FNB - F.N.B. Corporation: Well Positioned After Adept Interest Rate Management

2023-11-30 20:46:36 ET

Summary

- FNB Corp's shares have outperformed many regional banks, losing only 15% of their value compared to over 30% for some peers.

- FNB's net interest income increased by 10% from last year, and its net interest margin expanded compared to a year ago, thanks to a smaller securities portfolio and stable deposits.

- The bank has a diverse loan book and a strong capital position, which could lead to accelerated share repurchases and a higher dividend.

Shares of F.N.B Corp (FNB), which operates First National Bank, have been a poor performer relative to the market over the past year, losing about 15% of their value. However, this has been better than many regional banks, some of which have lost more than 30% of their value in the wake of Silicon Valley Bank’s failure with the KBW Bank Index ( KBWB ) down over 22% in the past twelve months. FNB has navigated through this crisis well, and I see upside in shares.

{kind=link}

In the company’s third quarter , FNB earned $0.40 in adjusted EPS, beating consensus by $0.04. This was up 2.6% from last year, one of the few regional banks to have earnings growth. Banks across the board have faced higher funding costs as Fed rate hikes and deposit volatility after SVB’s failure pushed deposit rates up meaningfully. Impressively, FNB’s net interest income of $326 million was up 10% from $297 million last year.

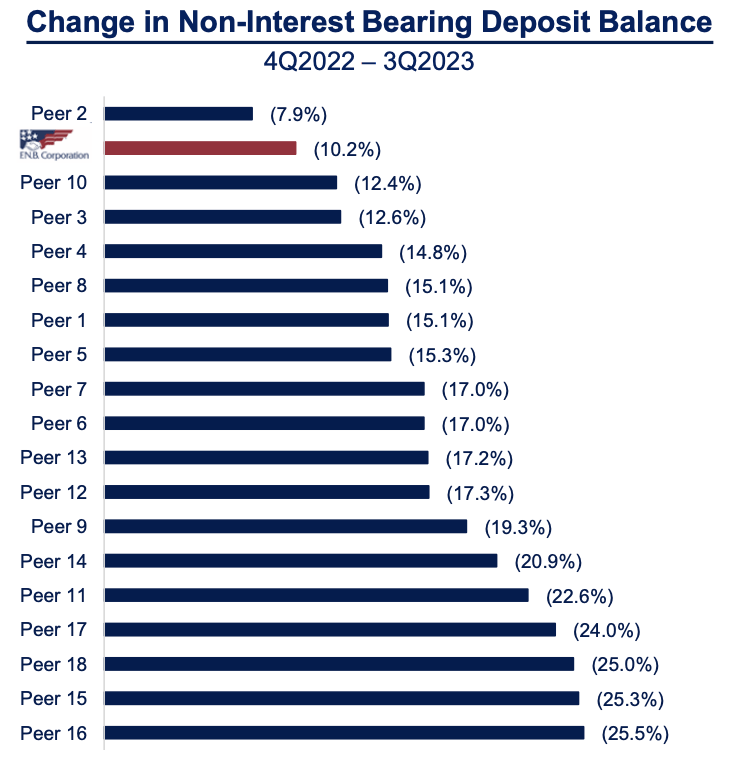

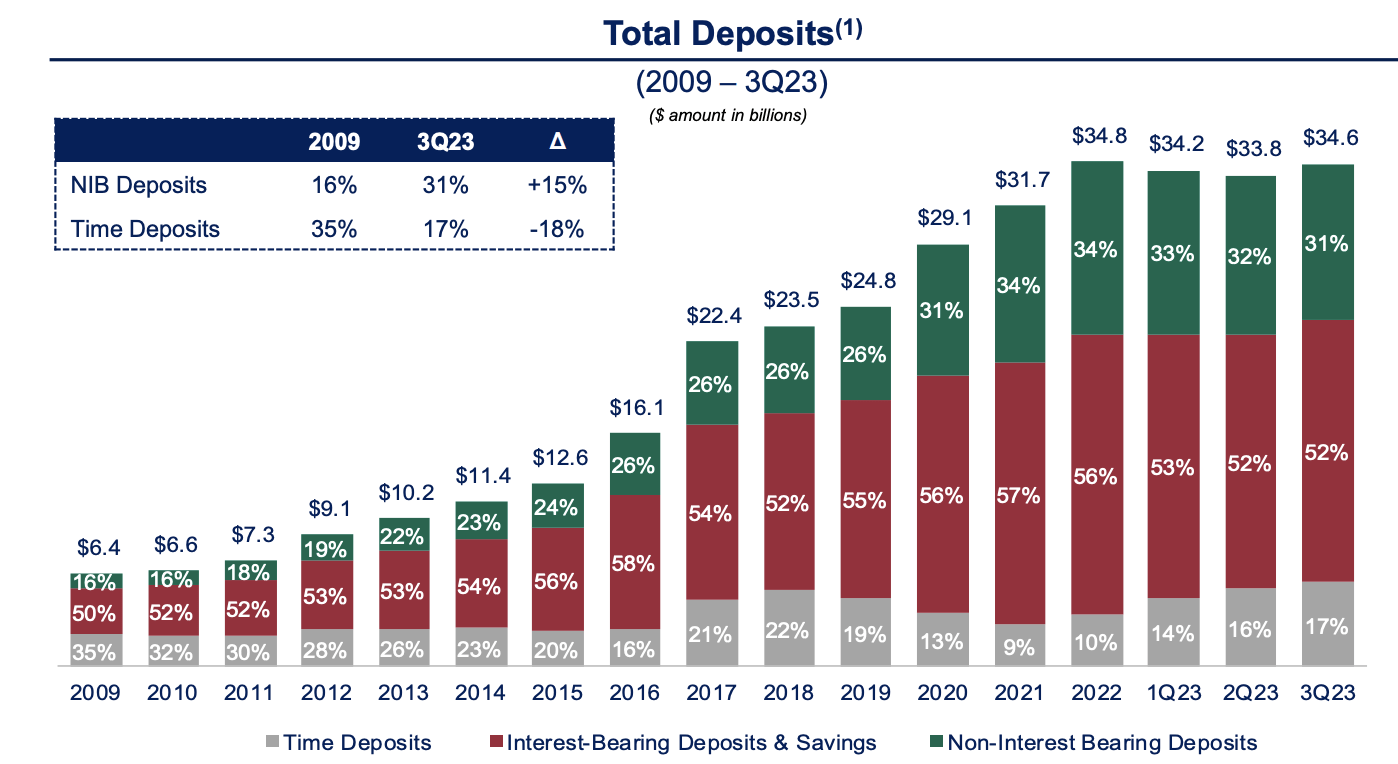

The bank’s net interest margin [NIM] was 3.26% in Q3. This was down 11bp sequentially but up 7bps from last year; FNB is an outlier in seeing NIM expansion relative to a year ago. This was because loan yields rose 155bp from last year to 5.69%. Offsetting this, interest-bearing deposits were also up to 2.36% from 0.57% and up 39bp sequentially. FNB has been helped by the fact it has lost fewer noninterest bearing deposits than peers. Noninterest-bearing [NIB] deposits were $10.8 billion from $11.8 billion last year. This comprises 31% of deposits.

{kind=link}

In a 5% world, noninterest-bearing funding is extremely valuable for banks. FNB has been steadily growing its NIB franchise for years, and NIB’s share of deposits remains above pre-COVID levels, even as it has fallen from its peak. FNB is benefitted by its granular deposit base. 40% of deposits are to consumers, 20% government, with the remaining business and private banking. The average balance is just $30,000 with just 22% uninsured or uncollateralized.

{kind=link}

For smaller accounts, the cost of leaving some extra cash in a NIB is often not worth the time and effort to actively invest the funds. This is especially true because many NIBs are transactional accounts, and there is a functional floor to their balances as consumers and businesses need sufficient cash to meet their monthly bills. The relative steadiness of its NIB platform has helped to protect net interest income. Moreover, even amidst funding turmoil in the industry, deposits rose by $800 million or 2.3% from last year.

On the asset side, FNB has delivered loan growth of 2.5% from last year. Its loan to deposit ratio is 93%, which is fairly full. As such, I would expect loan growth to be no faster than deposit growth over the next year. Most loans are floating rate, and the fact FNB focuses so much of its asset base on loans has protected it from the major damage other banks have faced on their securities portfolios with large unrealized losses in accumulated other comprehensive income (AOCI).

Now, FNB does have some fixed income securities, but at $7.1 billion this portfolio is manageable. It was down 1% sequentially and 2% from last year. The bank has just $382 million of unrealized losses here, or about 5% of the portfolio value, a manageable sum, thanks to its exposure to municipal securities. The taxable yield on the portfolio has risen to 2.46% from 1.96% last year as it has redeployed maturities into higher yielding securities. This incremental yield has also helped to offset the headwind of higher deposit rates.

FNB has a fairly high capital ratio with a 10.2% common tier one equity ratio (CET1). Including unrealized losses in AOCI, its capital position would be 8.3%, well above the 7% minimum. Because it has just $45 billion in assets though, FNB will not have to phase these losses into its capital considerations. It is worth keeping in mind the impact though as it does speak to its true economic capital position. Because of larger fixed-rate losses, many banks have capital ratios including AOCI in the 7%’s—including well-known institutions like PNC Financial ( PNC ) and Regions ( RF ) and smaller ones like Synovus (SNV).

FNB’s smaller securities portfolio has helped insulate net interest income better as well as leave pro forma capital in a stronger position. This should mean that it can accelerate repurchases and raise its dividend (which currently provides a 4% yield) more quickly than other banks, whose reported capital positions may be similar today, but who will need to retain more capital to offset the phasing in of larger AOCI losses in 2025.

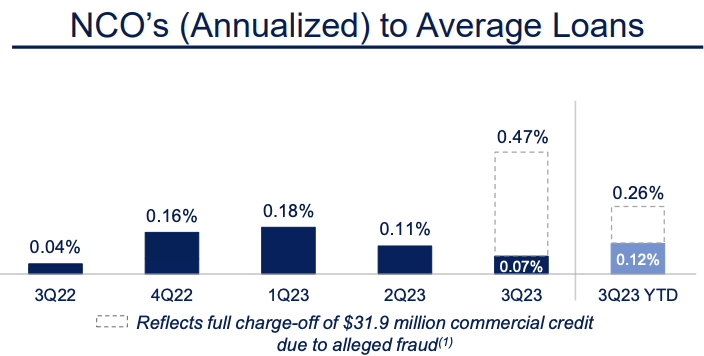

On the loan exposure, I would also add that I am comfortable with FNB’s credit exposure. Nonperforming loans [NPLS] have remained modest at 0.36%, from 0.32% last year. Now, charge-offs jumped to 0.47% from 0.04% last year. FNB took $19 million in provisions on a $32 million commercial loan. The entire outstanding balance on this loan has been charged off due to alleged fraud with the company now in bankruptcy. FNB aims to recover a portion of the charge-off during the proceedings, but given fraud allegations, it has conservatively assumed zero recovery. You can see how this one-loss skewed charge-offs.

{kind=link}

Given a history of low charge-offs, I am willing to look through this singular loss; sometimes, well-constructed frauds do occur that slip by even diligent investors and lenders. The fact this is a one-time item also exaggerates the annualized charge-off rate in the quarter, as a fraud of this size will not continue to repeat. Other than this loan, we are not seeing signs of credit degradation that is alarming. Additionally, it has allowances for credit losses of 1.25% of loans. This provides 354% coverage of NPLs, above my 250-300% level I view as strong. This provides some room for further degradation.

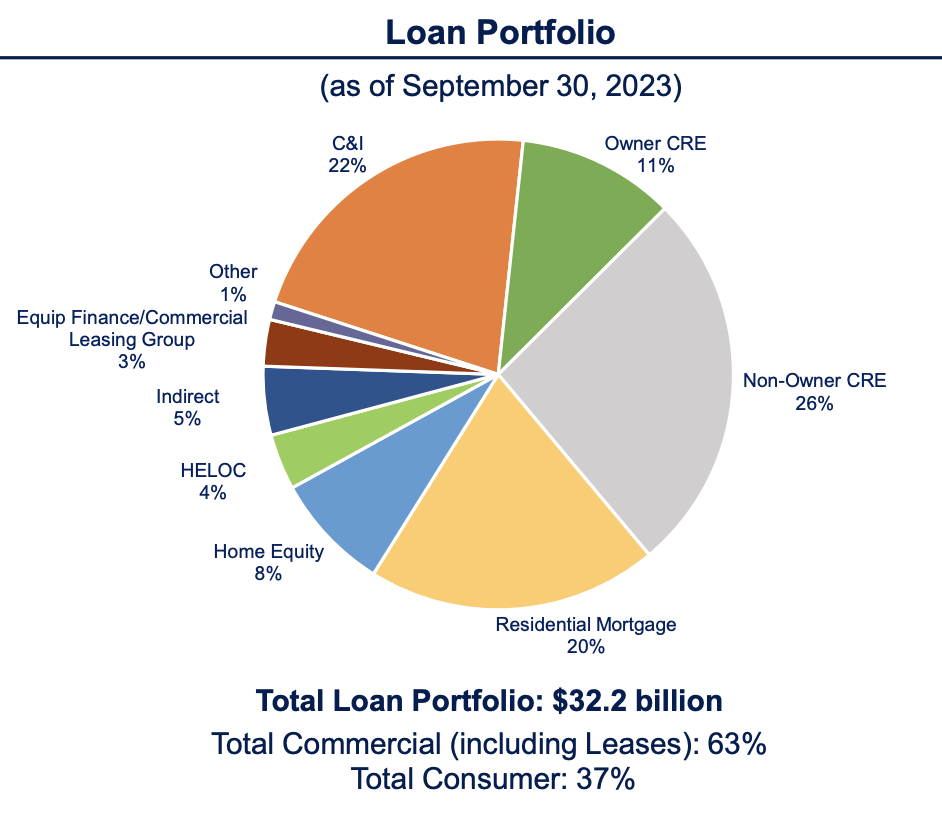

As you can see, the bank has a fairly diverse loan book with meaningful consumer, corporate, and commercial real estate exposures. Of its $8.5 billion commercial real-estate portfolio, 22% is in office. 0.25% of those are non-performing, a level which I would expect to rise given the pressures in the sector amidst remote working. Still with less than 5% of its total portfolio in office, we could see a meaningful increase here before it starts to eat through reserve and significantly impact the bank’s profitability.

{kind=link}

Now, as noted above, while NIM is higher than a year ago, it did decline last quarter. FNB has seen 3-4bps of monthly NIM compression, though the pace is moderating. As such, management expects net interest income to be about $315-$325 million of interest income in Q4, down about 2% sequentially. We are likely to see a continued gradual increase in deposit yields. Its time deposits yield 3.71% with an average maturity of 11 months; we are likely to see these roll at higher yields for the next few months, with NIM set to bottom in H1 2024. On the flip side, weaker capital markets pushed noninterest income down 2% to $81 million last quarter. With markets recovering, we may see a modest recovery here. We also should see some improvement in credit reserves as charge-offs decline to normal levels.

Assuming NIM bottoms at about 3.10% and gradually recovers, alongside a similar pace of credit reserves excluding the one fraud, FNB can earn about $1.50 next year, giving shares a less than 8x multiple. After doing just $37 million in share repurchases, FNB said it may be “active” in Q4. While the economic uncertainty may lead it to retain capital, during 2024, I would expect buybacks to pick back up. Even if it retains half of its post-dividend earnings, it can reduce the share count by 4%, on top of a 4% dividend, for an 8% capital return yield.

That is an attractive entry point for a bank that has handled interest rate stress quite well and proven to have stable deposits. Given the pressures facing the industry, virtually all regional banks trade for less than 10x earnings. I believe FNB has merited a premium valuation, relatively speaking, and see shares moving towards the 10x level as we see buybacks pick up. That provide an over 30% total return opportunity to $15, making shares quite attractive here.

For further details see:

F.N.B. Corporation: Well Positioned After Adept Interest Rate Management