SAFE - Farmland Partners: Approaching A Buy Point

Summary

- We revisit Farmland Partners after an 18-month hiatus.

- The stock took a drubbing on Q4-2022 earnings results.

- We look at the numbers and tell you why this is now on our watch-list to buy.

When we last covered Farmland Partners Inc. ( FPI ), we focused on the conversion of the preferred shares and suggested that the upside was not too great at the prevailing price point.

But the stock is still trading at a very high multiple and the dividend even if increased, will be rather tiny. But there is an opportunity here and that opportunity is if FPI shares start trading at a premium to NAV and FPI can accretively issue shares and buy more farmland. We will have to see if that happens but in the interim we are maintaining a neutral rating on the shares.

Source: Conversion

Of course that was prior to the massive inflation surge of 2022 and one would have expected FPI stock to have done well. After all, who has not heard about farmland being a hedge against inflation?

Apparently the shareholders of FPI.

Seeking Alpha

The stock peaked in the middle of 2022 and has actually underperformed the S&P 500 ETF ( SPY ). Now the entire net decline since our article, and the underperformance, mostly happened in the last 24 hours as the lower part of the screenshot shows. So what was there not to like?

Q4-2022

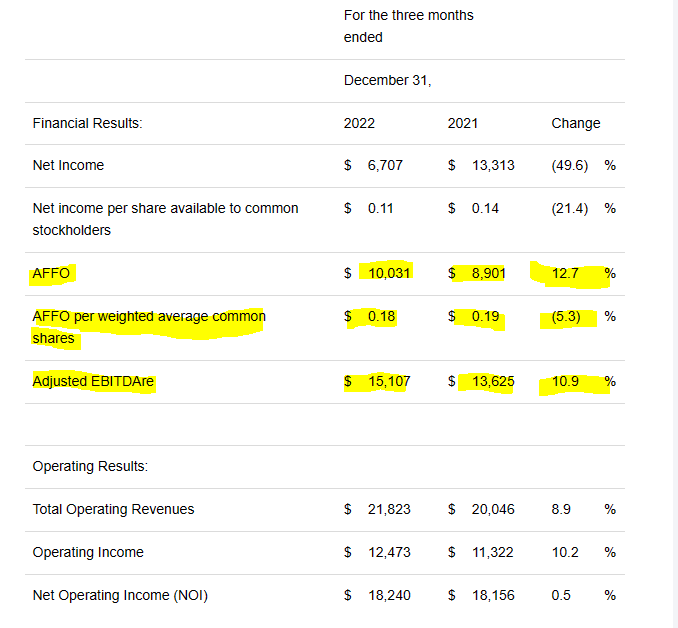

FPI's results were about in line with expectations. Revenues were up almost 9% and adjusted EBITDA rose about the same. The company noted that rent renewals were exceptionally strong.

renewed approximately 95% of row crop fixed farm rent leases expiring in 2022 at average rent increases of approximately 16%.

Source: FPI Q4-2022 Press Release

The fourth quarter also showed a solid expansion in Adjusted funds from operations (AFFO). That metric rose 12.7% in total but was down on a per share basis.

{kind=link}

We don't believe any of that should have surprised any of the market participants. FPI's preferred share conversion-related dilution has been known for some time (see vertical climb in chart below).

Additionally, FPI has sold a decent amount of shares using its ATM program.

During the year ended December 31, 2022, the Company sold 8.6 million shares of common stock at a weighted average price of $14.13 for aggregate net proceeds of $121.3 million under its “at-the-market” offering program.

Source: FPI Q4-2022 Press Release

These share issuances have been part of the deleveraging exercise and you can see the reductions in both debt levels and Series A preferred shares outstanding.

The Company had total debt outstanding of $439.5 million at December 31, 2022, compared to total debt outstanding of $513.4 million at December 31, 2021, a reduction of $73.9 million during the year ended December 31, 2022.

The company had Series A preferred units of $110.2 million outstanding after the redemption of $10.0 million of Series A preferred units during the year ended December 31, 2022.

Source: FPI Q4-2022 Press Release

So there was really nothing in the report that should have surprised anyone that followed the story. Except the guidance.

2023

The 2023 guidance can be accessed from the supplementary package on the company's website. That guidance likely created some jitters. We have highlighted what we think are the relevant portions below.

FPI Supplementary Package

The fixed farm rent was a solid boost from the 2022 levels. Offsetting that were the variable payments and to some extent even the crop sales. Total revenues are expected to be up marginally (midpoint of range). With revenues flatlining, the biggest detractor, interest costs, is what is driving the AFFO drop. The 30% decline in AFFO likely did not resonate very well with the rest of the read from the Q4-2022 press release. What also comes to the forefront is that these increases in interest expense are happening even though total debt has been meaningfully reduced.

Our Thoughts

While the drop in AFFO sounds bad, you really should not be investing in farmland and by extension in FPI, for the cash flow. At 20 cents a year or 30 cents a year or even 40 cents, the $10.50 stock price is not going to give you a reasonable cash flow. What you are investing for is the net asset value or NAV, and potential appreciation over the long haul. That's it. Farmland is a unique diversifier and a very resilient one at that. It is also one of the poorest cash flow producers. This gets even worse when you take a company buying or owning 3.0% and 3.5% cap rate properties and paying 5% and 6% interest rates on the leverage component. The math is not in your favor.

So if you accept that idea, then you have to determine if the current price and NAV make sense. Consensus estimates are around $15-$16 per share and the current price offers a decent margin of safety. We will note here that FPI has traded at big discounts to NAV for long periods and the company has also issued shares at what it considers to be a small discount to NAV. Both these facts will mean that anyone hoping for a quick move up will be disappointed.

Finally, we will note that there can be some risks to NAV. Farmland prices have always been promoted as never having a decline year over year. That is generally true. But we can see a flat price environment for many years if cap rates expand. While people are looking at the current 3.0 and 3.5% cap rates as if they are written in stone, we have indeed discoed (timeframe pun intended) with 8% cap rates in the past.

Agricultural Economic Insights

Let us show you some more math here how the trade can work poorly for you. Take a 3% cap rate farmland property and assume net operating income expands at 5% clip every year for 10 years and at the end of that 10 year period the property trades at a 5% cap rate. Your land value remains about unchanged after a decade.

Let us show you some more math. Safehold's ( SAFE ) a story which has the same asset-rich, cash-flow-poor, ring. The consensus NAV for SAFE was $60.49 14 months back .

State of REITs-Simon Bowler-Seeking Alpha

{kind=link}

Today it is at $28.87 .

State of REITs-Simon Bowler-Seeking Alpha

{kind=link}

Did you buy at $75.00 thinking you had a floor at $60.00? NAV at a given time point should not be used in isolation to make a buy or sell decision. Knowing where that NAV is headed is far more important.

Verdict

You have to have a big margin of safety when you frolic in low cap rate, ultra-long duration assets. SAFE's investors likely found that out in 2022 and FPI investors got the memo yesterday. That said, the current discount is looking modestly attractive. What is not looking attractive is the implied volatility on the stock. Generally we tend to establish positions using a defensive approach and that requires aiming for the strike we like via options. The current implied volatility is pretty low considering the massive drop that just happened. We are looking to get involved near the $8.50-$9.50 area and this is on our watchlist.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Farmland Partners: Approaching A Buy Point