FG - F&G Annuities & Life: Likely Acquisition Target With Projected 30%+ Annual Return

2023-04-21 12:26:18 ET

Summary

- Fidelity National spun off 15% of annuity company F&G in December 2022. The full spinoff is probable in the second half of 2025.

- Only two pure-play annuity companies remain independent. Others have been acquired by alternative asset managers and bigger life insurers. F&G is a likely target in 2025.

- F&G is quickly and profitably growing with ROE in the mid-teens. In 2025, it will be fully scaled.

- F&G has been undervalued since the spinoff exacerbated by the bank crisis in March. With a 4.4% dividend yield and a buyback program, it is a growth company priced at a value.

I stumbled on F&G Annuities and Life ( FG ) via an SA article . The company's filings further increased my interest: F&G was almost a perfect copy of Athene ( ATH ), Apollo Global's ( APO ) retirement services subsidiary.

I analyzed Athene several times in my articles on Apollo and other alternative asset managers. It did not take me long to formulate the investment thesis: several alt managers striving to increase their insurance footprint would gladly snap F&G the minute it becomes available at a huge premium to the current price. Big life insurers may also get interested, perhaps, in a combination with an alt manager. But even if the acquisition does not occur (which I find hard to believe), the standalone F&G is a delicious investment due to its combination of high growth, high yield, and low valuations.

What follows is a more detailed discussion of this investment thesis. My regular readers will find some themes familiar from my Athene analysis.

What is F&G?

The insurance company under the name Fidelity & Guarantee was founded in 1959 and went through several transformations until it was acquired on June 1, 2020, by Fidelity National Financial ( FNF ). For reasons that will become clear shortly, this date is important.

Even though the company is called now F&G Life And Annuities, there is very little Life in it but plenty of Annuities. Fixed annuities (mostly fixed indexed annuities) are by far the main product. Additional products include other types of annuities - immediate annuities, group annuities (aka pension risk transfers - PRT), and funding agreements (while not annuities, they are almost identical in structure). The only life product today is the so-called Indexed Universal Life comprising only 5% of GAAP Net Reserves. Since its contribution is so small, we will ignore it in our analysis.

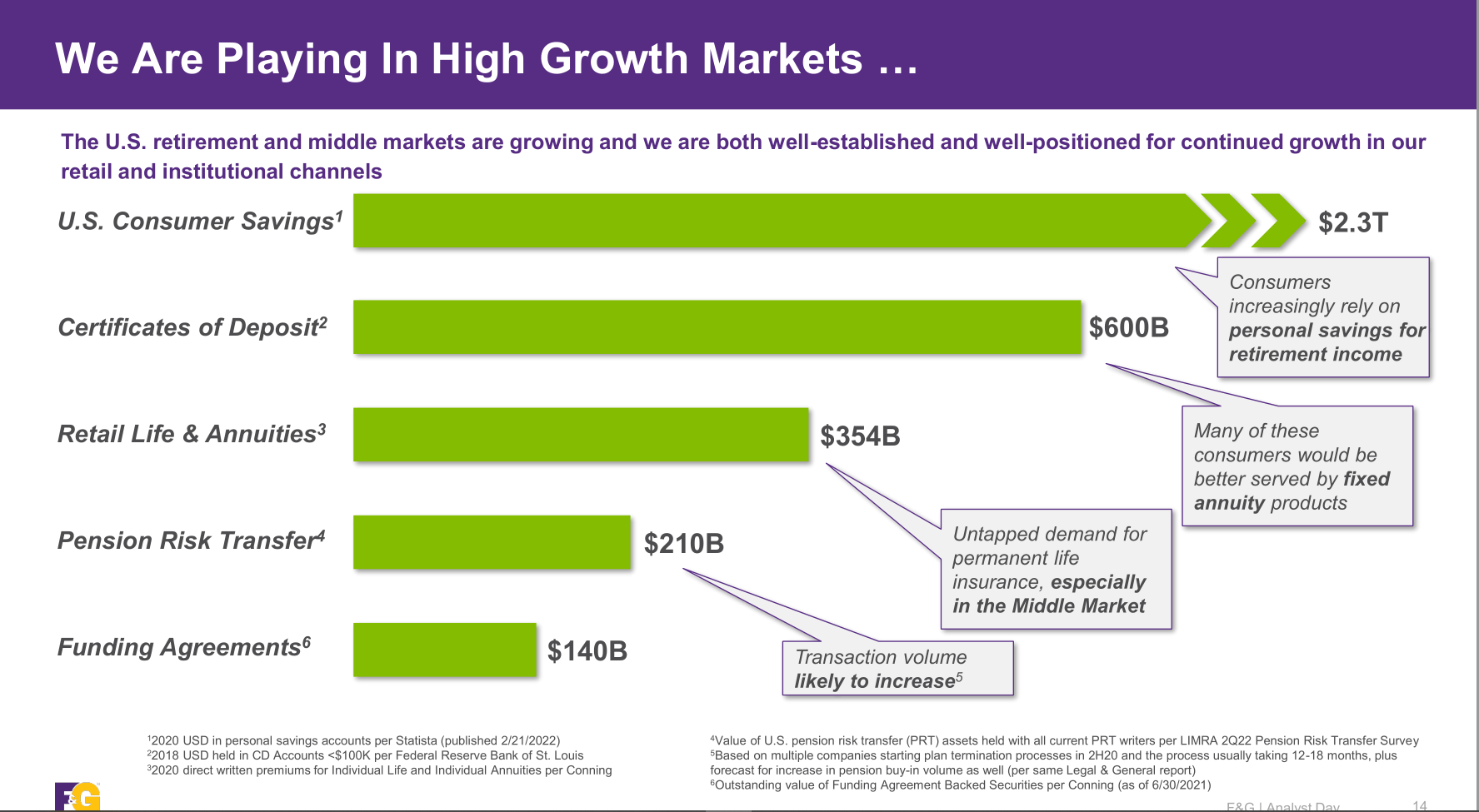

The number of retirees in the US is growing quickly because baby boomers quit the workforce and longevity keeps increasing due to medical advances. It stimulates demand for annuities which remain one of the main retirement vehicles. The demand is further exacerbated by PRTs when companies offload pension obligations to specialized retirement specialists like F&G. To illustrate what is going on, I will reproduce one of F&G's slides:

{kind=link}

Fixed annuities are structured almost exactly like bank CDs - they pay fixed interest for a specified term and can be renewed after that at a different interest rate. Differently from CDs, they are guaranteed by an insurance company instead of FDIC. Their major advantage is a tax deferral - an annuity can grow tax-free for many years until it is withdrawn.

Fixed indexed annuity adds a kick by offering potentially higher appreciation linked to an index, mostly to the S&P 500. While its appreciation rate is lower than the index appreciation in good years, a certain minimum return is guaranteed even in bad years. The insurer does not expose itself to equities. Instead, it purchases call options that provide appreciation but limit risks. Fixed indexed annuities are a hot product for (future) retirees.

I suspect that some stock investors may underestimate fixed annuities' appeal and consider them an inferior financial tool providing meager returns. By association, this attitude may be transferred to the annuity company's stocks.

This is biased logic. Plenty of rank and file prefer guaranteed and tax-deferred returns to the vicissitudes of the stock market. As a result, a fraction of (future) retirees always pick annuities as their main or auxiliary retirement vehicles.

Athene's example has demonstrated that smart annuity companies can be very successful when fostered by favorable demography. Athene has grown at a CAGR of 15-20% since 2009 with an ROE of 15% and higher. This is in stark contrast to most big life insurers that are not specifically focused on annuities.

Athene's secret juice has two ingredients. First, the company does not do anything but annuities. Even though it belongs to the life insurance industry, it does not sell any life insurance or any other type of insurance. Having only annuities on its balance sheet, Athene's obligations are very simple: it promises its customers x% in interest for the term of n years. Nothing more and nothing less (I am slightly oversimplifying but it is mostly correct). As long as Athene can invest customers' deposits at a rate higher than x%, it delivers a reliable spread. Its net profit consists of this spread less overhead and taxes.

Here comes the second ingredient. Using Apollo's investing capabilities, Athene generates returns superior to other life insurers. Consequently, its spread is high and its overhead is low due to the scale achieved.

F&G follows Athene's recipe almost literally. It has the same retirement products and generates superior returns as well due to its exclusive long-standing relationship with Blackstone ( BX ). Blackstone receives management fees as a percentage of the total F&G investment portfolio plus additional compensation for certain investment products. F&G in its turn determines the structure of this portfolio including duration, required credit quality, and so on.

Within Blackstone, a separate group is being responsible for investments designated for insurance companies. A former head of this group Chris Blunt has been F&G CEO since 2019.

The role of Fidelity National Financial

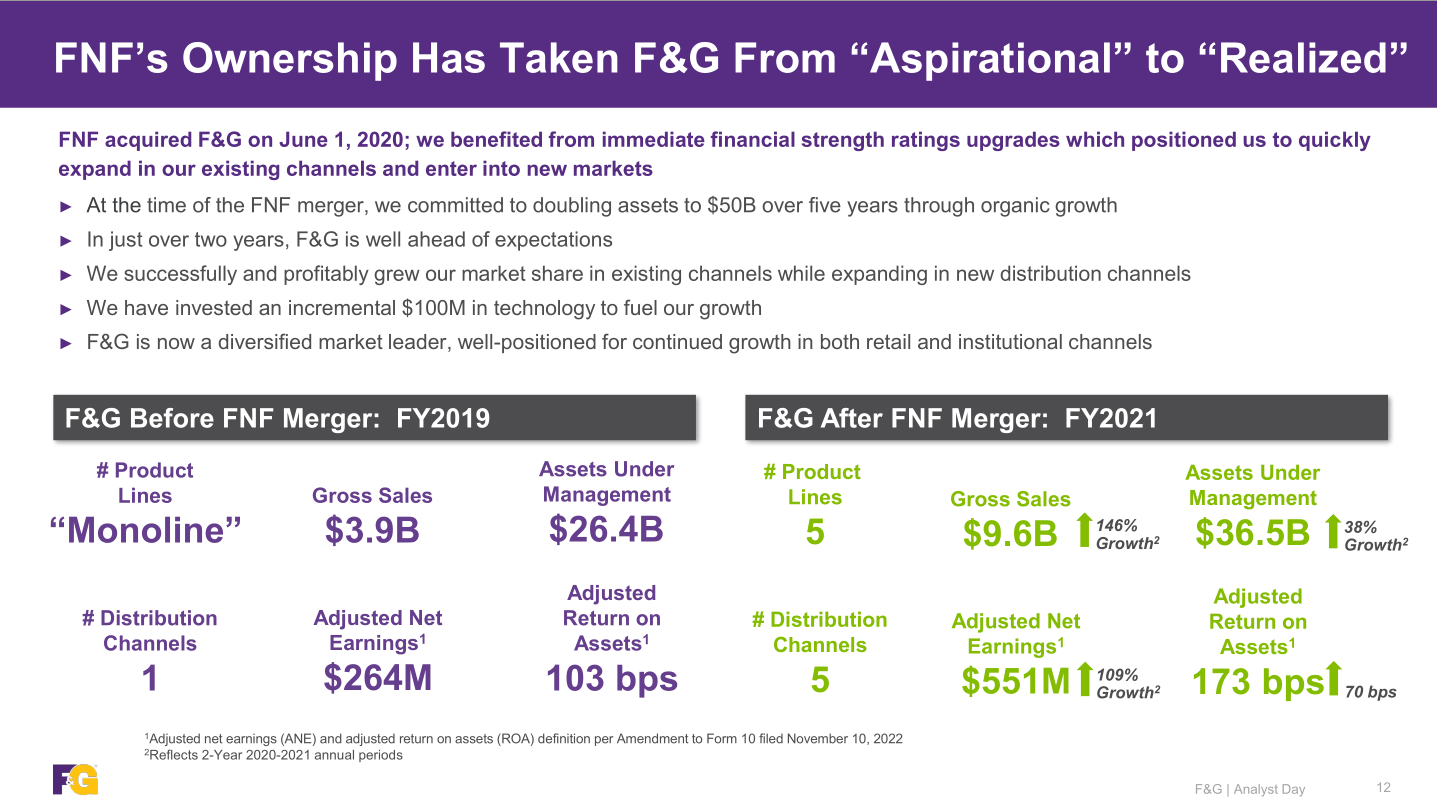

For almost 2.5 years, F&G has been a 100% subsidiary of FNF and this period was extraordinarily productive:

{kind=link}

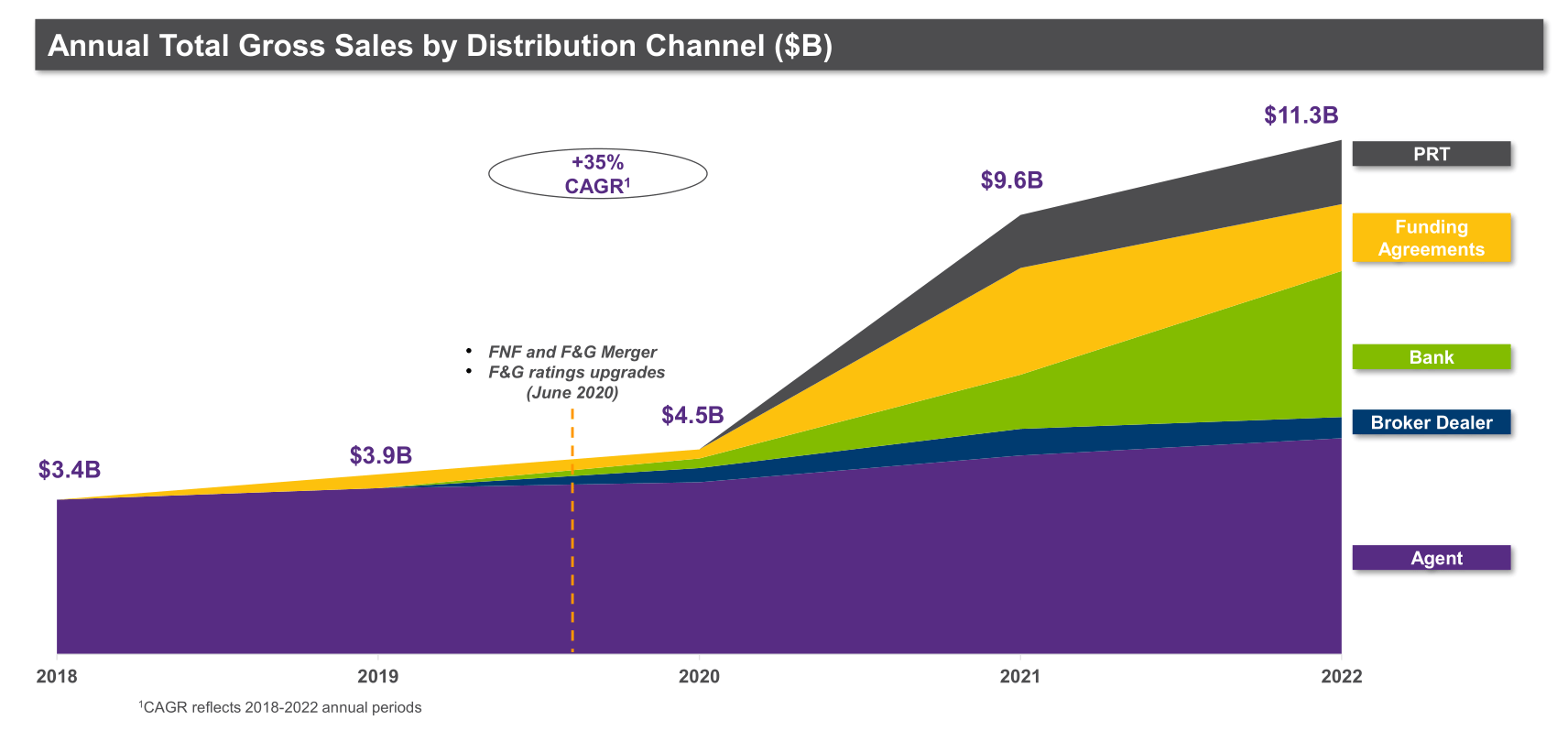

The progress is particularly impressive in a graphic form:

{kind=link}

In December 2022, FNF spun off 15% of F&G tax-free to FNF shareholders with an obvious intention to expose the company to external investors. It appears the first step of monetization. Starting from June 1, 2025 (after 5 years of ownership), FNF can spin off the rest of F&G tax-free to its shareholders, something it cannot do right now. 5 years of ownership of 80% or more is a requirement for tax-free spin-offs under the Section 355 of Tax Code.

FNF officers and Board members own 5.8% of its stock. Upon the full spin-off, they will receive a 5.8% of F&G tax-free and will pocket further significant gains if F&G is later acquired by one of the alternative asset managers and/or big life insurers.

Valuations

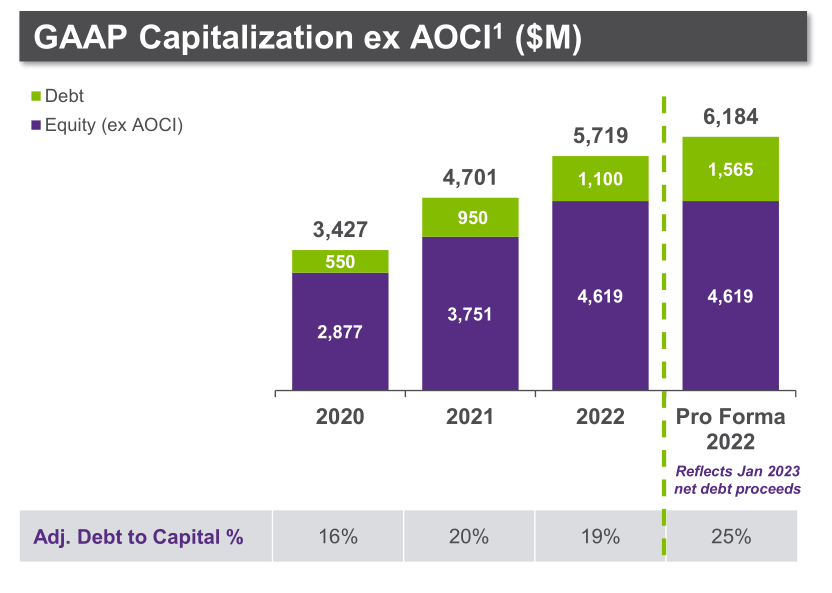

F&G's predecessor was acquired by Blackstone funds, FNF, and some third parties for $1.8B in 2017. In 2020, FNF paid $2.7B to become the only owner. The current market cap of F&G is $2.3B but the company is much bigger than it was in 2020. A partial spin-off is supposed to unlock value.

{kind=link}

At the end of 2020, the company's book value per share ("BVPS") ex-AOCI was about 2,877/105 ~ $27. At the end of 2022, the same number was 4619/126 ~ $37. The stock at the time of writing is trading at $18.50.

This is close to the level it was trading at immediately after the spin-off. CEO Chris Blunt made significant purchases on the open market at ~$18-19.

In early 2023, the stock reached $24 until it plummeted after the collapse of the Silicon Valley Bank (SIVBQ) and related bank panic. This is not surprising because annuity companies are the closest to banks among all insurers.

In 2023, the company made two important announcements. First, it started paying a dividend of 20 cents quarterly for a current yield of ~4.4%. Secondly, it announced a three-year share repurchase program of $25M equal to a meager 1% of the market cap. However, since only 15% of F&G shares are trading publicly, it represents ~6% of the public float and may become an efficient additional lever to affect the stock price.

Based on this combination of events, the stock appears cheap. Nonetheless, Two questions are timely:

- What is the fair value of the stock today?

- What could be the expected target price in case of acquisition in 2025?

The first question is more challenging.

Without adjustments, it is difficult to interpret GAAP results as they include mark-to-market (MKM) accounting entries of multiple moving parts - bonds, annuity liabilities, several kinds of derivatives, and alt investments that F&G uses for 6% of its investment portfolio. Many MKM changes are temporary that will eventually get reversed or non-recurring. To exacerbate things, F&G is also not fully scaled up yet and produces more accounting noise than, say, Athene.

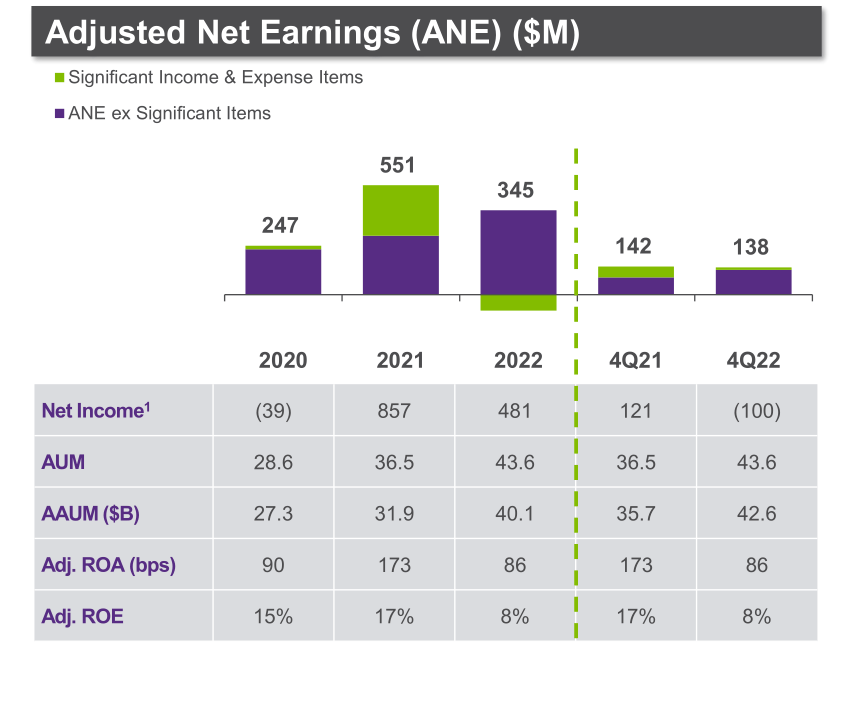

To present comparable year-to-year results, F&G adjusts its net income for all these items producing Adjusted Net Earnings on the slide.

{kind=link}

In 2021, Significant Items (i.e. various adjustments) were very big. In 2022, they seem small but only because several big adjustments cancel each other. Please notice, however, that Average Assets Under Management (AAUM) - an objective metric that does not need adjustments - are growing quickly which indicates strong progress.

If we further normalize ANE for alts (their returns fluctuate but F&G expects an 11% normalized return which is below historical results) and divide by the average number of shares, we get $3.34 and $3.55 ANE per share for 2021 and 2022 respectively. It corresponds to the current P/E of 5.2. This is cheap even for mediocre life insurers which are often trading at a P/E of 7-8 with inferior ROE and growth. At a P/E of 8, F&G would be worth ~$28. This is probably the best estimate of fair value available as long as one trusts normalized ANE numbers.

It is easier to estimate the F&G acquisition target price. Due to multiple M&A events in the industry, the only other publicly traded pure annuity company today is American Equity Investment Life Holding ( AEL ). In late 2020, AEL received a takeover proposal from Athene at $36 per share but found a white knight in Brookfield, that took a significant stake and agreed to reinsure $10B of AEL's annuity liabilities.

At the end of 2022, AEL received another takeover proposal for $45 per share which was rejected. First, it confirms that annuity companies are in high demand from bigger or opportunistic players. And secondly, we can assume that both offers were linked to AEL's BVPS.

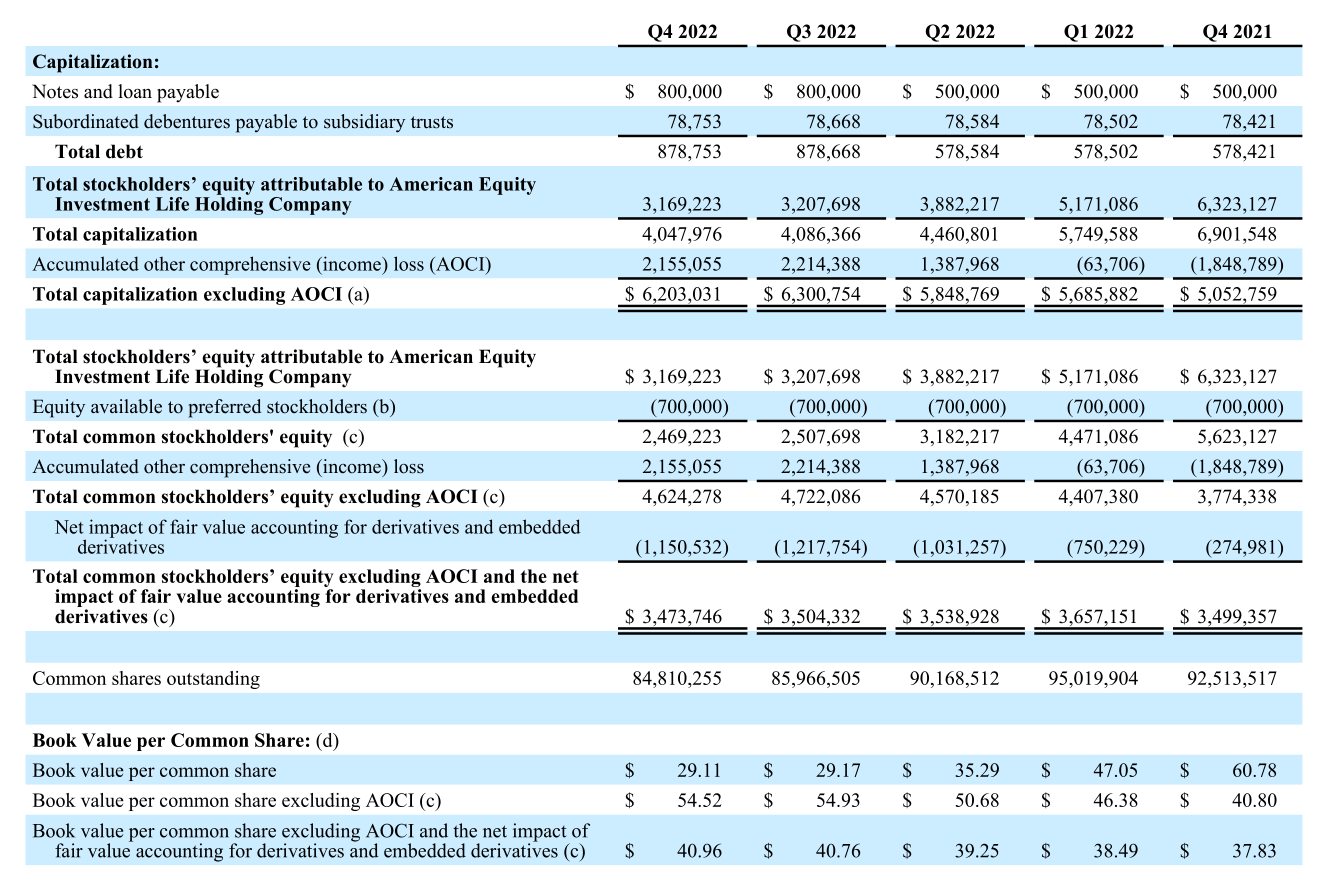

AEL publishes three variants of BVPS as on the next slide:

{kind=link}

I guess BVPS ex-AOCI and BVPS ex-AOCI and the impact of derivatives are what we need. They are currently ~$55 and ~$41 respectively in line with what was offered to take over. Between the two, I prefer BVPS ex-AOCI as a better gauge because AOCI is strictly temporary assuming no credit losses in the fixed-income portfolio. The impact of derivatives, on the other hand, accounts for the current valuations that may or may not be temporary in the end.

For F&G, BVPS ex-AOCI was $36.66 at the end of 2022. By mid-2025, we can expect the same number to appreciate, say, 20% (assuming mid-teen ROE and deducting dividends) and reach ~$44. A takeover proposal might come at $36-40.

$36 per share takeover price translates into a 100% return in 2.5 years plus a 4% dividend. The expected CAGR would be around 36%.

Conclusion

F&G presents a salivating opportunity if our acquisition scenario materializes. But what can go wrong?

If for some reason, annuity companies stop being in demand in 2025, the expected annual return will be much lower than 30%+ but still quite respectful: F&G seems very undervalued now due to the recent bank crisis and grows in the mid-teens with a rich yield. FNF is banking on the potential upside and will be very supportive. So, while the acquisition is a likely booster, the no-acquisition scenario by itself is not a risk.

Let us consider the usual scarecrow for life insurers - surrender risk. Deferred annuities are multiyear financial instruments that individuals use for long-term savings. Upon withdrawal, an individual pays a)taxes on accumulated multi-year gain at ordinary income rates; b) a 10% penalty if the individual withdraws before she/he is 59.5 years old; c)surrender charges if the withdrawal happens before the contractually stipulated term; d)MVA (market value adjustments) if an individual surrenders the policy to take advantage of rising interest rates that are higher than what an insurer promised.

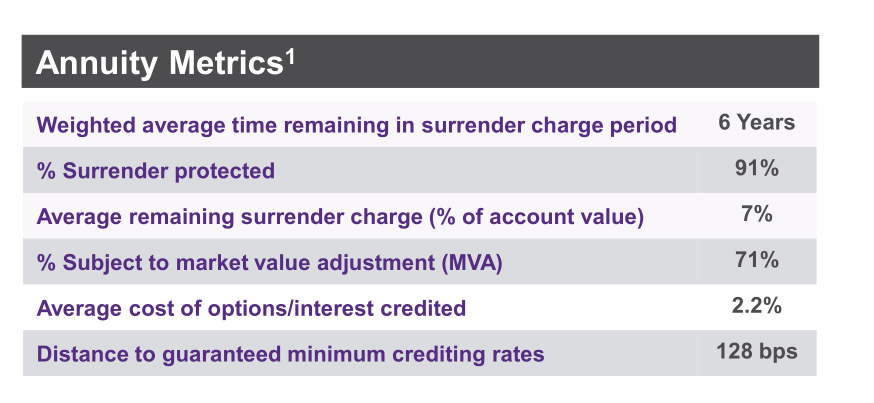

The damage to an individual's retirement savings upon surrender is so high that only in dire circumstances such as a long and deep recession, mass surrenders may be expected. And F&G's scorecard in surrender protections is strong:

{kind=link}

Other regular suspects such as leverage, credit risks, weak segments, and operational risks do not raise red flags either. Only short history of independent public trading and reporting limits our exposure to this promising issue.

For further details see:

F&G Annuities & Life: Likely Acquisition Target With Projected 30%+ Annual Return