EYPT - EyePoint Pharmaceuticals Soaring On Wet AMD Study Results: Durasert Looks Real Deal

2023-12-05 10:30:35 ET

Summary

- EyePoint Pharmaceuticals, Inc. EYP-1901, a potential treatment for wet age-related macular degeneration, showed positive results in a Phase 2 study, meeting primary and secondary endpoints.

- The drug demonstrated non-inferiority to the current standard-of-care treatment, Eylea, with a once every six months dosing regimen.

- EyePoint plans to initiate a Phase 3 study for EYP-1901 in the second half of 2024 and is conducting a $175 million fundraising to support its development.

- The superior durability of EYP-1901 compared to Regeneron's >$9bn p.a. Eylea, or Roche's blockbuster Vabysmo, looks compelling.

- EyePoint is set to complete a dilutive fundraising and thus buying shares today may not be advisable, but long term there may be a further substantial upside opportunity in play.

Investment Overview

Back in May this year, I gave Watertown, Massachusetts based EyePoint Pharmaceuticals, Inc . ( EYPT ) a "buy" recommendation in a post for Seeking Alpha , when the company's stock traded at ~$6 per share.

The recommendation was based on the potential of EyePoint's Durasert E drug delivery technology, and specifically its investigational therapy EYP-1901, described as follows in the company's 2022 annual report / 10K submission:

EYP-1901 is an investigational product and our lead pipeline program deploying a bioerodible Durasert insert of vorolanib, a selective and patented tyrosine kinase inhibitor ("TKI"), that potentially brings a new mechanism of action and treatment paradigm for serious eye diseases beyond existing anti-vascular endothelial growth factor ("VEGF") large molecule therapies.

EYP-1901 aced its Phase 1 DAVIO clinical trial , evaluating it as a potential every six-month treatment for wet age-related macular degeneration, with 12-month data showing no reports of ocular serious adverse safety events ("SAEs"), stable best corrected visual acuity ("BCVA"), and central subfield thickness ("CST") at 12 months, 35% of eyes supplement free up to twelve months versus 53% supplement free up to six months, and positive treatment burden reduction of 74% at twelve months versus 79% at six months.

This was a small study in only 17 patients, however, and despite its success, EyePoint shares had slipped in value to an all-time low value of ~$2.3 per share by March this year. EyePoint initiated a Phase 2 study of EYP-1901 in Wet AMD - DAVIO 2 - which enrolled 160 patients, and the company was able to announce yesterday that the study met all primary and secondary endpoints, sending its stock price soaring by >200%, to >$18 per share - its highest value since January 2020.

Phase 2 Data Suggests EYP-1901 May Warrant Standard-of-Care Status

First let's consider the data - according to EyePoint's press release:

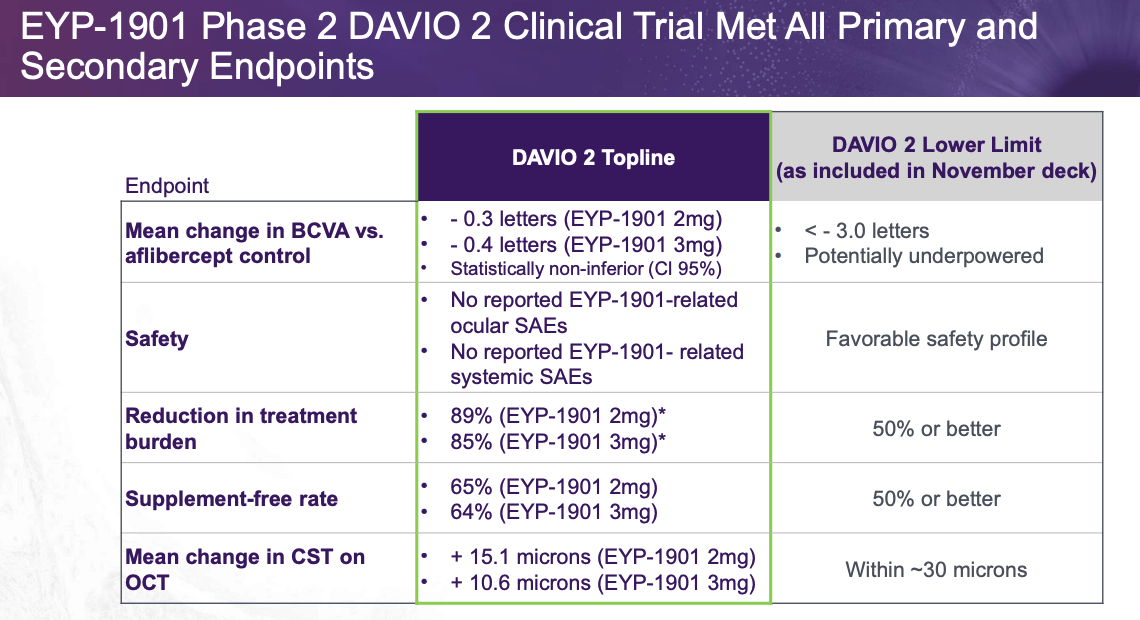

The clinical trial met its primary endpoint with both EYP-1901 doses demonstrating statistical non-inferiority change in best corrected visual acuity ("BCVA") compared to aflibercept control and a favorable safety profile with no EYP-1901-related ocular or systemic serious adverse events ("SAEs").

Aflibercept is an engineered protein designed to attach to and block the effects of a substance called vascular endothelial growth factor A (VEGF-A), which can stimulate the abnormal growth of blood vessels in patients with AMD and other ocular diseases.

It is the active ingredient in Eylea, the current standard-of-care treatment for Wet AMD, marketed and sold by the Pharma giant Regeneron ( REGN ) and partner Bayer ( BAYZF ), earning revenues of $7.8bn, $9.2bn, and $9.7bn in 2020, 2021, and 2022, respectively. While Eylea requires bimonthly injections, however, the DAVIO-2 study shows that a single injection of EYP-1901 every six months may be just as effective for patients.

Specifically, the DAVIO 2 study showed:

Statistical non-inferiority in change in BCVA (at a confidence interval of 95%) compared to aflibercept control, at weeks 28 and weeks 32 combined. The 2mg and 3mg doses were only -0.3 and -0.4 letters different, respectively, versus on-label aflibercept. The lower limit of the non-inferiority margin is defined as a -4.5 letters by the FDA with 5 letters representing one line on the eye chart.

The safety profile remained strong, with no drug related ocular or systemic SAEs, and the 2mg and 3mg doses achieved an 89% and 85% reduction in treatment burden, respectively, with 65% and 64% respectively supplement free up to 6 months.

{kind=link}

In summary, as illustrated above in a slide from EyePoint's data presentation , it seems the DAVIO-2 study could not have gone much better. Study investigator Carl Regillo, M.D., Chief of Retina Service at Wills Eye Hospital, was quoted in the press release as follows:

I am very encouraged by the data generated from both the Phase 1 DAVIO and Phase 2 DAVIO 2 trials with the latter showing essentially no difference in visual outcome at the blended six-month endpoint from a single injection of EYP-1901 compared to on-label, bimonthly aflibercept injections. Based on the meaningful reduction in treatment burden and supplement-free rates observed, along with the consistently favorable safety profile, I believe that EYP-1901 could be a paradigm shift in how patients with wet AMD are treated.”

Looking Ahead - Phase 3 EYP-1901 Study & Fundraising

Before EyePoint can consider pushing for approval of EYP-1901 the company will need to negotiate a Phase 3 clinical study to reinforce the data from Davio-2, but the good news is, according to Jay S. Duker, M.D., President and Chief Executive Officer of EyePoint Pharmaceuticals:

Since EYP-1901 achieved statistical non-inferiority to the aflibercept control in this trial there is potential for meaningfully lower sized and lower cost pivotal Phase 3 trials. The DAVIO 2 clinical trial was designed to support the initiation of Phase 3 clinical trials based on feedback received from the U.S. Food and Drug Administration ("FDA") at a Type C meeting last year. The 32-week topline DAVIO 2 data strongly supports our planned Phase 3 non-inferiority design, consistent with the FDA’s recent guidance for wet AMD clinical trials.

EyePoint says it plans to initiate "our first pivotal trial for wet AMD in the second half of 2024," and, as is more or less standard for any biotech after a successful study data readout, the company has announced plans for an underwritten public offering of $175m of shares of its common stock. The higher the price at which EyePoint can complete this offering, the less diluted existing shareholders will be.

Announcing Q3 earnings , EyePoint revealed a cash position of $133m, and a net loss for the quarter of $(14.3m), and $(58.7m) across the first 9 months of 2023. Back in May, EyePoint sold its lead commercial asset, YUTIQ, a treatment for chronic non-infectious uveitis affecting the posterior segment of the eye, to Alimera Sciences for $82.5m plus a low to mid double-digit royalty on future sales, in order to fund its studies of EYP-1901, and a second, earlier stage asset, EYP-2301.

Understanding Eye Disease Markets, Market Opportunity For EyePoint

Having shown itself to be non-inferior to standard-of-care Eylea with a 6 month injection, we might draw the conclusion that EYP-1901 is a nailed on "blockbuster" drug, i.e., one capable of >$1bn revenues per annum, but it is not quite as straightforward as that.

In August, the FDA approved a higher dose version of Eylea, at the second time of asking, as manufacturing issues identified by the agency saw it reject Regeneron's original application in June. According to a Regeneron press release :

The recommended dose for EYLEA HD is 8 mg (0.07 mL of 114.3 mg/mL solution) every 4 weeks (monthly) for the first 3 months across all indications, followed by 8 mg every 8 to 16 weeks (2 to 4 months) in wAMD and DME and every 8 to 12 weeks (2 to 3 months) for DR.

Regeneron was able to show non-inferiority to EYLEA 2mg injections in 2 studies, PULSAR and PHOTON, with a less frequent dosing regime, and although EyePoint's EYP-1901 still seems to be a clear winner in terms of dosing frequency, Eylea's established position as standard of care and Regeneron's vastly superior sales and marketing infrastructure will likely make it very challenging for EyePoint to gain a foothold in the market, should its drug and delivery mechanism be approved. Plus, there are other concerns.

Eylea achieved revenues of $1.49bn in Q3, with a $43m contribution from newly approved Eylea HD (high dose), but the drug's revenues were down 11% year-on-year, which management put down to "lower net selling price driven by changing market dynamics, including increased competition."

A new therapy from Swiss Pharma giant Roche ( RHHBY ), Vabysmo, approved by the FDA in January 2022, has been eating into Eylea's market share, earning revenues of >$1bn across the first half of 2023. After an initial four doses administered once every four weeks, patients are examined, and can move to either a once every 8, 12, or 16 week dosing regime n. Again, not as impressive as once every 6 months, but another significant competitor for EyePoint to contend with in a commercial setting.

Furthermore, with Eylea patents expiring, biosimilar versions of the drug will soon hit the market, putting downward pressure on pricing and making the overall wet-AMD less lucrative. High dose Eylea has a price point of ~$2,600 per vial, Eylea ~$1,850, and Vabysmo ~$2,200.

Some analysts have also expressed the opinion that EyePoint's study was "stacked for success," and that much of the benefit observed was down to prior use of Wet AMD therapies by patients, rather than EYP-1901 itself. One analyst at RBC Capital markets wrote in a note to investors that "we do not see 1901 as being nearly as important a threat as Roche, biosimilar Eylea, and the Inflation Reduction Act."

Concluding Thoughts - Davio-2 Results Stun Market, But Challenges Remain - Long-Term Upside Likely, But Not Guaranteed

How to interpret EyePoint's data with regard to the company's valuation, today and going forward?

My take would be that EYP-1901 may be the real deal - drug delivery is a hugely significant, yet often overlooked aspect of medicine, and how effectively a particular drug may work. With its Durasert technology, EyePoint appears to have a genuinely breakthrough product on its hands, that allows for administration via a routine in-office intravitreal injection, much less frequently than any other product on the market today.

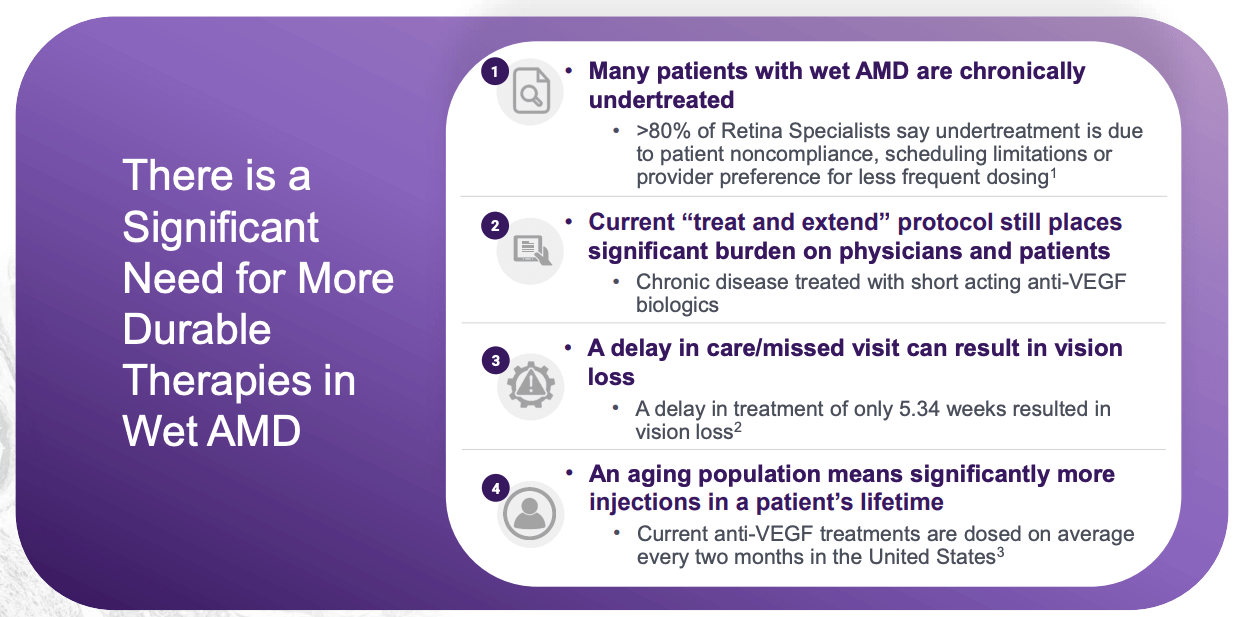

While some analysts may be critical of the DAVIO-2 study results, the once every 6-month dosing regimen for a Wet AMD therapy does seem to be vastly superior to any other product currently on the market, and even with Eylea revenues falling and the market becoming more competitive, it seems hard to argue that there is not a significant revenue opportunity in front of EyePoint, as management itself argues in a slide from the data presentation:

{kind=link}

If anything, an aging population is increasing the prevalence of Wet AMD - in my May note I quoted from EyePoint's 2022 annual report / 10K submission as follows:

As the proportion of people in the U.S. age 65 and older grows larger, more people are developing age-related diseases such as AMD. From 2000-2010, the number of people with AMD grew 18 percent, from 1.75 million to 2.07 million. By 2050, the estimated number of people with AMD is expected to more than double from 2.07 million to 5.44 million.

EyePoint has a composition of matter patent which extends into 2037 for vorolanib, it has outstanding clinical data both from its Phase and 2 studies that I would argue is difficult to put down solely to therapies used by patients beforehand, and it has agreement with the FDA over Phase 3 study protocols that could lead to a rapid completion of a pivotal study and a push for approval as early as 2025, perhaps. EyePoint management says its current funding runway will extend into 2025, and will likely soon complete a $175m fundraising.

The company may well attract some M&A interest - perhaps from the likes of Roche, Regeneron, or Astellas Pharma, which, as I pointed out in my last note, paid $5.9bn to acquire Iveric Bio and its geographic atrophy candidate Zimura, now approved as Izervay, or $40 per share - a 500% premium to the company's share price when I tipped it for success in a Seeking Alpha note in 2020.

Eye disease markets are highly lucrative and likely to remain so, and EyePoint certainly seems to be in possession of a very valuable asset, which is also in studies in non-proliferative diabetic retinopathy ("NPDR"), with Phase 2 data due in Q224, and diabetic macular edema, while EYP-2301, a TIE-2 agonist, is being developed for serious retinal diseases.

There are some risks that investors should carefully consider however - while vorolanib is patent protected, could a rival pharma copy the Durasert delivery approach? Does EyePoint have the finances or commercial acumen to compete in eye disease markets against vastly better resourced rivals? Will patients and physicians necessarily be won over by the lengthier dosing regimen - perhaps they will prefer to stick with tried and trusted methods? Will a Phase 3 study uncover issues with efficacy, formerly masked by the fact patients had been using other therapies long term?

All of these issues threaten the success of EyePoint, Durasert, and EYP-1901, and therefore threaten the company valuation. It's important to remember that less than 9 months ago, EyePoint stock traded <$3 per share. If the EYP-1901 push for approval is derailed for any reason, the share price will rapidly plunge back to a similar level.

Despite all of these risks, I suspect there is further upside for EyePoint stock to realize, because in my view, the "multi-billion" opportunity that management discusses in its presentations and earnings calls appears to be a genuine one, and a tangible one.

At this stage, however, I would give EyePoint stock a "Hold" recommendation. I expect that the dilutive upcoming fundraising will affect the share price negatively in the short term, plus there is the fact that biotech stocks often drift downward in value when the next major data catalyst is some way away, and in EyePoint's case, that will be Phase 3 data for EYP-1901 in Wet AMD that will not arrive until the end of next year, at the earliest, or possibly the NPDR data due in the middle of next year.

As such, there is no obvious compelling need to buy EyePoint Pharmaceuticals, Inc. stock today, but biotech investors may want to add it to their watchlists, as a ~$650m market cap valuation is very low for a company eyeing a market that is worth ~$10bn, in Wet AMD alone, with a product displaying durability that no other company - not even Roche or Regeneron - appears to be able to match.

For further details see:

EyePoint Pharmaceuticals Soaring On Wet AMD Study Results: Durasert Looks Real Deal