NOK - Extreme Networks: Adopting Caution Following Nokia's Dim Outlook

2023-07-17 12:14:21 ET

Summary

- Both Nokia's and Extreme Networks' stocks have seen recent downsides, possibly indicating a sector weakness in demand due to macroeconomic uncertainty and high customer inventories.

- Despite supply constraints, Extreme has managed to deliver a three-year CAGR growth and is expected to grow by 15% to 17% through fiscal 2025.

- The company's stock seems fairly valued, but factors such as a potential increase in the dollar's value and higher distribution costs could impact long-term gross margins.

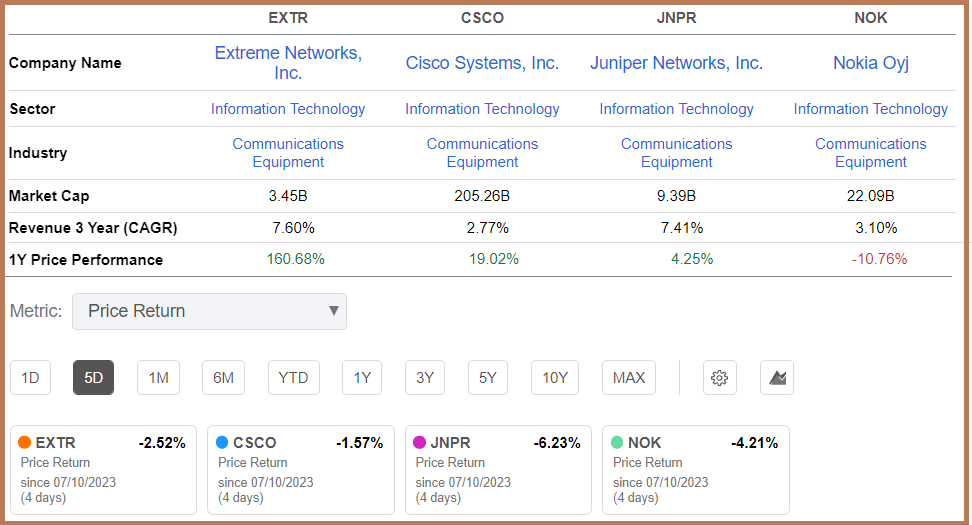

As illustrated in the deep blue chart below, Extreme Networks ( EXTR ) stock's latest price action shows a downside of 1.8% in the same period as Nokia ( NOK ) shedding 4.1% after downgrading its revenue outlook. This underperformance by the two equipment networks plays sharply in contrast with the tech-heavy Invesco QQQ Trust's ( QQQ ) gains of 3.5% and deserves to be investigated as it may point to demand weakness in the industry.

For this purpose, this thesis will consider factors like uncertainty in the macroeconomic environment, revenue split on a geographical basis and high customer inventories built as a precautionary measure against supply constraints. I will also build upon an earlier publication in January this year, when the company was still experiencing the lingering effects of Covid-induced supply chain issues.

First, I provide an overview of the company's product together with the competition.

Small, but Growing Fast

This is a $3.45 billion company founded back in 1996, and despite its relatively smaller size compared to much larger peers, has played a key role in the networking industry, notably by being the first to produce the fastest 10 Gigabit Ethernet switch in 2002.

Of course, technology has evolved considerably since, with speeds of 100 Gigabit being deployed in data centers nowadays. However, it is not only factors like speed that determine what CIOs choose to drive their network infrastructures. There is also plain simplicity as the network has grown complex with admins now spending a lot of time managing access points that are no longer confined to the office perimeter. This complexity also extends to people's homes as hybrid work seems to have become the norm after Covid.

To address this problem, there is Extreme's Fabric Connect , which by being agile and cloud-driven makes administrative tasks simpler while also providing automation features. At the same time, through the use of segmentation, the same level of IT security is provided whether it is for someone working in the headquarters building, or remotely.

Extreme Networks Network Fabric (www.extremenetworks.com)

{kind=link}

Now, whenever the talk is about automation, there is also a high dose of AI that finds useful applications in the networking arena due to the sheer number of data that is collected from various devices. The key here is for intelligent algorithms to quickly skim and learn through the tons of data with the intent of providing actionable insights. Examples are carrying out preventive maintenance actions to reduce outages or performing predictive analysis to avert cyberattacks. In this case, solutions like the ExtremeCloud IQ as pictured above, also offer real-time analytics.

Equipped with such strength, the company has been able to deliver a three-year CAGR growth of 7.6% which is even higher than the 7.4% delivered by Juniper Networks ( JNPR ), another company that has integrated AI deeply in product design, as I explained in a recent thesis .

Comparison with Peers (www.seekingalpha.com)

{kind=link}

Possible Demand Weakness For Equipment Makers

Coming back to Nokia, it must be mentioned that from its origins as a wireless radio access network or RAN provider, it now aims to increase its enterprise market share after restructuring operations into the Network Infrastructure and Cloud/Network Services business groups. This is in addition to the incumbent Mobile Networks group, which pertains to 5G RAN equipment. As such, the company possesses scale and competes with Extreme, Cisco ( CSCO ), and Juniper since 2020 after entering the data center switching market.

Interestingly, during Nokia's first quarter 2023 results, all these three groups grew revenues, but concerns were already raised about some "economic uncertainty impacting customer spending plans". Moreover, at that time, on April 20, the problem of inventory digestion, or customers taking longer to consume existing stocks and issuing fresh orders, was highlighted but was restricted to the Mobile Networks group. However, about 11 weeks later, or on July 14, weakness was also reported to affect the Network Infrastructure group.

Now, products from this business group support consumers, enterprises, hyperscalers like Microsoft ( MSFT ), or ISPs like Spectrum owned by Charter ( CHTR ) meaning that any weakness pertaining to Nokia could reverberate across the communications equipment industry and, this may be the reason why in addition to Extreme and Nokia, the five-day price returns of Cisco and Juniper have turned out to be negative as well (table above).

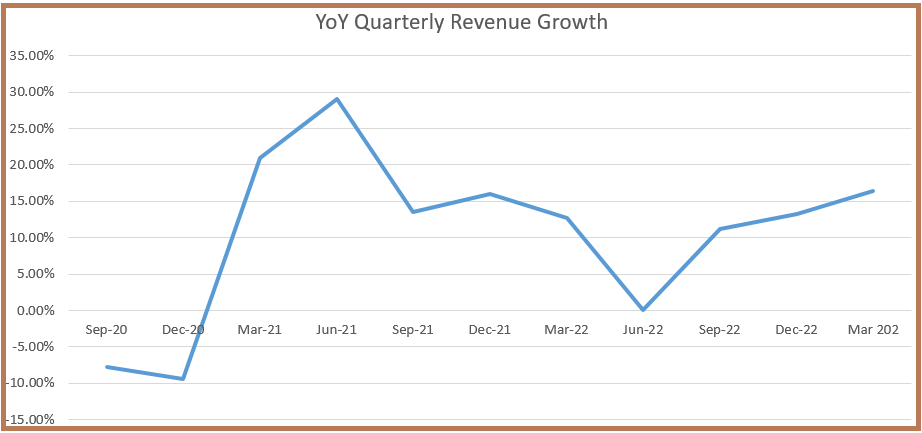

Focusing on Extreme, it has been growing at double digits in the mid-teens lately but well below previous growth rates of 21% and 29% in the quarters ending in March and June 2021, respectively, when the company was benefiting from a Covid-led surge in demand.

{kind=link}

Subsequently, demand was sustained but given that Extreme was itself supply constrained for components, it could not manufacture the networking devices in time to honor customer orders as I had pointed out in January . At that time, I had a Hold position on the stock based mainly on its ability to pass on additional supply-related costs to customers. However, I also mentioned that it was both "competitively well positioned" and progressing in resolving sourcing issues from China and Taiwan. About six months later, Extreme has progressed on both fronts resulting in the market rewarding it with a 43% upside.

This market optimism was also thanks to the additional tailwind constituted by both its distributors and end consumers building inventories as a buffer against future shortages, through the placement of advanced orders.

Backlogs, Topline, and Bottom Line

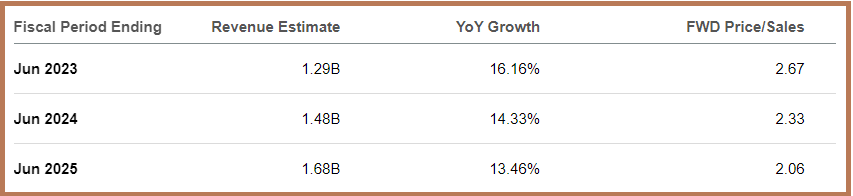

For Extreme, these orders translated into around $100 million in backlogs on a quarter-over-quarter basis. However, as per the management update, this is expected to shrink to around $75 million-$100 million by the first quarter of fiscal 2025 (or mid-2024 calendar year) as lead times get shorter due to improvements in the supply chain. Still, growth is expected to be in the mid-teens or around 15% to 17% through fiscal 2025, whose midpoint is aligned with the estimated 16.16% for the fiscal period which ended in June 2023 as shown below.

Revenue Estimates (www.seekingalpha.com)

{kind=link}

Thus, at a forward price-to-sales of 2.67x, Extreme appears fairly valued, which explains my Hold position on the stock. Furthermore, the more forward-looking topline estimates, namely for fiscal 2024 and 2025, already take into consideration that the demand-supply environment is now more normalized compared to the earlier supply-constrained one. These growth estimates are also justified from the viewpoint that enterprise IT spending, which encompasses Extreme's switches remains resilient.

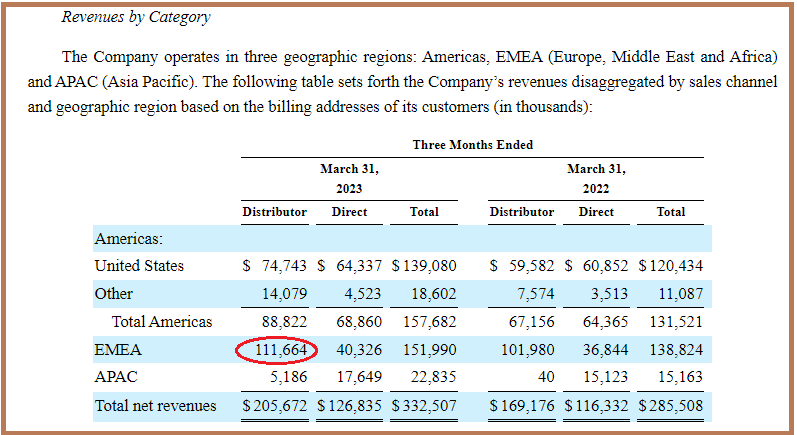

As for the bottom line, unlike Nokia which is seeing more margin pressures due to a change in geographical revenue mix as more sales are now generated in India compared to the U.S., this is not the case for Extreme currently. The reason is that in a high-demand environment, it can exercise pricing power. However, this may change in the later part of the year given that only 42% (139,080/332,507 as per the SEC filings below) of its third quarter 2023 (Q3) sales came from the United States, where the economy has been quite resilient .

SEC Filings for Q3 (www.seekingalpha.com)

{kind=link}

On the other hand, 58% of its sales were generated in the rest of the world at a time when global output growth should slow to 2.8% in 2023 from 3.4% last year according to the International Monetary Fund, and inflation should remain at 7% globally (after the 8.7% peak of 2022).

Time to Adopt Caution

In this case, without being utterly pessimistic, one can expect some margin pressures in case the dollar goes up again as equities suffer broadly as in October last year or investors flock to the greenback as a safe haven asset due to economic pains biting hard in some developed or emerging economies.

There is also the reliance on distributors for 61% (205,672/332,507 as per the above SEC filing) of overall sales, and as middlemen, they could ask for higher commission fees as wage inflation bites higher in the rest of the world. Asking for a greater share of profits may also be motivated by lower sales volumes in the balance of this year as their backlog is being consumed at a faster pace compared to customers to whom Extreme ships equipment directly.

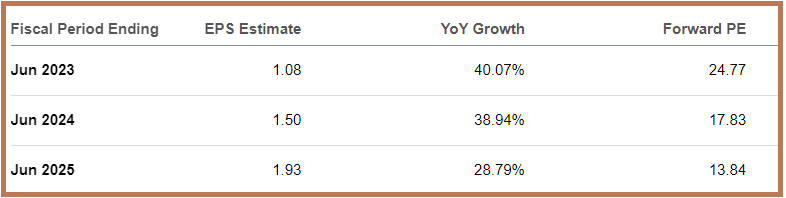

This may in turn result in higher distribution costs and impact Extreme's long-term gross margins of 64 to 66% expected through fiscal 2025 and whose midpoint represents nearly a 6% increase over Q3. This may in turn impact earnings projections further down the income statement. The basic reasoning here is that the math behind the above 38% EPS growth for fiscal 2024 (table below) has been done in a period of abnormal levels of backlog and high demand, and, now that shipment lead times are retrenching back (coming down), customers may be less willing to pay for inflated prices for the same products in the future.

Earnings Estimates (seekingalpha.com)

{kind=link}

Thus, after a one-year upside of above 160% (peer comparison table), which is much above the average, I believe it is now time to adopt prudence and wait for a management update during the fourth quarter earnings call expected on August 2 . Specific details to pay attention to include the evolution of the backlog, distribution costs, and supply chain status as all these factors are likely to impact gross margins going forward.

In conclusion, by going through some of Extreme's key products, this thesis has shown that it has been able to generate better revenue growth. Consequently, the market has rewarded the stock with an upside that is at least eight times more than peers. Nonetheless, the stock still remains undervalued based on certain metrics, which may be the reason why analysts rate it as a strong buy. However, my position is different due to macroeconomics in the rest of the world no longer being what it was last year and the level of customer inventories now not being favorable enough to justify those higher margin expectations.

For further details see:

Extreme Networks: Adopting Caution Following Nokia's Dim Outlook