FPI - Farmland Partners: Assessing If A Breakout Is At Hand

Summary

- Farmland Partners' shares have rallied up to significant resistance on the technical chart.

- Higher rents and lower costs lead to an earnings beat in Q3.

- Although not cheap, profitability of this REIT is headed in the right direction.

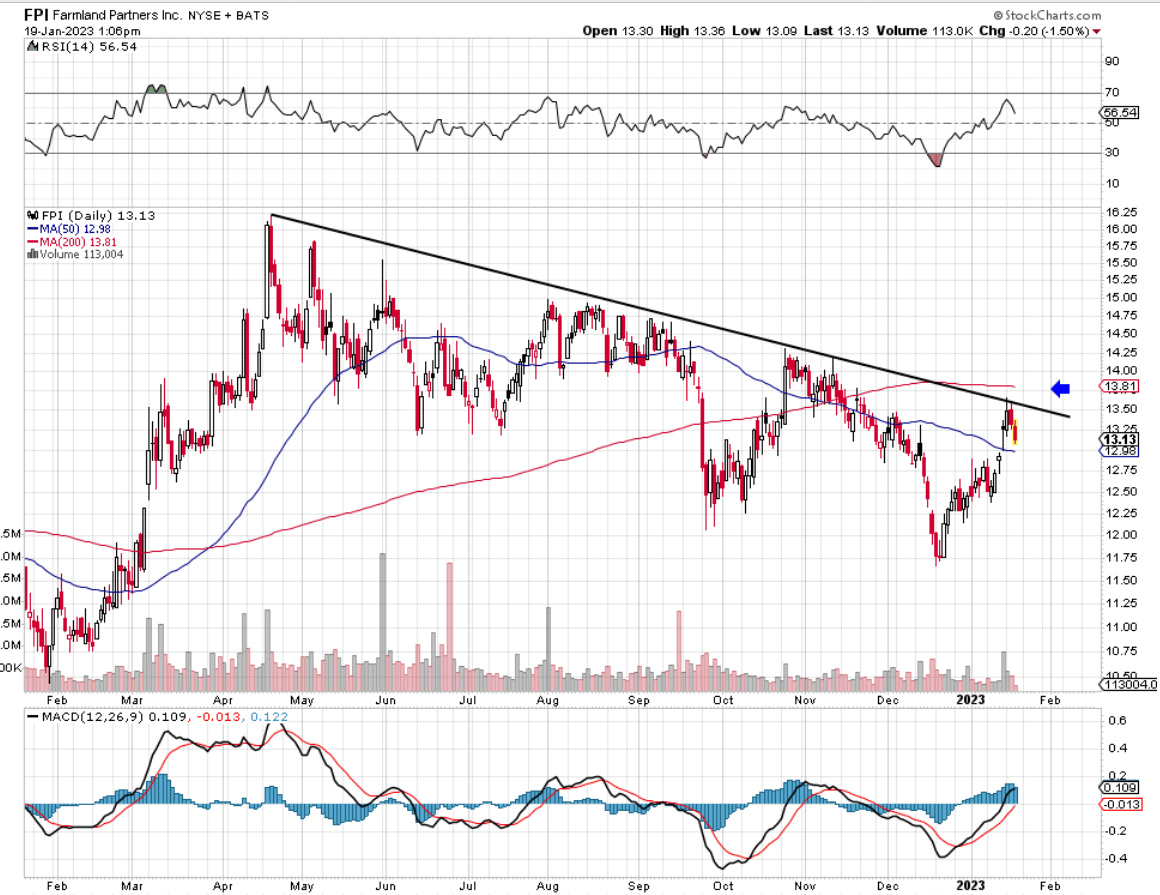

If we pull up a near-term chart of Farmland Partners Inc. ( FPI ), we can see that shares of the real estate investment trust ("REIT") are at a crossroads. We state this because if shares can source the necessary momentum to punch up above that downcycle trendline and the 200-day moving average consequently, it would stack the odds in favor of the resumption of the bullish trend that the REIT enjoyed prior to that April top last year. In fact, the bullish crossover of the REIT's OBV (On Balance Volume) line may actually be prompting this pending move.

On the latest earnings call, the former CEO spoke of FPI's total return potential and how the significant increase in the price of farmland has impacted the fund. On this point, the current CEO (Luca Fabbri) of Farmland Partners outlined how prices had increased by significant double-digit percentages in certain markets in 2021 alone, with growth following on into the current year. Therefore, given the REIT's current earnings multiple, which Farmland Partners is currently trading off, it is plain to see on the income side that earnings growth has underperformed how the REIT has grown in value over the past couple of years.

Farmland Technical Chart (StockCharts.com)

{kind=link}

We acknowledge that Farmland Partners Inc. looks very expensive across a whole host of valuation metrics, and here is where investors may find difficulty in buying any potential breakout. AFFO (adjusted funds from operations) came in at $2.5 million in Farmland's most recent third quarter, which means the trailing AFFO multiple now comes in at 35.08. Although Farmland has now reported positive AFFO numbers for three quarters running now, earnings would still have some distance to go before being in line with what the sector is currently trading at (Sector Median FFO multiple of 16.09).

Bottom Line Growth

Here, though, we again see how not only valuation influences price action, but also other key metrics such as profitability and the REIT's growth profile. Farmland's operating income came in at $4.7 million in the third quarter off total revenue of $13.1 million, giving a Q3 operating margin of 36%, just below the trailing average of roughly 40%. Furthermore, these encouraging trends have been dropping to the bottom line (Trailing net profit margin of 30% approx) due to lower legal and accounting costs as well as lower distributions on preferred stock in 2023 thus far. Higher margins invariably mean better property-level profitability. For one, the market on a potential breakout may be pricing in the continuation of this trend.

Improving Debt Metrics

Then you have the declining debt load on the balance sheet , where the total debt came in at $410 million at the end of Farmland's most recent third quarter. Total debt in the REIT has decreased by roughly 16% since the end of the preceding fiscal year, which is encouraging. In fact, if we look at Farmland's current equity (Share-price of $13.33 multiplied by shares outstanding of 54.5 million), we get total shareholder equity of $726.5 million. So if we look at Farmland's debt to the market-capitalization ratio (which is a solid read on whether the REIT is overextended or not), we divide the REIT's debt of $410 million by the sum of its debt & equity ($1.136 billion). Suffice it to say, the ratio turns out to be just above 36%, which is attractive and well down from the 46% ratio we witnessed at the end of fiscal 2021 and also well below the 48% average ratio across the sector in general. Again, as seen above, Farmland's trends with respect to its equity and debt continue to be favorable.

High Capital Costs

The issue, though, for sustained gains in Farmland Partners Inc. will be how well the REIT buys in the upcoming quarters. Land prices have increased significantly in recent months, and borrowing costs continue to increase. Therefore, to this point, management demonstrated some caution regarding future acquisitions for the cost of capital motives. However, there is still plenty of room to grow organically on the back end with respect to rents following asset prices higher. Furthermore, the Murray Wise acquisition was an excellent move by management, with financial results exceeding expectations to date, so plowing more money in here to increase returns would also be a viable option.

Conclusion

Therefore, to sum up, it will be interesting to see if Farmland Partners Inc. can break out above overhead resistance and initiate a fresh bull run. Although the valuations seem frothy, growing revenues (especially on the fixed side) and a stronger balance sheet are definite tailwinds for this REIT. Let's see what Q4 brings. We look forward to continued coverage.

For further details see:

Farmland Partners: Assessing If A Breakout Is At Hand