FPI - Farmland Partners: Investment Thesis Stands Buy The Assets Not The Cashflows

Summary

- Farmland Partners Inc. stock dropped strongly after issuing 2023 AFFO guidance below estimates.

- This was mostly driven by the increased pressure from rising rates, which I correctly highlighted in my prior article. But poor 2023 profitability in specialty crops was an added negative.

- The stock now trades at a sizeable discount to NAV.

- As I see an investment in Farmland Partners mainly as a way to get exposure to the asset class "U.S. farmland" as a great addition to a well diversified portfolio, I am more intrigued by the increased discount to NAV than worried by the reduced cash flow profile.

Introduction

In this article I will assess recent results and guidance for 2023 and what those mean for the Farmland Partners Inc. (FPI) investment case. I will also provide an update on my valuation and return expectations.

I view Farmland Partners as an asset play to gain exposure to U.S. farmland. I explained my reasoning of why I believe farmland to be a good addition from a portfolio perspective in this article . In the piece titled " Buy FPI for its assets, not its cashflow, " I gave an overview of the company and my thinking about investing in it. In this article, I will assume some familiarity with the company and its history.

FY 2022 results and 2023 guidance

FPI reported a good FY 2022 that was in line with expectations. As expected, they showed a much increased adjusted funds from operations ("AFFO") thanks to lower legal costs and their past rent increases.

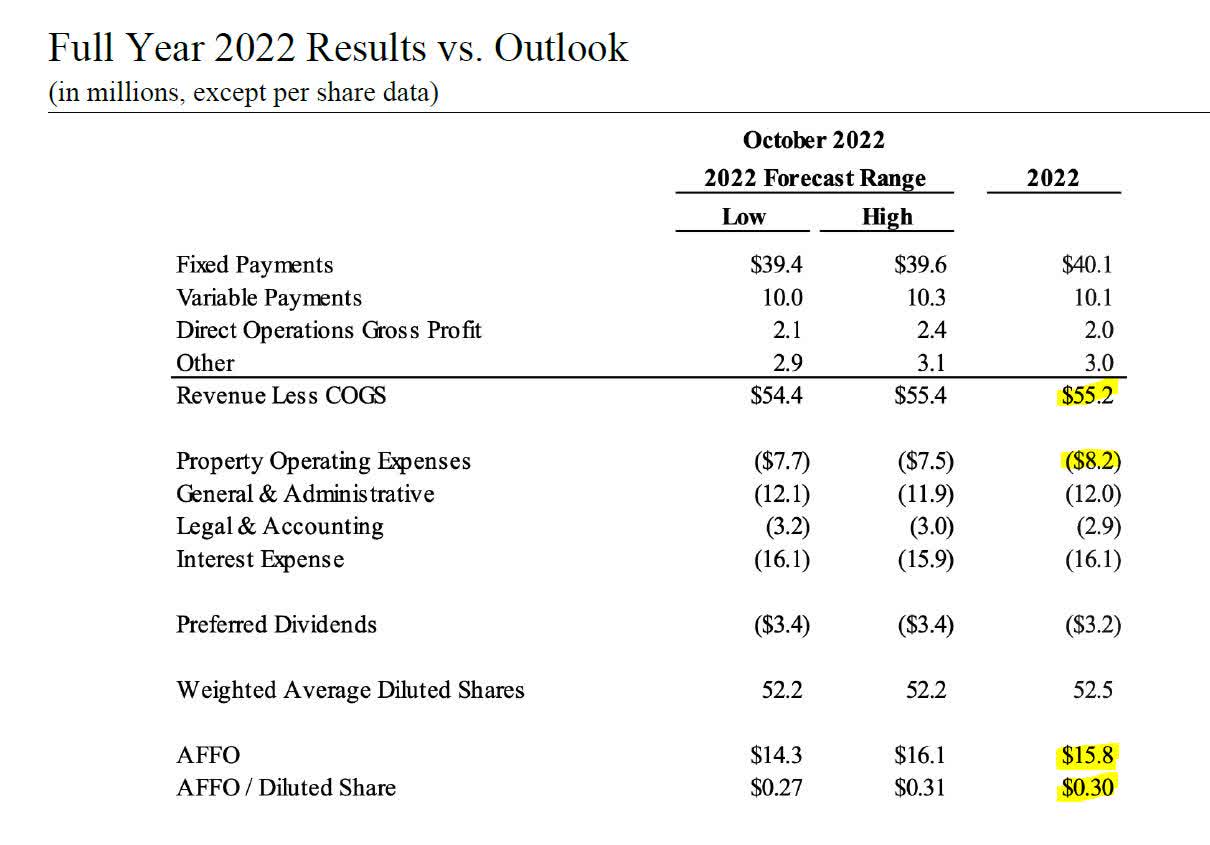

FY 2022 results vs. guidance (FPI Q4-2022 supplementary package)

{kind=link}

Both revenue as well as unfortunately operating costs came in high, leading to overall results at the upper end of guidance. The most important data point was the rent renewal, which happens mostly in Q4. They achieved a 16% growth in rents for those row crop farms that were up for renewal. That is solid and in line with prior guidance. Overall, 2022 results were good as expected and guided. And that is that - no need to dwell too much on it as the big driver for the shares collapse was their forward guidance.

FPI 2023 guidance (FPI Q4-2022 supplemental package)

As we can see, the actual business of renting farmland does well. Fixed farm rent continues to go up and they get additional income from renewable energy use on their land. As non-financial costs go down this should lead to high growth in operating income. However, they do guide downwards and not upwards for AFFO. Why is that?

Firstly, their direct operations suffer in 2023. This is their specialty crops, mostly in California. Last year's drought together with high worldwide supply impacts 2023 return expectations. While the drought situation has somewhat relaxed thanks to a wet winter, this will only show up in 2024. Taken together, variable payment, crop sales and crop insurance are all down to cancel out the positive growth from the fixed rents, leading to overall stable revenue at around $61m. They said this about the situation on their conference call :

When we turn to the specialty crop side, what we are experiencing and it's mixed up and complicated unraveled because of all the specialty crops with the exception of citrus, the most of the revenue or a large portion of the revenue shows up in the next year in these long marketing tails. So the negative impact of the drought is really having a 2023 impact equal to or greater than the drought impact during the 2022 financial year. So the '23 year gets hurt by the '22 drought.

I was surprised by the size of the negative impact of 2022's drought on their direct operations in 2023. There is a time lag for when you sell the produce (they only recognize revenue under GAAP when they have certainty about the amounts), but it seems they were also handed back a nuts farm increasing their exposure. On the other hand, citrus farms were leased out again, which makes it a bit difficult to really pinpoint how big the impact of the poor environment really is vs. changes of the farms involved. I am not too keen on them doing this part of the business as I want them to be owning land and not be involved in the actual farming business. That said, given the severe drought last year this should at least put in a bottom when it comes to low profitability in the direct business.

Secondly, on the cost side, higher interest rates show up. The $4-5m additional interest costs more than cancel out any improvement in the other cost items, leading to overall higher costs. Together with just stable revenue this leads to an overall fall in AFFO.

"Subsequent to December 31, 2022, the Company reset rates on $109.4 million of the $174.1 million with interest rate resets in 2023: MetLife Term Loan #5 repriced to 5.63%, effective January 12, 2023; MetLife #6 repriced to 5.55%, effective February 14, 2023; MetLife Term Loan #1 and 4 repriced to 5.55%, effective March 29, 2023." (FPI Q4/23 supplementary package).

Higher interest rates should not have been a surprise to anyone but clearly people still don't do their homework. I wrote an article last year where I highlighted the upcoming resets for 2023 and the sizable increase in costs in store for FPI:

Overall, it seems likely that we get several millions of additional annual interest costs

I still see downside risk to the interest cost guidance as I expect the Fed to be tougher than market expects right now which should lead to higher interest costs during 2023 thanks to the variable part of their exposure and the loans that reprice only in October. From 2024 onwards, however, things should look better. There are only relatively small amounts up for reset and should the Fed start cutting rates that provides relieve on the variable payments as well as prepayment optionality on their recently reset loans. They can now prepay up to 40% of face value annually without a penalty on their Met loans.

To sum it up: The aftermath of the Californian drought and supply chain disruptions from 2022 shows up in 2023 results and cancels out the revenue improvements otherwise achieved. Higher interest rates dominate the cost picture leading to lower AFFO. That said, 2023 should be a low point in that respect as the direct business is expected to recover, one set of repricing rents for row crop farms is still outstanding for Q4/23 and rates might retreat back lower in 2024.

FPI caught between a rock and a hard place

Until 2021, FPI was handicapped by the fallout from the short attack on them and sold at massive discounts to the underlying land values. This meant they could not issue equity to buy more farmland and increase in size. Which explains why FPI is still subscale in my view. Unfortunately, I believe we are in for a repeat performance. I do not see FPI trading up to NAV anytime soon. They managed to do so shortly last year with a very strong fundamental backdrop but those tailwinds won't be here this time around. Add to that the fact, that debt is prohibitively expensive right now for them the math simply does not work for new acquisitions. In Q4 last year, they had to resort to buying some Deere dealership to make a deal work. Not exactly what I want to see in a farmland real estate investment trust ("REIT").

Now, what about shrinking yourself to nirvana? During their conference call , CEO Paul Pittman appeared not happy about the stock price performance. He blamed it mostly on the poor guidance from their direct business specialty crop exposure and not on their messed up interest rate handling. Accordingly, his way of dealing with it was to hint about selling specialty crop exposure and focus more on row crop:

So no one should take from our comments that we are going to exit specialty crop, but we're certainly considering it.

[...]

The specialty crop side, because of the nature of the way those leases are, and we get these big swings. And I think it's frankly hurting us, and it's hurting the price of those stocks. So we've got to figure out how to have that stop happening, might be joint ventures, might be dispositions, might be some other way of structuring our leases. There's a lot of choices. But we've got to get that problem to frankly go away.

That way he could reduce the volatility in earnings. He also hinted that they might not use all proceeds for debt reduction but might also consider buybacks.

I think we're pretty dedicated to trimming parts of the portfolio that where we can get a profit and redeploy that capital into debt reduction or frankly into stock buybacks given what's happened this morning.

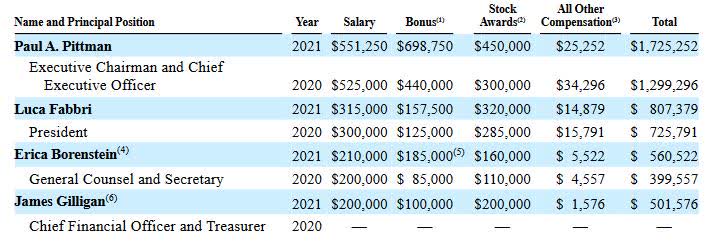

How does the math for this work? Basically, the opposite of issuing stock at a premium to NAV and then buying farms (I showed a worked example of how that works here ). Now they sell farms at NAV and buy back stock at a discount to NAV (after repaying the associated debt) and thus increase their NAV/share. Given the CEO's comments, it seems he wants to focus on the specialty crop side of things but they want to keep their best farms as those do not come to the market very often. This means he is looking to sell those farms with a fairly high cap rate and good cash generation. And while this strategy should increase NAV/share, it would reduce the cash generated to cover the fixed cost base at FPI. Therefore, the high cost ratio of FPI should put some limits to that strategy. Top management alone earned nearly $3.6m in 2021 plus over $400k for the board of directors:

FPI top 4 management compensation ((FPI))

{kind=link}

Those two expense items already account for 1/3 of total G&A costs. Overall the non-financial cost ratio is already north of 20% and will likely only increase if they shrink their business by selling the most cash generative farms. If they want to keep their dividend funded then that would limit their ability to sell cash generative farms. Personally, I would not mind them reducing their dividend (while keeping the REIT status) and increasing NAV/share by being more aggressive there as I believe some pruning of the portfolio is in order. I also would like it if they try to reduce the direct operations part by selling California-based, drought-exposed farms (one wet winter does not change the overall troubling picture). Cap rates on sale might not be as stellar as for top notch row crop farms but from a portfolio perspective of what one gets when investing in FPI I believe this is a good move. I agree with them keeping their best assets even if it hurts cash flow a bit. Eventually, FPI might end up with a higher quality more resilient portfolio. As I view FPI mostly as an asset play I like that outlook.

FPI also has some other options to increase value over the next few years. They might benefit from more activity via their brokerage operation, they could increase the solar and wind installations on their land and hopefully successfully lower their interest cost from 2024 onwards. Unfortunately, 2022 was the likely peak in profitability for the farming sector which means rent increases will be harder to get from 2024 onwards and we might even see some downward adjustments as the 2021 rents come up for renewal.

All put together, it seems that FPI is once again strategically handicapped for the next years, unlikely to grow to scale. It needs to sort through some issues to eventually position themselves favorably for the following up-cycle whenever that will come around. A shame.

Farmland Partners investment case

What does it mean for the investment case? In my initiation piece , I outlined the current scenario as the major risk facing FPI:

At $500m of debt, just one percentage point of higher interest cost would mean $5m more in interest that is not available to shareholders.

Given that they had only $51m in revenue and less than $9m in AFFO, this could lead to some nasty surprises on AFFO. Furthermore, if annual row crop farmland yields 3-4% in cash rents, we might soon have a situation where using leverage will actually have a detrimental effect on cashflows left over for shareholders (given that cost of debt is already close to 3% for FPI). This might very well counteract the increased operational efficiency from increasing rents and a larger asset base. Which is exactly why I view FPI as an asset play but not really as an investment based primarily on cashflows, because I fear they might be more under pressure going forward than analysts might assume.

With debt resetting at 5.6% and possibly more later this year, we are now pretty much where I described we might end up. Luckily, FPI also de-levered sizably by selling stock close to NAV, rental increases came through as expected and land prices increased further. Where does it leave us in terms of the investment case for FPI?

Firstly, I think the AFFO guidance which includes updated higher interest costs and a poor year for the direct business shows that the business model is sustainable. It does not bleed cash and there is no need for forced selling or highly dilutive capital raising. Those two things can often derail an asset based investment case. Therefore, fundamentally, the basic investment thesis of getting exposure to U.S. farmland value appreciation via FPI is still valid.

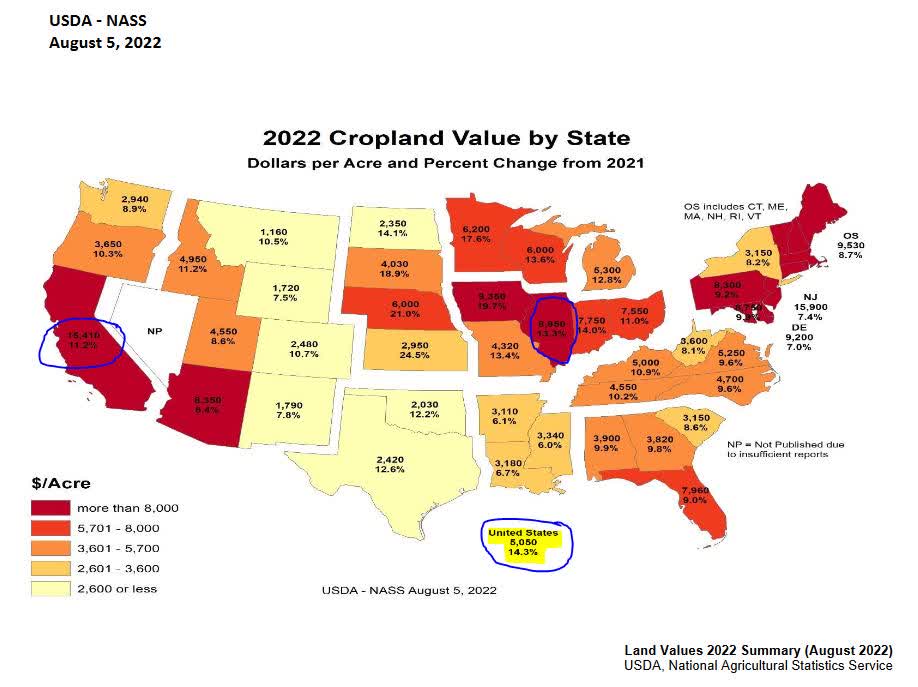

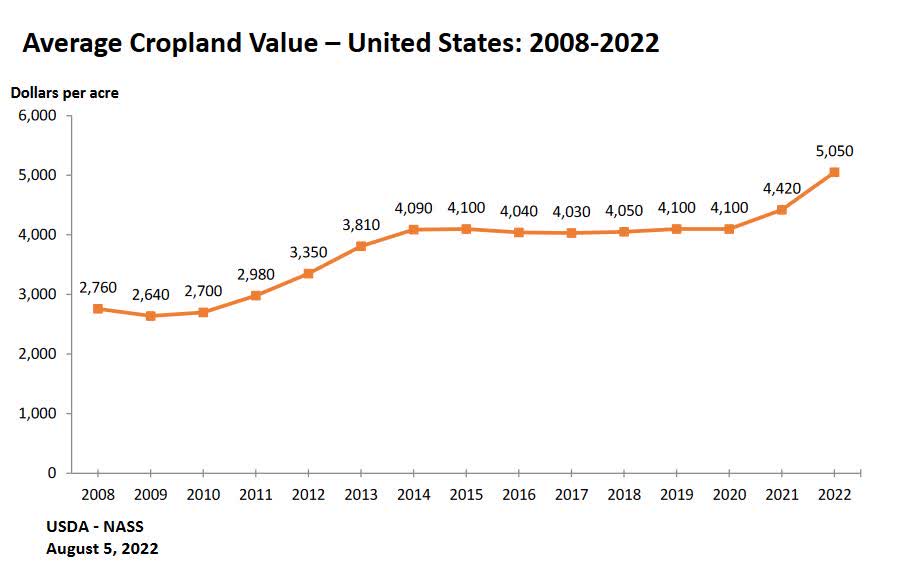

Obviously, the main issue when investing in FPI is what one thinks about the outlook for US farmland value appreciation. For 2022 the U.S. Department of Agriculture ((USDA)) showed increases in cropland prices of 14.3%.

{kind=link}

This is based on June 2022 surveys. As one can see, price increases for FPI's main exposures Illinois and California were less strong but still solidly double digit. Since then more than half a year has already passed. How have prices since then developed? The Chicago Fed had prices in Illinois increase by 5% in Q3 vs. Q2 and sequentially flat in Q4 . Overall this leads me to calculate a current NAV per share of roughly $16 for FPI.

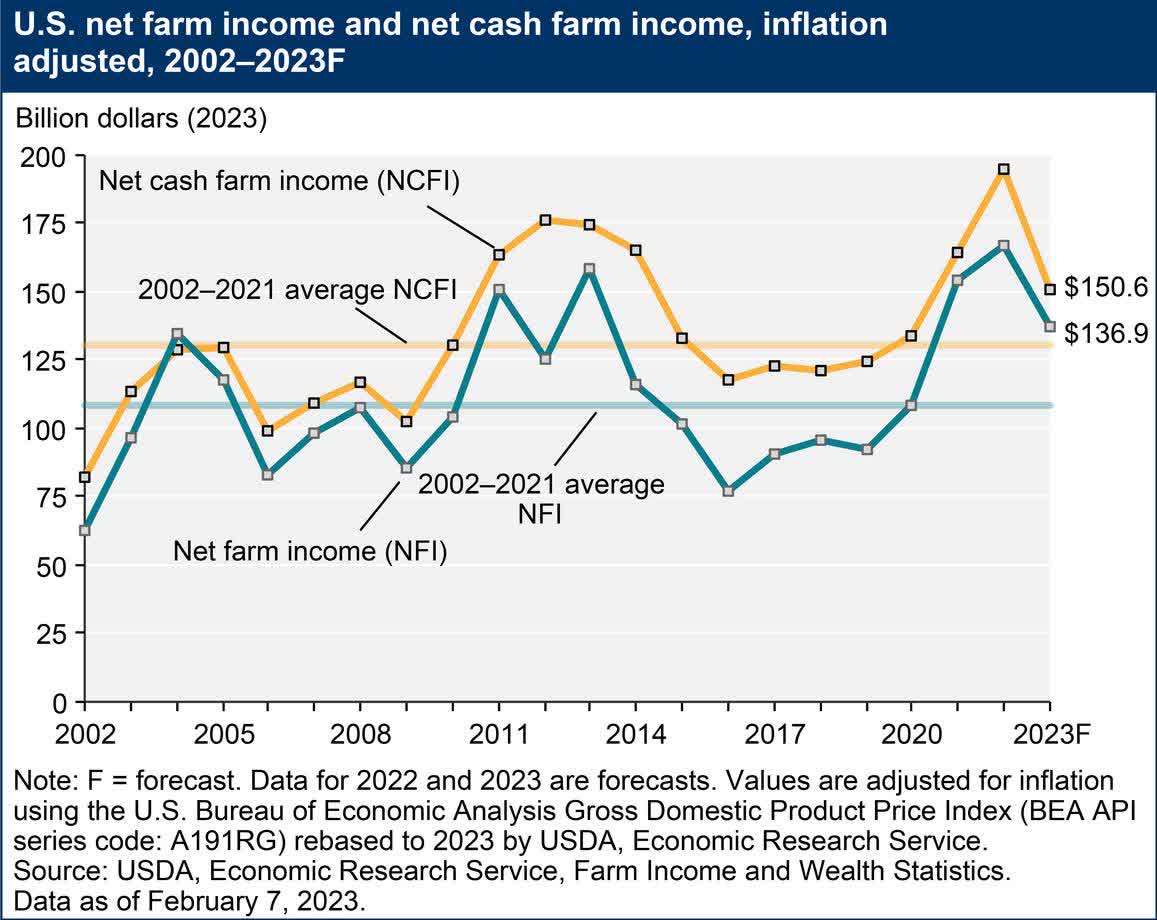

But this is the past, how is future? Higher rates should theoretically lead to an upward repricing of cap rates. This happens when rental increases are stronger than land value increases. Profitability for farmers was at record levels for 2022 but is forecasted to come down in 2023 to still very good levels.

{kind=link}

Debt levels are very manageable at 13% vs. assets and thus higher rates should not lead to major financial problems in the sector given the high profitability.

The Chicago Fed data showing some pause in Q4 hints towards a cooling off. The USDA expects farmland prices to still go up by 6.3% in 2023. Overall, it seems that after the strong increases in the past 2.5 years gains are more muted as was to be expected.

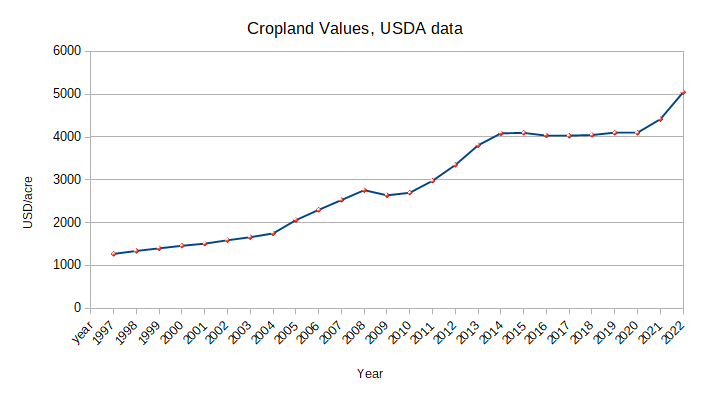

My investment case for FPI is based on the idea that adding U.S. farmland to a portfolio is very attractive as it shows relatively low correlation to other asset classes while keeping up in terms of total return. It is therefore a long-term asset based thesis. As such, I want to look how FPI holds up if we model a not so favorable land price environment. Historically, the recent run-up was not very strong after a very long period of price stagnation from 2014-2020 but I will assume that we already enter a subdued market as normalized higher interest rates lead to a reset of cap rates and dampen land value appreciation. Luckily, farmland has been fairly resistant to downturns and rarely drops strongly in value on a nationwide basis (individual properties are of course different). Instead it simply flatlines for a longer period of time. I, therefore, model a period of plateauing prices after the recent rises and then after some time an additional up-cycle. I will take the most recent cycle from 2014 to 2022 as a blueprint.

{kind=link}

This would encompass an 8 year period with 6 years of flatlining and then finally an upcycle movement of 25%. Both of those assumptions are on the conservative side. The flatlining period of 2014-2020 was very long by historical standards. Also an upcycle of only 25% is also very muted. The current cycle is more like 30-35% already given the latest data and USDA estimates for 2023. Here is the data I collected from a USDA spreadsheet from 1997 onwards:

{kind=link}

Historically, farmland increased by 5.5-6% p.a. on average. My base case above would be less than 3% annually. How to translate this into an investment in Farmland Partner's shares? I made the IRR calculations for an investment in FPI at the current price of $10.57 that assumes that NAV/share grows based on my farmland appreciation assumptions and I also assume some narrowing of the discount as we get into the up-cycle part and investors get more positive. Furthermore, I assume a 1.5% annual cash return on farmland. I believe this also to be on the conservative side as AFFO yield should be around 2% and growing over the 8 year period. I adjust that downward by 0.5% to account for replacement costs of "permanent" plantings which might be lower going forward as they sell off specialty crops. I then vary discounts ranging from -20% to +10% and value appreciation over the 8 year period from 15% to 35%. This leads to a table that shows the IRR from investing in FPI now and selling after 8 years at the respective discounts to NAV plus the 1.5% additional cash return. I don't give any credit for any additional value adding measures by management. Here is the table:

expected return table (own calculations)

This is how I think about investing in FPI, and for me this is still a valid investment without any aggressive assumptions. Mind you, I do not expect any short-term fireworks. I would not be surprised to see FPI trade at sizable discounts to NAV over several years. As an alternative to my above scenario, we might see a less back-end loaded environment where land prices continue to creep up a bit each year and FPI follows simply through staying at a discount. In such a scenario we might see relatively wider discounts similar to the lower rows but maybe higher overall appreciation.

If you are not looking at it from a portfolio perspective as I do nor simply want to own one of the most solid asset classes, you might as well skip FPI. But for me personally it still ticks the boxes as a worthwhile investment.

Investment risk

In my initial piece I argued that biggest risk for Farmland Partners Inc. was rising rates, as that could put a dampener on land price appreciation as well as pressure cash flows as debt reprices. I believe this is now mostly reflected in the current price.

My biggest risk has, therefore, changed: I think the biggest risk of investing in FPI right now is that the stock does nothing for a couple of years and then gets taken out on the cheap by private equity or a management buyout leading to poor overall returns.

I also assume that farming profitability stays at least reasonable and we won't get a repeat of the 80s inflation and farming crisis.

FPI might decide to cut the dividend at some stage, which might in turn lead to another bad day in the stock market.

Summary

Farmland Partners Inc. is likely in for a repeat performance in terms of trading at a sizable discount to NAV. This severely limits its options to grow. Instead it looks like FPI management is trying to prune its portfolio by focusing on top quality row crop farmland and try to at least partially exit the specialty crops business with the related direct exposure and profit volatility. They might also consider NAV accretive buybacks from the proceeds. Overall, these moves make sense given where they are right now.

As before, I view FPI as an asset play that allows me to get access to U.S. farmland. In terms of cashflow 2023 should hopefully mark a low and I can now get in at an even deeper discount to NAV. I expect roughly 10%+ returns from an investment in FPI over the cycle which works for me. That said, Farmland Partners Inc. could still prove to be mostly dead money over several years, and I expect those returns to be potentially back-end loaded once we enter a new strong up-cycle for land prices.

For further details see:

Farmland Partners: Investment Thesis Stands, Buy The Assets Not The Cashflows