AGM - Farmer Mac: Favorable Macro Tailwinds For Renewal Of The Rural Economy

2023-05-17 16:53:55 ET

Summary

- In the past year, the Federal Agricultural Mortgage Corporation has experienced better price growth than both the S&P 500 and the agricultural producer ETF.

- This reflects YoY 22.92% revenue growth, to $524.45mn, alongside a 30.90% growth in net income to $178.14mn.

- Representing high operational strength, Farmer Mac (as the company is commonly referred) has achieved $800,000 earnings per employee in 2022 alongside multi-decade CAGR of 10%.

- As agricultural productivity rises to meet insatiable global demand, Farmer Mac is poised to capture the subsequent demand for agri-finance.

- In conjunction with a general undervaluation and quality funding pipeline, this leads me to rate Farmer Mac a "buy."

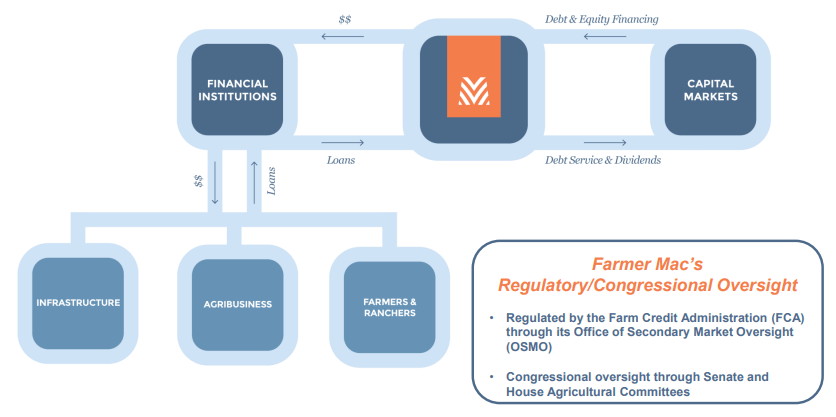

The Federal Agricultural Mortgage Corporation (AGM) is an American government-sponsored enterprise - a GSE - with a core focus on supporting the accessibility of financing for American agriculture and rural infrastructure.

Primarily operating on secondary markets, Farmer Mac is committed to innovation; for instance, the company has developed its FARM Series of securitizations, providing a direct link between capital markets and rural communities.

{kind=link}

The company's value chain thus operates at the intersection between capital markets, financial institutions, and the rural economy, providing much-needed liquidity and innovative financial instruments to respective parties.

Introduction

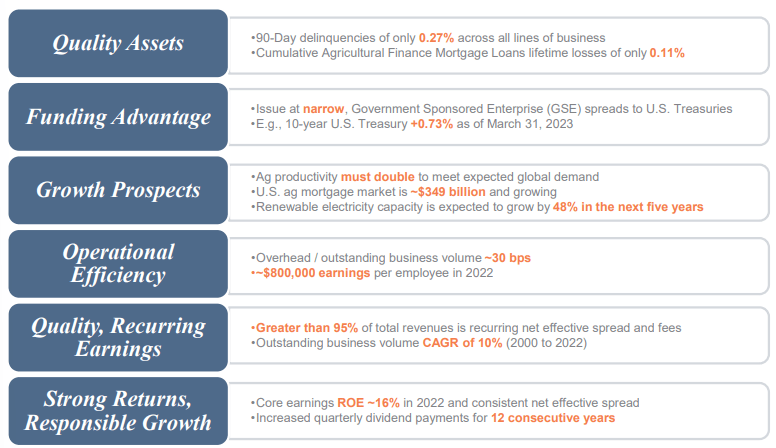

Farmer Mac employs a sixfold strategy to enable maximal, sustainable value creation; the maintenance of high-quality assets with low delinquency; a continued funding advantage as a GSE; leveraging growth prospects across the agricultural and rural renewables market; sustaining operational efficiency with high per capita productivity; stable and quality, recurring earnings; and strong returns, evidenced by core earnings ROE of ~16% in 2022 and increased dividend payments for 12 consecutive years.

{kind=link}

This fiscal and operational discipline has enabled a 22.92% increase in revenues to $571.23mn and an increase of 85.44%, to record a free cash flow ("FCF") of $809.27mn. This comes in spite of rising interest rate and the general inverse convexity of mortgage products to them.

Valuation & Financials

General Overview

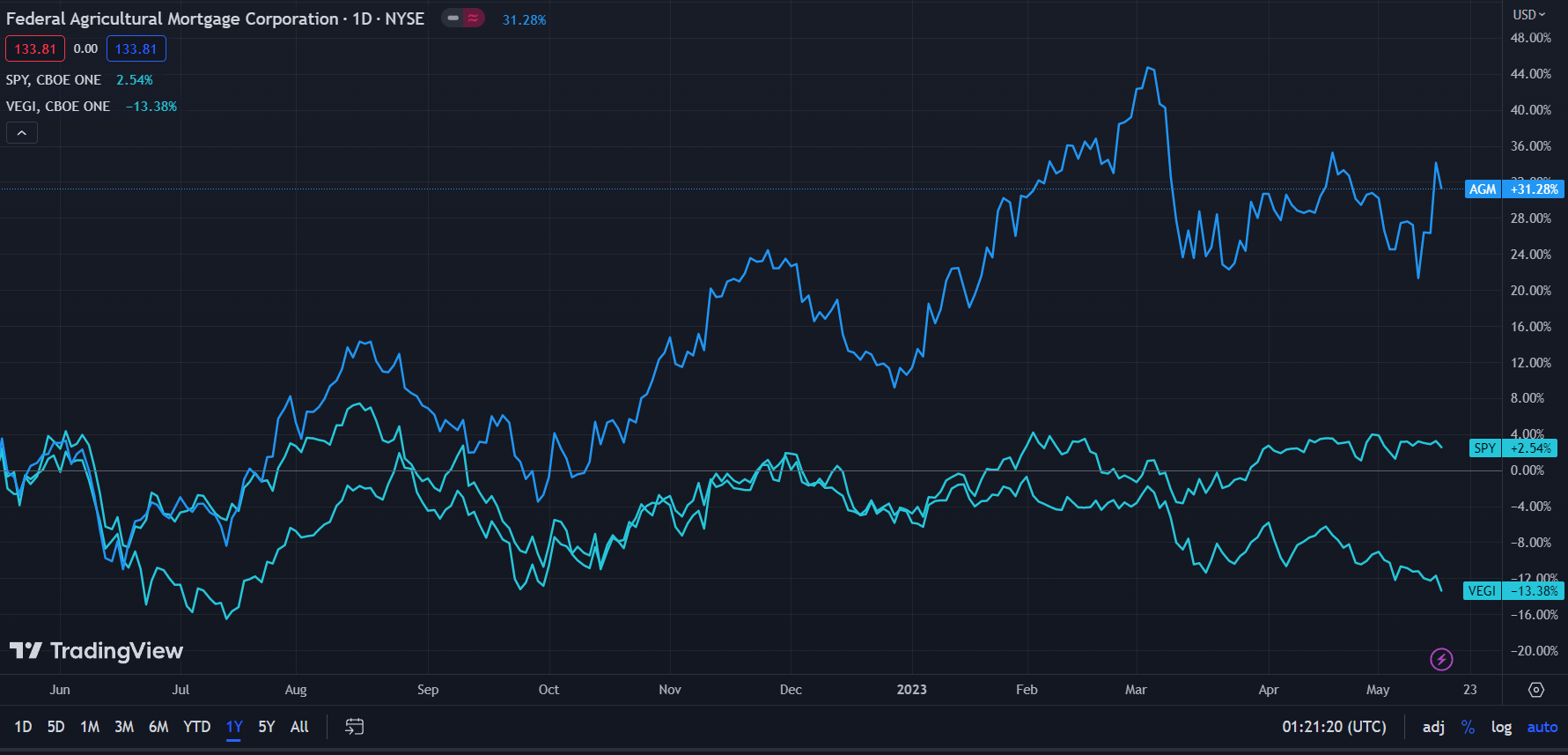

In the TTM period, Farmer Mac ( AGM ) has experienced superior share price action- up 31.28%- to both the general market, represented by the S&P500 (SP500), up 2.54%, and the iShares MSCI Agriculture Producers ETF ( VEGI ), down -13.38%.

{kind=link}

Such price movement demonstrates Farmer Mac's resilience and commitment to quality financial performance. The company's core product, agricultural mortgages and consequent securities do not demonstrate the same sensitivities to commodity price swings as agricultural producers do. Additionally, temporary global headwinds have failed to stifle the demand for agricultural mortgages, fueled by commodity supercycles and long-term agricultural needs.

Comparable Companies

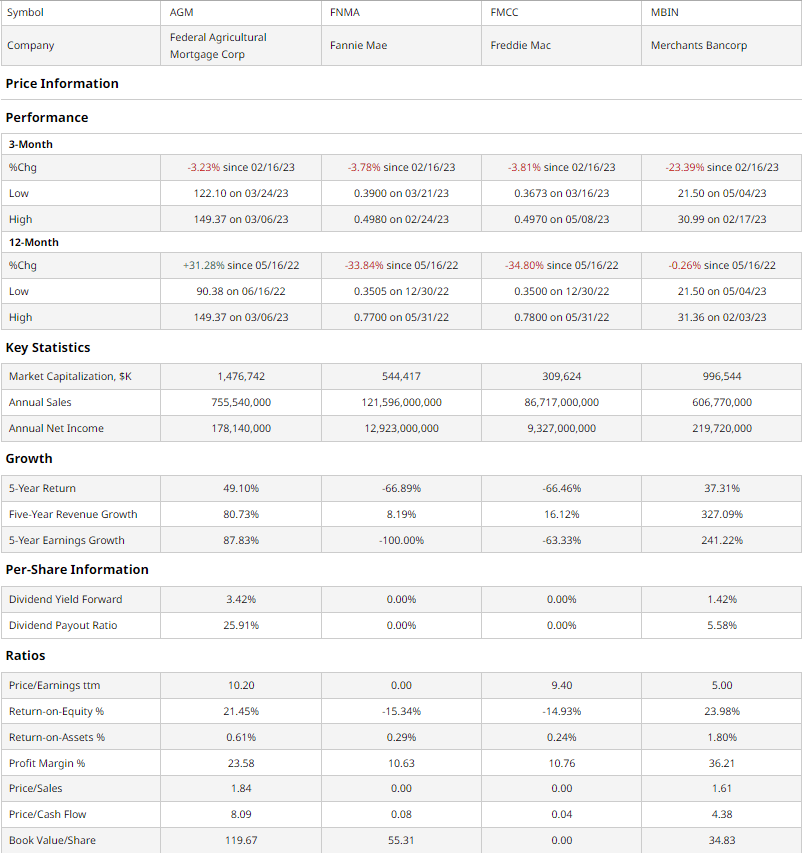

The exclusive nature of Farmer Mac as a secondary market operating, agriculture-focused mortgage provider means that they function without any direct competition. However, the firm can best be compared with other GSEs, such as retail mortgage and loan providers Fannie Mae ( FNMA ) and Freddie Mac ( FMCC ) and retail commercial mortgage firms such as Merchants Bancorp ( MBIN ).

{kind=link}

As illustrated above, Farmer Mac maintains the best quarterly and one-year price performance. Although this leads the firm to higher valuation multiples to peers, Farmer Mac still has low price/earnings compared to the market- all this without the same level of baggage other mortgage providers face from the 2008 Financial Crisis.

Even over a longer time frame, Farmer Mac sustains superior 5-year returns at 49.10%, mirroring similar growth in revenue and earnings over the time period- the second best among the chosen peer group.

Further supporting the firm's value proposition is Farmer Mac's second-best ROE, profit margin, and superior book value per share.

Valuation

According to my discounted cash flow ("DCF") analysis, at its base case, the fair value of Farmer Mac is $174.99, meaning that the stock is currently undervalued by ~24%.

Due to a relatively high debt/equity ratio, as well as potential reductions in agricultural mortgage-backed security demand due to compressed liquidity and interest rates, I assume a higher discount rate of ~10%. Similarly conservative, I anticipate revenue and subsequent net margin growth of ~5% a year, with actual CAGR for the firm, consistently ~10%.

{kind=link}

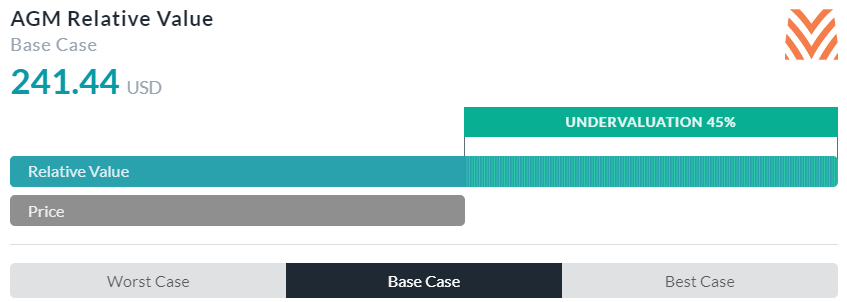

AlphaSpread's multiples-based relative value tool more than supports my thesis of undervaluation, calculating that Farmer Mac's stock is undervalued by 45%, with a fair value of $241.44.

Yet, due to the tool's inability to account for higher debt levels, the value of Farmer Mac may be skewed upwards.

Thus, applying a weighted average slanted toward my discounted cash flow, the real value of Farmer Mac should be $192.51, an undervaluation from its current price of 30%.

Combined Macro Impact of Rural Renewables & Ag Demand Spur Growth

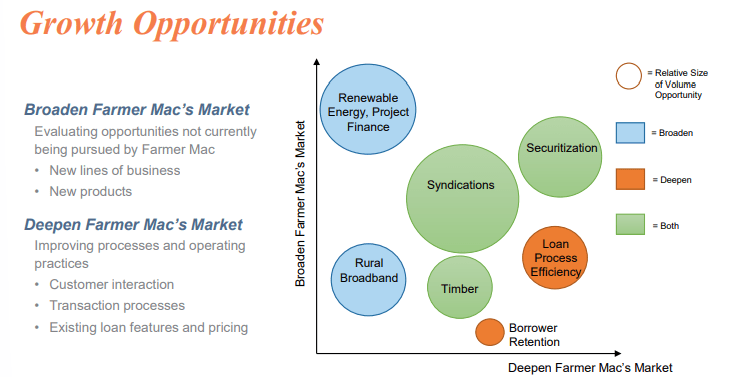

At a fundamental level, Farmer Mac aims to achieve growth through a dual mandate of broadening Farmer Mac's market- meaning new lines of business and new products- and deepening current relationships- essentially a level of vertical integration and operational efficacy generation. For instance, Farmer Mac aims to expand- or broaden- its footprint in rural infrastructure through renewable energy project finance and rural broadband projects. On the other hand, the company aims to achieve both scale and integration through increased securitization, syndication with partner firms and an expanded footprint in timber.

{kind=link}

As such, Farmer Mac successfully presents itself at the forefront of the resurgent rural economy, financing rural renewables projects and communications.

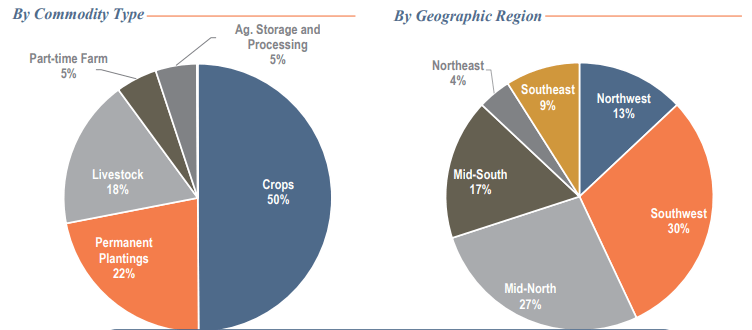

In its core businesses, understanding the record demand for agricultural production as well as the cyclicality of both the agriculture and mortgage businesses, Farmer Mac has committed itself to significant portfolio diversity. The firm splits its agricultural finance by crops, representing 50% of the loan portfolio, permanent plantings, representing 22%, livestock 18%, part-time farm, 5%, and agricultural storage and processing 5%. This extends into company geographies, with heavy diversification across U.S. regions.

{kind=link}

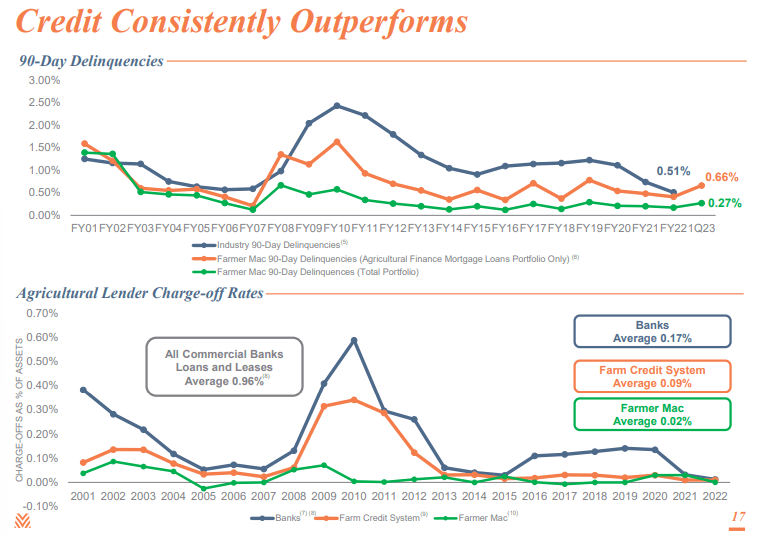

Ultimately, as Farmer Mac is a mortgage company, its credit portfolio performance deserves scrutiny. In this arena as well, the firm does well, with 90-day and lifetime delinquencies below the industry and farm credit averages.

{kind=link}

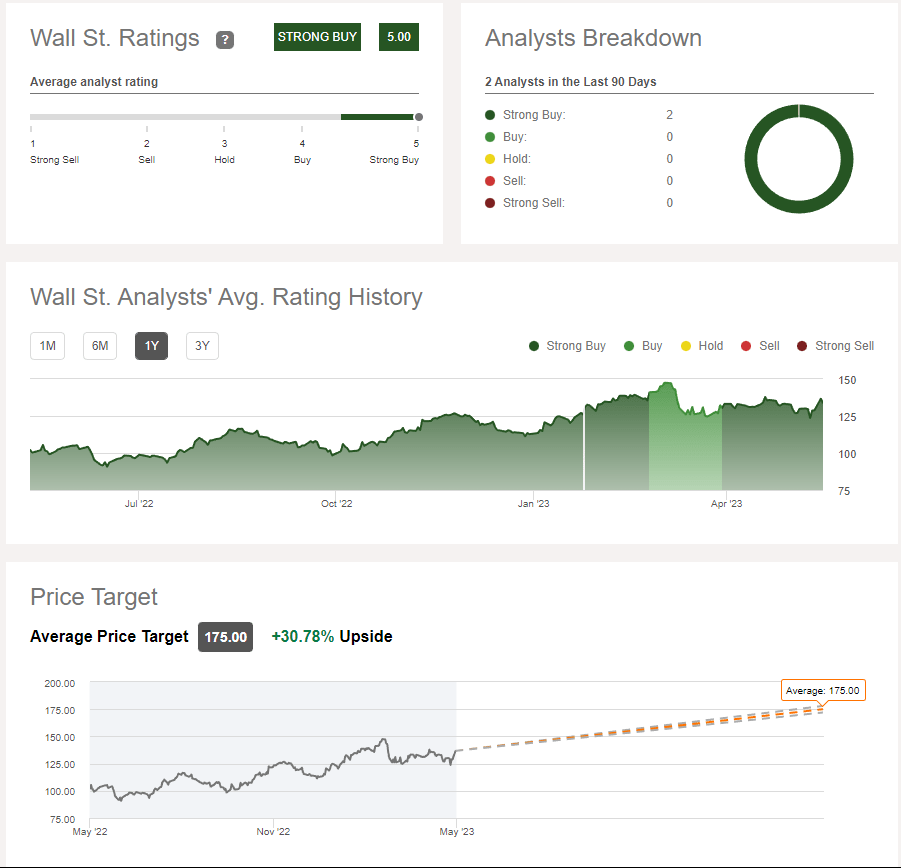

Wall Street Consensus

Analysts echo my positive view of Farmer Mac, projecting an average price increase of $175.00 in a 1Y period, representing an upside of 30.78%.

{kind=link}

Additionally, using Seeking Alpha's analyst coverage tool, analysts and quants rate Farmer Mac a "strong buy."

Risks & Challenges

Counterparty Financial Concerns

Operating on secondary markets primarily, Farmer Mac is exposed to capital markets, financial institutions, and agribusiness. As such, the firm must contend with the interests and concerns of all these stakeholders, and failures to do so may lead to compressed demand, capital supply, and reductions in the overall ability to compete and operate effectively.

Climate Change May Undermine Underlying Business

In the past year, the U.S. has recorded 18 separate billion-dollar weather disasters, with climatologists expecting increased frequency and severity of such events. Such events may lead to increased exposure to credit risk, as is the market value of many loan collateral. Not only would this harm Farmer Mac's current portfolio, but lead to increased cost of borrowing and reduced demand for Farmer Mac products.

Reductions in Market Liquidity

With continued increases in interest rates, capital markets, financial institutions, and agribusiness all face the greater cost of capital and thus may opt to reduce their positions in agriculture-backed securities. As such, the present value of Farmer Mac and its ability to fund its ventures without additional funding may be constrained.

Conclusion

In the short term, I expect Farmer Mac will revert to fair value and continue to post solid earnings.

In the long term, I project that Farmer Mac will capture maximal growth, having positioned itself as a proxy for rural economic renewal.

For further details see:

Farmer Mac: Favorable Macro Tailwinds For Renewal Of The Rural Economy