EXTR - Extreme Networks: Impressive Performance Amid Tough Competition

2023-09-20 03:03:01 ET

Summary

- Extreme Networks demonstrates strong financial performance and continues to invest heavily in innovation.

- The company demonstrates solid revenue growth and improving profitability metrics momentum.

- EXTR stock is massively undervalued with a 67% upside potential.

Investment thesis

Extreme Networks ( EXTR ) is a rising star in a highly competitive market with several big players with substantial financial resources. Despite such massive competition, Extreme Networks demonstrates stellar financial performance and continues to invest heavily in innovation. EXTR demonstrates strong revenue growth momentum, and its profitability metrics are improving rapidly. The company targets a large market, and its rapid revenue growth suggests that innovation investments are paying off, making it well-positioned to sustain impressive top-line growth. My valuation analysis suggests the stock is substantially undervalued with a 67% upside potential. All in all, I assign the stock a "Buy" rating.

Company information

Extreme Networks provides cloud networking solutions with related services and support. The company designs, develops, and manufactures wired, wireless, and software-defined wide-area-network [SD- WAN] infrastructure equipment.

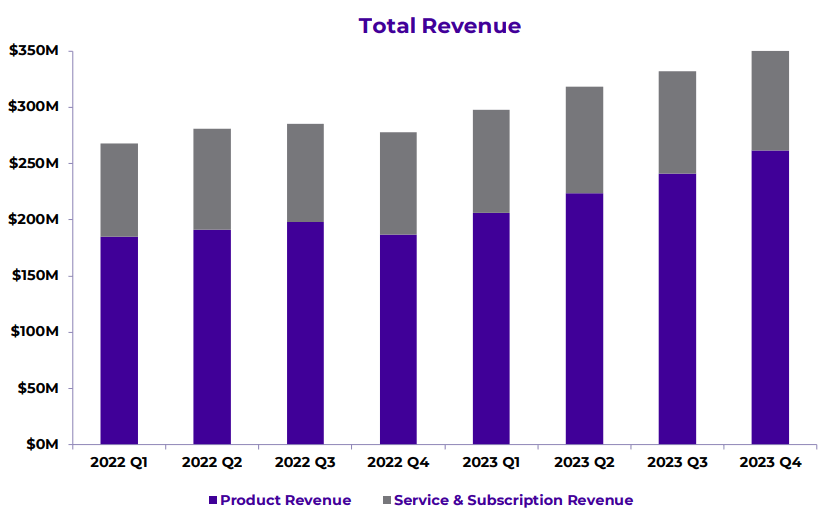

The company's fiscal year ends on June 30 with a sole operating segment. According to the latest 10-K report , the company generated approximately 55% of its sales outside the U.S. in FY 2023. Apart from product revenue, EXTR also generates sales from SaaS.

{kind=link}

Financials

The company demonstrated solid financial performance over the long term with revenue growth and improving profitability metrics. The topline compounded at a 10.8% rate annually, which is solid. The gross margin was consistently well above 50%, and the operating margin expanded from -2.5% ten years ago to 8.5% in the last fiscal year. The free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been consistently positive and has gotten closer to double digits in recent years.

{kind=link}

Widening FCF margin allowed EXTR to conduct stock buybacks in recent years, which is a positive sign for shareholders. At the same time, the company does not pay dividends, but given the ability to fuel revenue growth, I think that reinvesting in business is a more reasonable choice. The financial strength looks average to me because the company has a substantial leverage ratio, though EXTR's net debt position is relatively low, and the covered ratio looks comfortable.

Seeking Alpha

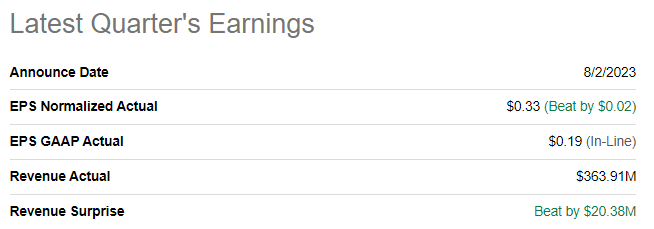

The latest quarterly earnings were released on August 2, when the company topped consensus estimates. Revenue demonstrated solid growth momentum with a 31% YoY increase. The adjusted EPS followed the top line and expanded from $0.15 to $0.33. The operating margin expanded notably YoY, from 4.2% to 10.6%. I like that this expansion was achieved not at the expense of innovation. The R&D to revenue ratio shrank by less than one percentage point and remained above 15%.

{kind=link}

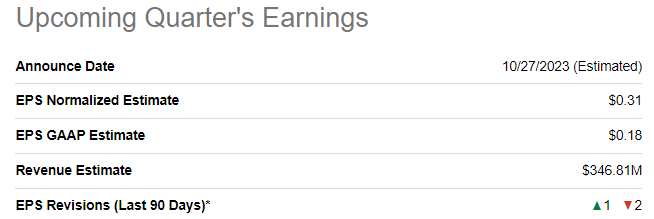

The upcoming quarter's earnings release is scheduled for October 27. Quarterly revenue is projected by consensus at $347 million, which indicates a 16.5% YoY growth. The adjusted EPS is expected to expand YoY from $0.20 to $0.31. That said, the momentum for revenue growth and profitability expansion is still solid.

{kind=link}

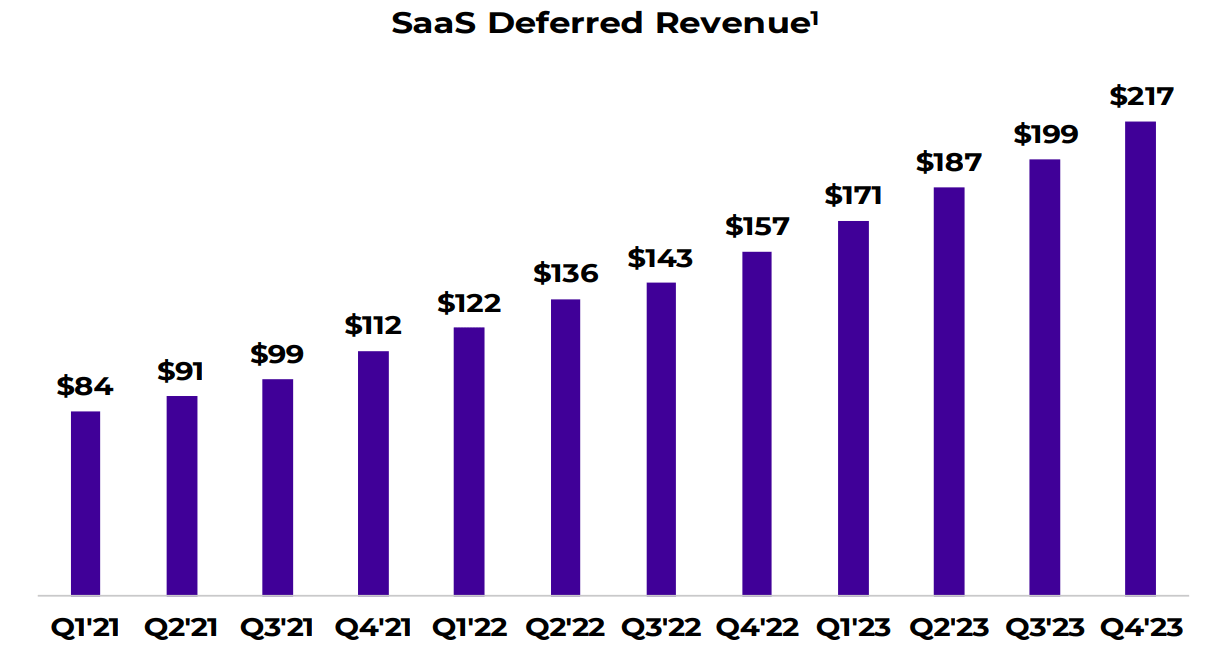

The current strong revenue growth momentum, together with a solid long-term track record of financial success, is a good indication that the company is well-managed. It is crucial for investors because the company operates in a promising market expected to compound at double-digits over the next five years. In its latest 10-K report, the company claims that its total addressable market is over $40 billion, which means there is still massive room for business growth in the long term. I also like that the company's business is diversified both from the geographical perspective and its set of offerings. The SaaS business demonstrated a solid dynamic of sequential QoQ deferred revenue growth over the last three fiscal years.

{kind=link}

Extreme competes with giants like Cisco Systems ( CSCO ), Hewlett Packard ( HPE ), and Arista Networks ( ANET ). At the same time, the company delivers strong revenue growth in this intense competition, which is a solid bullish sign to me. It is also important to mention that EXTR's gross margin aligns with the competition despite its smaller scale. This means the company is well-positioned to expand its FCF margin much wider as the business scales up. While competition with much larger players with substantial resources is tough, Extreme's smaller scale gives it the advantage to innovate faster than its hyper-scale competitors due to less internal bureaucracy and lower dependence on nurturing "cash cows".

Valuation

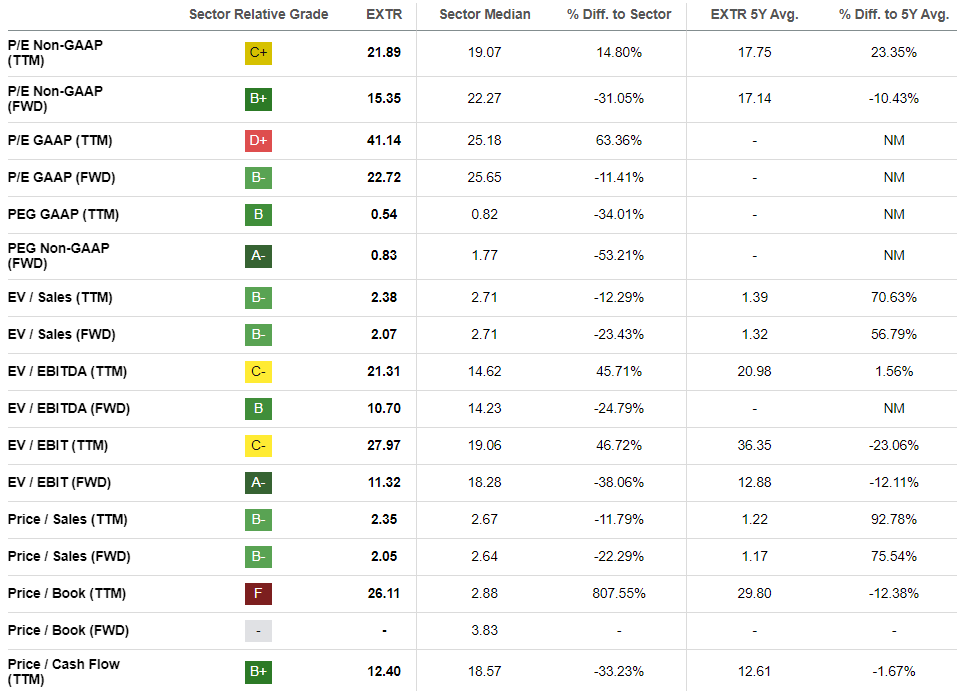

This year, the stock outperformed the broader U.S. market with a 31% year-to-date rally. Seeking Alpha Quant assigns the stock an average "C" valuation grade. Most of the multiples are substantially lower than the sector median but higher than the company's historical averages.

{kind=link}

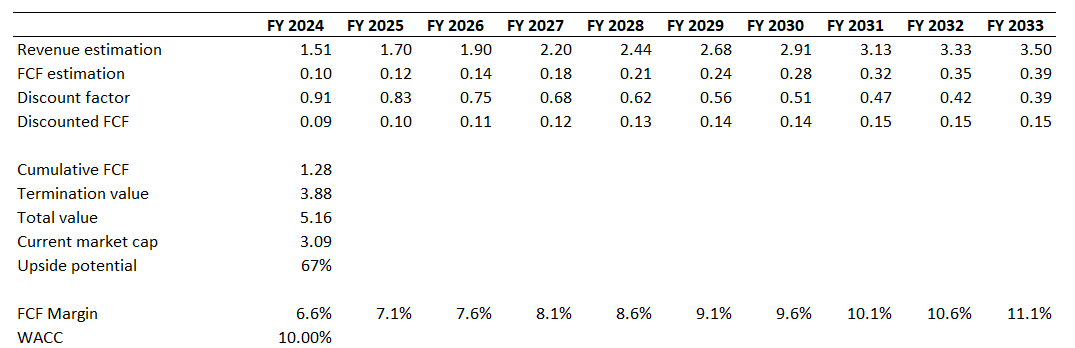

I want to continue my valuation analysis with the discounted cash flow [DCF] approach. I use a 10% WACC for discounting. I have revenue consensus estimates available for the next decade, and I think a projected 10% revenue CAGR is fair. I use the past five years' average FCF margin for my base year and expect a 50 basis points yearly expansion for the years beyond.

{kind=link}

According to my DCF simulation, the business's fair value is above $5 billion, which indicates a massive upside potential. That said, my target price for the stock is $40.

Risks to consider

As a growth company, EXTR constantly faces pressure to meet its ambitious revenue growth and profitability expansion plans. If there are hints that the company is lagging behind its aggressive growth trajectory, investors might be disappointed. At the end of the day, this will highly likely lead to massive stock selloffs, and it can take multiple quarters before the sentiment regarding the stock shifts to positive. That said, investors should be ready to tolerate volatility and be long-term holders of the stock.

Extreme generates a substantial portion of its revenue outside the U.S., making the company vulnerable to risks related to international trade. Among them, I consider the foreign exchange risk and changes in trade regulations as the most substantial.

The business faces significant revenue concentration risks. According to the latest 10-K report, sales to the top three customers contributed 53% to the total in the last fiscal year. High dependence on a very limited group of customers makes the company's earnings very vulnerable to spending decisions made by its major customers. That said, the financial difficulties of any of its significant customers might lead to substantial revenue decreases for EXTR.

{kind=link}

Bottom line

To conclude, EXTR is a "Buy". The company's stellar long-term financial performance together with solid current growth momentum suggest that its innovations are indeed appealing and attractive for customers. Risks and uncertainties are very high, but I believe that the 67% upside potential outweighs them.

For further details see:

Extreme Networks: Impressive Performance Amid Tough Competition