EXTR - Extreme Networks Looks Undervalued Based On FCF And EBITDA

2023-06-06 11:23:17 ET

Summary

- Extreme Networks, Inc. is a $2.8 billion market-cap networking company that specializes in providing software-driven solutions for enterprise and service provider networks.

- I like the way the company's balance sheet looks, bookings, revenue momentum, and margin expansion.

- In terms of FCF, EXTR stock looks undervalued when we consider that gross margin and EBIT margin are expected to increase by 90 and 80 basis points in Q4 [QoQ].

- My year-end target is $25.9 per share [21.36%], which is about in the middle of the 15-27% range I derived based on EV/EBIT.

The Company

Extreme Networks, Inc. (EXTR) is a $2.8 billion market-cap networking company that specializes in providing software-driven solutions for enterprise and service provider networks. It designs and manufactures network switches, routers, wireless access points, and other networking equipment. These products are designed to provide high performance, scalability, and reliability for the requirements of modern network infrastructures.

In addition to hardware [the Product segment, 72.5% of total sales], Extreme Networks also offers software solutions for network management, security, and analytics [the Service and subscription segment, 27.5%]. EXTR's management software enables network administrators to monitor and control their networks to ensure optimal performance and security. Its analytics solutions help organizations gain insight into network traffic, user behavior, and application performance.

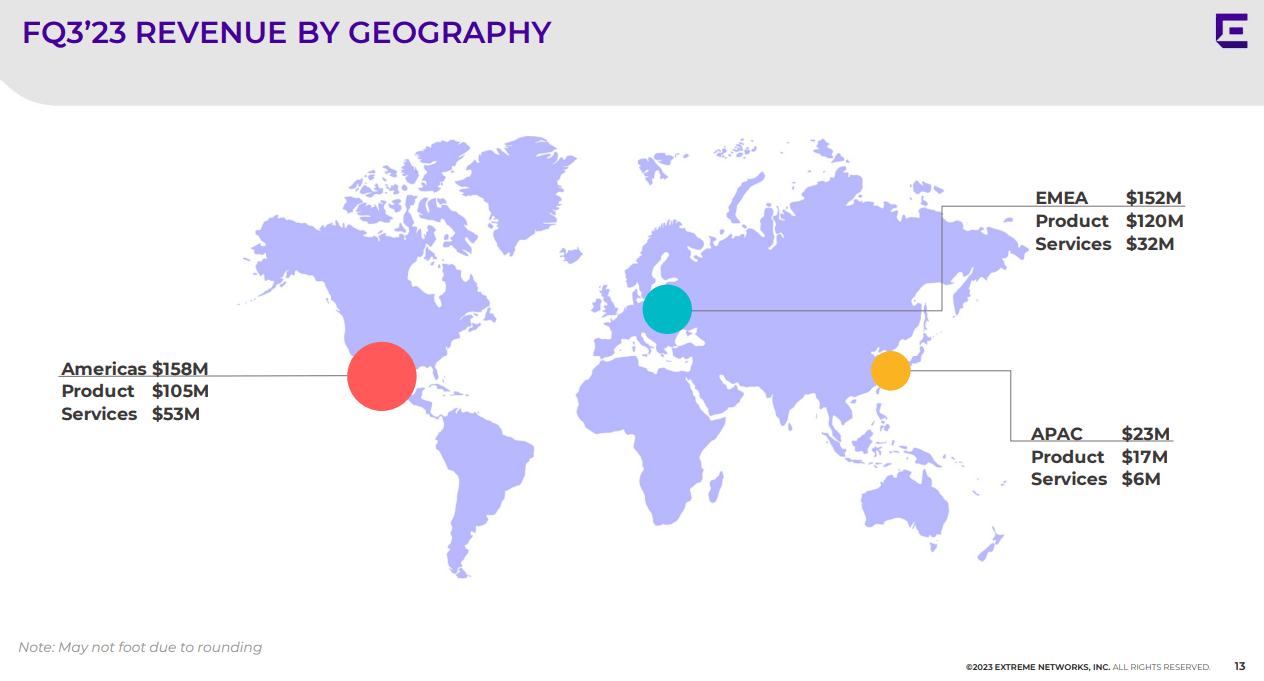

Extreme Networks serves a variety of industries, including education, healthcare, government, hospitality, and industrial. Customers range from small and medium-sized businesses to large enterprises and service providers. Roughly 47.5% and 45.6% of consolidated sales come from North America and EMEA markets , respectively, while the remaining ~7% come from APAC, which is quite good in terms of geography and geopolitical risk profile, in my view.

{kind=link}

According to the company's recent 10-Q , the management estimates the total addressable market for its Enterprise Networking solutions, including cloud networking, wireless local area networks ((WLAN)), data center networking, ethernet switching, campus LAN, and SD-WAN, to be around $33 billion. The company anticipates this market to grow at approximately 12% annually over the next 3 years. It further identifies specific market segments, such as a $4.6 billion opportunity in 5G and data centers and a $2.2 billion SD-WAN market, which it plans to target. Additionally, Extreme Networks participates in the $4 billion networking software market, offering solutions like cloud-based network management, network automation, on-premises network management, and other related software.

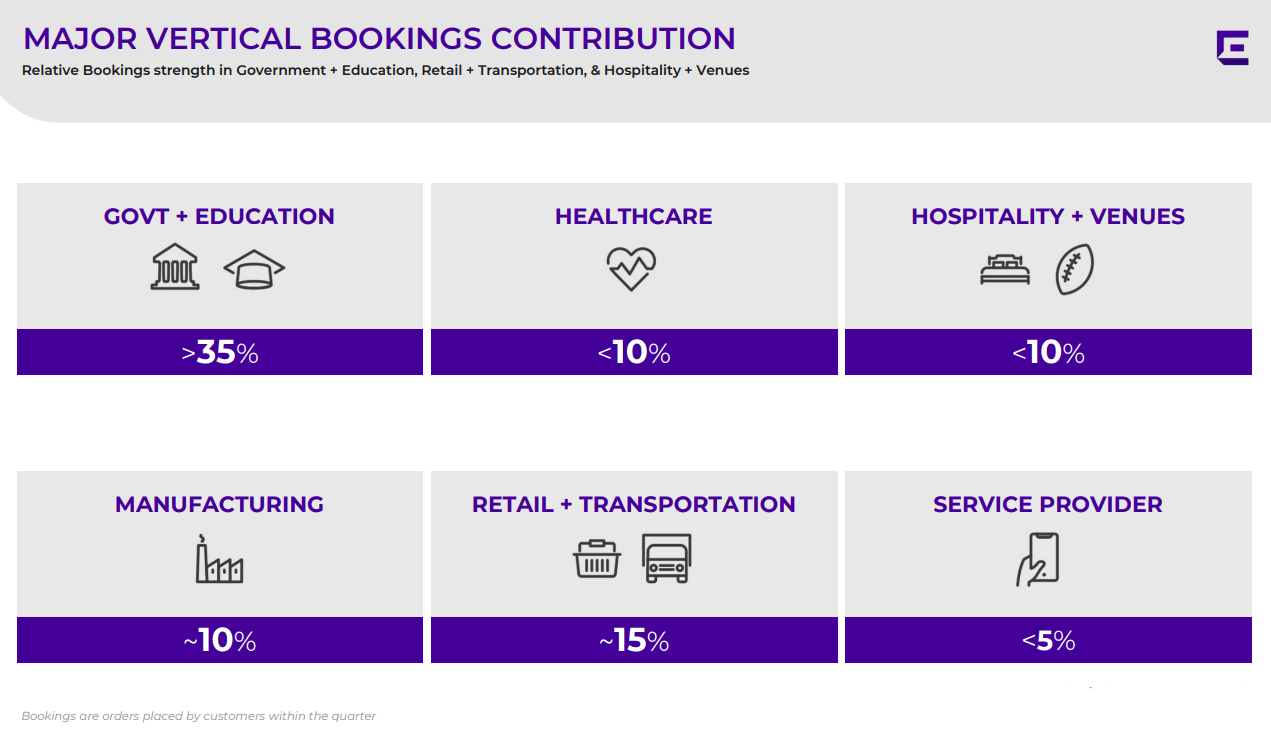

In Q3 FY23 [the latest fiscal quarter, reported on April 27, 2023] EXTR's total revenue grew by ~16.5% and product revenue grew by ~21.5% YoY, contributing to double-digit growth in 8 out of the past 9 quarters, according to the CEO's words during the earnings call . Product orders grew 6% sequentially, and orders from new customers increased by 20%. Despite the typical seasonal decline in bookings for Q3, Extreme Networks experienced growth compared to the previous quarter, reflecting strong demand. In terms of vertical mix, government, and education continue to be Extreme Networks' largest vertical, accounting for over 35% of total bookings in Q3. The company's significant wins in the retail sector have led to an increased mix of retail, transportation, and logistics, which now represents 15% of bookings. The manufacturing vertical remained stable at around 10%, while the sports and entertainment vertical experienced growth, making up slightly less than 10% of bookings.

{kind=link}

The company expects more normal seasonality and higher sequential growth in Q4. It anticipates total revenue growth to accelerate to >20% YoY based on improved product availability. Extreme Networks reiterates its long-term growth outlook in the mid-teens through fiscal 2025, driven by market share gains.

The non-GAAP operating margin surpassed the 15% mark for the 1st time. EXTR also saw an increase in EPS to $0.29 cents in Q3, up from $0.27 in Q2 and $0.21 in the year-ago quarter. It now expects bottom-line earnings trends to continue, with earnings growing faster than revenues over the long term due to increased gross margins and operating leverage.

{kind=link}

Extreme Networks secured significant wins and deployments during the quarter, including Kroger ( KR ), one of the largest US grocers, Ahold Albert Heijn, a global supermarket chain, a major healthcare provider in Saudi Arabia, Cedar Fair amusement parks, Catawba College, and sports franchises such as Amica Mutual arena and Prudential Arena. It has also established new partnerships with Comcast ( CMCSA ) and implemented new go-to-market motions with Verizon ( VZ ). Additionally, the company has built stronger relationships with large US-based resellers, leading to significant growth in E-Rate awards.

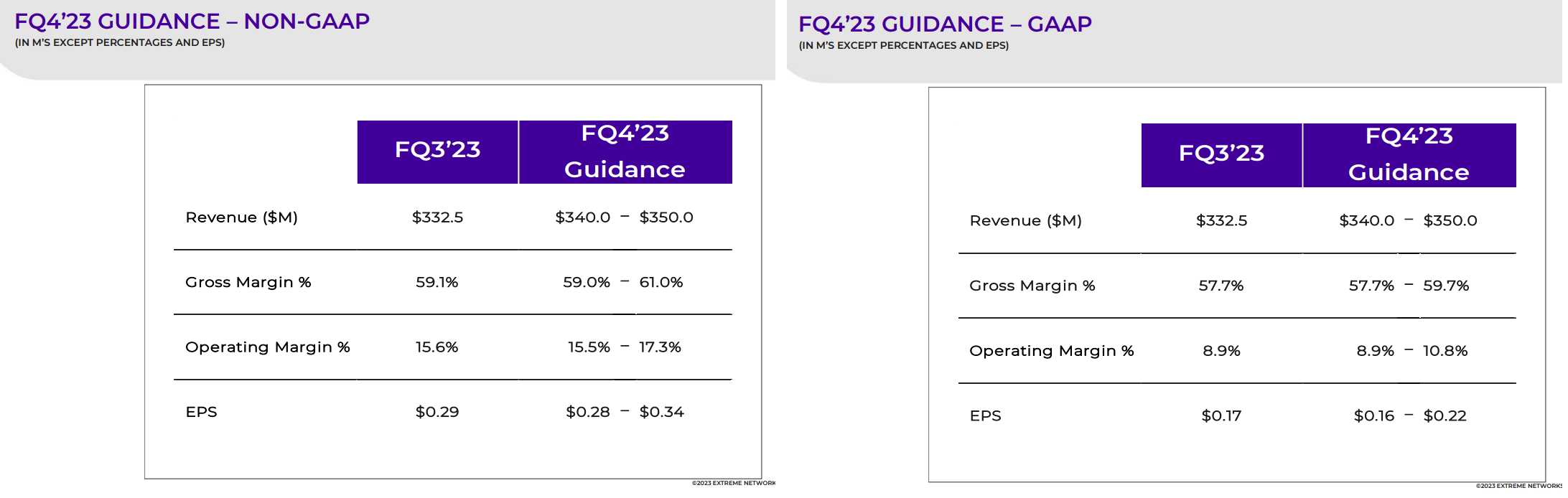

Based on the aforementioned new partnerships, improved margins, and a positive outlook, management has provided the following financial projections for Q3 and Q4 FY2023:

{kind=link}

To all this, it's also worth mentioning the improvement of the balance sheet: In the third quarter, the company repaid $25 million in debt and repurchased $25 million worth of stock, leaving net debt at just $34 million. Liquidity ratios look good: Current assets almost fully cover current liabilities, and cash on the balance sheet currently stands at 8.2% of the company's market capitalization, while the ratio has increased by almost 17% since the beginning of the year.

If everything is so good, maybe all the positives are already in the price and EXTR shouldn't be touched because of its insufficient richness? Let's figure it out .

Valuation

EXTR stock is now trading at an FCF yield of 7.72%, which is 347 basis points higher than the historical average of 4.25% over the past 10 years:

I forgot to mention that EXTR's cash conversion cycle was 22 days in Q3, which is 2 days less than in Q2. The company is making some progress on cash generation and management is focusing on that both in the presentation and during the earnings call:

Q3 earnings per share were $0.29 at the high end of our guidance entering the quarter. This quarter, we generated free cash flow of $45.8 million, driven by record EBITDA as well as a sequential two-day improvement in our cash conversion cycle to 22 days.

Source: Cristina Tate, EXTR's Interim CFO

That is why in terms of FCF EXTR stock looks undervalued when we consider that gross margin and EBIT margin are expected to increase by 90 and 80 basis points, respectively, in the 4th quarter [QoQ], based on the midpoint of management's guidance range. This means that if everything else remains the same, the company will report an increased FCF yield, assuming no change in cash conversion and higher gross and operating margins in Q4.

In terms of EV/EBITDA, EXTR stock looks a bit expensive in absolute terms at current levels, but from a historical perspective, this valuation multiple is close to the lower bound. The multiple for the next year prices-in a ~44% decline from TTM levels, which is too much in my opinion.

The momentum of the company's EBITDA margin is on an upward trajectory, and we know this will continue for the foreseeable future thanks to strong bookings and deferred revenues, as well as new partnerships.

At the EXTR's low in mid-2022, the stock was trading at 20x EV/EBIT, while the TTM is now 33.5x. Let's assume the company hits the guidance midpoint of a GAAP EBIT margin of 9.85% and revenue of $345 million [also midpoint] in Q4. Then FY2023 EBIT should be $107.1 million on revenue of $1,294 million.

That is, the market is pricing a forward EV/EBIT of ~26x [18% higher than the 2022 low] as the company continues to improve profitability and growth rates. I think it would be fair to maintain this multiple for the end of this year - which means that EV/EBIT should be 30-33x, implying an upside potential of 15-27% for the current share price.

The Bottom Line

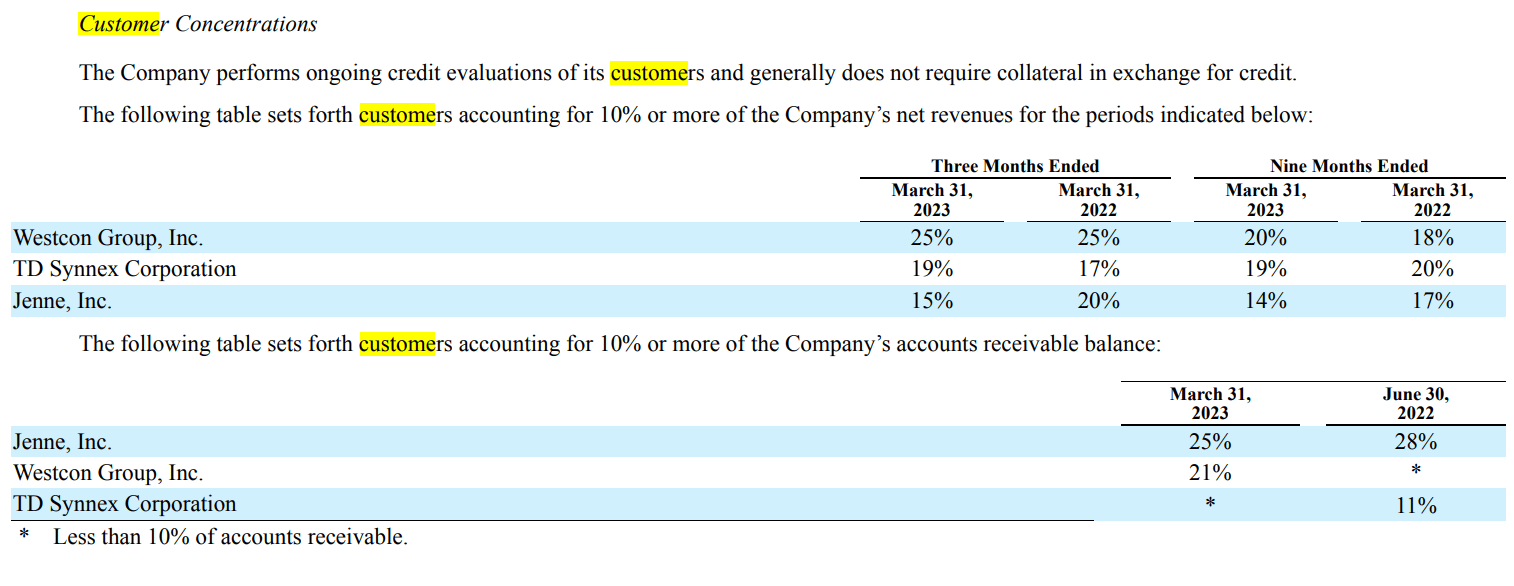

As always, my buy-rated thesis carries a number of risks. First, the $2.8 billion market cap carries liquidity risk - in the event of a massive market sell-off, the stock could fall quite sharply as the free float suffers from low demand. Second, the Communication Equipment industry, of which the company is a part, is cyclical, and demand for EXTR products, no matter how good, can plummet if major consumers cut their budgets. Incidentally, EXTR has a fairly large binding to just several consumers, which adds even more risk here:

{kind=link}

Despite the risks involved, however, I see a more positive picture for EXTR. I like the way the company's balance sheet looks, bookings, revenue momentum, and margin expansion. My year-end target is $25.9 per share [21.36%], which is about in the middle of the 15-27% range I calculated above.

Thanks for reading!

For further details see:

Extreme Networks Looks Undervalued Based On FCF And EBITDA