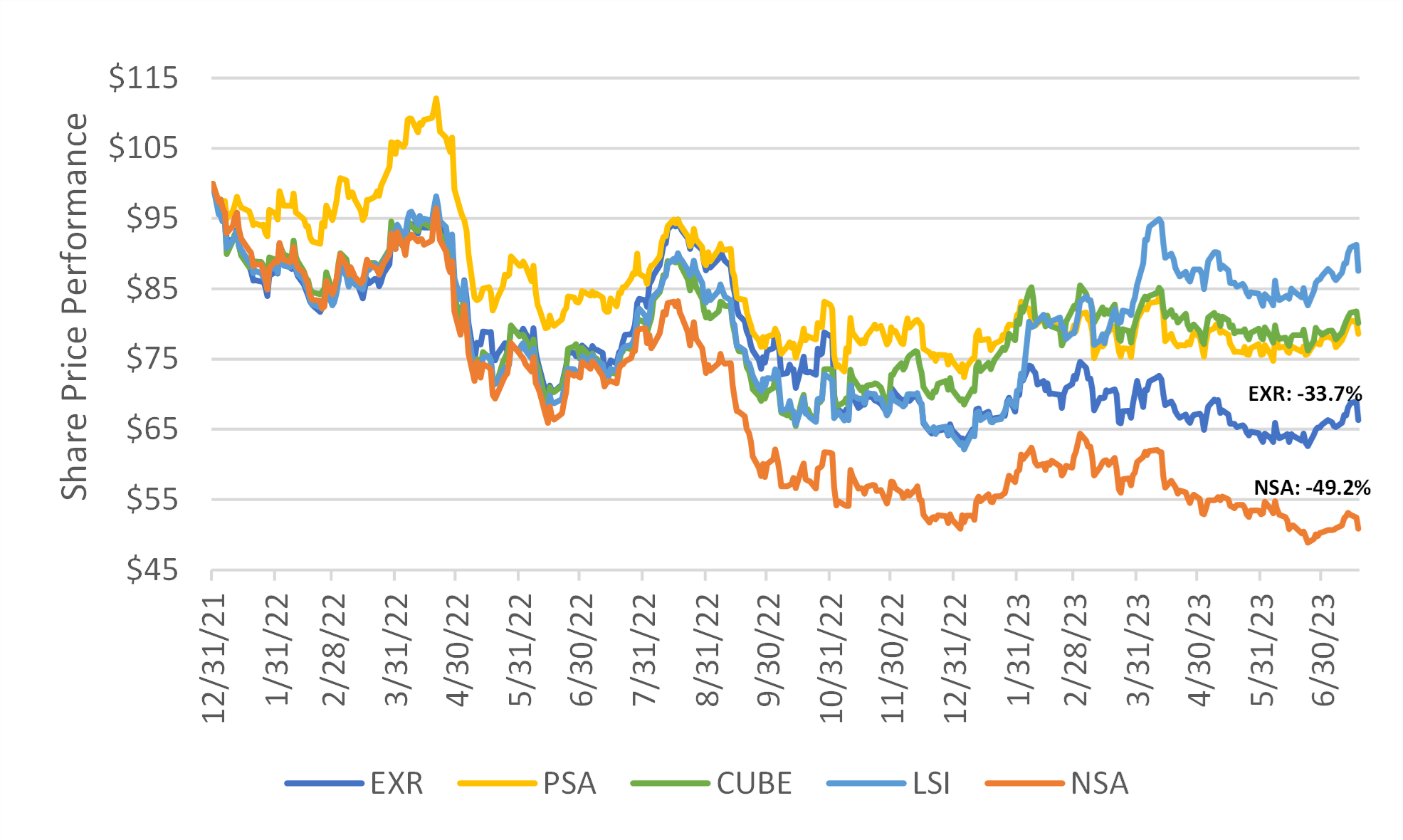

Self-storage REIT share price performance has historically exhibited a strong correlation with SS revenue growth. As SS revenue growth has decelerated precipitously, self-storage REIT share prices have responded in kind with shares declining by -27.3% on average since the end of 2021, presenting what I think is an opportune point of entry.

{kind=link}

Look to SS Occupancy for Emerging Green Shoots

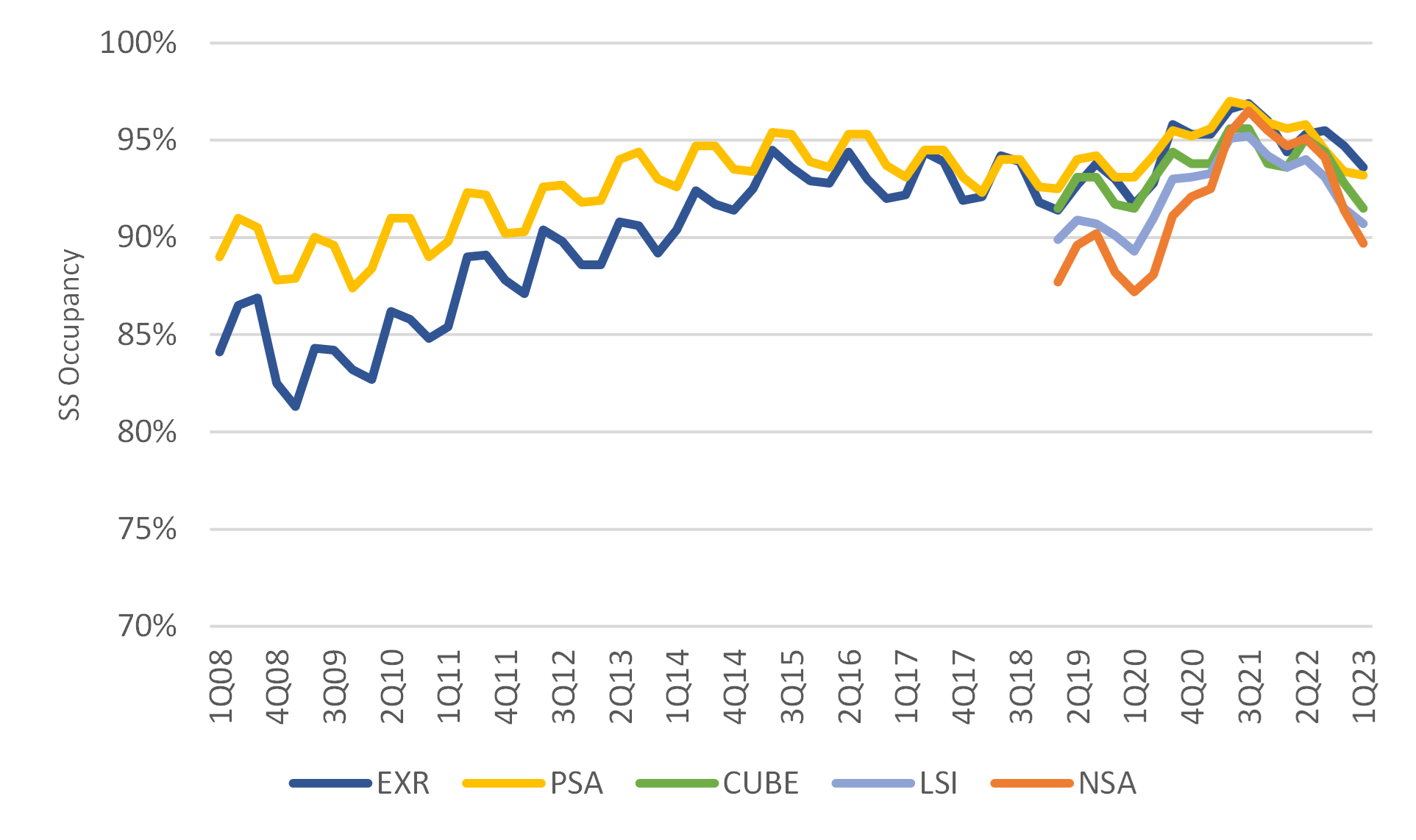

When self-storage REITs report earnings, they provide the average SS occupancy for the quarter as well as where SS occupancy stood at the end of the quarter. Investors will often compare the period end occupancy to the average for the quarter as an indication of how SS occupancy will trend going forward. Looking across publicly traded self-storage REITs over the last three quarters reveals that the delta between the average for the quarter vs. the period end has gradually improved from -0.9% in 3Q22 to -0.6% in 4Q22 and -0.1% in 1Q23 indicating that SS occupancy levels may be troughing.

{kind=link}

Furthermore, on EXR's 1Q23 earnings call, management mentioned that occupancy in April increased +30bps relative to the end of the quarter. I anticipate that the worst is behind us in terms of occupancy declines and we will start to see a rebound in occupancy trends in the next couple of quarters.

The Biggest Threat to Self-Storage Fundamentals is Development Deliveries…

EXR management mentioned on the company's 3Q22 earnings call that storage deliveries are moderating as there are continuing headwinds to development yields in the form of higher debt and labor costs.

Furthermore, on the company's LSI acquisition conference call , Ken Woolley (the veteran founder of Extra Space Storage) made the following quote:

"… the biggest threat to storage in terms of revenue growth, is too many properties being built. And the benefit of the current interest rate environment, is that it is going to slow down the development of new properties, which will enhance the growth of existing properties."

Given the current cost of capital and labor environment, I expect self-storage development deliveries will decline precipitously in the near future. However, given that it takes ~24 months to develop and deliver a self-storage property, I estimate that the rapid decline in self-storage deliveries due to high debt and labor costs is likely a future event, which should help contribute to a strengthening of SS revenue fundamentals.

Similar to what we are seeing in the residential housing market, I think that constrained supply can provide a significant support to self-storage rental rates, particularly in an environment where demand is increasing. Self-storage penetration stands at 10.6% of households, nearly double what it was in 2004 when penetration was 5.5%. While the rate of penetration almost doubling in 20 years may seem unlikely to repeat itself in the next 20 years, you need to consider that the penetration rate is still relatively low considering only 1 in 10 households are utilizing self-storage currently.

Company investor presentation.

Balance Sheet to Improve Post the Acquisition of LSI

Given the similar leverage profiles of EXR and LSI, EXR management communicated to the public that the acquisition of LSI, which is expected to close in 2H23, would be a leverage neutral event. However, when accounting for the expected synergies of $100mn, which is likely conservative in my view, the post-acquisition leverage profile of EXR improves to 4.7x net debt/EBITDA from 4.9x net debt/EBITDA.

Furthermore, looking at the post-acquisition balance sheet for EXR in its entirety, reveals that: (1) weighted average interest rate, (2) percentage of debt that is variable, and (3) enterprise value, all improve relative to the pre-acquisition balance sheet. While the primary impetus behind the acquisition of LSI may be its earnings accretion, EXR also stands to benefit from a strengthened balance sheet and improved cost of capital going forward.

Company filings, Google Finance.

{kind=link}

Real estate asset classes with short lease terms tend to weather periods of inflation better than asset classes with long lease terms, as they are better equipped to raise rental rates to keep up with inflation. As such, REITs with short term leases tend to have higher levels of variable rate debt relative to asset classes with long lease terms, and storage is no exception (most storage properties have monthly lease terms). Among self-storage peers, EXR has the highest level of variable rate debt with 29% of its outstanding debt having variable interest rate terms compared to a peer average of 16%. While this has been a significant headwind to earnings growth as rates have risen rapidly over the course of 2022, this headwind should turn into an earnings tailwind if rates decline from their record highs going forward.

{kind=link}

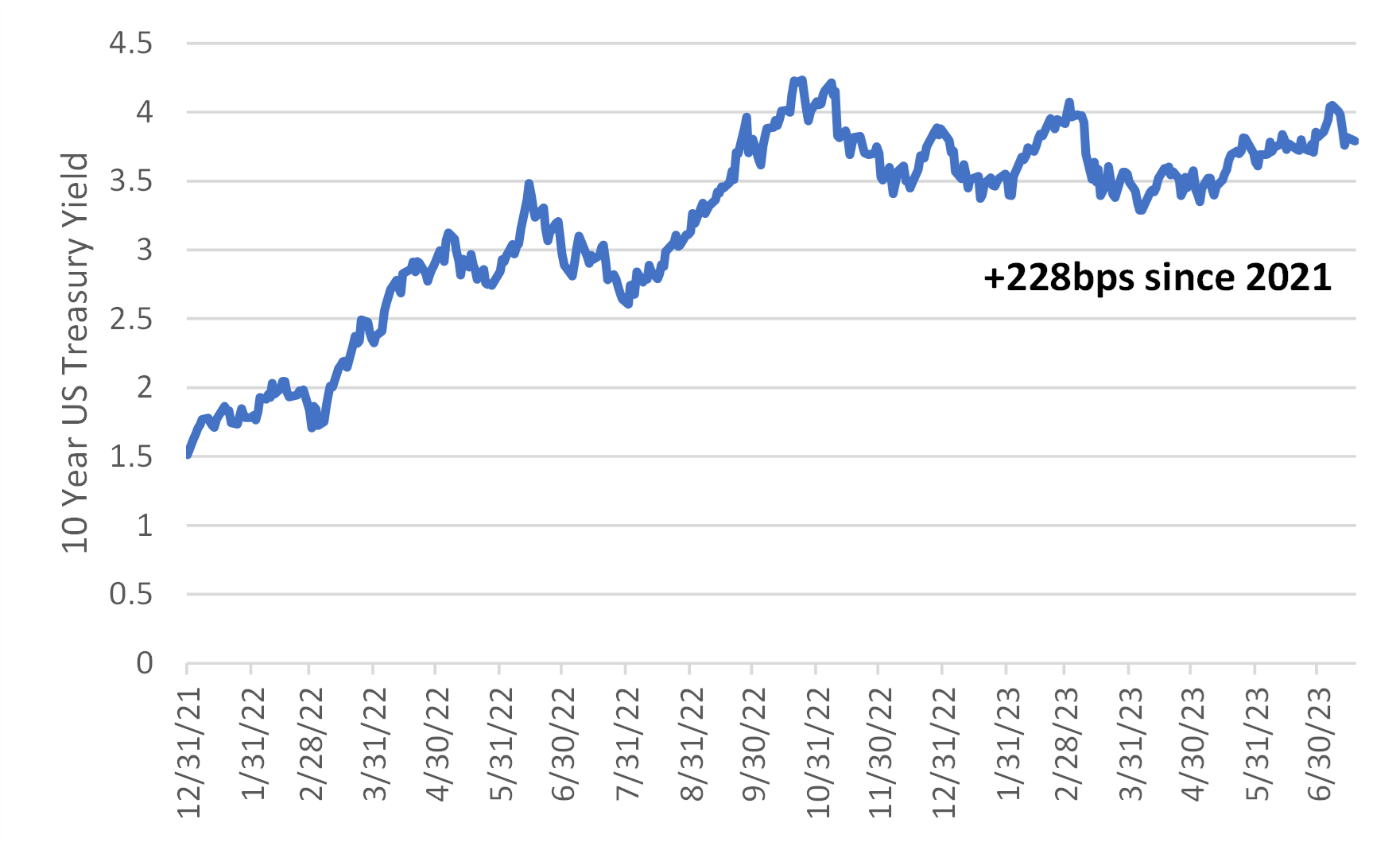

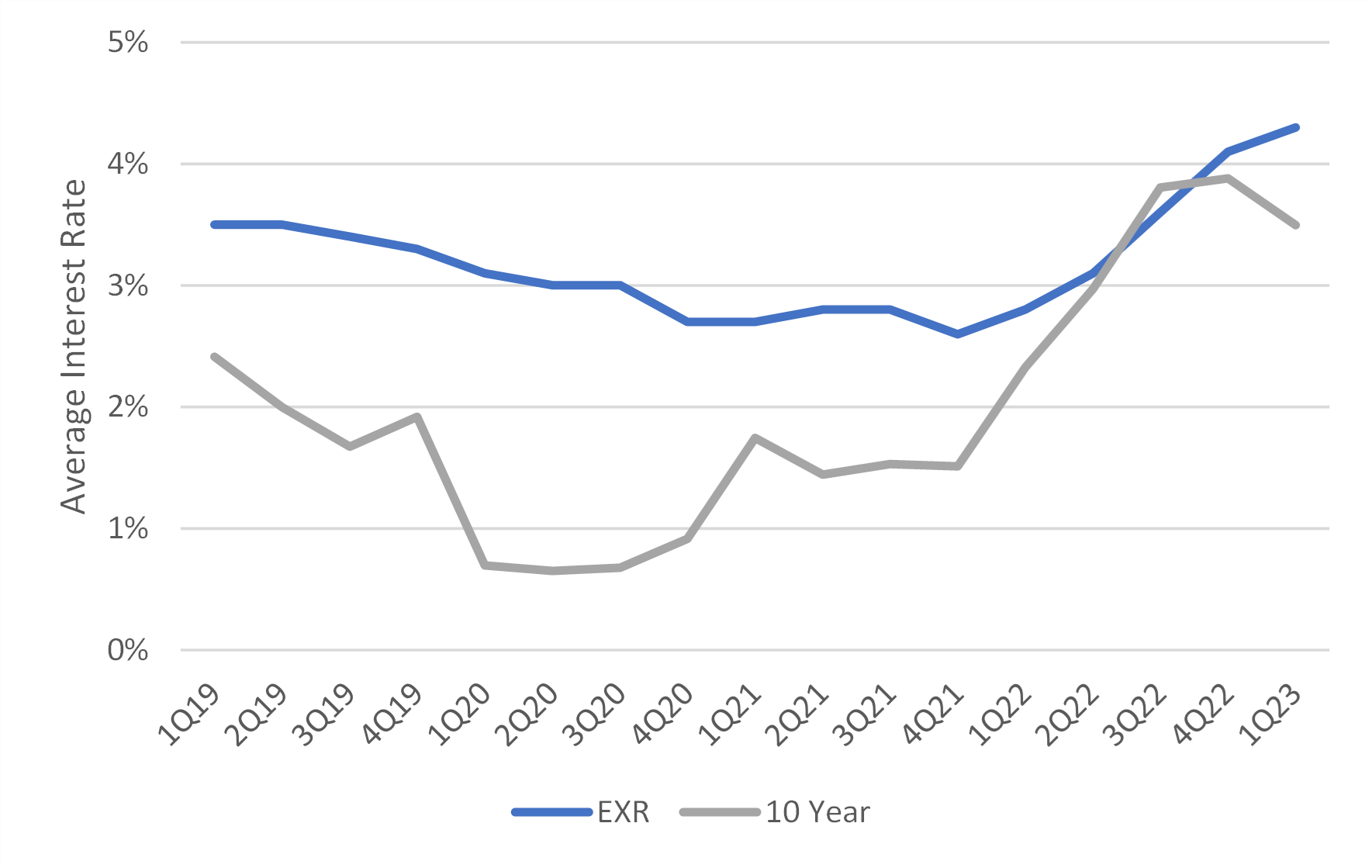

As 10 Year Treasury yields have risen +228bps since the end of 2021, self-storage REITs, which all have variable rate debt, have seen their weighted average interest rates increase to various levels. Since the end of 2021, there has been fairly tight correlation between the change in weighted average interest rates and share price performance with LSI being the notable exception given its share price performance was aided by the announcement of its pending acquisition by EXR.

{kind=link}

Company filings, Google Finance.

{kind=link}

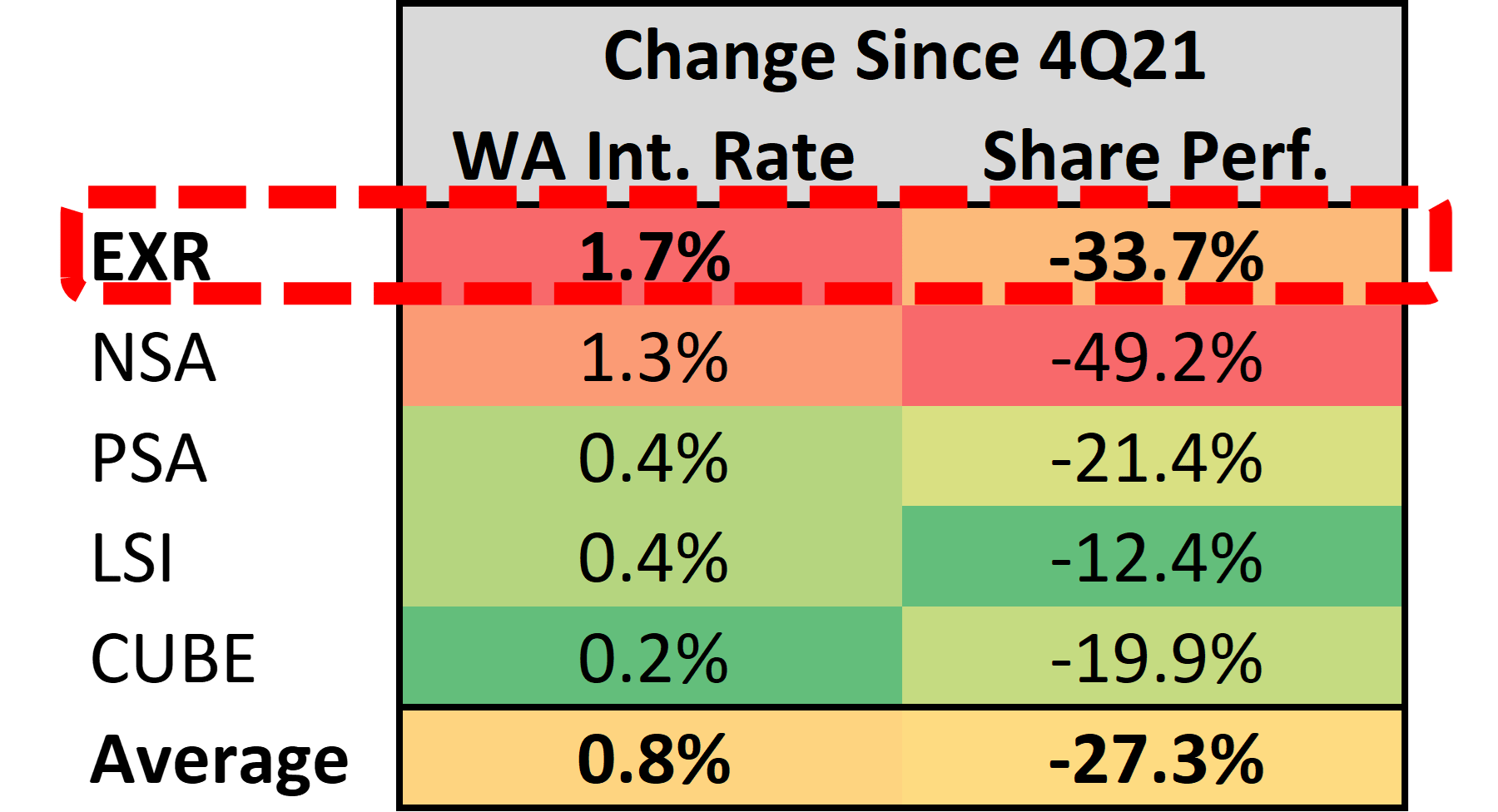

EXR's high level of variable rate debt has led to EXR's weighted average interest rate increasing by +170bps since the end of 2021, corresponding to a -33.7% share price performance. However, assuming that rates have peaked in this cycle, EXR's interest rate headwinds of the last five quarters should turn into tailwinds as its weighted average interest rate declines along with benchmark rates.

{kind=link}

Company filings, Google Finance.

{kind=link}

EXR's weighted average interest rate as of 1Q23 of 4.4% is significantly higher than the peer average of 3.5%. Along with peer REIT NSA, I estimate that EXR and NSA would see a -1.8% decline in FFO from a +100bps move in benchmark rates. However, assuming benchmark rates have peaked during this cycle I see this risk as relatively benign, and think that the market is currently over-estimating this risk given EXR's and NSA's share price underperformance.

Taking the Yield To Maturity (YTM) on a recent debt issue and subtracting the corresponding 10 Year US Treasury yield as of that date, I arrived at what I think is a reasonable estimate of the company's G Spread, or the added debt yield that the market is demanding for the incremental risk of the company's debt relative to the risk-free rate. By taking the appropriate G Spread and adding it the current US Treasury Yield, I arrived at what I believe to be a current estimate of the REITs' cost of 10 year debt.

According to my calculations, EXR has the highest cost of incremental debt at 5.7%, compared to my LSI estimate of 4.8%. Given that EXR's post-acquisition equity market capitalization will make EXR the 6th largest REIT in the RMZ index, I think that ratings agencies are likely to view EXR more favorable from a balance sheet perspective resulting in a lower cost of debt capital going forward.

{kind=link}

Valuation: EXR is Currently Trading at a -13.9% Discount to its Intrinsic Value

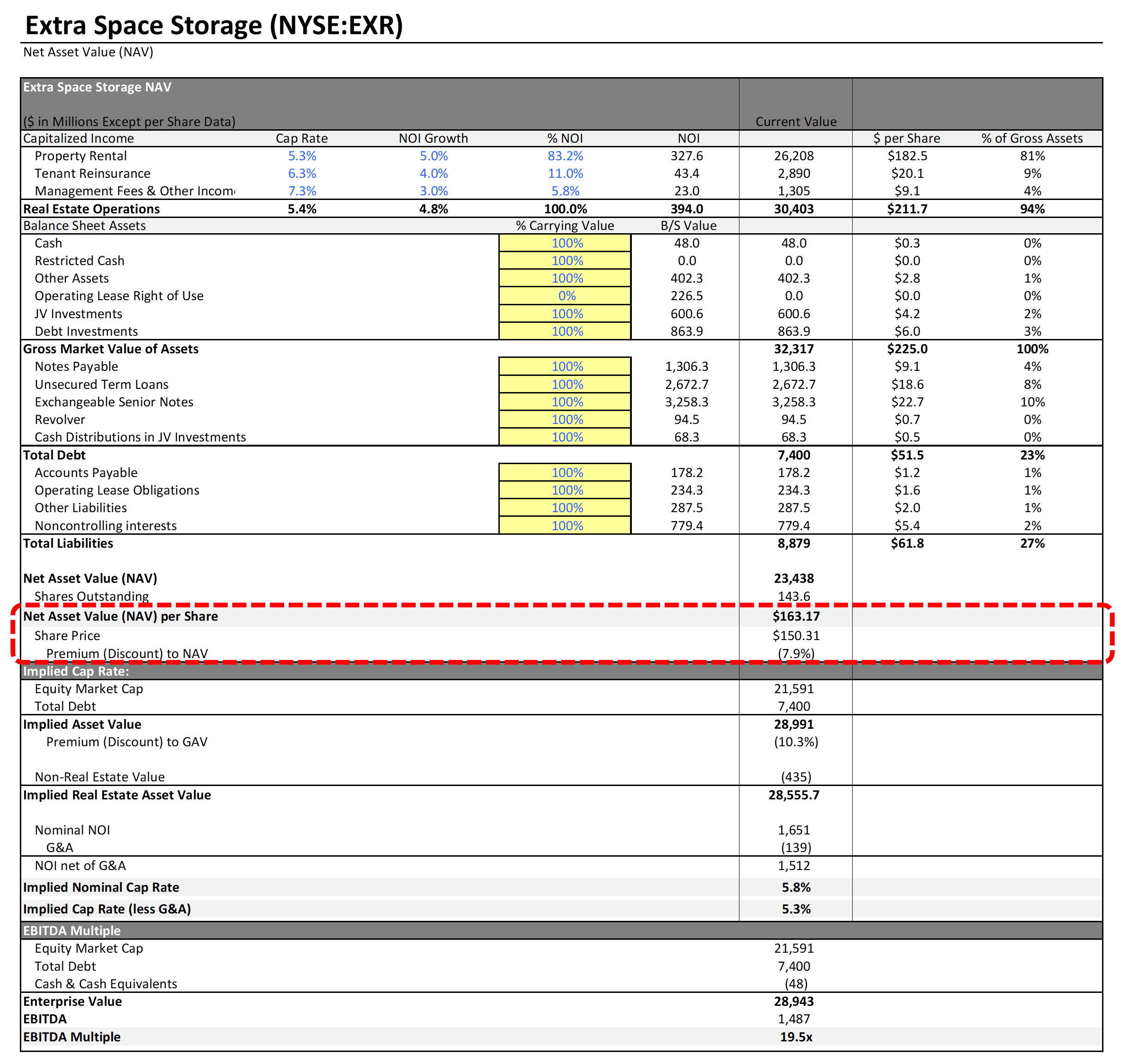

Historically, REITs have been valued on Net Asset Value ((NAV)), which seeks to approximate the private market value of the REIT's net assets. When EXR's CEO was asked on its 4Q22 earnings call where stabilized cap rates were currently, EXR's CEO indicated that cap rates on stabilized assets were in the low 5's. Given that 10 year Treasury yields have only declined by -9bps since the CEO's comments on February 23, 2023, I think that 5.25% is an appropriate cap rate for EXR's stabilized assets.

Applying a 5.25% cap rate to EXR's NOI results in an NAV/share of $163.17. EXR's current share price of $150.31 (as of 7/18/23) implies a cap rate of 5.8%, and indicates that purchasing a share of EXR at current levels allows investors to purchase EXR's net assets at -7.9% discount to their private market value.

Company filings, Google Finance.

{kind=link}

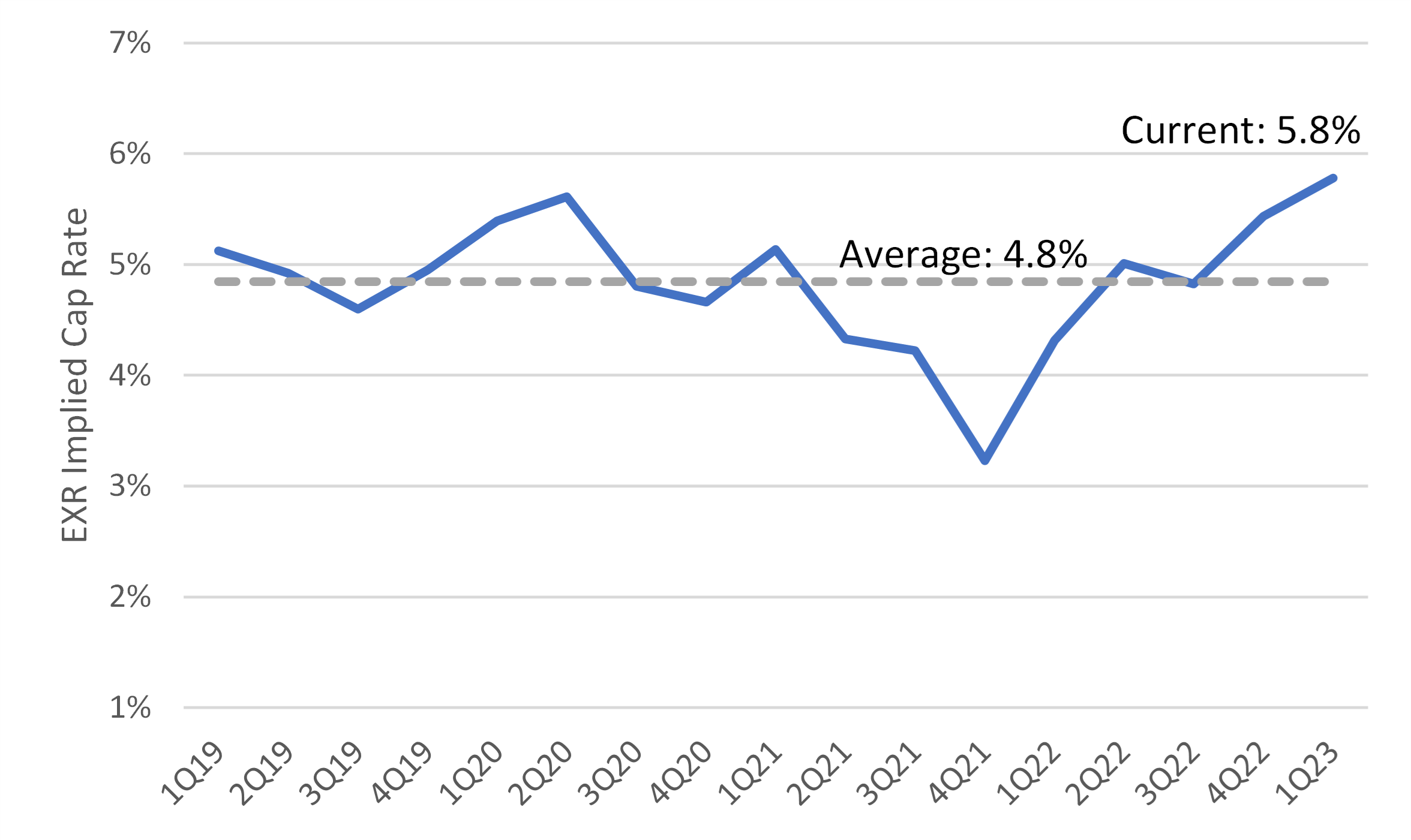

EXR's current implied cap rate of 5.8% stands +100bps above its four-year average of 4.8%, and +20bps above its prior peak of 5.6% in 2Q20 during the depths of the COVID pandemic. While rates are higher now than they were in 2Q20, I think the macroeconomic environment and the outlook on the strength of the consumer has improved significantly representing an attractive entry point for investors.

Company filings, Google Finance.

{kind=link}

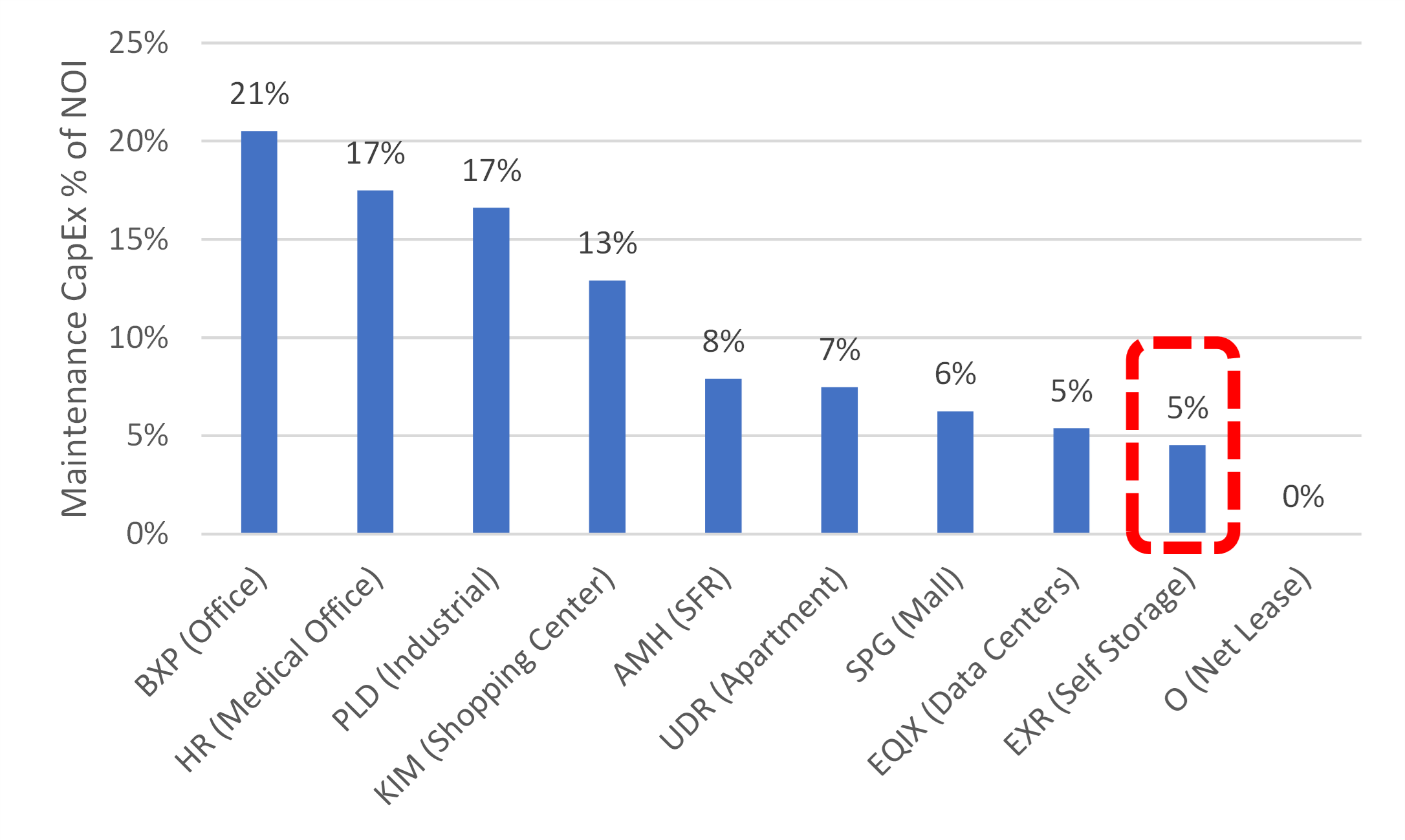

While Net Asset Value ((NAV)) may be an effective method for estimating a REIT's private market value, what it ignores is the cost of real estate maintenance, or the amount of maintenance/recurring capital expenditures that are required for the real estate to maintain its value. In FY2022, EXR spent less than 5% of its NOI on maintenance capital expenditures, lower than all real estate asset classes with the exception of Net Lease REITs, where the tenant is responsible for all maintenance capital expenditures.

{kind=link}

In an environment where rates are higher for longer, cash should be king. Furthermore, considering that EXR will be the 6th largest REIT by equity market capitalization after it acquires LSI, I view EXR's discount to Net Asset Value ((NAV)) as less relevant.

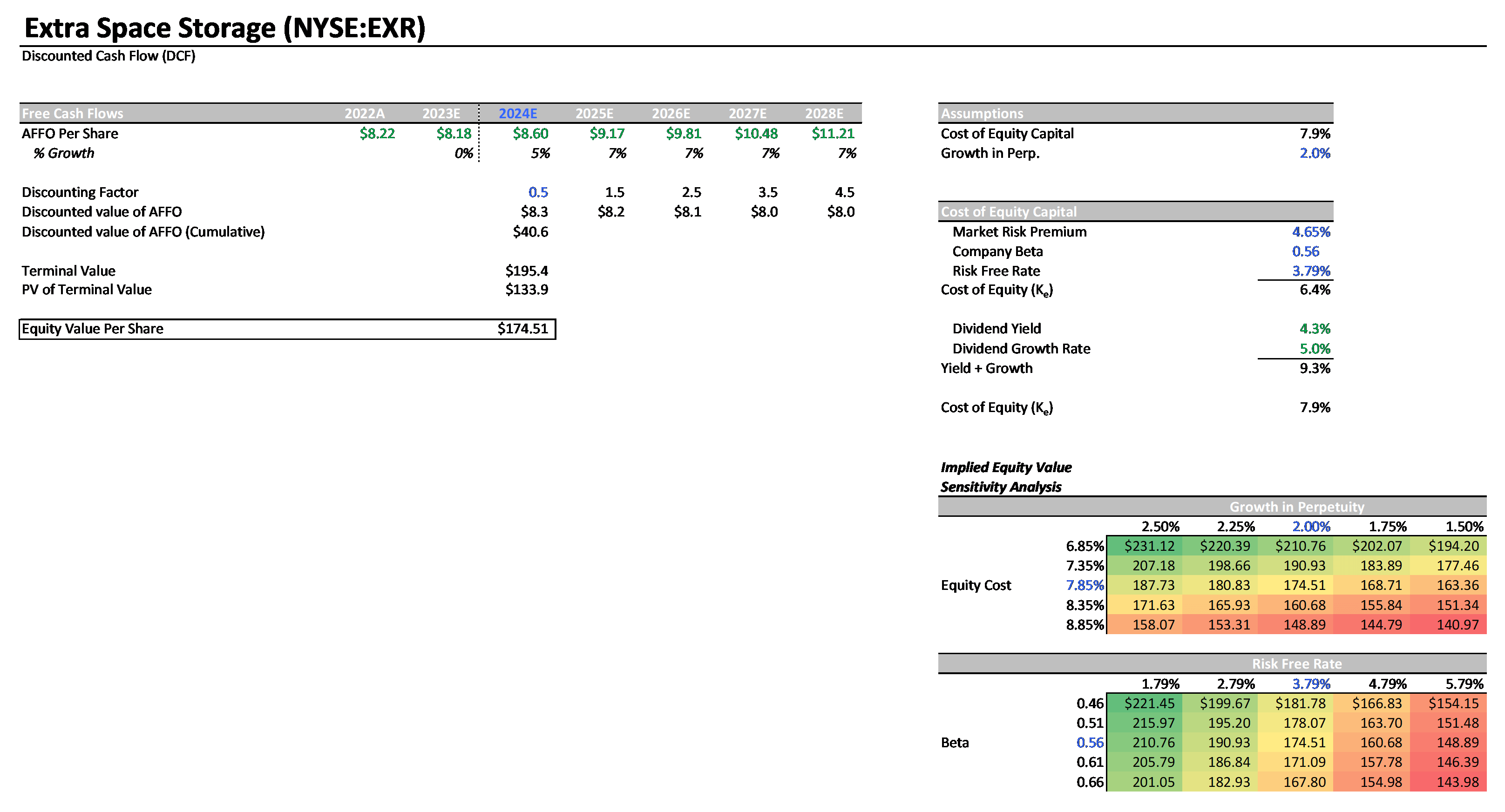

Given the low likelihood of EXR being acquired outright, I think that a Discounted Cash Flow ((DCF)) analysis is the most appropriate method for determining EXR's intrinsic value given that it incorporates higher rates in its cost capital calculation while also accounting for its lack of maintenance capital expenditures in the free cash flow estimates.

Assuming the current 10 year Treasury yield of 3.79% persists for the long term, I estimate that a share of EXR has an intrinsic value of $174.51. Considering EXR's current share price of $150.31, EXR currently trades at a 13.9% discount to its intrinsic value despite several positive catalysts that I outlined above.

Company filings, Analyst estimates.

{kind=link}

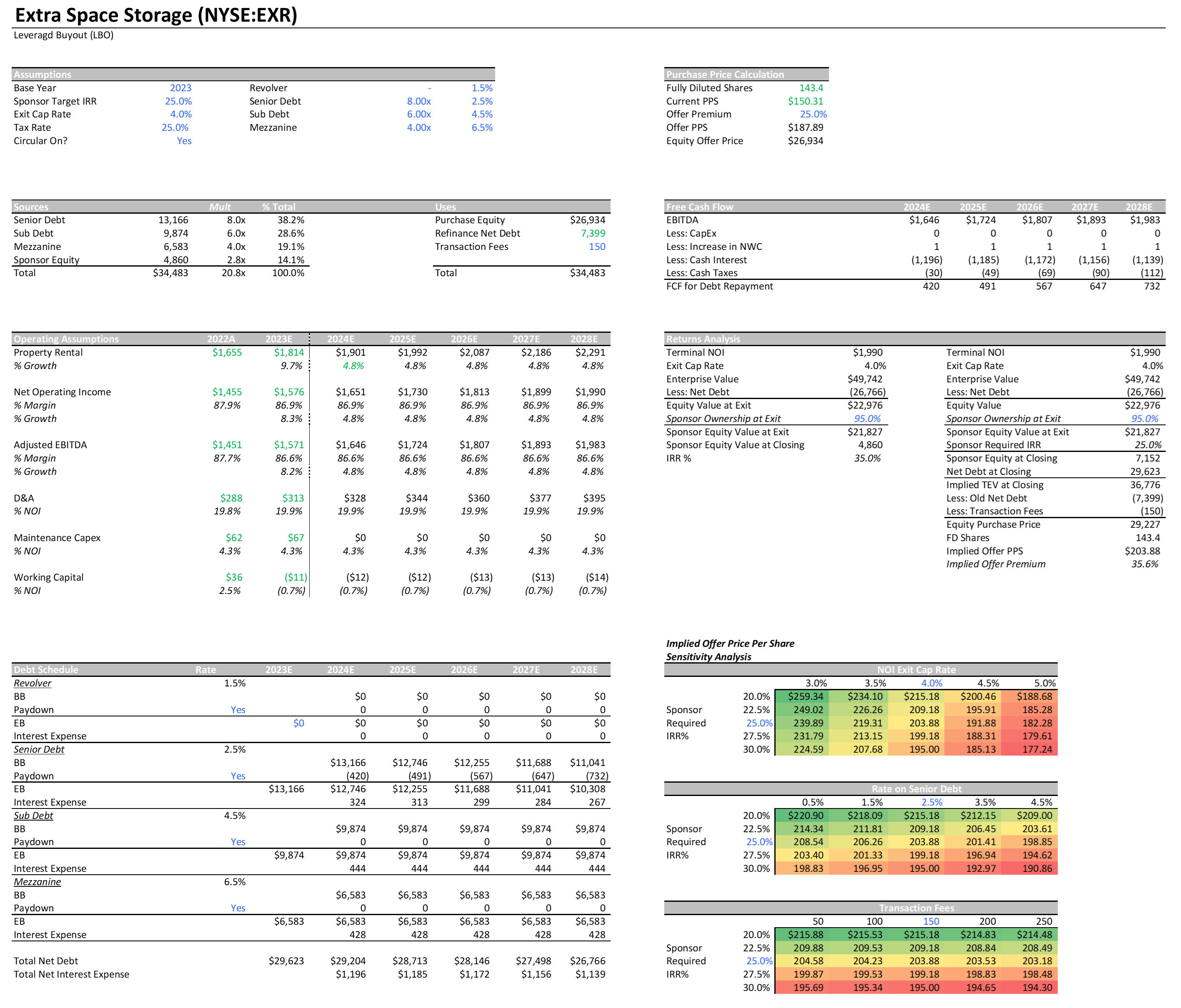

Given the strong internal growth profile of self-storage (EXR has averaged SS NOI growth of 7.6% over the past 15 years), and the low level of capital intensity (EXR's maintenance capital expenditures as a percentage of NOI was 4.5% in FY2022), self-storage as an industry would be ideal for being acquired by a financial sponsor in a Leveraged Buy Out ((LBO)) transaction. I estimate that a financial sponsor targeting a 25% Internal Rate of Return ((IRR)) could pay up to $203.88 (a 35.6% premium to EXR's current share price), and still achieve a 25% IRR hurdle rate. However, considering EXR will be the 6th largest REIT by equity market capitalization after it acquires LSI, I see EXR being acquired in a Leverage Buy Out ((LBO)) as an unlikely event.

Company fillings, Google Finance.

{kind=link}

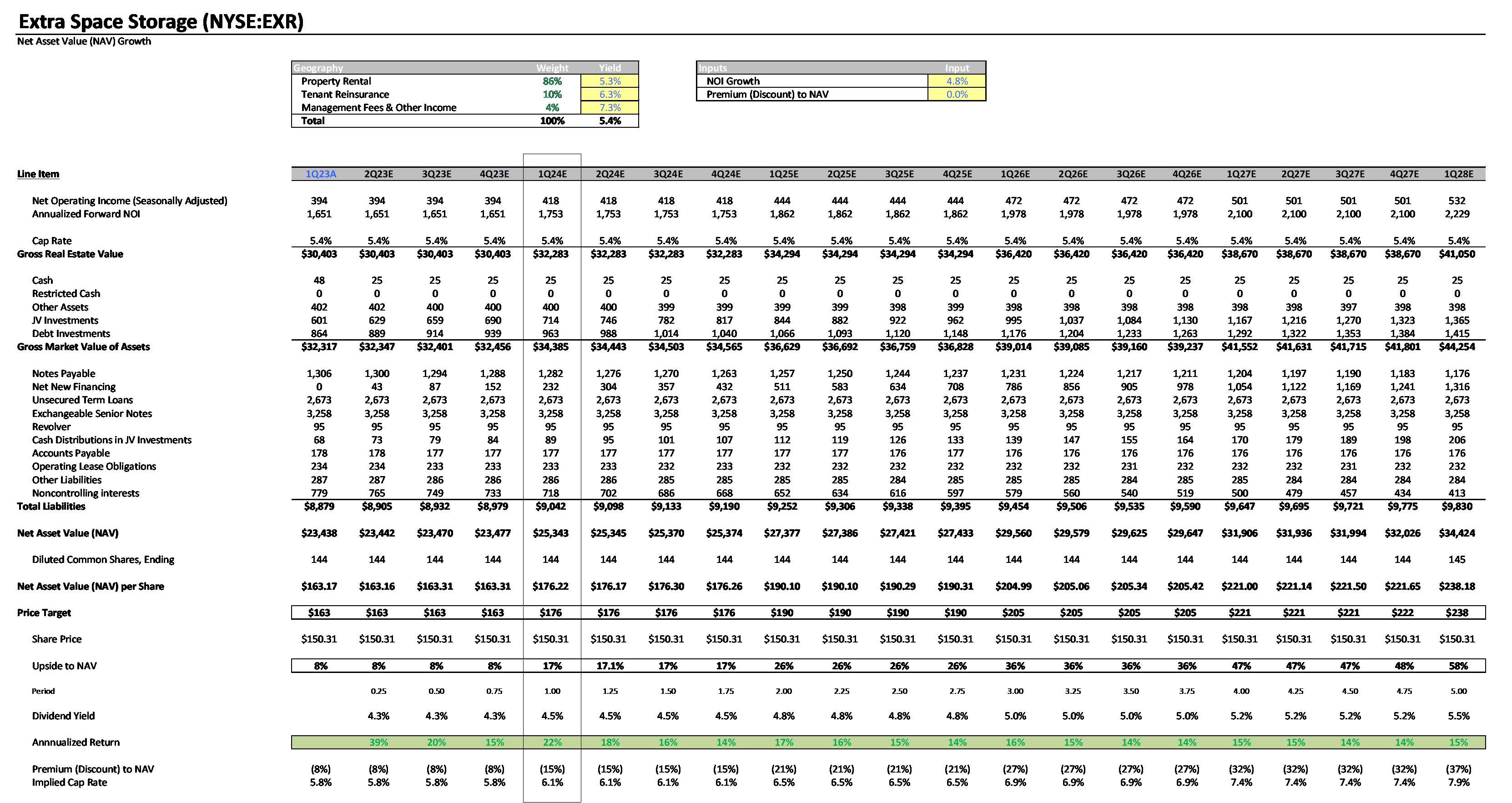

Returning to Net Asset Value ((NAV)), I estimate that EXR will be able to grow its Net Asset Value ((NAV)) per share by 7.9% over the next five years. Including EXR's 4.3% current dividend yield and assuming that EXR can close the gap to its NAV results in a 15.1% average total return over the next five years. Assuming EXR cannot close the gap to its Net Asset Value ((NAV)) per share, I still estimate an average total return of 13.3% over the next five years.

Company fillings, Google Finance.

{kind=link}

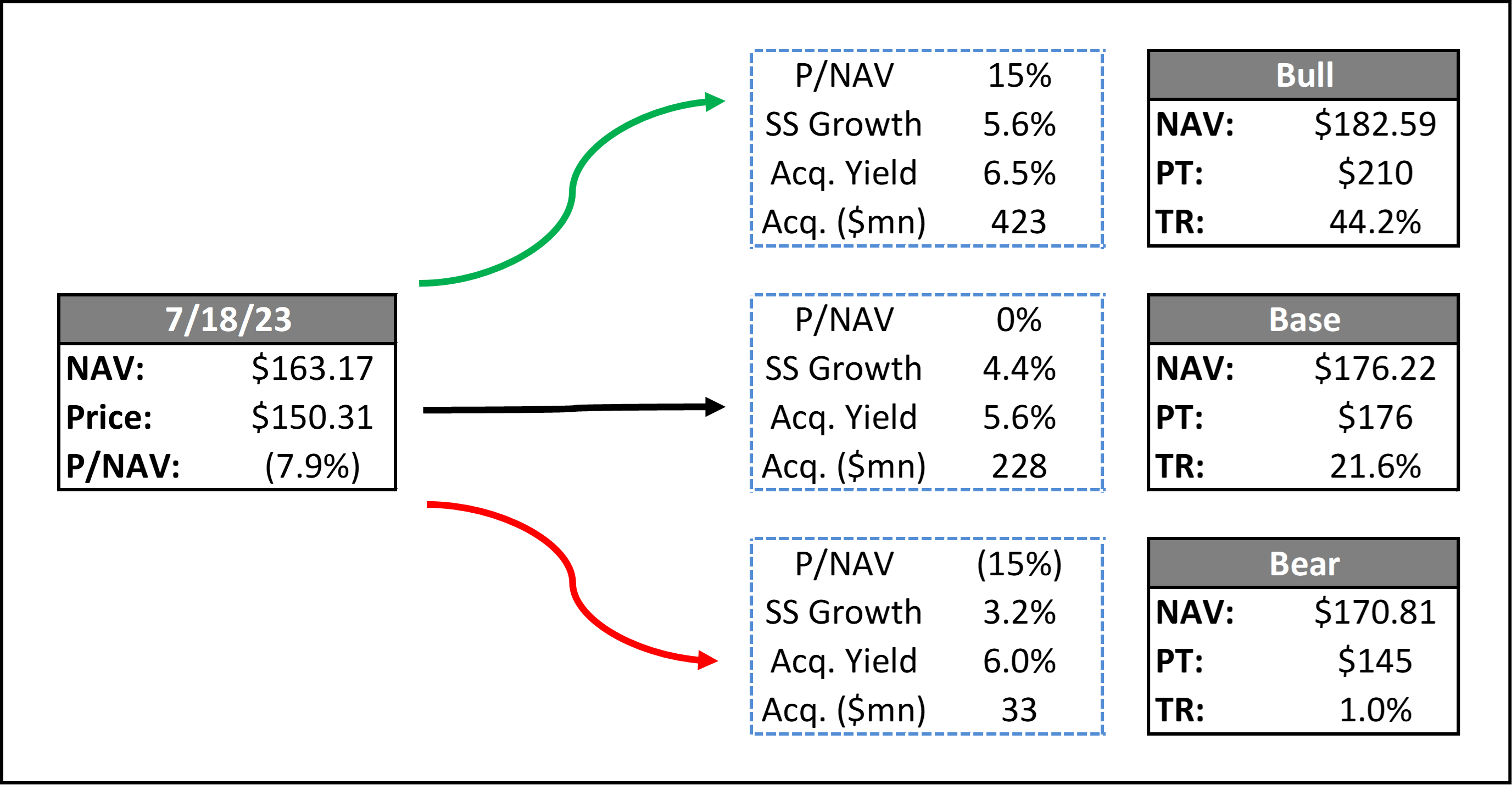

Bull Case

$210 price target represents a 44.2% total return and assumes EXR's stock trades at a 15% premium to its NAV, 5.6% SS NOI growth, and $423mn of real estate acquisitions at a 6.5% acquisition yield.

Base Case

$176 price target represents a 21.6% total return and assumes EXR's stock trades inline with its NAV, 4.4% SS NOI growth, and $228mn of real estate acquisitions at a 5.6% acquisition yield.

Bear Case

$145 price target represents a 1.0% total return and assumes EXR's stock trades at a 15% discount to its NAV (this compares to a 5% discount to NAV during the depths of COVID pandemic), 3.2% SS NOI growth, and no further real estate acquisitions in 2023.

Conclusion

I believe EXR has a number of positive catalysts and tailwinds in the near future including: (1) higher than expected accretion from the acquisition of LSI, (2) a strengthened balance sheet and improved capital costs, and (3) an improving internal growth outlook as competition from development deliveries subside. Despite these positive developments, EXR continues to trade at its lowest valuation in the last five years and at a greater discount to NAV than during the depths of the pandemic. While this does perplex me, I also recognize that it opens the door to what I think is an extremely favorable point of entry for investors.

For further details see:

Extra Space Storage: Opportune Time To Buy A Best-In-Class REIT