FFXDF - Fairfax India Holdings: Not Sure About BIAL Valuation

2023-10-19 11:29:45 ET

Summary

- Fairfax India gives exposure to investments in Indian infrastructure and industry, in particular in one of Bangalore's airports, and it's one of the most active in Asia.

- Extensive use of DCF as well as perpetual growth assumptions may be leading to the valuation gap between the company and the market.

- However, the increased prosperity of India, especially after the Ukraine war, cannot be denied.

- On balance, we see the issue as a hold, but will continue to monitor it as it provides a vehicle to get Indian exposure, which every portfolio should have.

Fairfax India ( FFXDF ) is part of the Fairfax Financial ( FRFHF ) umbrella. They have quite a few exposures, all in India, and are planning on increasing their infrastructure investments in India in particular. A large amount of their exposure is in one of Bangalore's airports, the 29th most active airport in all of Asia. We have some concerns about how the company values the holding, as well as most of the other private holdings, and think that it contributes to the low P/B ratio between 0.6-0.7x. On the other hand, we like the India exposure.

Discussion of BIAL

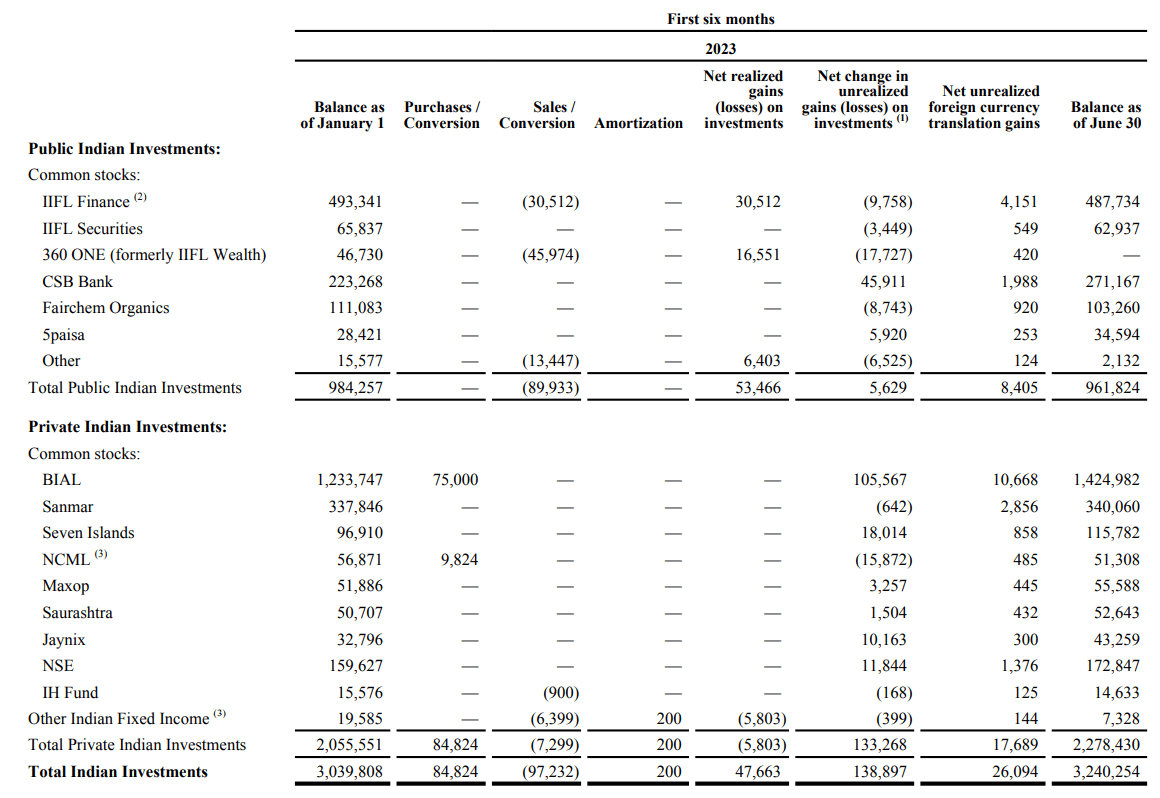

Here are its investments . Most are private:

{kind=link}

The big one is BIAL, which is one of the two airports in Bangalore. There is a precedent transaction for BIAL from September 2021. Rate expectations were also a lot lower then, so keep that in mind.

In September 2021, Fairfax India, as previously agreed, transferred 43.6% out of the 54% that it owns in BIAL to Anchorage and OMERS (the pension plan for municipal employees in the Province of Ontario, Canada) invested $129.2 million to acquire from Fairfax India an 11.5% interest on a fully diluted basis in Anchorage. This resulted in OMERS indirectly owning approximately 5% of BIAL. At that time, this transaction valued 100% of BIAL at $2.6 billion.

Fairfax India owns about half of BIAL, and that is almost exactly how their fair value figure lines up in H1 2023. There are a couple of arguments that could be posed for why the figure should be lower.

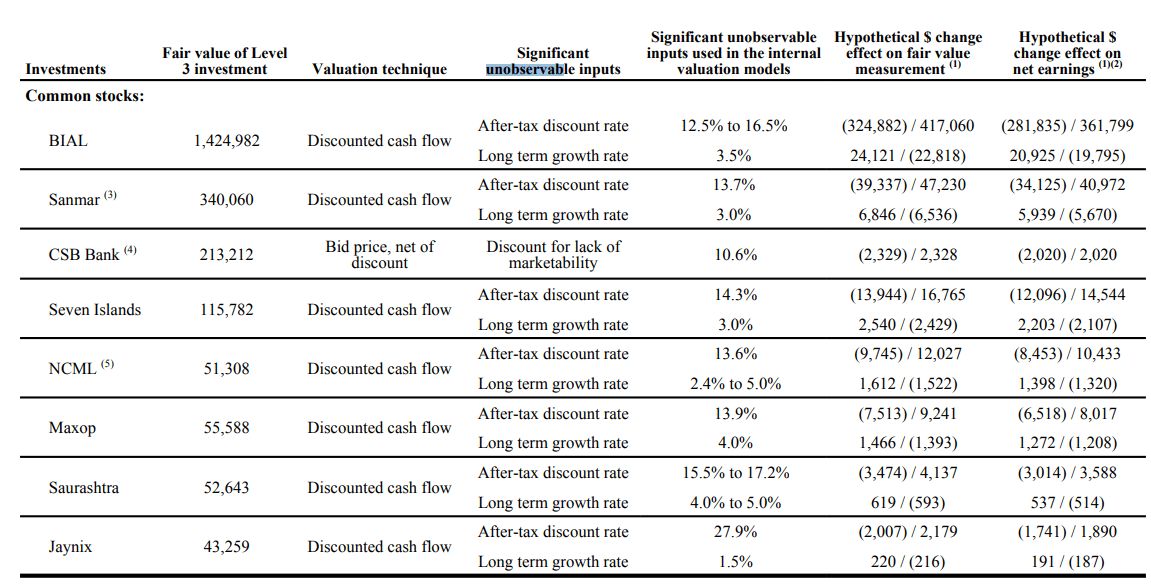

- Global rates have come up since then, and therefore so have costs of capital. With the T2 expansion plan now underway, they are also demonstrably capitally intensive. Moreover, the asset is valued on a DCF basis by the company with a substantial horizon value as the concession lasts well into the 2060s. There is a lot of rate sensitivity, and global rates have come up substantially.

{kind=link}

- Furthermore, DCF tends to overstate the value of assets due to the horizon value sensitivities in general. Multiples tend to give more conservative figures, particularly in long-dated projects like infrastructure.

Counterarguments would be:

- The correct risk-free benchmark should be RBI rates, not global rates. RBI rate changes over the last 5 years would show current rates to be not too dramatic of an increase at around 6.5% from a 5.5% in 2019.

- Furthermore, DCFs converge closer to multiples when you are not in an economy with exceptionally low rates.

We definitely think that with substantial changes in the global rate, the first counterargument fails. Taking US rates and then adding on hedging costs for the INR would be a better way to benchmark risk free rates, not using the RBI rates. This would capture the risks of the INR, with all currencies not matching the staggering rise of the Fed rates subject to higher risk now than before, with the USD being so compelling for yield at the moment. The second counterargument makes a point, but multiples are also typically discounted for countries like India, so if there is a gap in the West there would be a gap in East Asia as well.

Bottom Line

P/Bs are low. What's more is that considering the net debt position as well as NCIs, taking the values at face would render the stock highly undervalued. The NFP is around $500 million, and the total share value at around $3 billion. The current market cap is around $1.5 billion, meaning an almost $1 billion value gap.

We don't think that for a USD and CAD listed instrument with quite high profile, also in an interesting geography to allocators at this point in time, particularly due to India's geopolitical positioning, such an undervaluation is terribly likely. With almost all the private assets being valued by DCF, even commodity industry assets, and all being given 3% terminal growth rates and with the GAPs being unknown, what is likely happening is that the market's SoTP is simply more conservative than that of FFIH. The lack of change between the precedent transaction valuation and the current valuation despite changes in market environment likely also reflect why the fair value measures are better undertaken independently, which is almost always the case by the way for any financial holding company - there is nothing untoward going on here.

On the other hand, while cost of capital is up, India has also experienced a profound improvement in its geopolitical positioning. It is one of the biggest beneficiaries from the current geopolitical regime, and Western investors tend to have a very close minded view. I note the coverage from the beginning of the year of India's 'high' inflation in major financial media outlets, and that the RBI should be more aggressive in raising rates. This was an uninformed perspective, as India's inflation was highly benign, driven by accelerated outsourcing and an exceptionally good commodity cost position due to its surging imports of then highly discounted Russian oil, mostly in the $40 per barrel area. India's ability to be non-aligned has provided a lot of prosperity with the inflation, actually very much in line with emerging economies, reflective of this.

Bangalore has benefited in particular . While christening it the Silicon Valley of India might be an arguable point, what is certain is that the demographics reflect massive rent increases and recent immigration and earnings power. The male population rose meaningfully, there are outsized numbers of engineers there, and it is definitely the technology hub of India. Also, if you compare the BIAL valuation to the concession paid by Vinci ( VCISF ) for Belgrade's Nikola Tesla airport , or indeed of other regional airports with listings in Europe, BIAL's valuation is proportionate to their relative activity.

It is not clear that the difference in valuations by the company and markets cannot be in part explained by an inefficient market.

However, with a decent amount of exposure to relatively cyclical industries in addition to BIAL, and with these questions around BIAL, we will for now stay on the sidelines. However, FFIH may just be the compelling angle we were looking for to get an Indian exposure.

For further details see:

Fairfax India Holdings: Not Sure About BIAL Valuation