EZA - EZA: South African Stocks Offer High Returns But Remain Risky (Rating Upgrade)

2023-05-15 07:05:01 ET

Summary

- EZA invests in South African stocks.

- The fund seems to offer a very compelling return profile, even adjusted for historical realized volatility.

- However, local risks remain, and investor sentiment is not yet supporting the fund.

- I think EZA is absolutely worth monitoring, but it may not yet be the time to buy into the fund. Having said that, long-term investors will probably do well at present prices.

Introduction

iShares MSCI South Africa ETF ( EZA ) is an exchange-traded fund that invests in South African stocks. My last article covering EZA was published in March 2021 , at which point I believed the fund was overvalued. The fund's significant indirect exposure to Tencent (OTCPK: TCEHY ) also made the fund attractive to me. Since then, EZA has fallen -20.43% vs. the S&P 500's change of +4.59%. However, much time has passed since then, so it is perhaps worth revisiting EZA to see if there is any opportunity at present price levels.

EZA had assets under management of $326 million as of May 12, 2023, with an expense ratio of 0.58% and a 30-day median bid/ask spread reported by iShares of 0.18%. A bid/ask of 0.18% is actually quite large, it indicates some noteworthy degree of illiquidity. However, EZA is also a volatile fund, and so this kind of spread can be justified if there is enough opportunity. I calculate the fund's three-year beta as being 1.29x, with 0.64x correlation to the S&P 500. So, there is the potential for somewhat uncorrelated returns, as well. Having said that, the three-year correlation with the U.S. on a downside-only basis is higher at 0.76x; in a risk-off environment, you can expect EZA to fall harder than U.S. stocks.

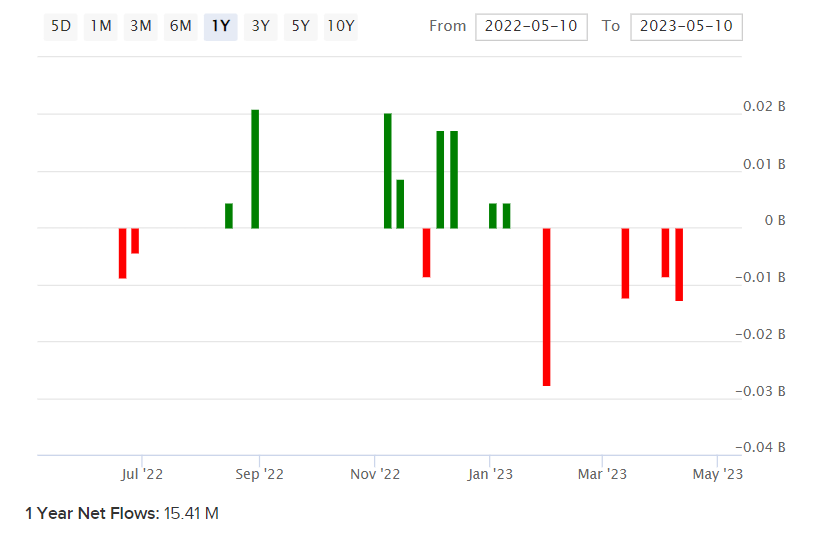

EZA's net fund flows are positive on a twelve-month trailing basis, as pictured below, but only by about $15 million.

{kind=link}

As you can see, net fund flows have been mostly negative most recently. I also saw South Africa in the headlines recently having supplied arms to Russia in a clandestine manner, although claims were denied by the country's President Cyril Ramaphosa's office.

I should note before proceeding that South Africa in general is not considered to be a politically stable country, although this has been subject to much debate in recent years. The country is a relatively young democracy primarily governed by the African National Congress. While perhaps outwardly stable, there are social divisions within the country owing to historical legacies and post-apartheid governance failures. While South Africa remains a relatively stable democracy, the country maintains high societal inequalities, and I have often seen South Africa being used as a kind of archetype for a high Gini coefficient . The unemployment rate is also still very high at 32.7% as of 2022 Q4. Professor Damodaran has previously assigned a country risk premium to South Africa of 5.19%, which I will consider in my analysis.

The country's core inflation is high, but not especially high in relation to the rest of the world at the moment who are also experiencing persistent inflationary pressures. Core inflation in the country was 5.2% year-over-year in March 2023 . However, the country's risk-free rates are high; the local 10-year yield is 10.94% at the time of writing. This means that local equities must offer very high nominal returns in order to compete with local "risk-free" rates.

Return Profile

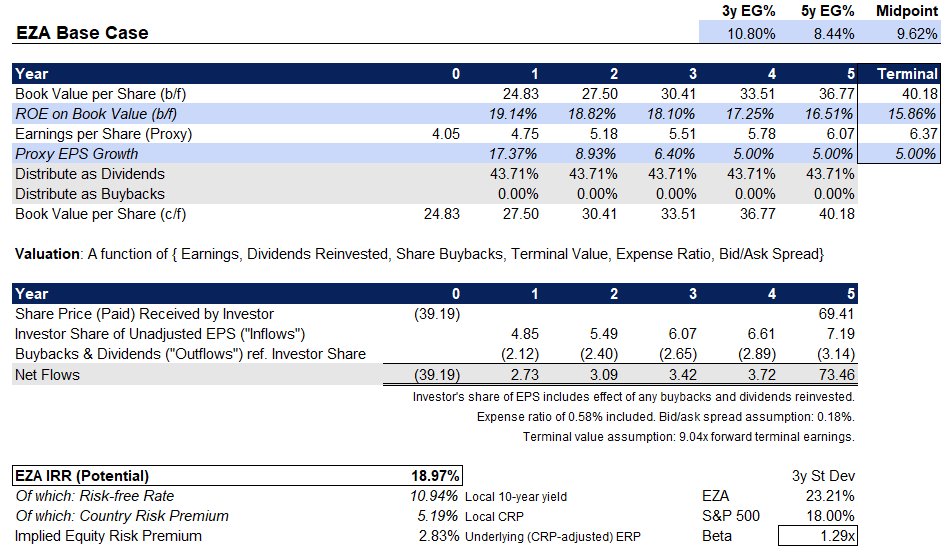

I can attempt to gauge the value of EZA by reviewing the most recent factsheet for the fund's benchmark, the MSCI South Africa 25/50 Index, as a proxy for EZA's portfolio. According to the index, the trailing and forward price/earnings ratios were 10.61x and 9.04x, as of April 28, 2023, with a price/book ratio of 1.73x and an indicative dividend yield of 4.12%. Based on this data we can say that the forward return on equity is 19.14%, with a dividend distribution rate from earnings of 43.71% and a one-year forward earnings growth rate expected of 17.37%.

Separately, Morningstar expect 10.23% earnings growth on average over three to five years. If I assume 9.62% on average, this sets the earnings growth to a floor of about 5% by year four in my projection. The return on equity implied falls to about 16% by my terminal year. If inflation were to hold at 5%, this would reflect zero 'real' earnings growth. Holding most other factors constant then, my analysis overall suggests a forward IRR of just under 19% per annum. While high, that would suggest a very thin underlying equity risk premium after accounting for the high country risk premium of 5.19%.

{kind=link}

However, in this case, I would suggest summing the CRP and underlying ERP to get a net ERP of 8.03%. If we then divide that by the fund's beta of 1.29x from a U.S. investor's perspective, we get a beta-adjusted ERP of 6.22%. That is actually quite close to the fair range for mature markets of about 3.2-5.5%. It would suggest that, all considered, EZA is probably undervalued. The high nominal return of 19% does however need to take into account the high local risk-free rate of 10.94%.

FX Considerations

It is worth noting that high risk-free rates suggest the potential for FX carry trades and thus a stronger local currency. However, there are many factors at play here. These factors are relevant as EZA's holdings are ultimately denominated in South African rand (abbreviated: ZAR).

Since my last article on EZA, in which I thought ZAR looked undervalued, the U.S. dollar has in fact appreciated by over a third relative to ZAR. Once again, it would seem like there is plenty of potential (far more, now) for local FX appreciation. However, weak confidence in the country is a warning sign. The country has suffered power cuts (ongoing), poor investor risk sentiment, stronger U.S. rates (i.e., the USD as a competitor), and lower commodity prices (ZAR is viewed as a quasi commodity currency). Meanwhile, the country's current account is in deficit, which is usually a sign of over-valuation.

That said, I would not feel too much anxiety over the South African rand's future, as the currency is already objectively weak. I would however suggest that EZA is likely to remain volatile and a high country risk premium is deserved.

Final Note

EZA's largest holding was Naspers Limited ( NPSNY ) at 16.83% as of May 12, 2023. The company still owns a large stake in Tencent indirectly through its ownership of Prosus ( PROSY ). Prosus was listed in 2019. Naspers owns 56.92% of Prosus, which in turn owns 26.9% in Tencent most recently after having pared its holding from over 30%. Bizarrely, Prosus owns 49% of Naspers itself in a complicated cross-shareholding structure. In any event, it is good that EZA's indirect exposure to Tencent has fallen and should continue to fall over time as Prosus sells off Tencent stock. EZA does not own Prosus, only Naspers. You could argue EZA's exposure to Tencent, a Chinese multinational tech company, is now about 2.6%. Therefore, EZA's portfolio is now looking a little cleaner than before.

Meanwhile, EZA's weighted sector exposures are generally emphasizing financial services (30.49%), basic materials (27.01%), and communication services (24.75% -- this includes Naspers 17.35% as of Morningstar's reference date of May 11, 2023; see below).

Morningstar.com

Therefore, EZA is also likely to act as a higher-beta instrument during cyclical upswings. As we move into a new business cycle, you could have a perfect (favorable) storm of higher commodity prices, a stronger ZAR, stronger equity risk sentiment, and cyclical/sensitive stocks (such as the kind that EZA is exposed to) all rallying in tandem. That makes EZA's IRR potential of almost 20% per annum quite compelling.

However, with core inflation still running high in the West, let alone South Africa, I would suggest caution at present. Investor sentiment is still very weak, with EZA falling -10% year-to-date while U.S. stocks have rallied almost 8% (per the S&P 500 index). EZA looks potentially very attractive if timed correctly. I think EZA is therefore worth monitoring, but not worth buying at this precise point in time.

For further details see:

EZA: South African Stocks Offer High Returns But Remain Risky (Rating Upgrade)