FG - F&G Annuities & Life: Further Upside But Its Investment Portfolio Bears Watching

2023-11-10 23:54:09 ET

Summary

- F&G Annuities has seen significant gains this year and reported a strong quarter, leading to increased share buybacks and dividends.

- The company's earnings per share and revenue have improved, with assets under management rising over 15%.

- F&G has been diversifying its product mix and trades closer to book value compared to other annuities providers.

- It does take more risk in its investment portfolio with a large CLO allocation, but earnings should sustain at about $4.

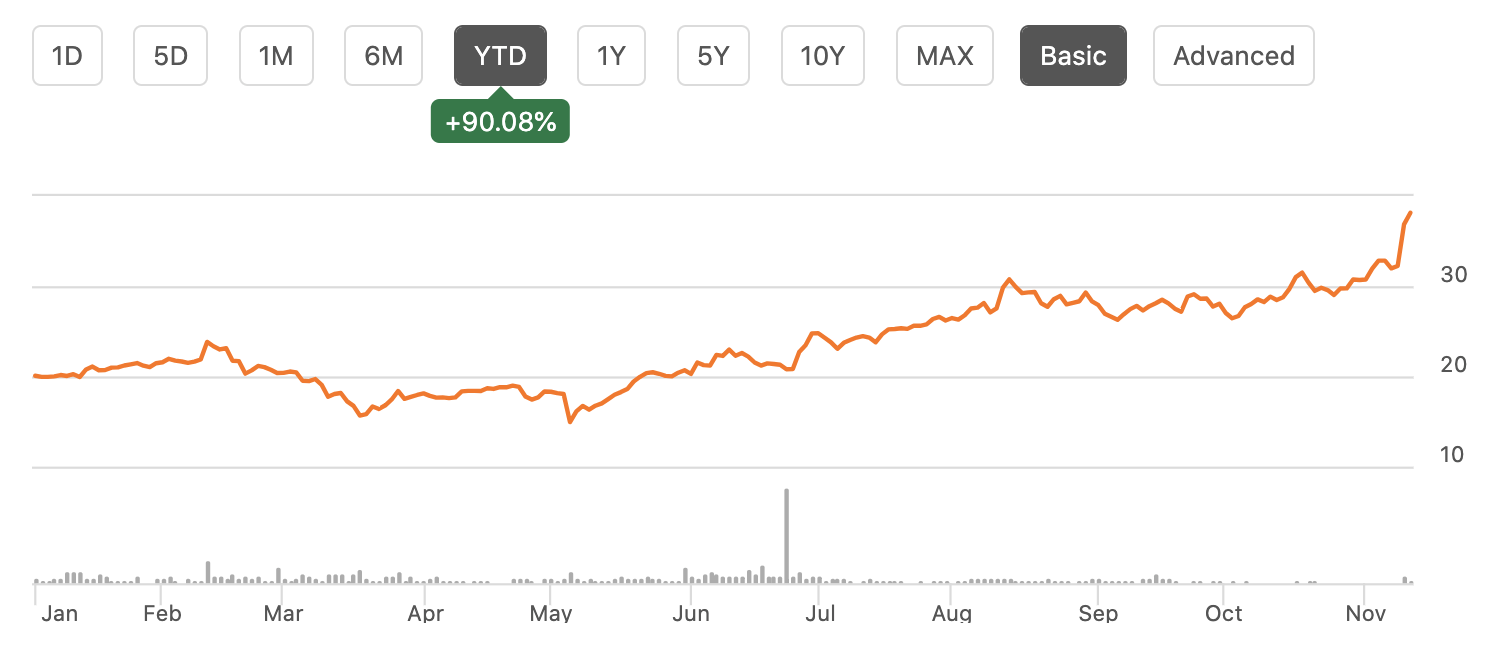

Shares of F&G Annuities & Life ( FG ) have been a tremendous performer this year, nearly doubling, and those gains accelerated this week after the company reported a strong quarter. Alongside results, FG also increased its share buyback program by $25 million and increased its dividend 5% to $0.21. While the company is performing well, after a run like this, we have to ask whether there is any upside left or if all of the good news is priced in.

{kind=link}

In the company’s third quarter , it earned $0.96 in adjusted EPS on revenue of $2.78 billion, up from a $0.01 loss last year. Alternative investments underperformed relative to long-term expectations by $28 million or $0.22/share, meaning adjusted normalized earnings would have been $1.18. These returns can be volatile quarter to quarter. The company is on track to earn over $4.20 this year, having generated a 10.5% return on equity ((ROE)) so far. Thanks to markets and strong sales, its assets under management ((AUM)) have risen over 15% to $45.5 billion.

F&G sells annuities, and with higher rates, these products have been in demand with the company’s net sales up 2.5% to $2.3 billion last quarter. Importantly, it has been diversifying its product mix. Fixed index annuities accounts for 39% of gross sales this year from 77% in 2020 with multiyear guaranteed annuities (often called fixed annuities) up to 37%, and pension risk transfers at 13%. Relative to more well-known publicly traded annuities providers, Brighthouse ( BHF ) and Jackson Financial (JXN), F&G actually trades much closer to its book value. It has a per share book value excluding accumulated other comprehensive income of $43.30, so it trades at .88x book value.

This is because it does not have variable annuity exposure; these are complicated insurance products sold in high-volume before the financial crisis that often generated poor returns for insurers. They have since been simplified, but they still require complex derivative hedging to minimize market risk.

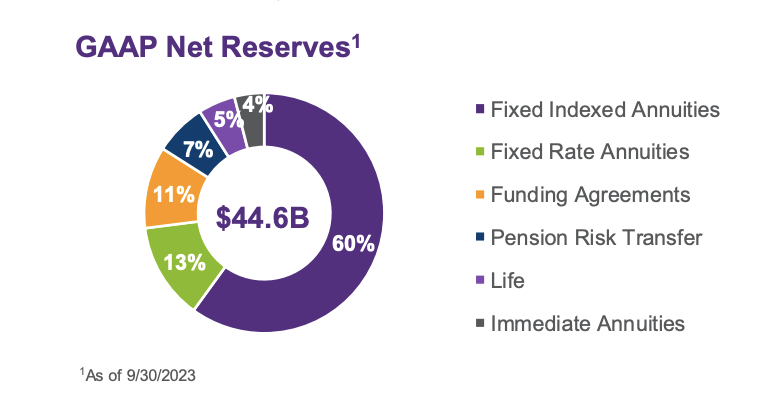

F&G’s two primary products are much simpler. Fixed index annuities are pegged to a market, like the S&P 500, or a blended 60/40 index for instance, offering a share of the upside, with downside protection. Fixed annuities pay a guaranteed return based on interest rates; i.e. it pays out 4.5% like the 10 year treasury, and F&G invests in bonds of a similar duration to earn a spread over this payout. These two products account for 73% of its insurance reserves, and while fixed index is by far the largest, the mix shift is slowly diversifying.

{kind=link}

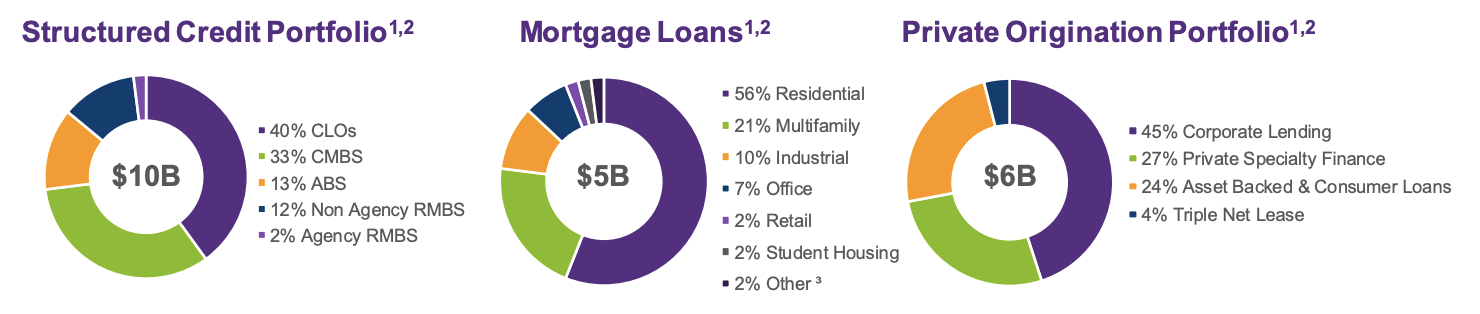

F&G essentially sells less complex annuities, and it instead runs a more aggressive investment portfolio with Blackstone ( BX ) in order to earn a return. Its portfolio has a yield of 515bp while its cost of funds (what its annuities pay) is 273bp. After paying 123bp of operating expense, it has generated a 119bp return on assets this year. Now, the portfolio is performing quite well with just 2bps of credit impairment in the quarter and 5bps loss rate over the past three years. Moreover, 96% of its fixed income portfolio is investment grade. Relative to other insurers, F&G invests relatively little in corporate securities, at 29%, and it has a significant 24% in structured securities.

{kind=link}

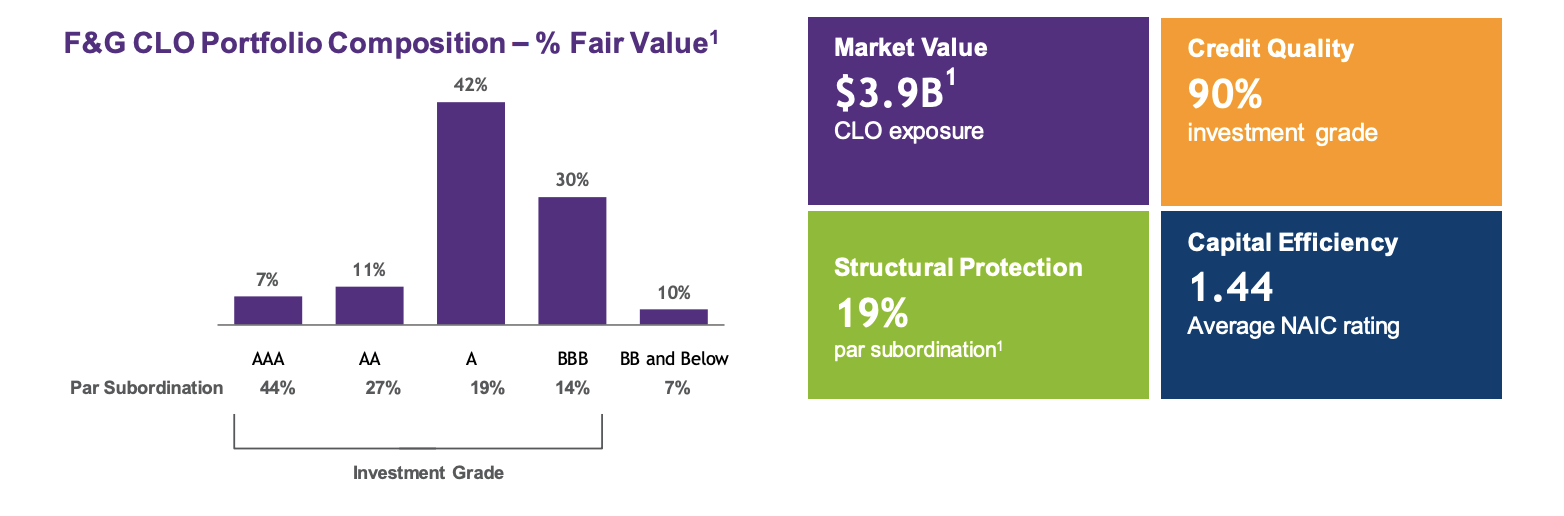

In particular, I would note that F&G has $3.9 billion in CLOs, “collateralized loan obligations.” These are complex securities that are very capital efficient because they are highly-rated by the credit agencies while trading at higher yields, on average, than similarly-rated corporate bonds as they are less liquid.

Rather than lending to a single company, like Verizon (VZ), a CLO is a special vehicle that will lend to dozens of smaller, riskier companies. Each individual company is typically “junk” not investment grade. Because there are many loans, the underlying pool should be fairly diverse. As companies pay off their loan, the CLO is paid off with the proceeds.

However, adding further complexity, the CLO does not pay all of its investors back together; the CLO is made of tranches, senior to each other. So if the underlying portfolio has losses, the least-senior tranche bears the losses first, and it goes up the ladder. As a consequence, the most senior tranche is typically rated “AAA” (i.e. “risk free”) and offers the lowest yield. Below, you can see how F&G’s portfolio is structured.

{kind=link}

It primarily investments in the “A” tranche, which has 19% subordination. In other words, there would need to be more than 19% lost on the underlying loan portfolio for that debt to take a loss at all. For comparison purposes, a company like The Home Depot ( HD ) has an “A” credit rating. HD is stronger than any of the individual companies the CLO lends money to, but the belief is that due to the diversification of the portfolio and the subordination beneath the A tranche, that the underlying credit risk is comparable. Additionally, most CLOs are less than $1 billion, with each tranche a fraction of that total, which makes their debt relatively illiquid and harder to trade. F&G aims to hold to maturity, allowing it to withstand mark-to-market noise.

Historically, CLOs have performed well; in the financial crisis, while securitized mortgage products failed en masse, contributing to the great recession, most CLOs did not, which is why the asset class has persisted. I am not saying that F&G is doing anything wrong; I am just emphasizing it has a complex investment portfolio, enabling it to return a wider spread relative to its average credit rating. In a significant economic downturn, markets are likely to fear it will have greater credit losses than peers, even if it does not end up having those losses.

On the positive side, only 2.3% of its commercial real estate portfolio is in office, which is an area where I fear there could be larger losses, given secular challenges. Moreover, its debt to capital is just 22% vs its 25% target. While F&G runs a more aggressive investment portfolio, it offsets this with a reasonably conservative balance sheet.

Because the economy is doing fairly well, there are not many corporate defaults, which is why F&G’s credit losses are running as low as they are. I would argue that the company is “over-earning” on credit at the moment, and that there will be some uptick here. In Q3, F&G took $6 million in provisions for credit loss. If we assume the environment got 5x worse to have a credit loss rate of 10bps, that would add $24 million per quarter in credit costs or $0.15/share.

That still leaves over $1 in quarterly earnings power, or $4 annualized. I view this as a more sustainable earnings level than the ~$4.72 annualized last quarter. Even then, shares are just 9.5x, for a company that is growing. Balancing out the fact its policies are less complex with the fact that its investment portfolio is more complex, I view book value as fair value for the business. That does still provide about 13% upside from here and would leave the stock with an 11x earnings multiple.

I would caution that if you expect a significant economic downturn, that there will likely be a better time to buy F&G, as its CLO exposure will cause some concern about potential losses, but that would likely prove to be a buying opportunity. While insurance is seen as “noncyclical,” I view F&G as likely to trade as a cyclical company, and investors should recognize that. Overall, while shares will not repeat their 93% return, FG generates an attractive spread on its investments, creating further upside, and I see 15% total return potential between appreciation and dividend payments over the next year.

For further details see:

F&G Annuities & Life: Further Upside, But Its Investment Portfolio Bears Watching