EXTR - Extreme Networks: Consider Buying This Dip

2023-11-05 08:47:23 ET

Summary

- Extreme Networks is a global provider of software-driven networking solutions with a market cap of $2.3 billion.

- The company reported strong financial results for Q1 FY2024, with revenue growth of 19% YoY and EPS growth of 75% YoY.

- Despite a more pessimistic outlook for the next few quarters, the company remains optimistic about its long-term growth potential.

- Over the next three years, EXTR stock appears to be an attractive investment with strong growth potential, poised to recover from its current low valuation multiples as growth picks up.

Extreme Networks (EXTR) is a $2.3-billion market cap global provider of software-driven networking solutions, based in North Carolina. They design, develop, and manufacture wired, wireless, and software-defined wide area network (SD-WAN) infrastructure equipment. Their flagship product, ExtremeCloud IQ, is an AI-powered cloud network management solution that provides advanced visibility and control over users, devices, and applications. They also offer various add-ons like ExtremeCloud IQ - Site Engine for automation and analytics, and ExtremeCloud SD-WAN for software-defined wide area networks. In addition to networking equipment, they provide customer support and services.

In June 2023 , I wrote about the company and rated it a 'Buy' at the time, expecting the business growth acceleration and strong margins to keep driving the stock's performance. Since June, EXTR has indeed grown strong, posting a gain of nearly 70%, but eventually, the momentum turned negative and my rating is now no longer as good:

Seeking Alpha, the author's rating

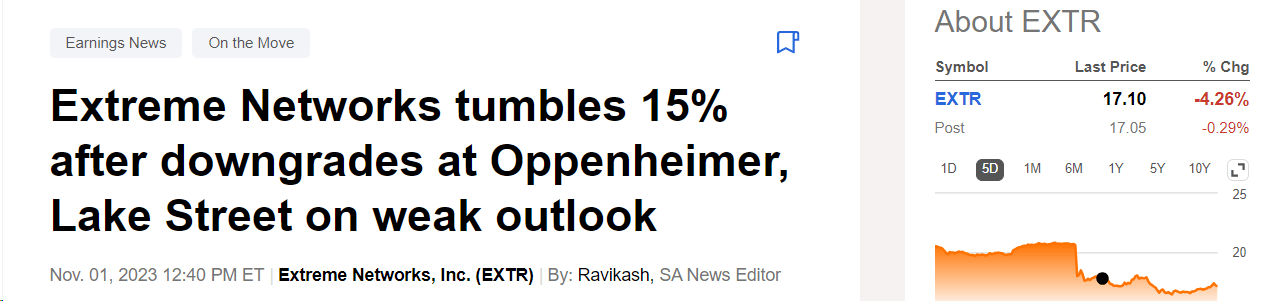

Since the beginning of November 2023, when the entire market was showing phenomenal strength, EXTR continued to fall after some banks downgraded their estimates after the company guided for a more pessimistic next few quarters than previously expected.

{kind=link}

Let's find out how such a sharp decline in recent days was justified.

Q1 FY2024 Results And Outlook

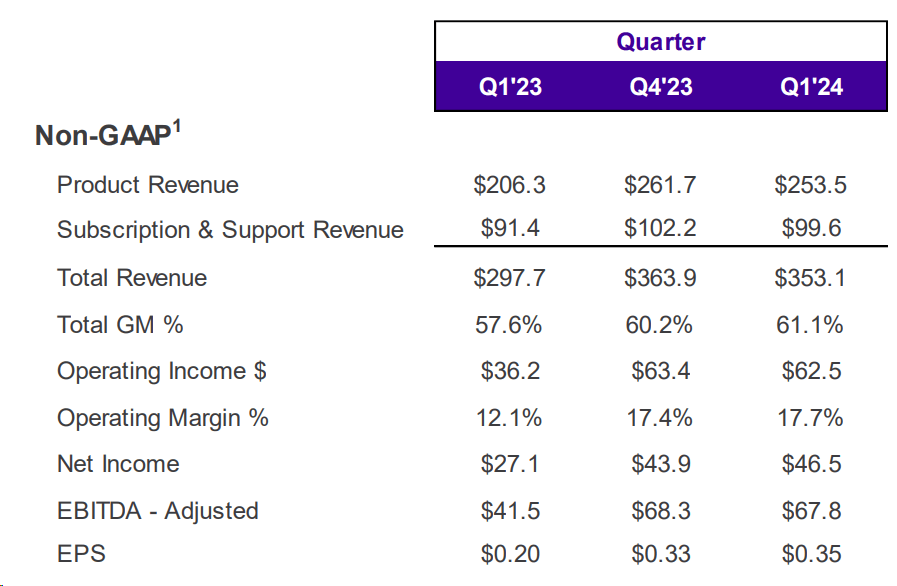

In Q1 FY2024 , Extreme Networks reported strong financial results, with a 19% YoY growth in revenue and a 75% YoY growth in EPS. EXTR expanded into larger deals, with the dollar value of deals over $1 million increasing. Cloud adoption remained strong, with a 30% year-over-year growth in Annual Recurring Revenue ((ARR)) to $141 million, and SaaS deferred revenue grew by 38% year-over-year. EBIT and net income increased by 71.6% and 72.65%, respectively, year-on-year, but decreased slightly quarter-on-quarter.

{kind=link}

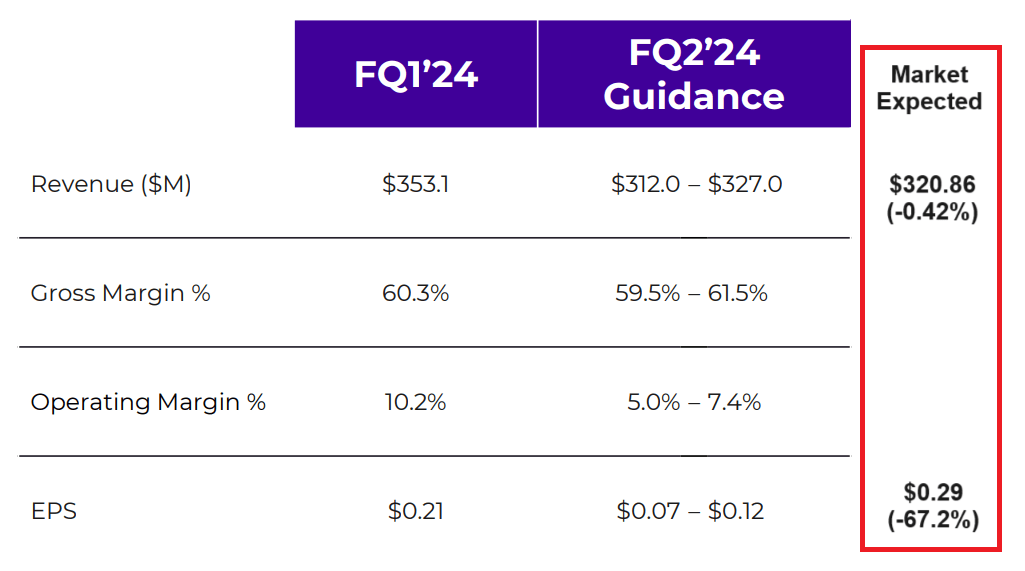

During the earnings call , the company mentioned that customer retention remained high, and they outpaced overall market growth in the quarter. However, they indeed adjusted their growth outlook due to macroeconomic factors, including higher interest rates and economic challenges in certain markets, which led to longer sales cycles and delays in orders. In fact, the new management forecasts deviated considerably from analysts' expectations - look at the variation in the EPS figures:

EXTR's IR materials, author's notes

{kind=link}

Despite the near-term challenges, the company outlined its strategic initiatives, including a focus on operational simplicity, unmatched flexibility, and cloud solutions that offer actionable business insights, security scale, and innovative technologies like AIOps and automation.

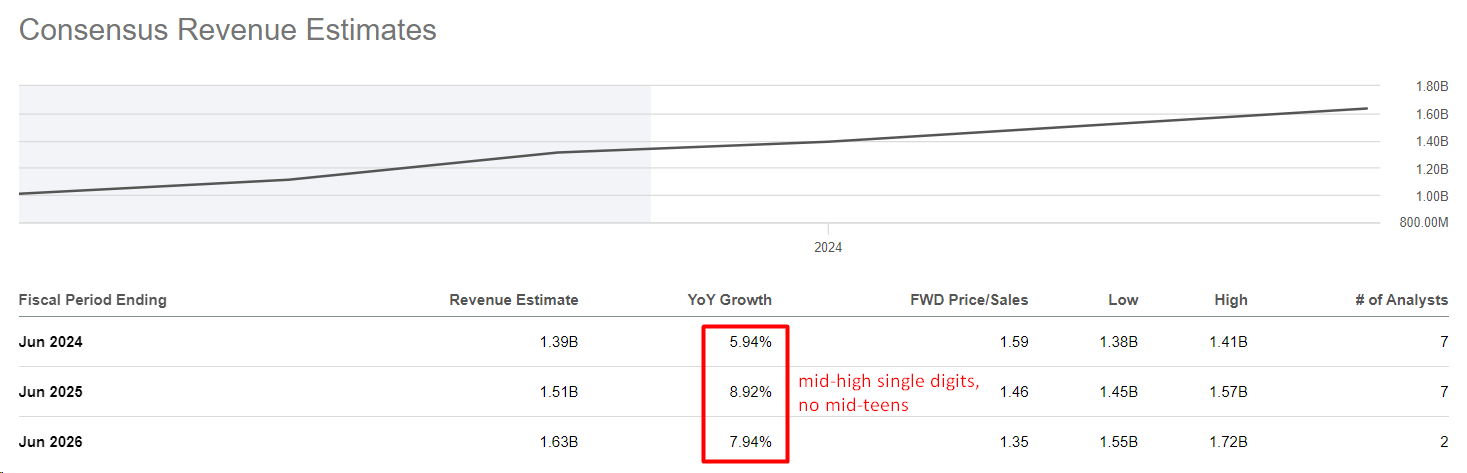

The company mentioned a healthy customer order backlog and reiterated its commitment to high teens operating margins in FY2024, allowing for over 25% EPS growth during the year. In the long term, they expect to return to mid-teens top-line growth and mid-20s operating margins. Compared to the projected growth rates that Wall Street analysts are awarding the company today, this forecast already looks quite optimistic:

{kind=link}

And this is despite the fact that EXTR's operating margin has still not reached the mid-20s that the company is aiming for in the long term according to the management commentary:

EXTR's IR materials, author's notes

{kind=link}

The management acknowledges a significant backlog in EXTR's channel, which has led to delays in customer demand as channel partners prioritize deploying the products they've received (this backlog, along with macroeconomic factors, was the reason for a slower outlook). However, they view this situation as a temporary "air pocket" and anticipate a return to normal demand once the channel partners complete their product deployments.

I do not see any serious negative changes in the balance sheet: EXTR's financial position continues to look strong with a current ratio above 1 and total debt down 12.31% QoQ.

The company only needs a few quarters, in my view, before the current headwind is no longer so significant.

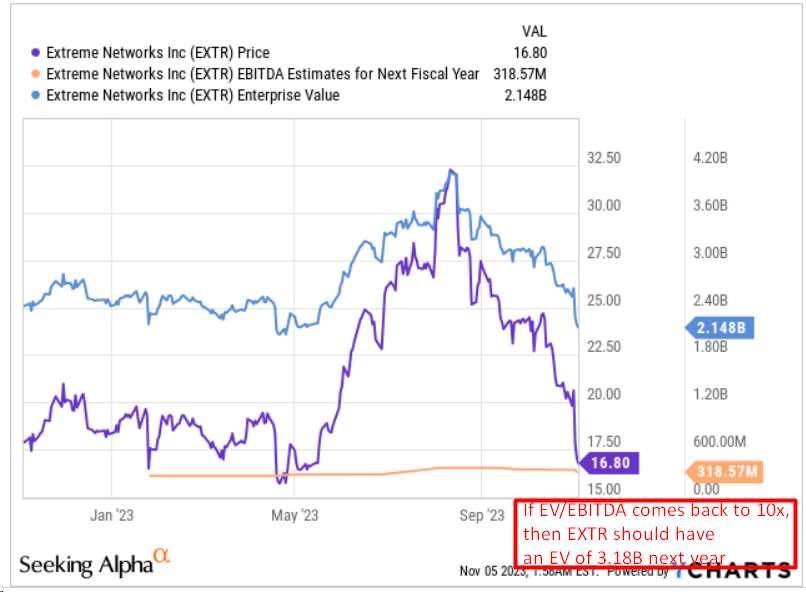

Meanwhile, EXTR is now trading at an EV/EBITDA ratio of 8.1x, which is well below the TTM value and historical norms for the stock.

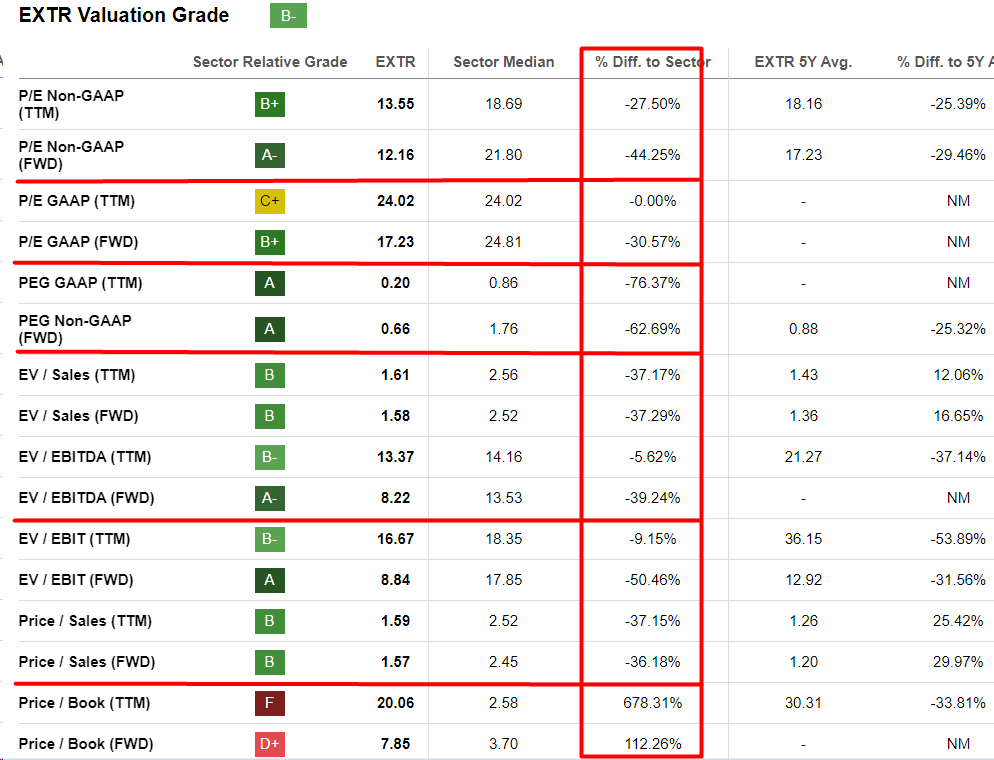

The median EPS ((FWD)) growth rate in the information technology sector is around 8%, and the CAGR over the last 3-5 years is 13.1%. For EXTR, these figures are 29.77% and 18.5%, respectively, according to Seeking Alpha's Quant System. In other words, the company's business growth is significantly outpacing the sector as a whole, which tells us that a slight premium to its valuation would be justified. In reality, however, we see a rather large discount, which is 30-60% in some places after the stock's recent correction:

{kind=link}

Therefore, I believe that the discrepancy between the current multiple and its historical values I have outlined above is likely to be short-lived. If the revised consensus EBITDA estimate is correct and EXTR's EV/EBITDA multiple rebounds to at least 10x next year, then by my calculations the company's enterprise value is undervalued by ~48% today .

{kind=link}

The Verdict

In my opinion, EXTR has overreacted as its valuation multiples have fallen so much in a matter of days due to challenges that are likely to disappear in a few quarters. I agree with the analysts that the EPS guidance revision was indeed much more negative than expected before the release of the last quarterly report. However, the forecasts for gross profit and EBIT margins held steady for the long term, as did the forecasts for long-term sales growth.

Of course, EXTR faces certain risks that could further affect its business. Its reliance on cloud computing makes it vulnerable to disruptions in the cloud computing industry, while its exposure to international markets introduces volatility and unpredictability. Additionally, the success of EXTR is closely tied to the effectiveness of its management team; any mistakes they make could have adverse consequences for the company's performance.

But despite the existing risks, I think EXTR is quite an interesting investment with high growth potential over the next 3 years, which should theoretically start to grow out of the current low valuation multiples as soon as growth accelerates again. I therefore confirm my 'Buy' rating.

Thanks for reading!

For further details see:

Extreme Networks: Consider Buying This Dip