FMCB - Farmers & Merchants: Harvesting The Fruit Of Prudence

2023-05-29 04:53:00 ET

Summary

- Farmers & Merchants Bancorp had a solid start with its well-balanced revenue growth and margins.

- Its impeccable financial positioning is one of its vigorous foundations.

- Macroeconomic risks are still intense these days, but market opportunities are already on the horizon.

- Dividend payments continue with increasing payments and reasonable yields.

- A recent stock price downtrend makes it a good bargain.

Banks are in a highly cyclical and volatile market these days. Despite this, some remain unperturbed by their solid business performance. Farmers & Merchants Bancorp (FMCB) demonstrates its durability with its robust core operations. It generates increasing revenues and returns. Most importantly, it has a sound financial positioning to support its growth and expansion. Its borrowings are low and manageable, making its capital returns well-covered. With that, dividends keep rising, matched with decent yields. It is no surprise the stock price has increased over the years. But recently, it had a pullback, making it suitable for our risk appetite. Its divorced movement from the fundamentals gives it an upside potential.

Company Performance

Banks have a higher risk exposure today. With the still elevated prices and interest rates, their operations may be affected. Even Farmers & Merchants Bancorp feels the impact. Thankfully, it keeps navigating the stormy market with caution. Its robust performance reflects the fruits of its strategies and efforts.

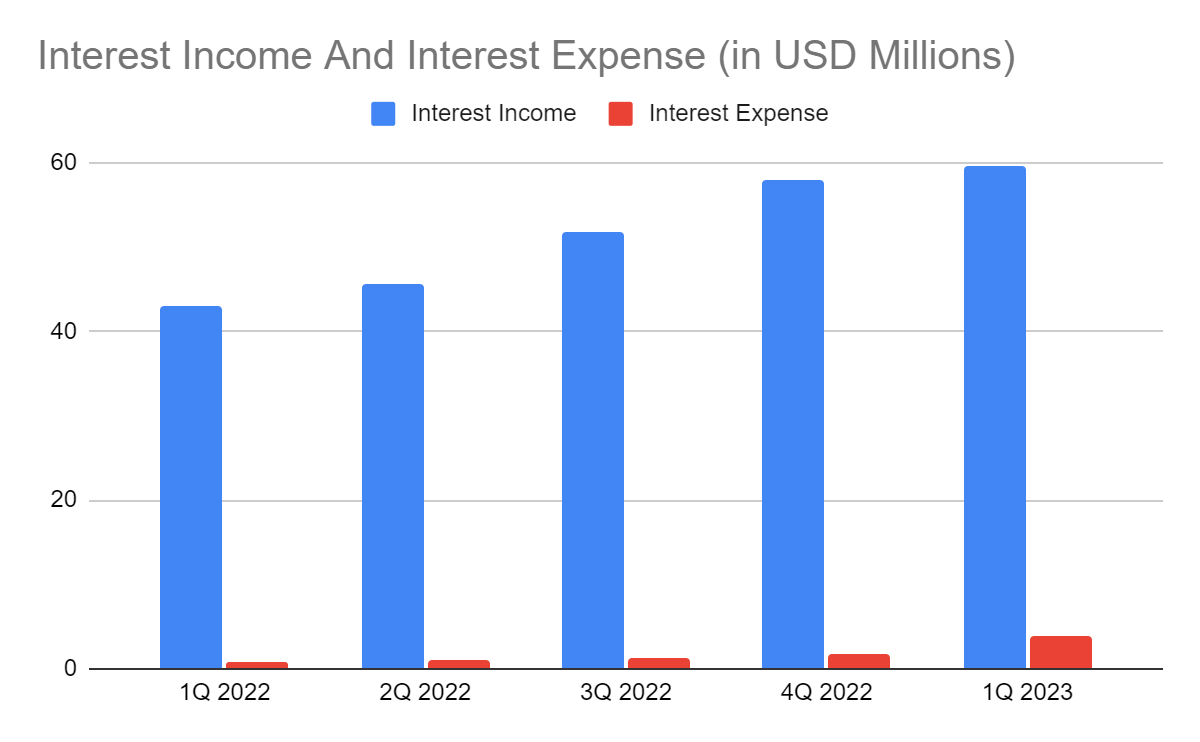

It started the year strong with promising results. Its operating revenue, in the form of interest income, remained solid with the well-managed portfolio. More specifically, loan and investment yields rose despite the rugged market. Interest income reached $59.63 million , a 38% year-over-year increase. This massive growth was impressive for its operating capacity and the current market condition. Also, it was the highest value in the past five quarters, showing a sustained increase. We can attribute this uptrend to several factors. The most common one could be the impact of inflation. When it peaked at 9.1% , interest rate hikes intensified. It was most visible in its loan portfolio since higher interest rates mean higher loan yields. Unsurprisingly, the company used it to its advantage. On top of it, the company maintained active loan repricing to stabilize loan volume and organic growth. It also helped keep the risk of defaults and delinquencies at bay. Most importantly, its loan quality continued to improve as non-performing loans remained very low. It even decreased from 0.02% in 1Q 2022 to 0.01% last quarter. As such, its interest income on loans rose by 28% .

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Likewise, the remaining revenue components showed double-digit growth. Investment securities rose by 7%, which could be attributed to their nature. Most of them were government-backed securities, such as government bonds, treasuries, and GSE securities. In essence, they are more suitable in the current market. Since they are more inflation-linked than many other securities, they have better yields and valuation hedges even in a high-interest environment. Its interest-bearing deposits comprised 0.8% of interest income in 1Q 2022. But the value increased by more than fifteen times and comprised 10% of interest income. Given all these, its interest-sensitive Balance Sheet remained solid amidst interest rate hikes.

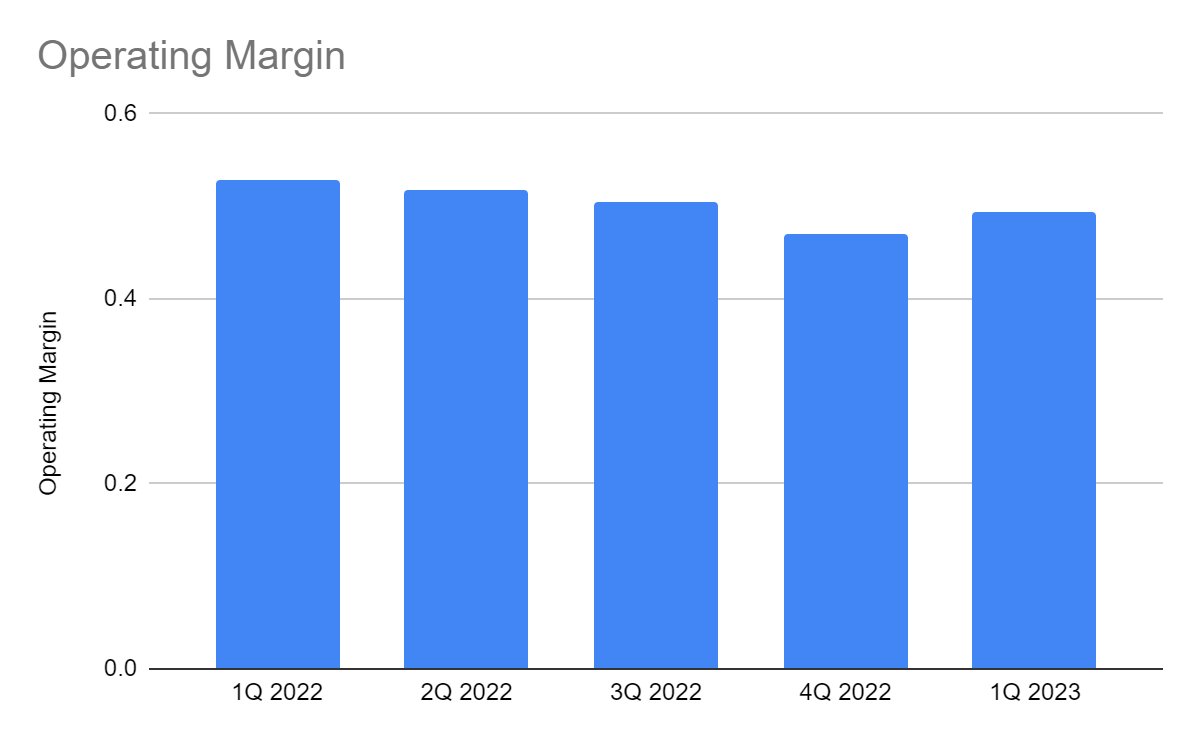

But what makes FMCB a solid company is its efficient business management. The interest expense more than quadrupled, primarily driven by deposits. Despite the decreased amount in the Balance Sheet, interest rate hikes raised deposit costs. Meanwhile, its non-interest segment stayed relatively stable. It led to high and stable margins at 49% versus 53% in 1Q 2023. It was lower than in the comparative quarter, but the actual value was higher at $29.5 million versus $22.7 million. Also, it showed a margin rebound from 47% in 4Q 2022.

Operating Margin (MarketWatch)

{kind=link}

This year, market conditions may remain almost the same as interest rate hikes continue. But it must beware of the potential recession that may impact its demand and yields. Even so, its wise portfolio management may help keep its solid performance. There may be risks, but opportunities are also on the horizon. We will discuss more of these in the following section.

Why Farmers & Merchants Bancorp May Remain Secure This Year

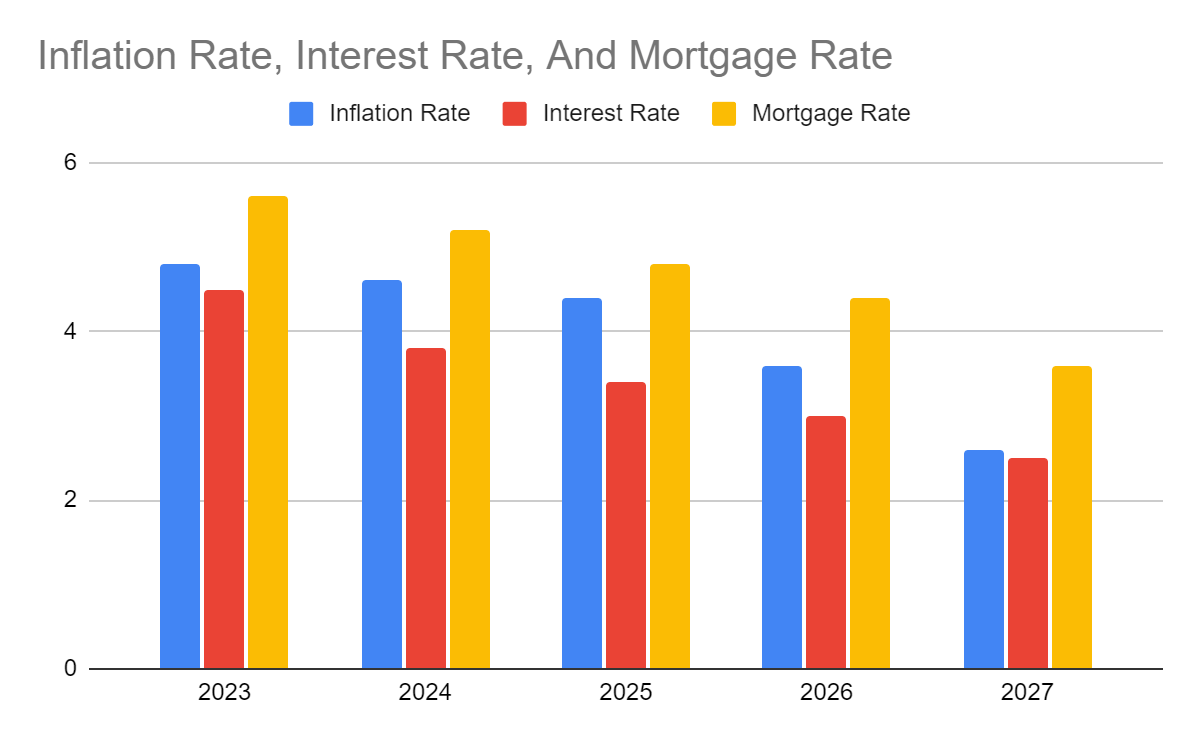

Farmers & Merchants Bancorp made sure it could withstand headwinds amidst market volatility. Yet, it did better in sustaining its impeccable growth while staying viable. It should not be too relaxed, though, as interest rates remain high. In fact, it has already reached 5% , higher than the 4.5% estimates by many analysts. And while it makes its loan and interest-bearing deposit yields higher, there can be disadvantages. One of these is that higher interest rates mean higher costs for borrowers. If it persists, FMCB may have to be more cautious of a lower loan volume. It may be more difficult to offset it through loan repricing. It may also increase the risk of defaults and delinquencies. But the effect may be more visible in deposits. In turn, interest expense may rise some more and squeeze margins. On a lighter note, interest rate hikes appear to have slowed down recently. It already decreased from 75 bps in 2022 to 25 bps. Also, The Fed hinted it may not increase rates as its efforts stay effective.

Moreover, inflation has already decreased substantially. At 4.9%, it is 46% lower than the 2022 peak. It shows that the conservative move of The Fed paid off. With that, The Fed can maintain interest rates at the current level to reduce recession woes. At the current interest rate, prices may become more stable or even decrease. The same pattern can be seen in mortgage rates, given the softer property demand. It became evident in 1Q 2023 when median the home sales price decreased by 9%. With regard to CRE loans, the bank may stay safe since a property market crash may not happen or at least not be massive. We can attribute it to increased property sales and loan demand as prices relaxed. It is consistent with the still high property shortages, intensifying from 6.5 million at the start of 2023 to 7.3 million last month. Additionally, there are no overselling and overborrowing despite the demand influx in 2021. It is way different from the events before the Great Recession. Indeed, many property builders have learned their lesson, so they do their best to prevent another bubble burst.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

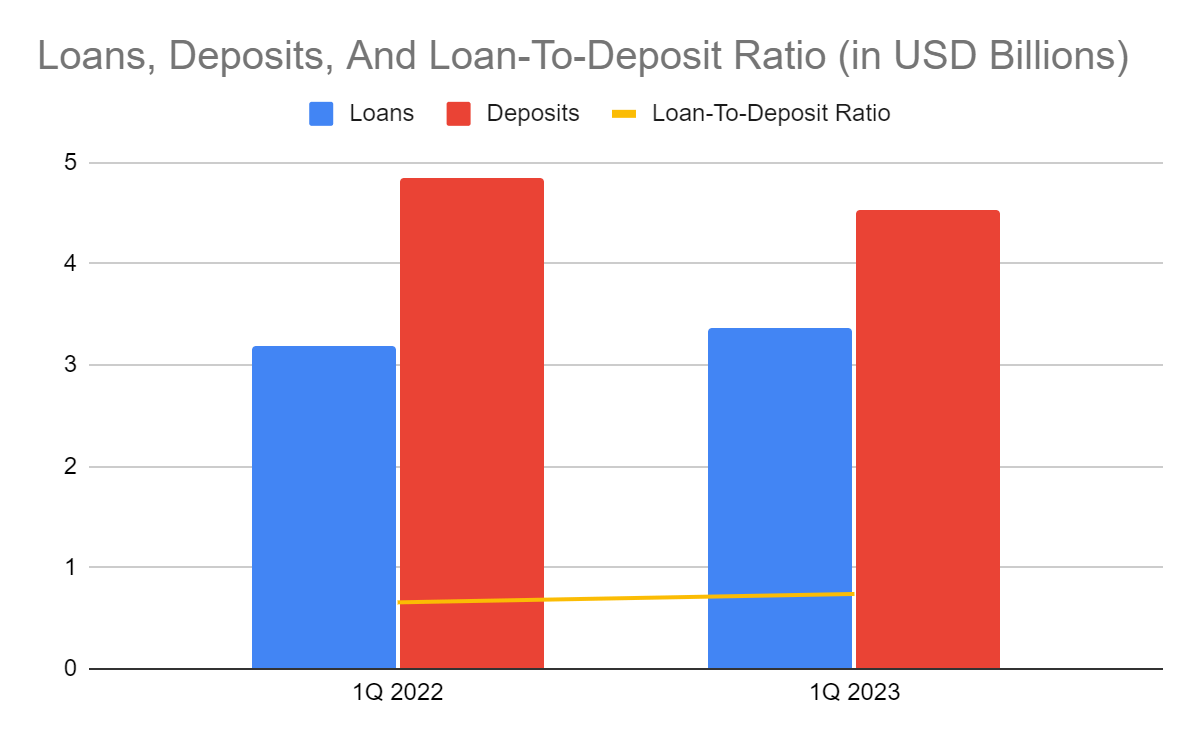

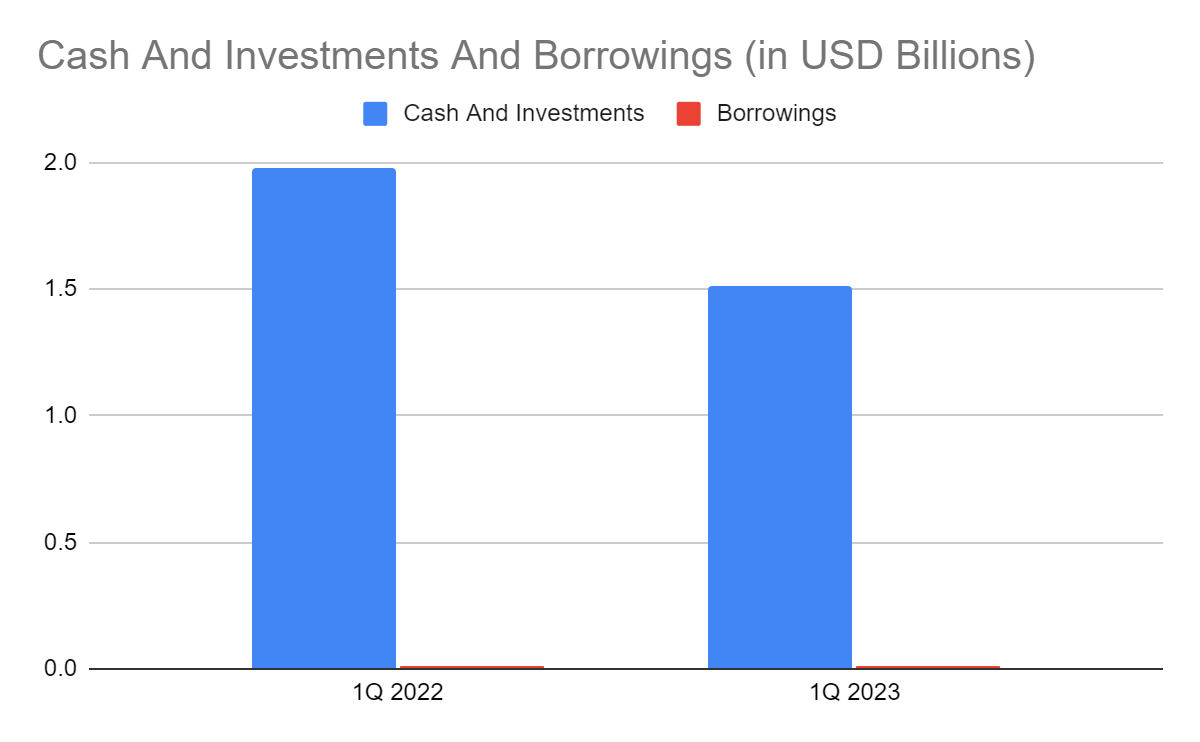

What makes Farmers & Merchants Bancorp a secure company is its solid fundamentals. These can be demonstrated by its impeccable financial positioning. Its loans and deposits are the lifeblood of the business. What is impressive is that despite its growth, the bank stays conservative. It maintains active loan repricing but avoids overlending to remain liquid. Its loan-to-deposit ratio remains low at 74%, so it has high reserves if there are defaults and delinquencies. It can also lend more since many banks have a higher ratio. Likewise, cash levels demonstrate its high capacity to cover its size, borrowings, and capital returns. They remain high to cover all borrowings and dividends even in a single payment. If we combine cash and investments, their value will comprise 29% of the total assets, making FMCB very liquid. Also, borrowings stay flat, suitable for a high-interest environment. The bank maintains the balance between growth and viability with sustainability.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch) Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

{kind=link}

{kind=link}

Stock Price Assessment

The stock price of Farmers & Merchants Bancorp has increased over the years. There was a recent pullback, but it remained high. At $975, the stock price is 2.4% higher than last year's value. Yet, it stays reasonable, making it a good bargain. The PB Ratio verifies it, given the current BVPS and PB Ratio of 665 and 1.44x. If we use the current BVPS and average PB Ratio, the target price will be $1,008.

Moreover, it is an ideal dividend stock with its consistent payments. Its yields are 1.69%, higher than the S&P 600 average of 1.65%. These are also well-covered, given the Dividend Payout Ratio of 0.26% and adequate cash levels. To assess the stock price better, we will use the DCF Model.

FCFF $32,550,000

Cash $68,280,000

Borrowings $10,310,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 762,931

Stock Price $975

Derived Value $1,024

The derived value adheres to the supposition of a potential undervaluation. There may be a 5% upside in the next 12-18 months. So, investors may buy shares at a reasonable price.

Bottomline

Farmers & Merchants Bancorp remains a very attractive bank with its robust core operations. Its stellar Balance Sheet shows its sound fundamental health. Its liquidity levels remain high, allowing it to sustain its size while covering borrowings and capital returns. Most importantly, the stock price remains undervalued with decent upside potential. The recommendation is that Farmers & Merchants Bancorp is a buy.

For further details see:

Farmers & Merchants: Harvesting The Fruit Of Prudence