FNB - F.N.B. Corporation: A Solid Bank In The Current Environment

2023-06-01 13:00:00 ET

Summary

- F.N.B. Corporation's share price remains down 22.3% from its 52-week high, despite strong fundamentals and stability during the recent banking crisis.

- The company has a solid deposit base, with 76% of deposits insured, and has maintained profitability with growing net interest income and other income.

- Although the loan book composition is not ideal, F.N.B. Corporation's low debt and high loan amounts make it an attractive buy opportunity.

Although the seeds of disaster were planted far earlier, early March of this year marked the beginning of a rather painful time for the financial sector. Multiple regional banks, some fairly large and others small, failed. This sparked concerns of contagion spreading. And as a result, many quality companies were significantly negatively impacted. Some of this pain was definitely warranted. But some of it was also unwarranted. One company that experienced a downside during this time, and that still remains depressed from a share price perspective, happens to be F.N.B. Corporation ( FNB ). While it is true that shares have not fallen as hard as what other firms experienced, the stock is still down 22.3% from its 52-week high and has only recovered by 13.3% from its 52-week low. But when you dig into the fundamentals, it becomes confusing why the market is worried at all. When you factor in all of the important data points, it's difficult to imagine the company representing anything other than a fairly attractive 'buy' opportunity at this time.

Great stability

The banking crisis that we experienced earlier this year began with the collapse of Silicon Valley Bank. With large amounts of uninsured deposits, and exposure to some of the most vulnerable companies imaginable during a period of high interest rates and uncertain economic conditions, the company made for a perfect spark for the crisis. Frankly, I think it's shocking that really nobody predicted this coming, myself included. After it failed, with the failure being driven by significant deposit withdrawals engaged in by customers, the contagion spread to other institutions. Some failed, while others took a beating but kept on ticking. But there were some firms that held up really well during this time. One great example that I can point to is none other than F.N.B. Corporation.

As I mentioned already, shares of the company plunged. I can understand why some initial downside might have been generated. After all, it's a fairly small bank and during a crisis, you rarely have a good idea of which firms will hold up and which ones won't. But since then, new data has come out, and it has shown that the company is remarkably strong right now. But before we get that, we should touch on the data leading up to this point.

{kind=link}

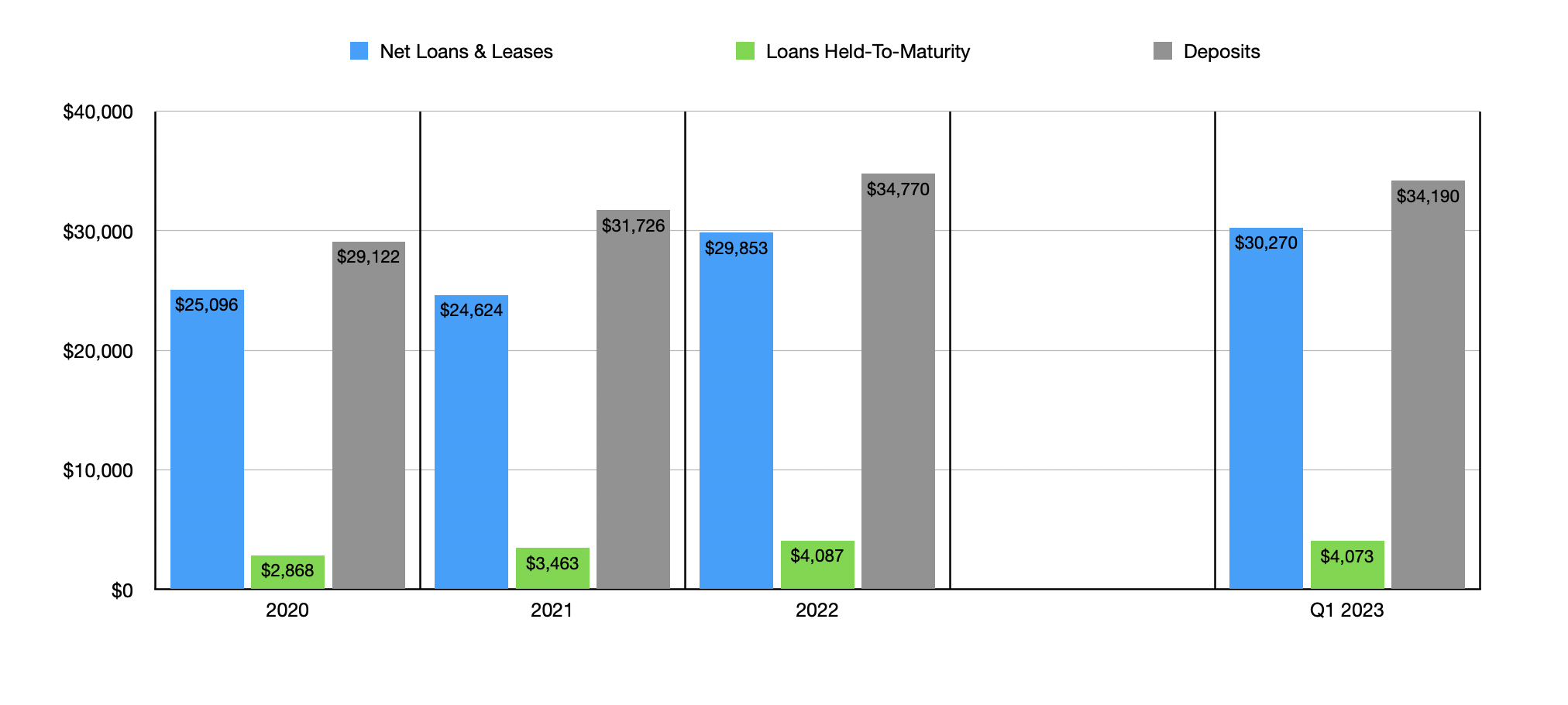

In 2022, F.N.B. Corporation boasted net deposits of $34.77 billion. That's up comfortably from the $29.12 billion worth of deposits that the company generated in 2020. In my opinion, the deposit picture is the most vital when it comes to a bank. Given how painful the crisis was lurking, it wouldn't be shocking to see some pullback in overall deposits. This would be fueled by depositors withdrawing their capital from uninsured accounts and relationships. But as you can see in the chart above, we saw only a modest dip in deposits. These came out during the first quarter of the 2023 fiscal year to $34.19 billion. That's a decline of only $580 million, or 1.7%. In addition, management said at the end of the most recent quarter that approximately 76% of the company's deposits are currently insured. That translates to roughly $8.21 billion of uninsured deposits. Unfortunately, management has not provided data for any time period before that. But that is quite a large portion of assets that are insured. To put this in perspective, the amount of assets that were insured for First Republic Bank, which ultimately failed, came out to 33% at the end of its 2022 fiscal year prior to the crisis starting.

{kind=link}

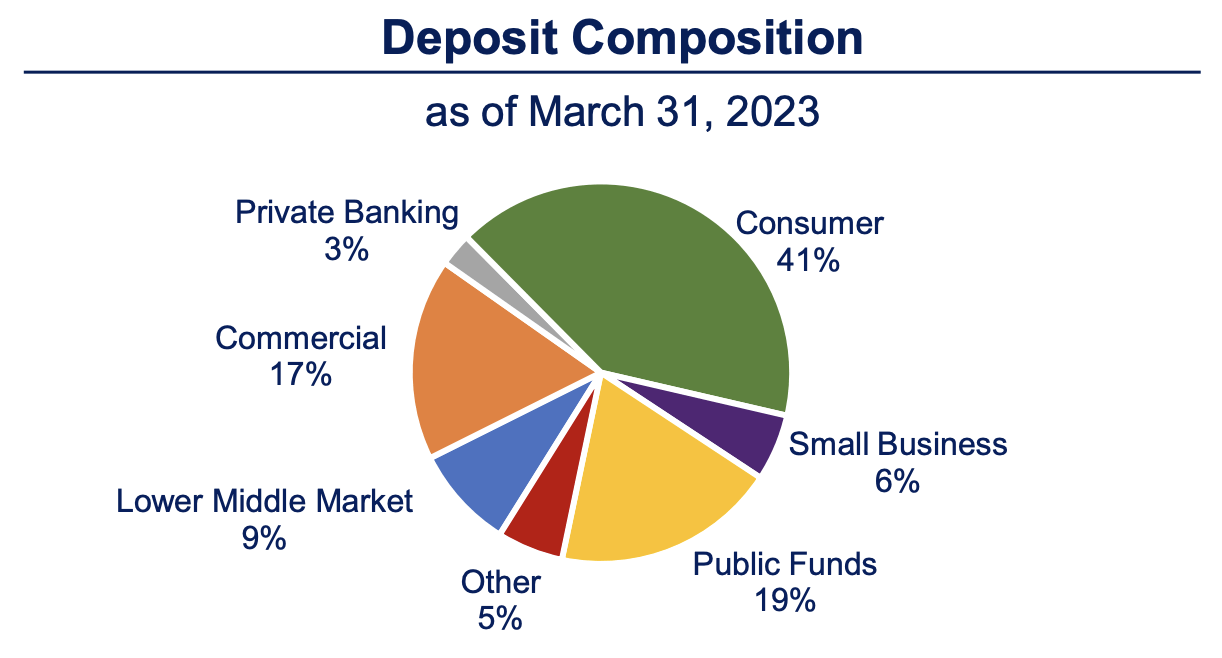

When it comes to deposits , it is worth noting that 41% of overall values are associated with consumers. Public funds and commercial enterprises accounted for the next largest amounts at 19% and 17%, respectively. One of the issues facing many of the banks that failed is that they had a good amount of exposure to startups and funds that invested directly in them. Only 6% of deposits on F.N.B. Corporation's books come from small businesses. Never mind the fact that essentially all of the company's assets are located between eastern and midwestern states, excluding New York.

{kind=link}

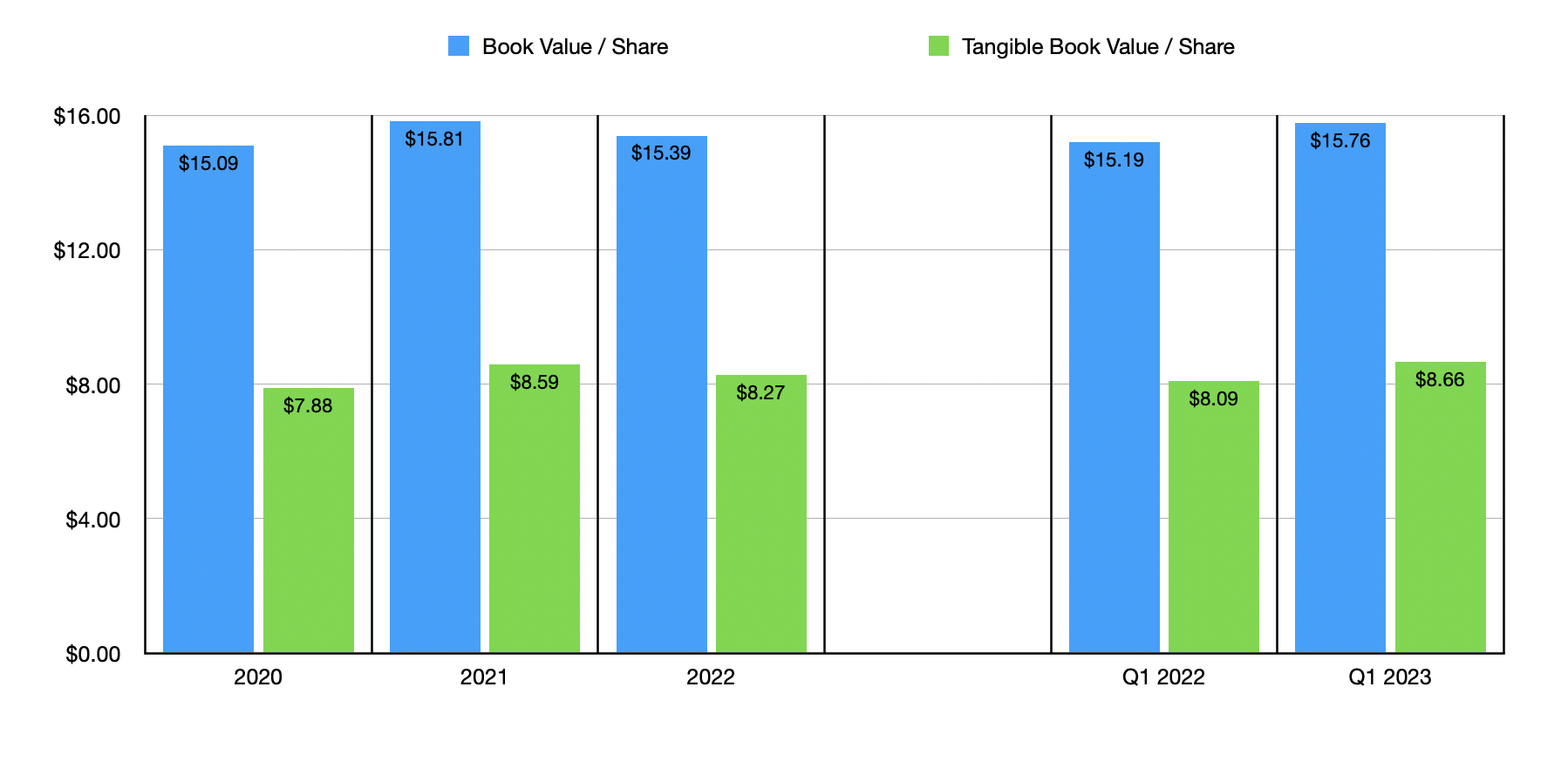

There are also some other positive facets for investors to look at. For instance, the value of loans on the company's books continues to climb. At the end of 2022, the firm had net loans and leases totaling $29.85 billion. By the end of the first quarter of this year, this number had inched up to $30.27 billion. This helped to keep the book value per share of the company elevated as well. In 2022, overall book value totaled $15.39. This grew to $15.76 by the end of the most recent quarter. Tangible book value, meanwhile, grew from $8.09 per share to $8.66 per share. It is worth noting that, on its own, this is not all that important a figure. Some of the more troubled banks, including at least one that failed that I covered, saw this metric increase immediately before it collapsed. This is all useful in conjunction with the deposit data.

{kind=link}

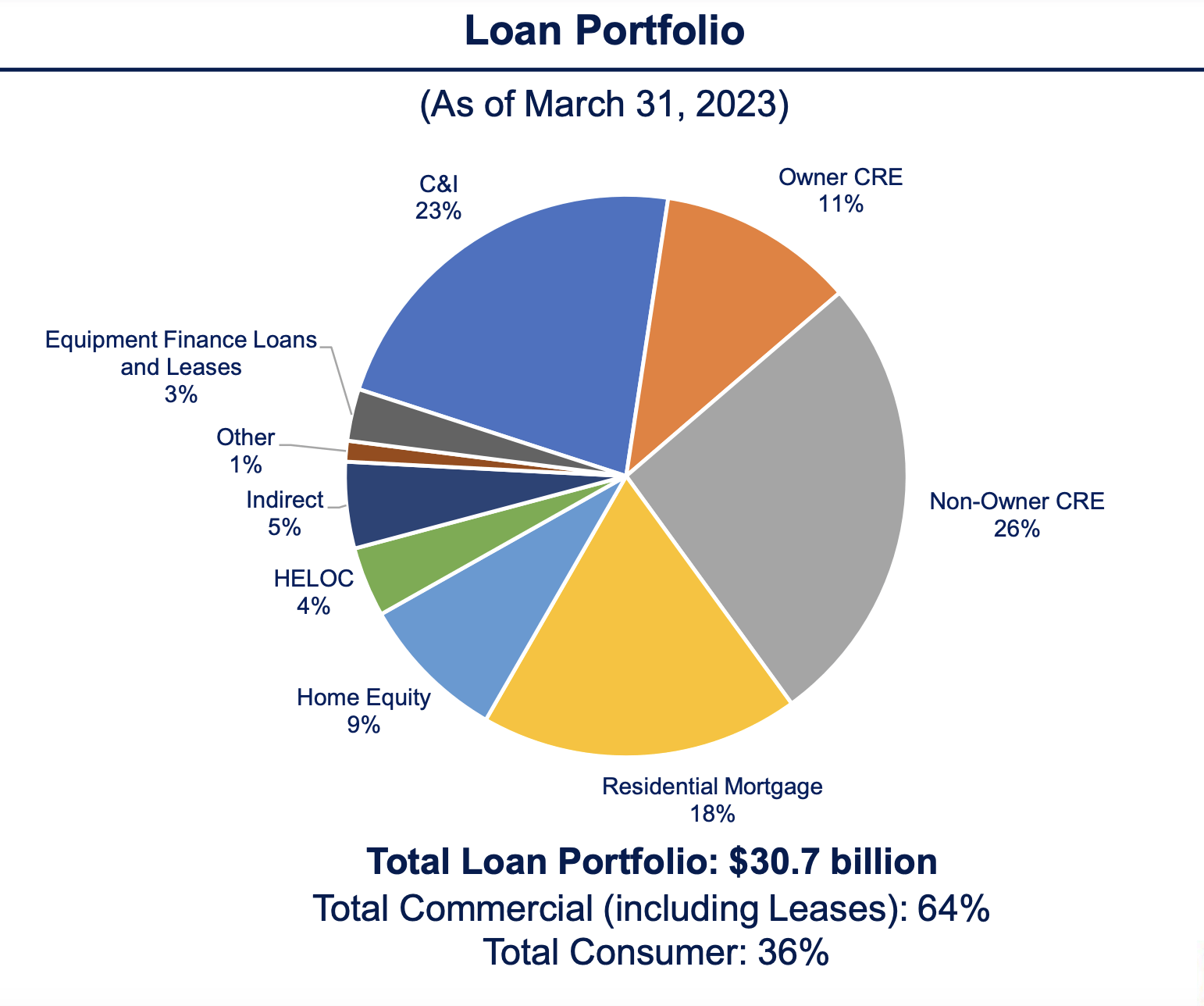

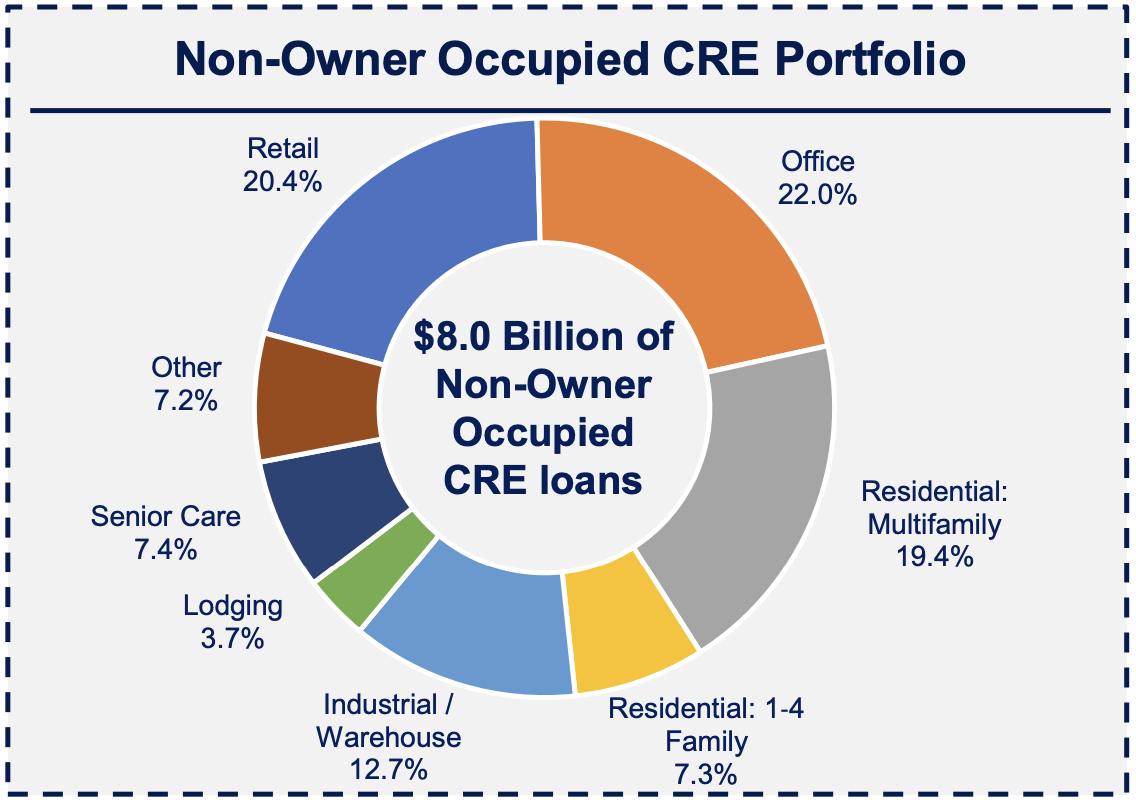

I wish I could say that the company had a fantastic loan book. It's certainly not bad. But it's not exactly the composition I would like to see. It is true that 18% of the loans are associated with residential mortgages, with another 13% split between home equity and HELOC arrangements. However, 23% of loans are centered around commercial and industrial activities, with another 37% attributable to commercial real estate. Of that 37%, only 11% involves commercial real estate that's owned by the party that has taken the loan out. This leaves a rather large 26% that's classified as non-owner commercial real estate. This translates to about $8 billion of non-owner occupied commercial real estate, with 22% of that involving office space and another 20.4% involving retail. While not enough to sink the ship, that office exposure does not sit terribly well with me.

{kind=link}

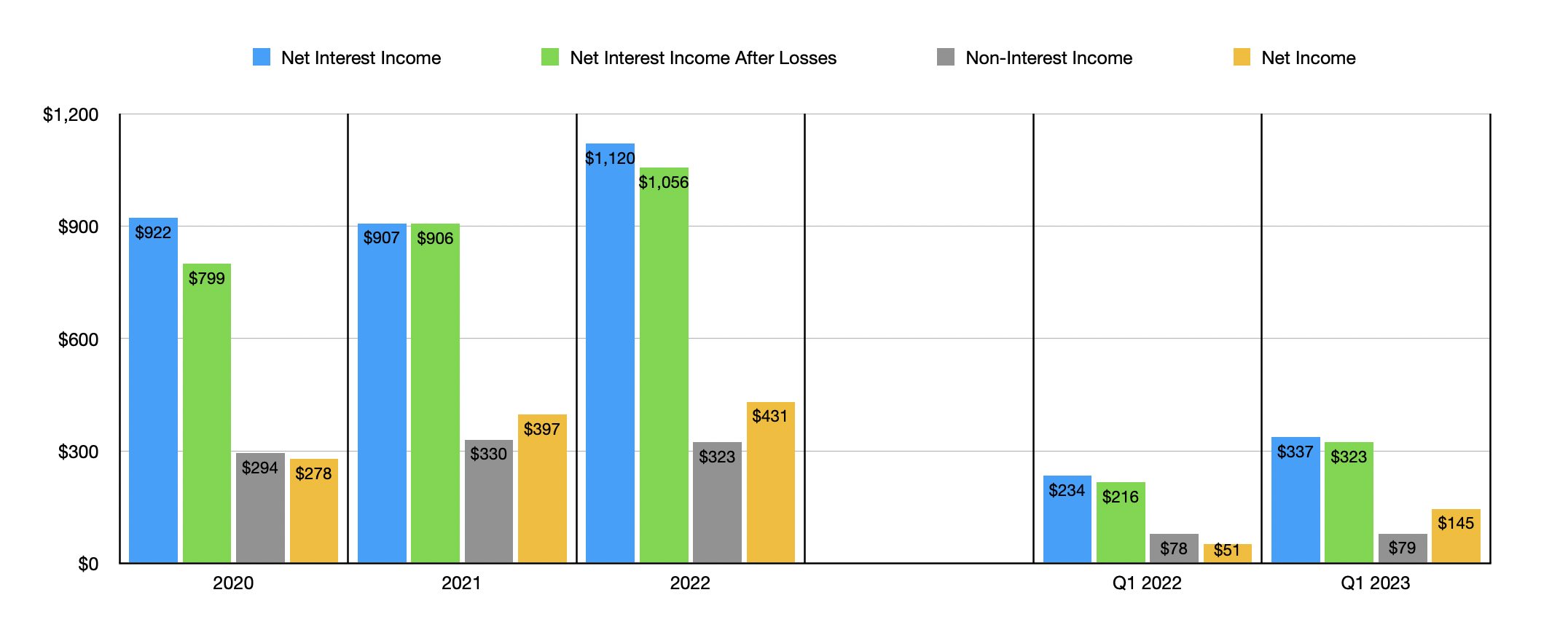

Another great thing about F.N.B. Corporation is that it has succeeded in keeping itself highly profitable. Net interest income for the company expanded from dollars in 2022. Other income increased during this time period from $294 million to $323 million. These items helped overall net income for the company jump from $278 million to $431 million. For the most recent quarter, overall net profits came in at $145 million. That's almost triple the $51 million reported one year earlier. And this was also driven by higher net interest income and other income.

{kind=link}

One problem that some of these banks faced leading up to the collapse was that, as deposits plunged, they were forced to take on short-term borrowings from regulators. These borrowings brought with them significantly higher interest expense. And that, in turn, pushed profits down. As you can tell, profits aren't an issue right now. And that's because, in part, overall borrowings for the company remain low. Total short-term borrowings on the company's books came in at $3.45 billion during the most recent quarter. This is up from a $2.47 billion reported at the end of 2022, with a sizable chunk of the increase coming from a rise in FHLB (Federal Home Loan Bank) borrowings from $930 million to $1.60 billion. The rise in borrowings does not have a material impact, by the way, on the company's overall liquidity. At the end of the most recent quarter, according to management, the business had liquidity that was 170% of its uninsured and non-collateralized deposits. This gives it plenty of wiggle room in the event that uninsured deposits do become a problem.

{kind=link}

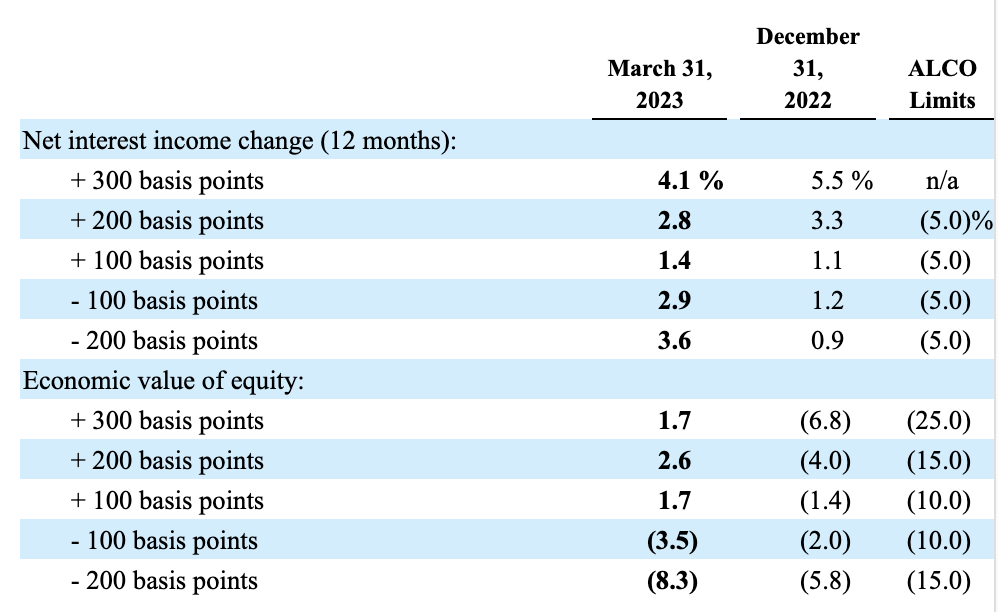

The low amount of debt, combined with the high amount of loans that the company has on its books, actually means that an increase in interest rates should prove bullish for the company. I know that we are likely at the point where interest rates won't rise from here. In fact, I suspect that around the end of this year, we will be talking about an interest rate decrease. But as you can see and the image above, a 1% increase in interest rates would cause net interest income for the company to grow by 1.4%, while the economic value of equity for the company would grow by 1.7%. The general trend here is that the higher interest rates are, the better off F.N.B. Corporation is. Interestingly, a sudden decrease in interest rates can also help the company. A drop of 2%, for instance, will cause net interest income to grow by 3.6%. However, the economic value of equity for the company would decline by 8.3% as a result of this. This disparity seems to be thanks in large part to hedging that helps the company in the event of a sudden interest rate shock. And on the upside, the company benefits from the fact that about 60.4% of total net loans and leases on its books are variable or adjustable rate.

Takeaway

From all that I can see, F.N.B. Corporation is a really solid operator. The company's loan book is not ideal in my opinion. But beyond that, the picture looks really positive. Frankly, I'm amazed, especially after the firm showed stability during the end of the first quarter of the year, that we haven't seen any more significant rebound in the share price. I do believe that a move higher is warranted at this point. And because of that, I have no problem rating the company a 'buy'.

For further details see:

F.N.B. Corporation: A Solid Bank In The Current Environment