EYPT - EyePoint Pharmaceuticals: A Puncher's Chance For Long Acting Eye Disease Drug Success

2023-05-30 08:00:48 ET

Summary

- EyePoint is a $200m market cap biotech focused on eye disease.

- The company's long-acting Durasert technology has been supporting its commercial product, YUTIQ, which earned $28m of revenues in FY22.

- EyePoint recently announced however that it had sold YUTIQ to Alimera Sciences for $75m upfront plus $30m in instalments, and royalties on net sales.

- The company's focus now turns to its Phase 2 stage candidate EYP-1901 - which could be used as a maintenance therapy after treatment with Regeneron's Eylea.

- It could be the case that EYP-1901 need to only be dosed on a 6-monthly basis, as opposed to Eylea's ~6-weekly basis. That ought to open up a substantial market opportunity for EyePoint - or make it a buyout target.

Investment Overview

EyePoint Pharmaceuticals ( EYPT ) is a Watertown, Massachusetts based ocular disease focused biotech whose share are currently trading at $6 per share - up 67% so far this year, although down 70% on a 5-year basis - giving the company a market cap valuation of just over $200m.

EyePoint has developed proprietary "Durasert" technology for sustained intraocular drug delivery - according to the company's 2022 10K submission :

Durasert allows for the development of a miniaturized solid cylinder of drug for sustained "zero-order kinetics" release delivered through a single intravitreal injection in the physician's office. A Durasert intravitreal insert is designed to provide consistent, sustained intravitreal delivery of a drug over a period of months to years and can be tailored to each drug and disease indication.

Eye disease markets are crowded and competitive - but also highly lucrative for the right drugs. For example, the wet age-related macular degeneration ("wet AMD") market is discussed as follows in EyePoint's 2022 10K submission .

As the proportion of people in the U.S. age 65 and older grows larger, more people are developing age-related diseases such as AMD. From 2000-2010, the number of people with AMD grew 18 percent, from 1.75 million to 2.07 million. By 2050, the estimated number of people with AMD is expected to more than double from 2.07 million to 5.44 million.

Currently, New York based Pharma Regeneron's ( REGN ) Eylea (aflibercept) is the leading therapy for Wet AMD, driving close to $10bn of sales in 2022. Eylea mechanism of action is described by Regeneron (in its annual report) as follows:

a soluble fusion protein that acts as a vascular endothelial growth factor ("VEGF") inhibitor, formulated as a 2 mg intravitreal injection for the eye

Lucentis, which has a similar mechanism of action ("MoA") to Eylea, and is marketed and sold by Roche ( OTCQX:RHHBY ) in the US, and by Novartis ( NVS ) ex-US, also earned ~$2.8bn of revenues in 2022. Both Lucentis and Eylea are injectable therapies, requiring an injection approximately every 4-8 weeks.

Earlier this month, on May 18th, EyePoint announced the sale of its commercial product, YUTIQ - a "once every three-year treatment for posterior segment uveitis in the United States" (source: Q321 10Q submission ) - to Alimera Sciences ( ALIM ). According to the press release:

EyePoint received a $75 million up-front cash payment at closing and will receive an additional $7.5 million in equal quarterly installments in 2024. In addition, commencing in 2025, EyePoint will receive a low to mid double-digit royalty on Alimera's related U.S. net sales above defined thresholds for the calendar years 2025-2028.

YUTIQ earned EyePoint $28.3m of revenue in FY22, and $7.4m in Q123, and is more or less EyePoint's only source of revenue, after reimbursement was discontinued for its only other commercial product, DEXYCU at the beginning of this year.

It may seem a little odd for a small biotech to be selling its only commercial product - although the $75m upfront payment plus additional 4 payments of $7.5m represents nearly 4 years of product sales, and EyePoint will still collect royalties on net sales.

More importantly, however, the sale of Yutiq enables, according to EyePoint's CEO Nancy Lurker:

This transaction completes EyePoint's transformation into a pure play drug development company focused on advancing and expanding a pipeline of sustained delivery treatments for serious eye diseases, including our lead product candidate EYP-1901, currently in Phase 2 trials in wet age-related macular degeneration and non-proliferative diabetic retinopathy.

This value-creating transaction has enabled EyePoint to pay off all outstanding bank debt at closing, reduce our projected SG&A spending and extend our cash runway into 2025 as we prepare for the potential Phase 3 pivotal trials for EYP-1901

In other words, EyePoint is selling Yutiq to fund development of its lead drug candidate EYP-1901, discussed as follows in EyePoint's 2022 10K:

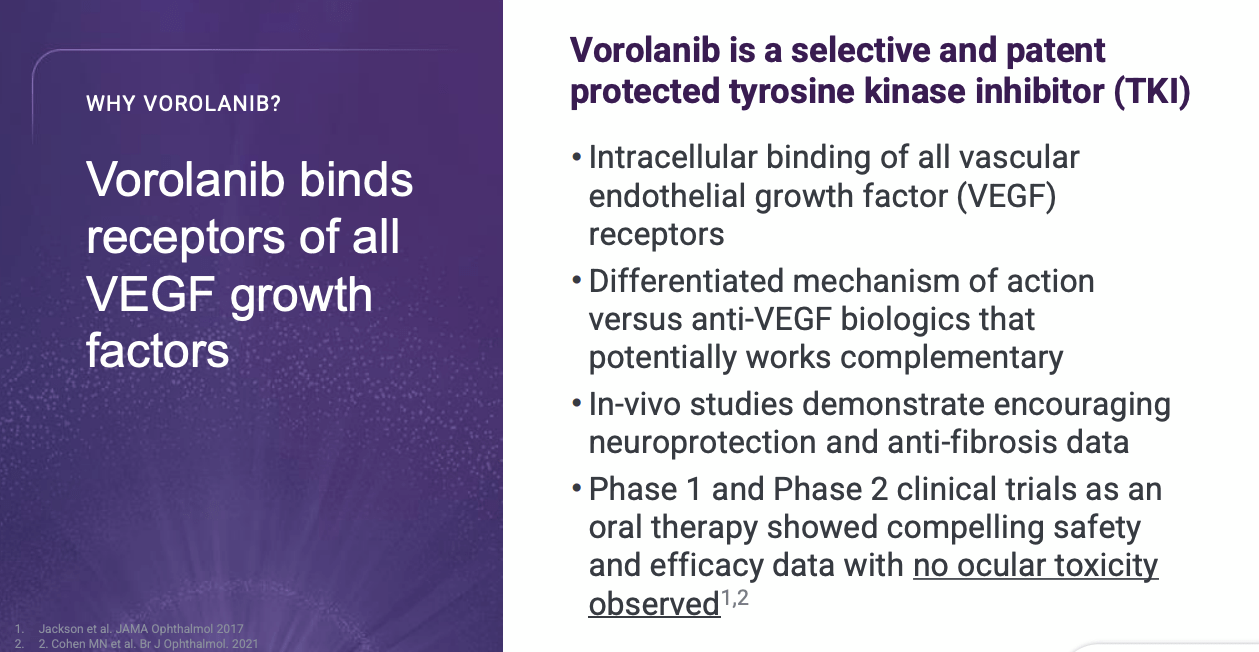

EYP-1901 is an investigational product and our lead pipeline program deploying a bioerodible Durasert insert of vorolanib, a selective and patented tyrosine kinase inhibitor (TKI), that potentially brings a new mechanism of action and treatment paradigm for serious eye diseases beyond existing anti-vascular endothelial growth factor (VEGF) large molecule therapies.

The unique selling point here appears to be the "sustained delivery" angle, i.e. EYP-1901 could be administered in a physician's office once every 6 months, when the likes of Eylea and Lucentis must be administered once every couple of months. The sale of YUTIQ appears to show that management are increasingly confident that its pipeline therapy can ultimately secure approval for commercialisation, and once on the market, offer a more convenient, longer lasting, and more effective therapeutic alternative to the likes of Eylea and Lucentis.

Given the near double-digit billion sales of Eylea, it seems obvious that, were EYP-1901 to ace its 2 Phase 2 studies, one in Wet AMD and the other in non-proliferative diabetic retinopathy ("NPDR") - expected to become a $12.3bn market by 2032 - then its share price is likely to grow substantially based on a genuine prospect of commercial success, and perhaps even blockbuster sales.

For example, using a rule of thumb that a commercial stage Pharma is typically valued at ~3-5x annual sales, and assuming the long-term commercial opportunity for EYP-1901 is a "blockbuster" (>$1bn per annum sales) one, we could argue that EyePoint deserves a $3bn - $5bn market cap valuation.

Or, being more conservative and discounting the risk of clinical study failure, lack of funds to complete studies or fund a commercial launch, or losing out to a drug with a superior safety / efficacy profile, we could take the lower valuation of $3bn, and discount it by 75% for a risk-adjusted valuation. We would still get to $750m - nearly 4x higher than EyePoint's current valuation.

As such, at the very least we can say the investment opportunity in relation to EyePoint is an intriguing one, based on the markets in play, and the results of clinical studies conducted to date, which I will discuss in the remainder of this article, along with additional discussion of strengths, weaknesses, opportunities and threats.

EyePoint's EYP-1901 - Development To Date

The progress of EYP-1901 in the clinic so far appears to have been quite promising - according to EyePoint's 10K submission:

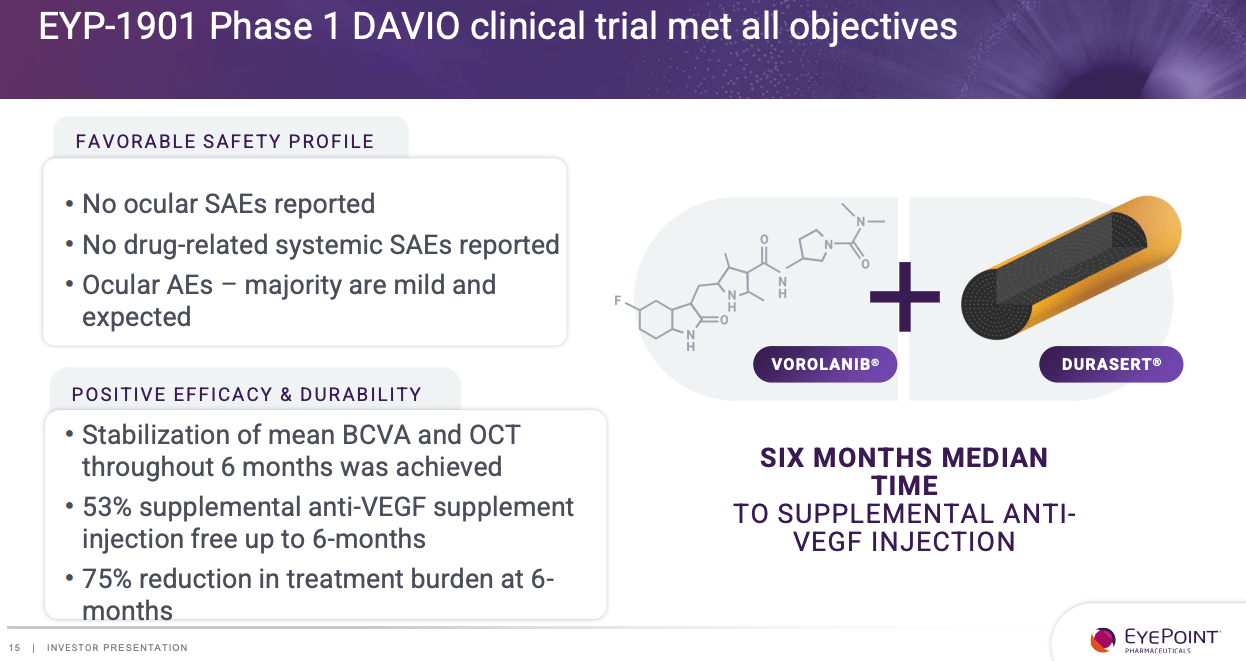

In 2022, we reported positive twelve-month safety and efficacy data in a Phase 1 clinical trial of EYP-1901 (DAVIO), delivering the active drug vorolanib.

Vorolanib acts through intracellular binding of all VEGF receptors thereby blocking all VEGF isoforms. Vorolanib has also demonstrated encouraging neuroprotection data in preclinical in-vivo studies potentially bringing an additional treatment benefit.

Vorolanib has the same target as Eylea and Lucentis - VEGF - although vorolanib is a tyrosine kinase inhibitor ("TKI") as opposed to an anti-VEGF inhibitor, which could mean it can be used as a complementary therapy to these blockbuster drugs.

{kind=link}

The Phase 1 DAVIO study enrolled only 17 patients, using 4 different doses, with safety as the primary endpoint. According to EyePoint, the drug met all of its endpoints, as shown in the slide below:

{kind=link}

Safety is of course paramount, and EYP-1901 seems to have been strong in that area, with no serious adverse events ("SAEs") recorded, and ocular adverse events ("AEs") generally mild and manageable.

The efficacy also looks initially impressive - the median time to a supplemental anti-VEGF injection being 6m, and a 75% reduction in treatment burden observed after 6m. In patients with no "excess fluid" at screening, an 89% reduction in treatment burden was observed after 12m.

There was more good news as EYP-1901 made its case for use in a "treat-to-maintain" treatment paradigm, i.e. a patient's condition could be initially treated with current standard of care - Eylea or Lucentis, for example - with the treatment then "maintained" every 6 months using EYP-1901. Management's conclusion is that:

based on DAVIO outcomes, we believe over half of all wet AMD eyes may be maintained visually and anatomically with EYP-1901 alone.

Phase 2 Studies in Wet AMD and NPRD

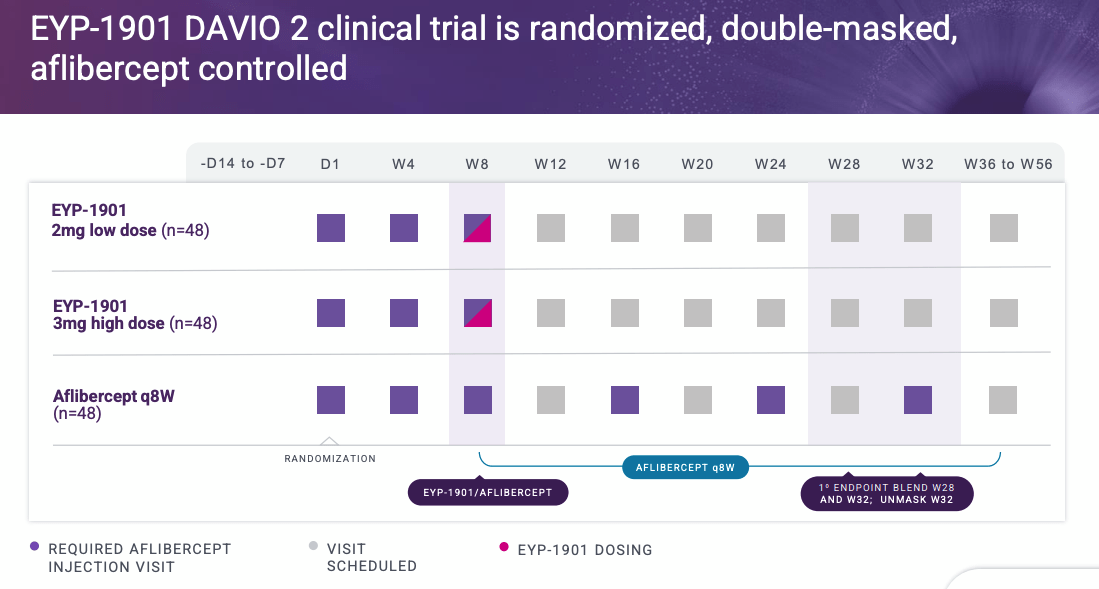

In March this year EyePoint completed its enrollment for its DAVIO 2 study evaluating EYP-1901 as a potential 6-month maintenance treatment for Wet-AMD - according to the company's Q123 10Q submission:

The trial exceeded its original target of 144 patients, enrolling a total of 160 patients. All patients were previously treated with a standard-of-care anti-VEGF therapy and were randomly assigned to one of two doses of EYP-1901 or to an aflibercept on-label control.

{kind=link}

The results of this study certainly ought to be worth waiting for - management informed analysts on its Q123 earnings call that "we remain on track to report top line results in the fourth quarter of this year", adding that:

The primary efficacy endpoint of the DAVIO 2 trial is non-inferiority change in visual acuity to the aflibercept (EYLEA) control as measured by best corrected visual acuity six months after the EYP-1901 injection.

Meanwhile, a Phase 2 study in NPDR - PAVIA 2 - is also underway. According to EyePoint's President and Chief Operating Officer Dr Jay Duker, speaking on the earnings call:

NPDR is a very common eye disease that affects almost 1/3 of diabetic adults over the age of 40 and is projected to impact over 14 million Americans by 2050...

As currently approved intravitreal therapies for NPDR requires significant visit and treatment burden, the vast majority of NPDR patients are merely observed and not treated. This provides a significant market opportunity for EYP-1901, which may be able to be effectively delivered at nine-month or longer intervals in NPDR.

And as a result of the strong proof-of-concept data, we have modified the Phase II PAVIA clinical trial evaluating EYP-1901 to enroll a minimum of 60 patients, which will represent a reduction from the original plan and of 105 patients. This change allows for a shortened time line to NPDR Phase II data and potentially an accelerated initiation of Phase III clinical trials.

It is interesting to note the reduction in trial size, as it seems to me, and similarly to the Wet AMD opportunity, that management appears to be very confident in its drug and its data, and desperate to get to the Phase 3 registrational study stage as quickly as possible, to get the product in front of the FDA and seek approval. In fact, management is also planning a Phase 2 study in diabetic macular edema ("DME"), anther eye disease that currently represents a market opportunity of ~$4bn.

Taking A Step Back & Considering Some Risks

On the face of it, a drug that could be administered every 6 months as opposed to every 6 weeks, without losing its potency would demand consideration as an alternative to current standards of care, and likely be popular with patients and physicians alike. Dr Duker summed up the opportunity on the Q1 '23 earnings call:

We had a significant reduction in treatment burden in DAVIO, the Phase I trial of 75% at six months to 73% at one year. I think if our reduction in treatment burden is in the neighborhood of 50%, that would be an excellent result and anything better than that, obviously, would be even greater result. In talking to practitioners and asking them what type of reduction in treatment burden would be useful to them in practice, they actually will quote a number even less than 50%.

So far so good, but unfortunately for EyePoint, biotech companies do not operate in a vacuum, and in EyePoint's case, its rivals present a formidable obstacle to success.

First of all, it is worth noting that Eylea has been the dominant therapy in wet AMD for around a decade. Frequently, companies have believed they have designed superior drugs that can finally knock Regeneron's drug off its pedestal - Novartis' development of Beovu, for example - only to discover that they had either underestimated the competition, or over-estimated the strength of their own product, or both.

It is hard to imagine a scenario where Regeneron enthusiastically welcomes a drug like EYP-1901 to the market, given that is designed to eliminate the necessity for long-term treatment with Eylea, which would surely seriously impact Eylea's revenue generation. As such, EyePoint's clinical studies will have to show incontestably that it is superior to Eylea and not inferior, because Regeneron will doubtless scrutinise those results thoroughly and be very quick to point out any signs of reduced efficacy, or safety concerns, to the FDA.

And of course, Regeneron is busy working on its own pipeline of next-generation products, with an R&D budget that is astronomical compared to EyePoint's. In Q123, for example, Regeneron earned net income of $818m, and spent ~$600m on SG&A. EyePoint, on the other hand, made a net loss of $21.2m, barely investing in R&D, and reported a cash position of $123m. Arguably, EyePoint management may not be able to raise the funds to sponsor pivotal studies in Wet AMD and NPDR, let alone DME.

Furthermore, Regeneron is far from EyePoint's only rival. Roche's drug development subsidiary Genentech actually recently launched a 6-monthly "port delivery system" of ranibizumab - Lucentis - which it named Suvismo. The drug struggled to take market share away from Eylea post-launch, however, and has now been "taken off the market by Genentech via a voluntary recall", according to EyePoint's 2022 10K.

Suvismo may come back to market and may yet be successful, although the main objection to the drug raised by physicians was that its implant was less safe than Eylea - an issue that may not affect EYP-1901, which has demonstrated a strong safety profile to date. Nevertheless, a host of other Pharma's and biotechs are intent on bringing new and improved ocular disease therapies to market.

EyePoint lists its competition as REGENXBIO ( RGNX ) and Adverum Biotechnologies ( ADVM ) - both are developing gene therapies for Wet-AMD - 12 and 16 week dosing regimen versions of Eylea being developed by Regeneron (2 pivotal trials have met endpoints), Ocular Therapeutix ( OCUL ) phase 1 stage TKI delivered via intravitreal injection, Clearside Biomedical's ( CLSD ) axitinib injectable suspension, Kodiak Sciences anti-VEGF therapy, Opthea's Phase 3 study stage OPT-302 (designed to be used with Eylea), plus 2 candidates from Belgian Pharma Oxurion, and candidates from Oculis ( OCS ) and Unity Biotechnology ( UBX ).

Concluding Thoughts - A Rare Undervalued Gem Or Struggling Biotech Forced To Sell Crown Jewels? I Am (Tentatively) Impressed With EyePoint

Drug development is a hit and miss industry within which even the largest global Pharmaceutical company may have a less than 1-in-5 chance of successfully guiding a pipeline asset from early clinical studies all the way to a successful Phase 3, and an FDA approval. Successful drugs generate so much revenues at such a good profit margin, however, that Pharmas are prepared to keep investing billions upon billions of dollars into discovering (or acquiring) and developing promising drugs.

Looked at in this way, what chance can a ~$200m market cap biotech possibly have with a single asset designed to take market share away from a near double-digit-billion selling asset like Eylea, or a near $3bn per annum selling Lucentis - drugs that are owned by companies with market caps of >$75bn and >$235bn respectively.

I would not be surprised if EyePoint is squashed like a fly by these globally significant Pharmas, but another way of looking at the Pharma industry is that it is a more level playing field than it seems. You can have all the money and staff at your disposal, but you cannot turn a poor drug into a successful one, and since drug "discovery" is a far from perfect science, it is not uncommon for a small biotech to discover and develop a drug product with blockbuster potential.

That helps to explain why Pharma's often pay billions to acquire small biotechs with a single promising drug - in the eye disease space, witness Astellas Pharma's recent $5.9bn buyout of Iveric Bio . The acquisition price was $40 per share, which is 500% higher than Iveric's shares were trading when I first profiled the company and gave it a "BUY" recommendation back in 2022, based on its promising Geographic Atrophy Therapy, Zimura.

My point is that it would not necessarily be right to conclude that because EyePoint is a small biotech with a single drug product, it stands no chance against the mighty Pharma industry incumbents in the field of eye disease. In fact, promising results from DAVIO 2 and PAVIA 2 could even lead to a buyout of the company at a substantial premium to current valuation.

My research - most of which I have shared above - has not uncovered any obvious issues with EYP-1901 as a longer acting therapy for Wet AMD. That does not mean that larger clinical studies won't uncover some, but it does mean that, at present and in my view, EyePoint's opportunity with this product could be worth getting excited about.

I suspect that the DAVIO 2 results due Q4 will have a fundamental effect on EyePoint's share price. If EYP-1901 is unable to show non-inferiority against Eylea, that could be the end of the line for the product, but if it can, Regeneron et al would surely have to acknowledge that less frequent dosing is better, and if I were Roche or Regeneron I would be then be desperate to get a buyout of EyePoint completed before it can gain too much publicity (driving up the valuation) or make it to market.

Positive DAVIO2 data ought to be enough to allow EyePoint to raise funds at a much higher share price than it enjoys today, if management wanted to commercialize the drug themselves.

In summary, based on data to date, target markets, risks, and competition, my conclusion is that the opportunity in front of EyePoint is sufficiently large, and near term, and risk mitigated, to suggest that a market cap valuation of ~$200m is too low for this company. Unfortunately, it could still be the case that later stage data scuppers the investment opportunity and the company sinks without trace, but a risk-on investor may just feel that risk reward profile in play here is a strong one.

For further details see:

EyePoint Pharmaceuticals: A Puncher's Chance For Long Acting Eye Disease Drug Success