FAM - FAM: Beat Inflation With This 12.44% Yielding CEF

2023-05-31 08:29:50 ET

Summary

- Investors today are in desperate need of income due to the rapidly rising cost of living.

- FAM invests in sovereign bonds from around the world and applies a layer of leverage to boost the effective yield of the portfolio.

- The past year has been very difficult for bonds, but it appears that things may be improving.

- The fund has failed to cover its distributions for the past two years, but recent hikes provide some reasons to be optimistic that this situation has improved.

- The fund's shares are trading at a very attractive discount to the net asset value today.

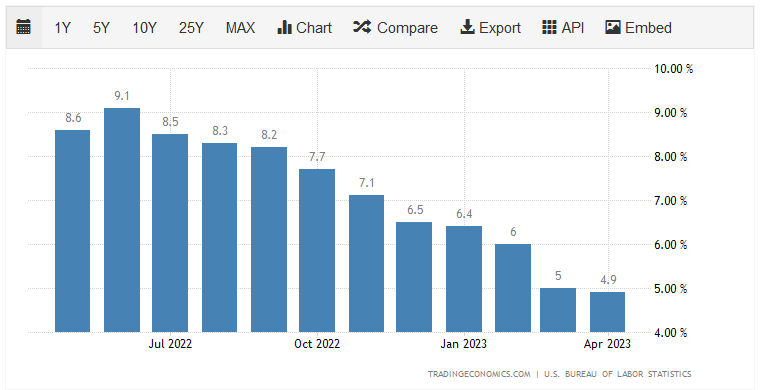

There can be little doubt that one of the biggest problems facing the average American household today is the incredibly high rate of inflation that has been aggressively ravaging the economy. This is evidenced by the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average household. As we can see here, there have only been two months out of the past year that this index was not at least 6% higher than in the prior-year month:

{kind=link}

While the index has seemingly been moderating its year-over-year growth, this was mostly due to falling energy prices. Indeed, as I pointed out recently, the average American has not likely felt any comfort from this. In fact, there still exists the very real possibility that the proposed debt ceiling agreement could make inflation worse . In short, this is a problem that has certainly not been going away and it continues to wreak havoc on many people.

Americans have been desperately trying to increase their incomes or find alternative methods to obtain the extra money that they need just to make ends meet in this environment. I have pointed this out in numerous previous articles and it hardly needs to be mentioned anymore.

As investors, we are certainly not immune to this as we have bills to pay, require food for sustenance, and need money to finance our lifestyles. Thus, most readers are likely looking for additional sources of income just like anyone else. Fortunately, we have some methods through which this can be accomplished that some other people may not possess. Most importantly, we have the ability to put our money to work for us to earn an income. One of the best ways to accomplish this is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are not very well-followed in the investment media, which is unfortunate as that makes it difficult to obtain the information that we would like to have in order to make an informed investment decision. That is a shame because these funds have a number of advantages over open-ended and exchange-traded funds, including the ability to employ certain strategies that can boost their yields well beyond that of the underlying assets or indeed anything else in the market.

In this article, we will discuss the First Trust/abrdn Global Opportunity Income Fund ( FAM ), which yields a jaw-dropping 12.44% at the current price. This is certainly an attractive yield, but unfortunately anything with a yield this high is surrounded by concerns that it may be forced to cut the payout in the near future. As such, we will want to pay special attention to its finances in our analysis. I have discussed this fund before, but many months have passed since that time so obviously a great many things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's finances. Let us investigate and see if this fund could be a good addition to a portfolio today.

About The Fund

According to the fund's webpage , the First Trust/abrdn Global Opportunity Income Fund has the stated objective of providing its investors with a high level of current income. This is hardly surprising given the bond's name and the fact that it is a bond fund. Indeed, as we can see here, the bond's portfolio currently consists entirely of bonds, with only a small amount of cash:

CEF Connect

The reason that the fund's objective is not surprising is that bonds by their nature deliver all of their returns through direct payments made to their investors. After all, an investor will purchase a bond at issuance at its face value, collect regular payments over the life of the bond, and then receive the face value when it matures. Thus, a bond does not deliver any capital gains because it has no link to the growth and prosperity of the issuing entity. Any investor that holds a bond for its entire lifetime will receive no capital gains and incur no capital losses unless the bond issuer defaults. Thus, the provision of income is the only logical objective for a bond fund.

With that said, the market price of bonds fluctuates with interest rates. It is an inverse relationship. As interest rates increase, bond prices decline, and vice versa. This is especially important today because the Federal Reserve has been increasing rates in the United States over the past year to combat the incredibly high domestic inflation rate. As we can see here, the effective federal funds rate has gone from 0.33% a year ago to 4.83% today:

{kind=link}

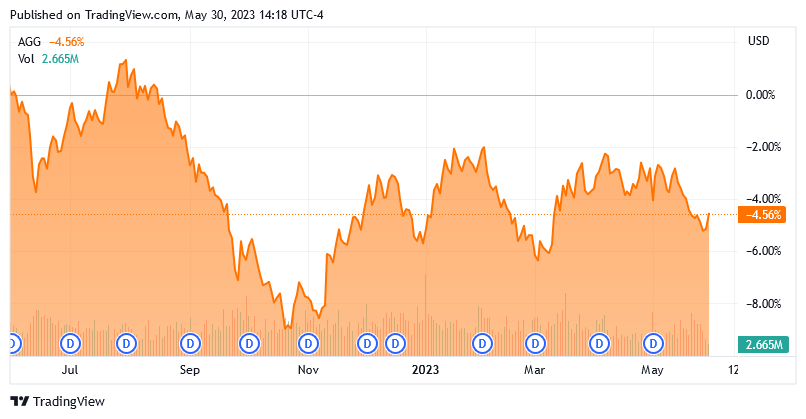

This has had a devastating effect on the market price of most bonds and bond funds. For example, the iShares Core U.S. Aggregate Bond ETF ( AGG ) is down 4.55% over the trailing twelve-month period:

{kind=link}

The reason for this is that bonds provide a regular payment to their investors that causes them to deliver a yield that is linked to the market interest rate at the time of issuance. Therefore, when interest rates rise, newly issued bonds will have a higher yield than older bonds. In such an environment, nobody will buy existing bonds because they could purchase a brand-new one with a higher yield. The older bond must therefore decline in price so that it offers the same yield-to-maturity as a brand-new bond with identical characteristics. Thus, it is possible to obtain some capital gains from bonds by trading them prior to maturity and taking advantage of these price fluctuations. In the case of bond funds, they are generally valued based on the value of their assets and these have been falling as just discussed. Thus, investors in these funds have suffered either realized or unrealized losses over the past year regardless of whether the fund has sold any bonds or not.

The First Trust/abrdn Global Opportunity Income Fund has certainly not been immune to this. Over the past year, it has declined by 11.63%:

{kind=link}

There are a few reasons why the fund's decline has been so much greater than the Bloomberg U.S. Aggregate Bond Index. One of the reasons for this is that this fund employs leverage as a way to boost its yield. We will discuss this later in this article. A second reason is that the closed-end fund does not only invest in American bonds so it is not directly comparable to the index. In fact, American bonds only comprise 16.33% of the portfolio right now:

First Trust

This is one of the lowest allocations to the United States that I have ever seen a global fund possess. That is a good thing though as most American investors are substantially over-exposed to their home country. That is amplified by the fact that most Americans also earn the majority of their incomes domestically so they will be severely impacted by any economic problems in the United States. An investor that is more diversified around the world will enjoy some insulation against problems that only affect a limited number of nations. Thus, it is important to ensure that only a small proportion of your portfolio is exposed to any individual nation to protect against this risk.

The First Trust/abrdn Global Opportunity Income Fund is still exposed to American interest rate changes despite its limited exposure to that nation, however. One of the biggest reasons for this is that American investors can obtain a higher yield by putting their money into risk-free options such as money market funds and bank savings accounts than they could a few years ago. As such, investors will demand a higher risk premium for taking on the risks of holding a global bond fund. That causes the price of this fund to decline and its yield to rise to provide that premium. In addition to this, China and Japan are the only countries in the G20 that have not raised interest rates over the past year, which are not represented in the largest ten holdings in the fund. As a result, the bonds held by the fund have generally fallen in price over the past year regardless of what country issued them. That would naturally have a negative impact on the fund's share price, as that should at least somewhat correlate to the value of its assets.

Fortunately, there may be reasons to believe that the worst may be behind us when it comes to bonds. The Federal Reserve is widely expected to stop hiking rates or institute only one more hike before pausing. The market expects that the Federal Reserve will cut rates in the second half of this year, but I find that very unlikely given the current hawkish talk from numerous central bank officials. The Federal Reserve is only one of the central banks that we need to consider with this fund, however. Most of the other central banks around the world have been less aggressive than the Federal Reserve over the past year and have not hiked rates nearly as much. The current European interest rate is 3.75%, which is much lower than the federal funds rate, for example. However, there are some signs that both the American and many foreign economies are nearing a recession. Thus, we may not see too many more rate increases from most foreign central banks, either. It is possible that the Bank of Japan will begin tightening at some point given the high inflation in that nation, but this fund does not count Japan among its largest holdings so we probably do not need to worry too much about it. In short, the worst is almost certainly over but we also will probably not see much in the way of capital gains from this fund for a while until rate cuts start being implemented and that may be a ways off.

Leverage

In the introduction to this article, I pointed out that closed-end funds such as the First Trust/abrdn Global Opportunity Income Fund have the ability to employ certain strategies that have the effect of boosting their effective yields beyond that of any of the underlying assets in the portfolio. One of these strategies is the use of leverage. In short, the fund is borrowing money and using that borrowed money to purchase sovereign bonds issued by nations all around the world. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the entire portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that would expose us to an excessive level of risk. I generally like to see a fund's leverage be under a third as a percentage of its assets for this reason. Fortunately, the First Trust/abrdn Global Opportunity Income Fund satisfies this requirement. As of the time of writing, the fund's levered assets comprise 30.83% of the portfolio. Thus, it appears that this fund is running with a pretty good balance between risk and reward.

Distribution Analysis

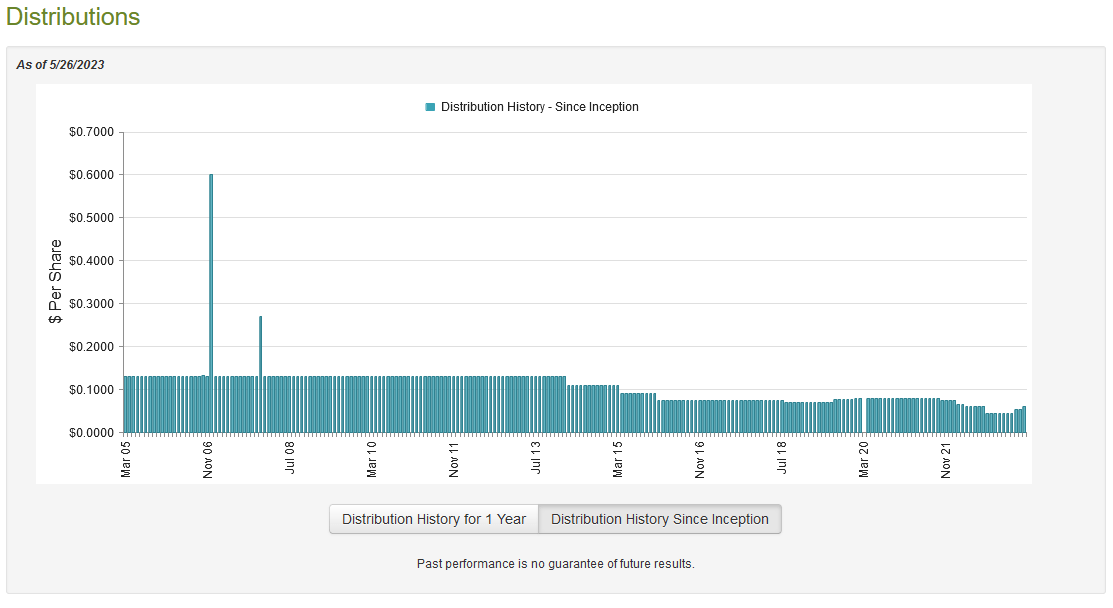

As mentioned earlier in this article, the primary objective of the First Trust/abrdn Global Opportunity Income Fund is to provide its investors with a high level of current income. In order to achieve that objective, the fund purchases sovereign bonds issued by various foreign nations. Many of these nations' bonds have historically had a substantially higher yield than U.S. Treasury securities or most bonds issued by Eurozone countries. For example, the fund's second-largest holding is a 10.00%-yielding Brazilian Treasury security. The fund then applies a layer of leverage to boost the already high-yielding portfolio above that of any of the underlying securities. The fund then aims to pay out all of its investing profits to the shareholders. As such, one might assume that this fund boasts a remarkably high yield itself. This is indeed the case, as the fund pays a monthly distribution of $0.06 per share ($0.72 per share annually), which gives it a whopping 12.44% yield at the current price. Unfortunately, the fund's distribution has varied quite a lot over the years:

{kind=link}

This is not exactly surprising since the fund's fortunes ultimately depend on a variety of things, including changing rate regimes of multiple nations and certain governments that may not respect the rights of foreign creditors. While many of these risks can be diversified away, it is uncommon to find even a domestic bond fund that does not vary its distribution over time so the fact that this is a global fund is not the cause of this variation. Regardless, its history might still prove to be a turn-off for those investors that are seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, the First Trust/abrdn Global Opportunity Fund has raised its distribution twice year-to-date so things seem to be working in its favor right now.

As is always the case, it is important that we determine how well the fund can afford its current distribution. After all, we do not want to be the victims of a distribution cut since that would reduce our incomes and almost certainly cause the fund's share price to decline.

Fortunately, we have a very recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. While this will not include information about the fund's performance over the past few months, it is much newer than the report that we had available the last time that we discussed this fund. It will also give us a very good idea of how well the fund handled the incredibly challenging conditions of 2022. During the full-year period, the First Trust/abrdn Global Opportunity Income Fund received $5,541,876 in interest from the assets in its portfolio. When combined with a small amount of income from other sources, the fund reported a total investment income of $5,545,756 during the period. It paid its expenses out of this amount, which left it with $3,378,717 available for the shareholders. As might be expected, that was nowhere close to enough to cover the $6,947,995 that the fund actually paid out in distributions over the period. At first glance, this is likely to be concerning.

However, a fund like this has other methods through which it can obtain the money that it needs to pay its distributions. For example, it might have had capital gains from fluctuations in the prices of the bonds in its portfolio. As might be expected given the challenging conditions of 2022 though, that was not the case. The fund reported net realized losses of $16,810,908 and had another $9,625,220 net unrealized losses. All in all, its assets declined by $29,989,441 after accounting for all inflows and outflows during the period. This is concerning as it clearly indicates that the fund failed to cover its distributions over the course of the year. This was also the case in 2021 when its assets under management declined by $46,322,261 in aggregate. This makes the fund's recent distribution increases puzzling as it appears that it could not afford its payouts over the past two years, so it certainly cannot afford a larger one. Hopefully, the fact that it did increase the payout twice year-to-date is a sign that things are improving for the fund.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the First Trust/abrdn Global Opportunity Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing a fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of May 26, 2023 (the most recent date for which data is available as of the time of writing), the First Trust/abrdn Global Opportunity Income Fund had a net asset value of $6.63 per share but the shares currently trade for $5.82 each. This gives the fund's shares a 12.22% discount to the net asset value at the current price. This is a very substantial discount that is in line with the 12.67% discount that the fund's shares have had on average over the past month. Thus, the price certainly appears to be acceptable today.

Conclusion

In conclusion, the First Trust/abrdn Global Opportunity Income Fund offers a very interesting way to earn a very high level of income by investing in sovereign bonds issued by nations all over the world. This is very nice for American investors that likely need to diversify their holdings away from the United States. Unfortunately, the fund failed to cover its distributions over the past two years but it has been raising its distributions recently, which provides some reasons to be optimistic that things may be improving for it. When considering the likelihood of improvements and the fact that the huge discount to net asset value allows for some margin for error, it might be worth considering adding this 12.44% yielder to a portfolio today.

For further details see:

FAM: Beat Inflation With This 12.44% Yielding CEF