LNC - F&G Annuities: Huge Insider Buying Bargain Priced At 5.8x Earnings 3.8% Yield

Summary

- Fidelity National Financial spun out 15% of their stake in F&G Annuities on December 1st.

- F&G earnings crushed Q4 estimates, as this business is benefiting from higher interest rates.

- F&G trades at only 5.8x forward 2023 earnings.

- With the company guiding to double-digit sales (and likely EPS) growth, we view fair value as 20-50% higher potentially in 1-2 years.

- We like collecting the 3.8% dividend while we wait for the market to improve.

We are fans of Fidelity National Financial ( FNF ), a long-term Compounder with a remarkable track record of generating well above market returns (especially from M&A activity followed by spinoffs). On December 1 st last year, FNF spun off 15% of their stake in F&G Annuities (FG), with the stock roughly flat since then. Given huge insider buying at F&G (almost $2 million by the CEO in December), a super cheap valuation at 5.8x forward earnings and expected double-digit sales and EPS growth, FG stock looks like a solid buy today.

We target 20-50%+ upside in the shares in 1-2 years.

F&G Annuities Results

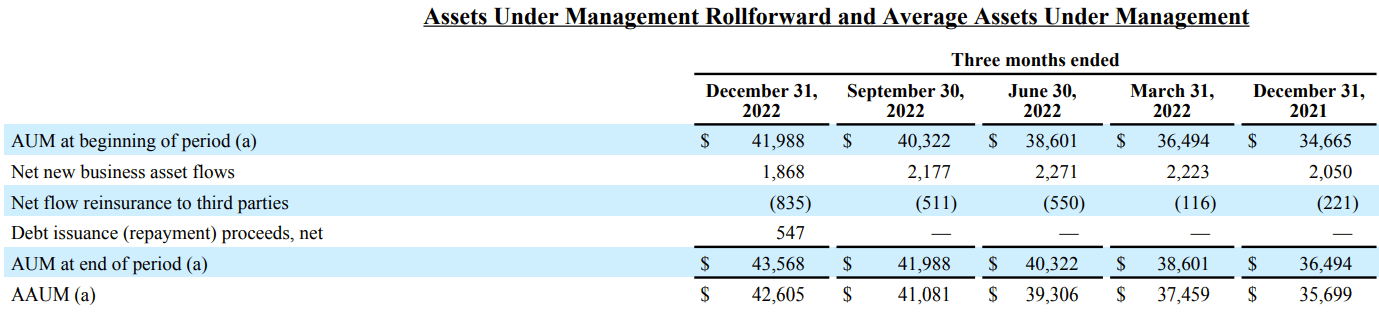

Since the acquisition of F&G by FNF in June 2020, we have been quite impressed with CEO Chris Blunt. For the fourth quarter, F&G reported terrific results. Gross sales were up 23% in Q4 and up 18% for the full year. Ending assets under management [AUM] grew to almost $44 billion at year end, up 19% year over year. That is up from $25 billion in mid-2020 when F&G was acquired by FNF.

Average Assets Under Management (Company financials)

Here are fund flows by quarter, averaging around $2 billion.

{kind=link}

Note: The chart above is average assets under management in the reported quarter. The above table illustrates both assets under management at period end and average figures. These non-GAAP measures include accrued interest income and other items which may not be reflected exactly on the balance sheet.

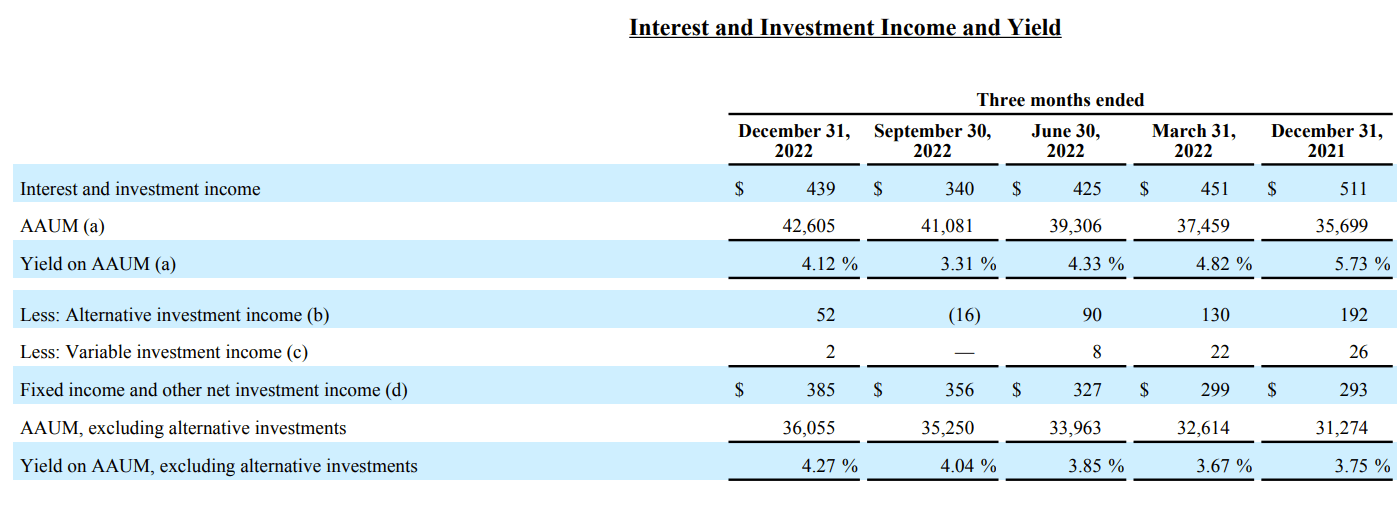

With these fund flows and AUM growth (averaging 15% in the past 2 calendar years), F&G looks like a growth stock trading at what is clearly a non-growth multiple. While fund flows will likely moderate a bit from the most recent growth figures, there is margin upside should the Fed continue raising rates. Yields on their investment portfolio rose steadily last year.

{kind=link}

Due to new accounting rules (again), F&G must report adjusted EPS including all the noisy gains and losses inherent in mark to market accounting. To get a sense for recurring EPS, we simply took those MTM movements out of earnings and added back the long-term assumption on returns (this all relates to their alternative investment portfolios).

Here is our math with Q4 unchanged but 2022 earnings better than reported adjusted EPS of $3.00 by 40c.

Author spreadsheet, company financials

The above assumes 10% returns in their alternative investment portfolio, which is seemingly high and a risk in the future. But historically this book has earned 12% returns, so we see upside as well (note the recognized gains in the past 2 years above). The portfolios at F&G seem well managed as do their reserves.

While reported adjusted EPS was $3.00 last year, adding back some losses and normalizing returns implies $3.40 of economic EPS , up 43% year over year.

In 2023, the company expects double-digit growth in total sales. New sales channels have been extremely value additive.

Gross Sales (FG Investor relations)

Street EPS estimates are $3.66 for F&G for 2023. Run rate earnings look to be well over $4.00 (but could be impacted by any number of moving parts like surrender rates, claims experience, investment returns, sales, etc.). We would not be surprised to see estimates move higher but confess that this one is extremely tough to model.

Big picture too, the company does a bit better than 1% ROAs, which on $46 billion of average AUM next year, implies $3.68 in EPS in 2023 (explaining Street estimates).

At 1.1% ROAs and $47 billion of AUM then EPS looks closer to $4.14.

F&G EPS potential (Author spreadsheet)

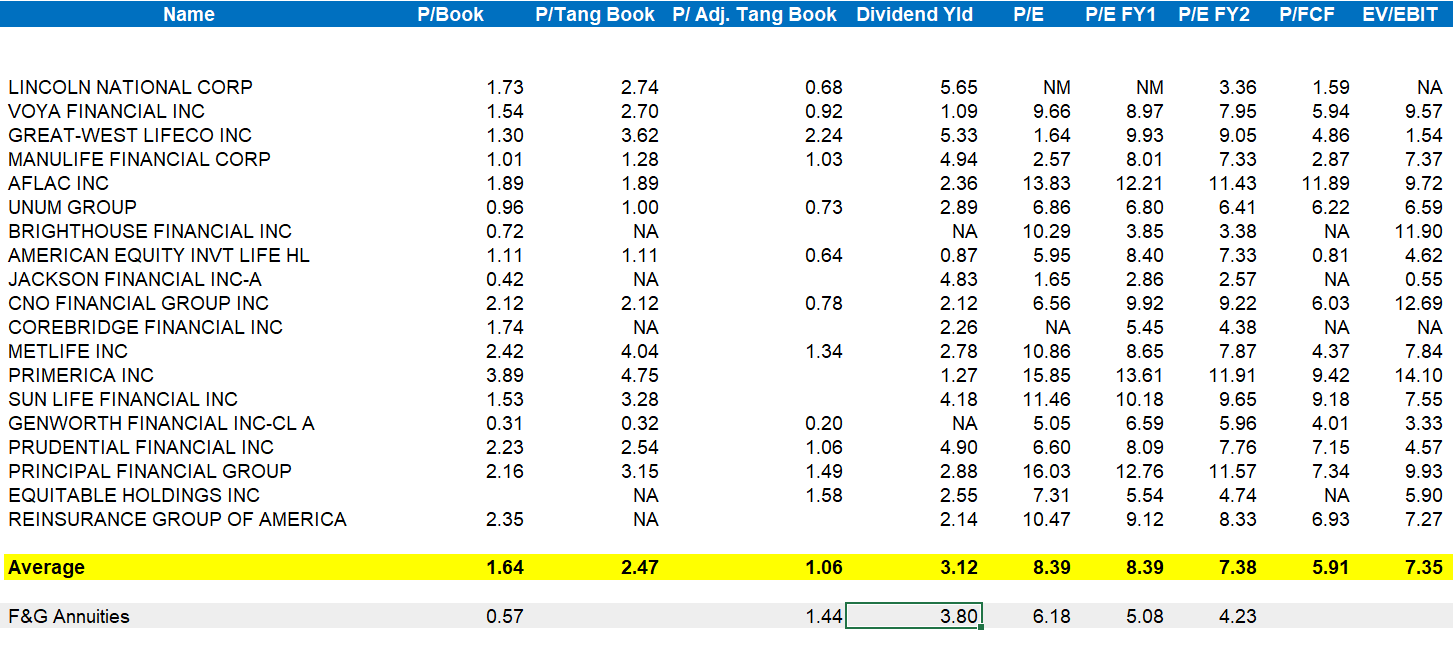

At 6-9x typical annuity business earnings multiples, we get valuations between $24 to $36 in potential upside for the stock (using a rough $4 in EPS). Note that insurance comps on average are trading at over 8x 2023 earnings.

As mentioned, F&G benefits from higher rates, and in the “higher for longer” rates scenario, will mean the company should continue to book higher yields on their $39 billion fixed income portfolio (which is 95% investment grade).

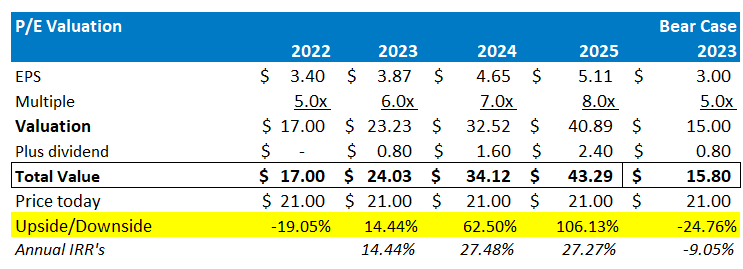

P/E Valuation (Author spreadsheet)

{kind=link}

As for the balance sheet, statutory capital was solid with an RBC ratio of 440% (well above 250% requirements and the company’s target of 400%). Debt to cap adjusted for AOCI was 19% at year end. Moody’s and AM Best have F&G on positive watch.

Chris Blunt purchased a lot of stock below $20, where we have been interested buyers. Given performance, $21 looks like a solid entry point today.

This name seems like a no brainer keeper/buy compared to peer Lincoln National ( LNC ) whose management, in our view, did not accurately represent reserve adequacy last year. LNC continues to struggle with a weak balance sheet and lingering lapse rate problems. That stock trades at 8.2x run rate earnings today.

Below is a more complete list of peers and how they trade compared to F&G.

Comp Trading Multiples (Bloomberg)

{kind=link}

Conclusion

In 2025, we anticipate a tax free spin off of F&G. Given its performance, we see strong odds that a divested, more liquid and performing F&G should trade at the high end of its peer group.

Longer term, F&G targets over 1% in net income for every $1 billion in assets under management (1% ROA's). Last year they exceeded that by a smidge. In 2-3 years, with continued double digit AUM growth, F&G could easily be at $55-60 billion assets under management. That implies over $5 in EPS.

At just 6x earnings we see optionality for the stock earning 50%+ type returns.

For those that own FNF, FG is a nice offset to FNF’s exposure to higher rates (as mortgage activity slows).

For further details see:

F&G Annuities: Huge Insider Buying, Bargain Priced At 5.8x Earnings, 3.8% Yield