FRFHF - Fairfax Financial Holdings: A Classic GARP Stock

2023-05-01 15:19:22 ET

Summary

- Fairfax Financial Holdings is a Canadian $17.6-billion market cap holding company focused on insurance, reinsurance, and investment management.

- Despite all the difficulties, Fairfax was able to increase its gross premium by 16% year-on-year in FY2022 on a consolidated basis.

- Despite experiencing $1 billion in unrealized bond losses for the year, the CEO expects much of it to reverse over the short term. The bond portfolio duration is quite low.

- Fairfax is expected to be the biggest beneficiary among Canadian P&C insurance companies in the transition to IFRS 17 due to its conservative practice of not discounting its reserves.

- I see an upside potential of ~15% by the end of FY2023, so I rate Fairfax stock as a "Buy" at its current price levels.

The Company

Fairfax Financial Holdings Limited ( FRFHF ) ( FFH:CA ) is a Canadian $17.6-billion market cap holding company focused on insurance, reinsurance, and investment management. Founded in 1985 by CEO Prem Watsa, the company owns several subsidiaries in the insurance and reinsurance industry and has investments in various industries.

It operates in 3 segments: Property and Casualty Insurance and Reinsurance, Life insurance & Run-off, and Non-Insurance Companies. Its insurance products include coverage against property losses from various causes, automobile, commercial and personal property, crop, workers' compensation, liability, and other risks. The company also offers reinsurance products. In addition, it owns and operates various businesses, such as restaurants, sports retail, travel services, holiday resorts, food processing and distribution, and hospitality real estate.

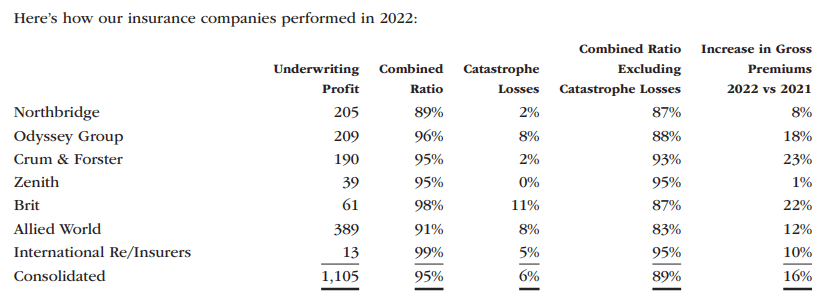

Despite all the difficulties - for example, the war in Ukraine, where the holding company had a subsidiary, or the severe catastrophe losses caused by Hurricane Ian - Fairfax was able to increase its gross premium by 16% year-on-year in FY2022 on a consolidated basis, while only 2 subsidiaries - Northbridge and Zenith - showed growth of less than 10%:

{kind=link}

Fairfax Financial Holdings has a total of about 200 profit centers that could not be managed effectively without the decentralized structure that the holding company follows - when reading the annual reports, I found myself several times thinking about how much CEO Prem Watsa prioritizes this specific feature.

Out of Fairfax's total consolidated gross premiums amounting to $27.6 billion, 75% is contributed by North America, 14% by Brit at Lloyd’s, and the rest of the 11% is spread across different regions, with 3% coming from Asia, 4% from South America, and another 4% from other international regions.

In FY2022, Fairfax experienced a substantial increase in its operating income, with a YoY growth of ~64%. The company achieved a record EBIT of $2.6 billion for the year. With the deployment of cash and short-term investments at higher rates and a strong and increasing underwriting income, Fairfax anticipates continued growth in its operating earnings.

During Fairfax's Q4 FY2022 earnings call , Prem Watsa explained how their low-duration [1.2 years] fixed income portfolio reduced the impact of rising interest rates on their bonds, resulting in a smaller decrease of only 2.8% compared to other companies in the industry that experienced 8-15% drops [recall Silicon Valley's case here]. Despite experiencing $1 billion in unrealized bond losses for the year, Watsa expects much of it to reverse over the short term. The company has been able to invest at higher interest rates, resulting in an increase of their current normalized annual run rate for interest and dividend income to $1.5 billion, which is almost 3x higher than what they had at the end of 2021 - a fantastic result amid the latest banking turmoil, in my view.

As BMO Capital Markets analysts write in their April 18 note [proprietary source], Fairfax is expected to be the biggest beneficiary among Canadian P&C insurance companies in the transition to IFRS 17 due to its conservative practice of not discounting its reserves [other peers discount them currently]. The analysts say that the company's pro forma BVPS looks attractive compared to its Canadian peers, with a 14% CAGR in pro forma BVPS growth expected through 2024, and a 14-15% ROE. The expected growth is driven by reliable sources such as strong underwriting income, higher interest income, and rebounding earnings from associates/subsidiaries.

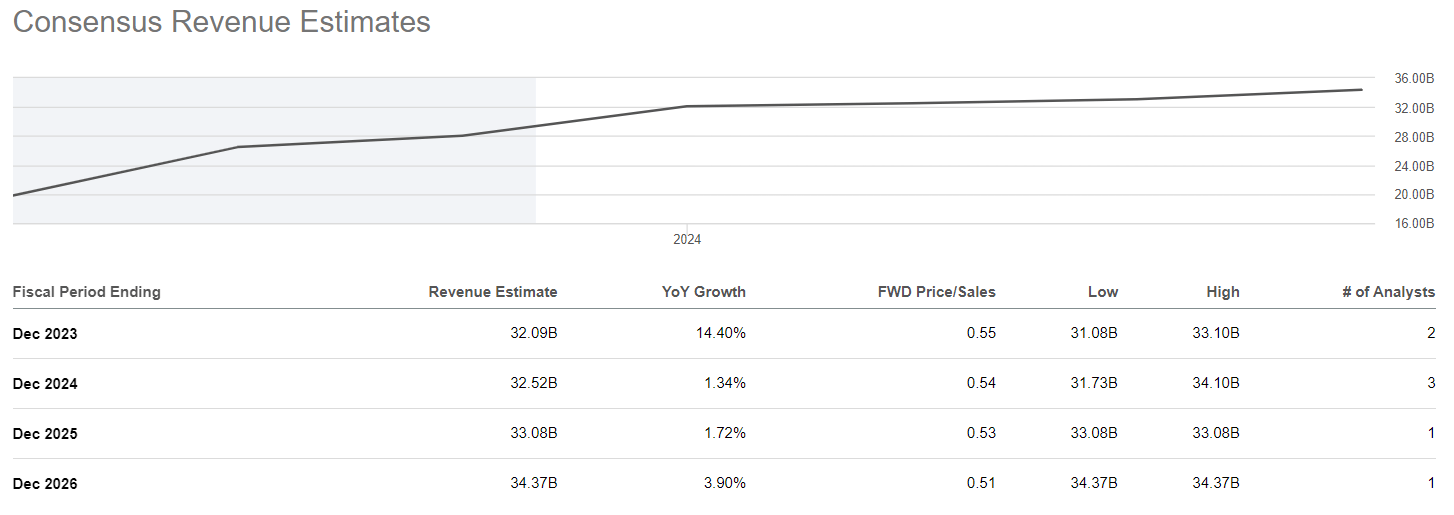

With this in mind, I would like to draw readers' attention to how the market [ consensus ] views Fairfax's revenue growth over the next few years - double-digit growth in FY2023 is likely to turn into a barely perceptible 1.34% and 1.72% in FY2024 and FY2025, which in my view seems quite unrealistic against the backdrop of a 13.35% CAGR in revenue over the last 10 years [2012-2022].

{kind=link}

Yes, past performance is no guarantee of future success - every investor learns this adage at the very beginning of their journey. But as a potential shareholder in an insurance company, it is important for me to know how management has performed in different market cycles and what its investment vision is today. To illustrate, let me quote from Fairfax's recent earnings call:

We continue to believe our common stock positions are very undervalued. I remind you that in the years 2000 to 2002, in that downturn, most stock market indices were down about 50%, but our portfolio was up 100% . In 2022, particularly in the third quarter of this year, as we discussed in our third quarter call, technology stocks including FANG stocks and Microsoft have come down significantly.

From its high-end 2021, currently, Alphabet is down 37%, Amazon 48%, Facebook 54%, Microsoft 25%, Netflix 48%, Tesla 50%. Only Apple has dropped by less than 20%. Of course, smaller tech companies like Zoom and Shopify are down 70% plus. And if history is any guide, there is more to come. I will note to you that the NASDAQ dropped 50% in 2000 and then dropped another 50% in the next two years .

Source: FFH's Earnings Call, author's emphasis added

That is, the company's chief executive, who is a member of both the operating and investment committees, is quite conservative about how Fairfax funds will be invested in the nearest future - this, I believe, provides a kind of protection in the event of a possible recession, which I have written about several times in my previous articles. As for the management's quality and financial health of the holding company, I see no reason to doubt the sustainability of Fairfax in the long run. With this in mind, I would now like to turn to the valuation of the stock and try to assess whether it has upside potential.

The Valuation

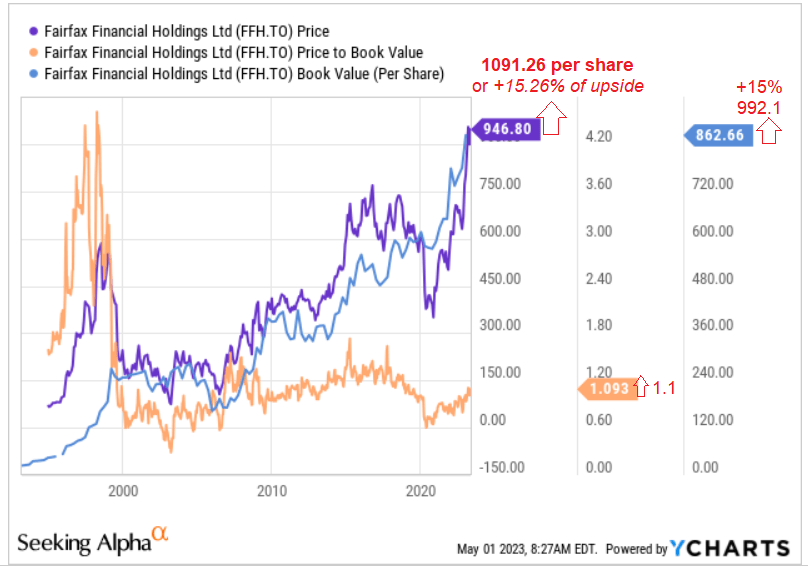

The management writes in its annual report that its focus is long-term growth in book value per share and not quarterly earnings. And if we look at the current ratios of price-to-book value and tangible book value, we can see that Fairfax stock is currently priced at about its book value level - this is the historical about-middle of the range:

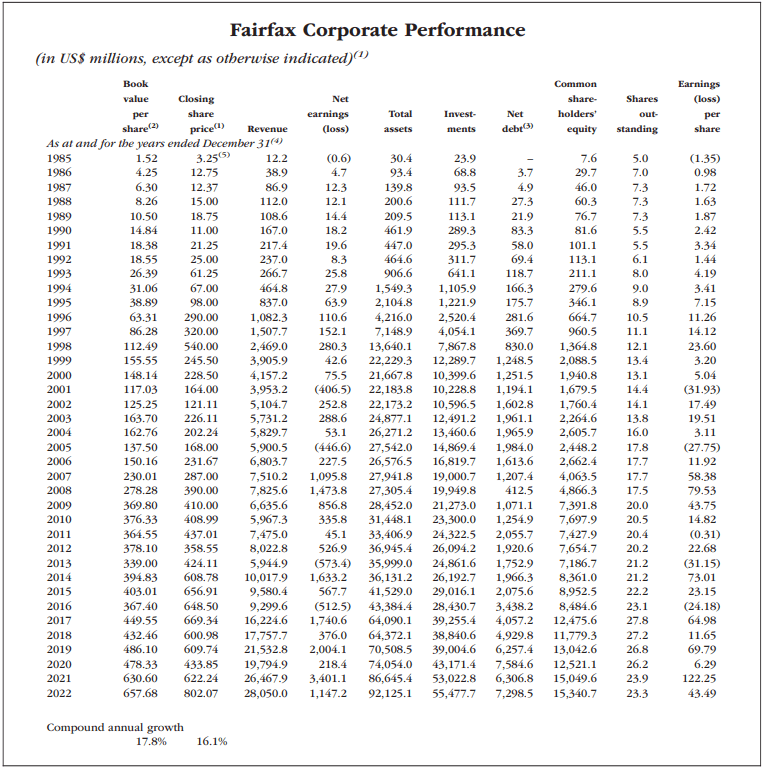

At the same time, since its inception - 38 years ago - Fairfax has grown its book value per share at an annual CAGR of 17.8%, with a target of 15%. At the same time, the share price has grown at a CAGR of about 16.1% over the same period.

{kind=link}

Seeking Alpha shows a forward dividend yield of 1.43% at the time of this writing, but dividends are far from the only type of total shareholder return. As you can see from the table above, Fairfax's management has tried to reduce the number of shares outstanding by buying them back when the market has been depressed at different periods over its nearly 40 years this was the case in 1990, 2000, and 2008. The same thing happened in 2022, when Fairfax reduced the number of shares by 2.51% year-over-year in one year, which is very good for a multi-billion dollar financial holding company. Since 2017, the total number of shares has fallen by 16% - over the same period, common shareholders' equity has increased by 23% in absolute terms and by 46% per share, according to the company's annual report. Earnings per share, while down and up, have had virtually no impact on share price performance - Fairfax stock has risen from $449 per share to $699 per share [+55.7%] since 2017.

Assuming that Fairfax can grow its book value per share by 15% by the end of FY2023 - the long-term target - and that the price-to-book ratio grows within a reasonable range and without too much deviation from historical averages, then the implied upside potential for Fairfax shares should be just over +15%:

{kind=link}

Note: The calculation is based on Fairfax shares traded in Toronto.

And if we consider that current revenue growth forecasts appear too pessimistic, then further upward revisions may be forthcoming, which should provide an additional catalyst for the stock to grow.

So when we put 2 pieces of the puzzle together - a fundamentally high-quality picture with relative cheapness - we get a pretty comfortable Buy-rated investment case here.

The Verdict

Of course, an investment in Fairfax, like any company in the insurance sector, involves certain risks. Although management is primarily focused on book value growth rather than EPS, the latter is also very important to consider. Throughout its long history, Fairfax has reported huge losses per share that it eventually recouped within a few quarters, but this usually had a significant negative impact on the stock at those moments. In addition, it's important to understand that the upside potential I come to in the previous section of this article is based on quite positive forecasts - there is a possibility that they will not come true in the end [in terms of multiples, book value growth, or both].

Despite the risks, I see Fairfax as a great compounder at a reasonable price - it's a classic GARP stock. In the past 6 years, Fairfax has achieved an impressive annual growth rate of over 13% in its book value per share. This was thanks to the company's sound capital allocation strategy, which has involved actions such as the sale of its pet insurance business (resulting in a $42/share gain on sale), share buybacks, and the potential for increased profitability in the bond portfolio due to higher interest rates. Additionally, the potential for growth from improved operations of its privately held businesses presents further opportunities to compound earnings at even faster rates. I see an upside potential of ~15% by the end of FY2023, so I rate Fairfax stock as a "Buy" at its current price levels.

Thanks for reading!

For further details see:

Fairfax Financial Holdings: A Classic GARP Stock