EXTR - Extreme Networks: Thanks To The Extreme Overreaction I Opened A Position Early (Rating Upgrade)

2023-12-05 04:57:53 ET

Summary

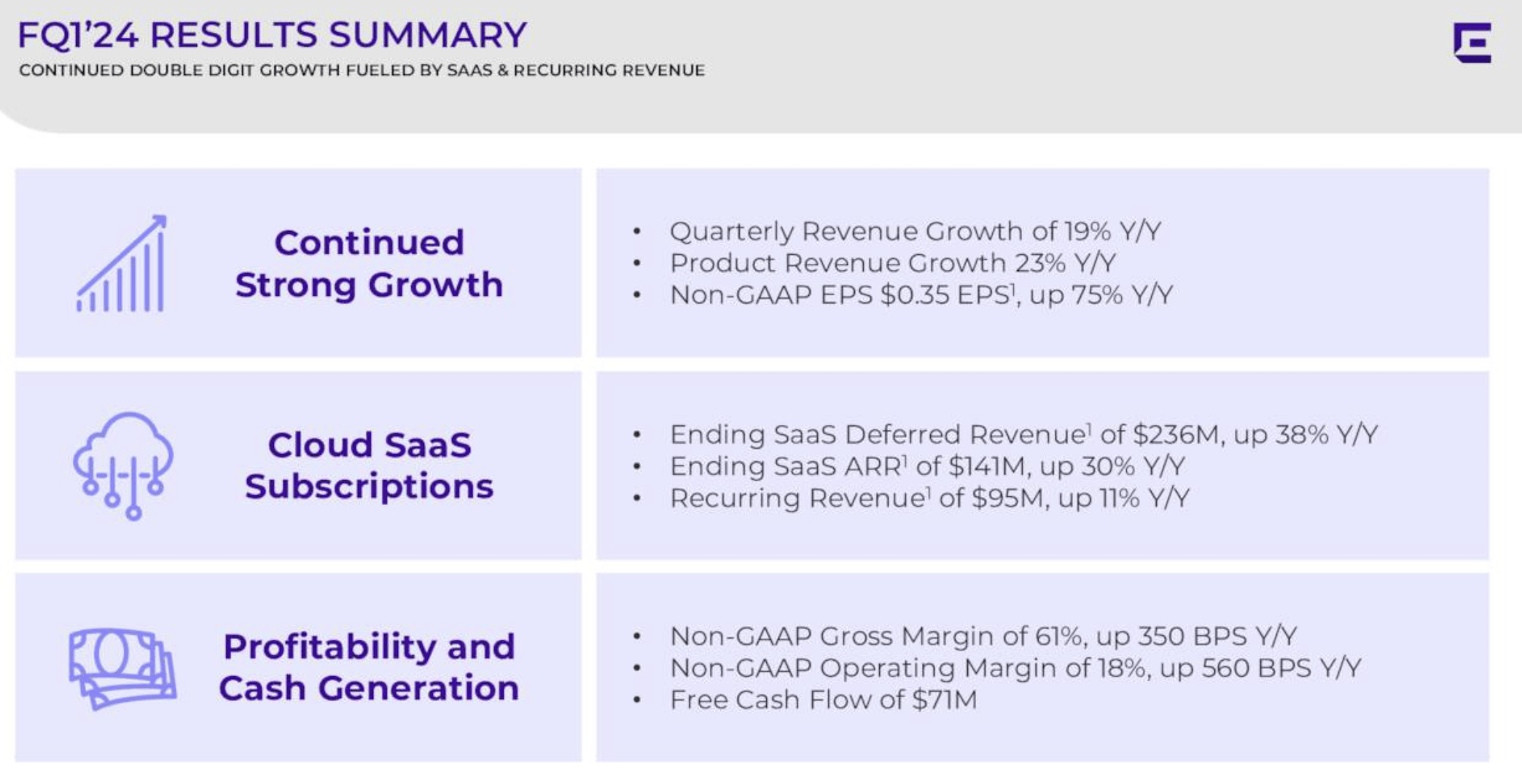

- Extreme Networks reported strong Q1 '24 earnings, beating expectations with revenue growth and improved margins.

- The market reacted negatively to weak guidance, leading to a significant drop in share price.

- Despite short-term volatility, EXTR's long-term outlook remains strong, especially in the cloud and AI/ML sectors.

Investment Thesis

Extreme Networks ( EXTR ) reported Q1 '24 earnings last month, which were great numbers-wise, however, the market didn't like the weak guidance. This overreaction brought an opportunity for long-term investors like me to start a position in a great company with a great long-term outlook and I was able to add the company to my portfolio much earlier than anticipated. I am upgrading my rating to a buy, since the bullish thesis is still intact, even if the outlook for the upcoming year is seen as terrible.

Briefly on the Company

Extreme Networks is a company that essentially helps the internet run smoothly. If we think of the internet as a highway, EXTR is the one to build the roads, bridges, and tunnels so that everything goes as smoothly as possible. The company builds switches, routers, and Wi-Fi access points. It also employs AI and ML to optimize traffic, which helps predict any obstacles it may encounter, and keep the huge amount of data safe against hackers. In such a connected world, EXTR is an essential company that will be relevant for many years to come, if it continues to operate at such a high level as it has.

Comments on the latest earnings

Overall, I think the numbers for Q1 '24 were very good! Revenues and EPS beat expectations. Revenue came in at $353m, which is almost a 19% increase y/y. SaaS ARR came in at $141m, up 30% y/y. The company doubled its GAAP EPS going from $.09 to $0.21 y/y. GAAP and non-GAAP margins saw fantastic improvements also, around 400-500bps across the board y/y.

{kind=link}

So, why have the company shares plummeted since reporting? Many analysts and investors didn't like the guidance. What followed after that were downgrades from many analysts. Was it justifiable? If we focus only on the short run then sure, it is justified. These quarterly upgrades and downgrades are surely meant to be for the traders and not actual investors who focus on the longevity of the business. Since I don't tend to trade stocks very often and occasionally options, the downgrades brought an opportunity I asked for since my previous article back in September when I rated the company a hold and wanted a pullback.

Comments on the Outlook

Not much changed since my last coverage of the company, since it has been only around two months, however, what did change was the biggest gripe I had with the company, which was its share price trading above its fair value. Now that the share price has retreated 33% since then, I believe the risk/reward is much more enticing than it was before.

Price change since September '23 (Seeking Alpha)

Since I still believe in the company's long-term outlook, which is very strong in the cloud and AI/ML area in my opinion, the company is very attractive right now for a long-term hold. EXTR is operating in one of the most promising segments right now and the growth is still very robust, which is much more than what the analysts are estimating, I believe that the only reasonable number to go by is the upcoming fiscal year because it is impossible to predict what the company will do in such uncertain environments.

With such a strong quarter as Q1 '24, I don't see the company performing very badly. In the short run, yes, we will see some lower numbers as the demand softens, however, once we get through this uncertain time, the company will return to robust growth that will match the overall sector CAGR, which is around 16% growth through '26.

Margins

The company so far has done a tremendous job at improving margins in such a tough year, as shown in the first image above. The management is doing a phenomenal job at finding ways of cutting costs that play a large role in efficiency and profitability. Even with lowered guidance, the management is looking to increase EPS by 25% for FY24, which is very impressive, and just shows that the management knows its company very well and knows where to strategically cut costs during the tough times. The management is eyeing the 62%- 63% gross margin range, which looks to be very achievable if we look at how much the company has already improved from the previous year.

AI and ML

In my previous article, I mentioned that the company is trading a bit too high because of the AI/ML hype, however, now that the company's share price retreated considerably, which was a total overreaction, AI and ML become a massive driver for the company's success once again. The AI and ML market in networking is expected to grow at a whopping 33.5% CAGR (page 5 of the report) through 2027, and Extreme Networks will be able to capture a decent share of that growth in the long run if it plays its cards right. These AI and ML initiatives will play a huge role in the company's ambition of achieving that double-digit long-term growth.

Risks of the Thesis

The biggest risks I believe are all to do with the short-term outlook, which is clouded by the softening demand and top-line growth. The company is going to experience a lot of volatility for the next few quarters in my opinion, and even if the management is going to guide for subpar numbers, the investors will forget that they did that and might bring the share price further down, even though the slowdown should have been priced in already. This is going to bring an even better entry point to average down for long-term investors like me, and I welcome that.

The US and EU economies are not out of the woods yet. Inflation, although, not as prevalent as before, still is very sticky, and it would only take one bad CPI read to send indices off the ledge and into bear territory. If the company can perform with such numbers as it did for Q1 '24 or even slightly lower, the company's long-term outlook is still intact and it should be able to weather the downturn that is yet to come, if it'll come at all.

The potential benefits of AI and ML are massive, however, we still don't have much regulation in terms of privacy and data collection. AI uses data collected from many different sources. EXTR needs to ensure that the data collected and trained in its AI models will be as transparent as possible to avoid scrutiny of data misuse and will have to implement security measures to gain the trust of its customers.

Valuation

I went ahead and updated my previous intrinsic value calculation, which has slightly more conservative estimates so that I would get a higher margin of safety. Below are my revenue estimates, which I think are very conservative in the long run, especially considering that the company feels very confident in achieving double-digit long-term growth.

{kind=link}

In terms of margins and EPS, I decided to go considerably lower than what the analysts are estimating. As I mentioned earlier, it is impossible to predict what the company is going to do 2 years from now, since even the management is hesitant to predict. Sometimes the management doesn't even want to provide numbers for the upcoming year. So, the best I can do is go with some conservative estimates and hope that the company performs better. At least that way I get a good night's sleep knowing that I have beaten down the company's estimates, so it can only go up from there unless we get a complete shift in operations and economic environment that could change the company's long-term prospects, at which point I would have to reassess. Below are those estimates.

{kind=link}

On top of these rather conservative estimates, I decided to keep the same additional margin of safety of 25% just to beat the estimates down and stress-test the company. With that said, the company's intrinsic value is $18.45, which is slightly lower than what I previously had, but still higher than what the company is trading at right now, therefore I am upgrading my rating to a buy.

{kind=link}

Closing Comments

My price alert of $20 a share went off some time ago, however, I didn't have time to re-visit straight away as I had other stocks to look at. I'm glad I skipped out on it until now as the company continued its unfair plummet and provided me with an even better entry point than $20 a share. I have opened a small position to start with and will be adding more over time. There is no need to rush into a full position yet as the myopic investors that focus on the short term may bring an even better entry point, and I welcome it.

The company is a strong competitor in the segment and has a very good outlook in the long run, which may be plagued by short-term noise, eventually unlocking value for patient shareholders like me. As I said I don't think the 15% drop in earnings was justified, but I was sure happy to see it since I was able to start a position in the company much earlier than anticipated.

For further details see:

Extreme Networks: Thanks To The Extreme Overreaction, I Opened A Position Early (Rating Upgrade)