IYR - Farmland Partners: Portfolio Diversifier And Tail Hedge

Summary

- Farmland Partners Inc. is an internally managed REIT that owns over 161,000 acres of farmland across the U.S.

- It gives investors a convenient investment vehicle to the farmland asset class that has historically been a good inflation hedge.

- FPI's low market correlation makes it ideal as a portfolio diversifier, potentially enhancing returns and reducing risk.

While Farmland Partners Inc. ( FPI ) has unremarkable cash returns (2.6% ROE in 2021), I believe investors should consider an allocation to FPI as a tail hedge against adverse weather events that are becoming increasingly frequent and the ongoing conflict in Ukraine. Historically, farmland has been a good inflation hedge. Finally, an allocation to FPI can potentially both enhance returns and reduce risk.

Brief Company Overview

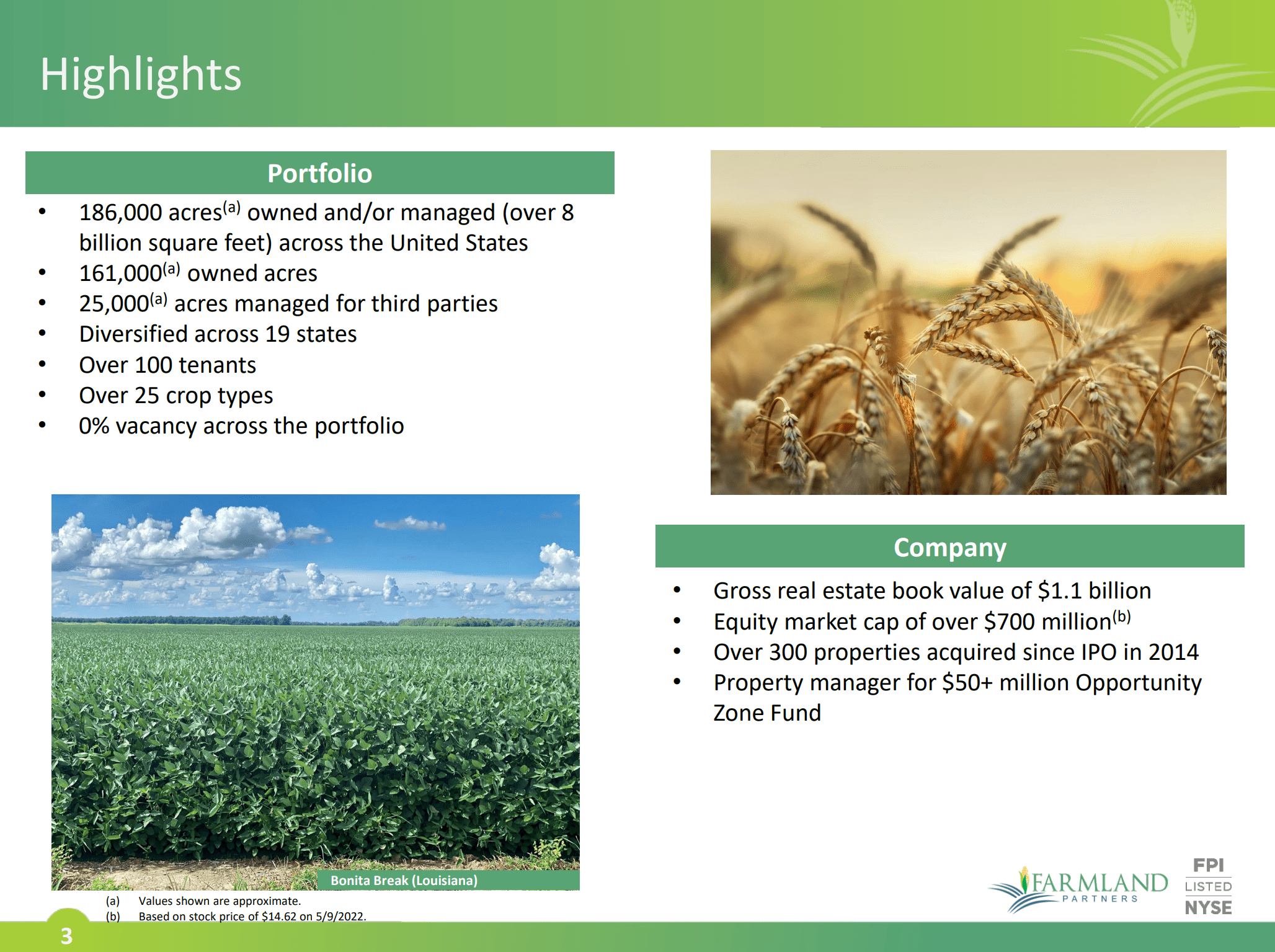

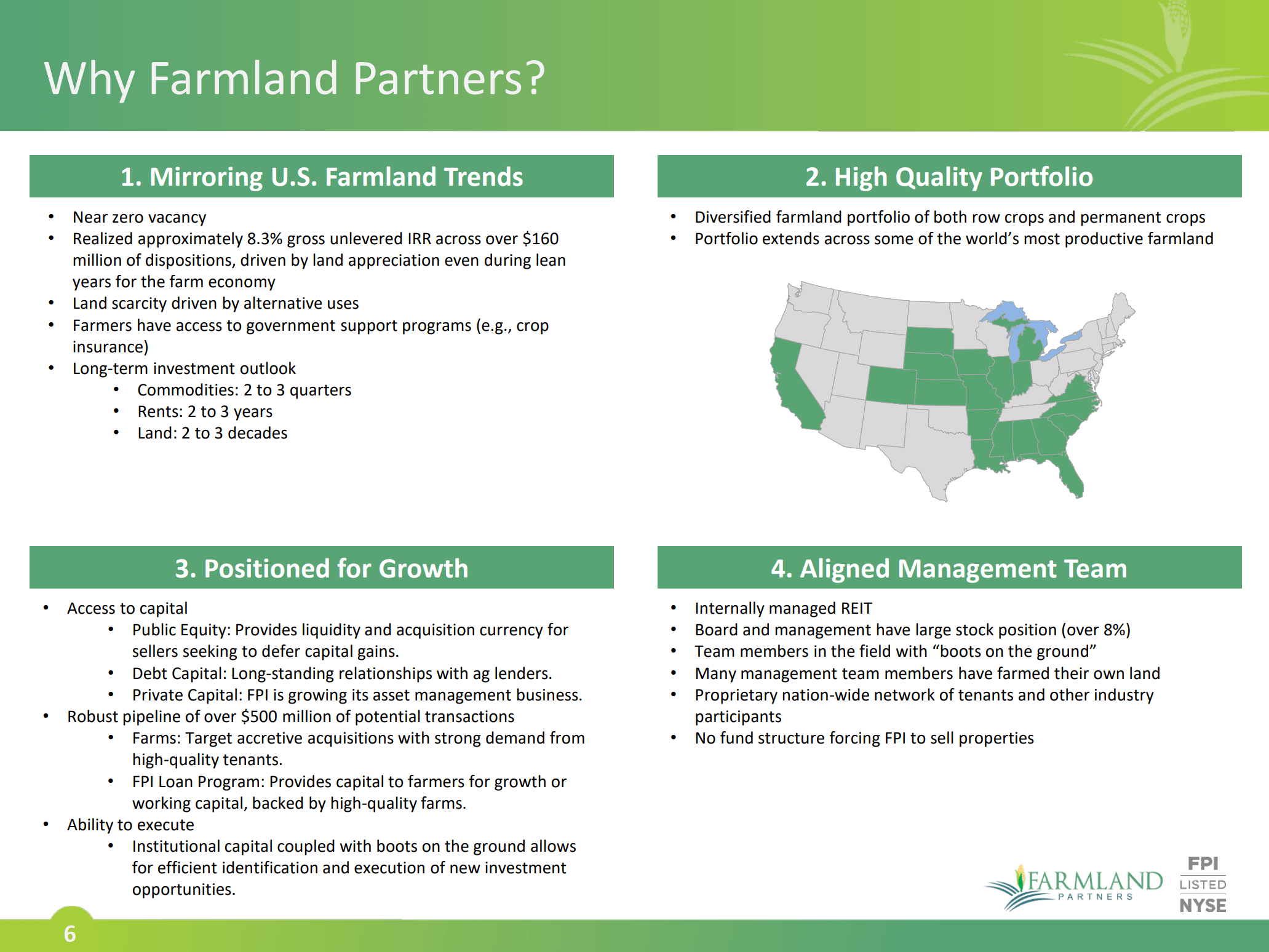

Farmland Partners Inc. is the owner 161,000 acres of farmland across the United States (Figure 1). It also manages 25,000 acres for third parties. FPI has over 100 tenants growing over 25 different crop types on its lands, and it has a 0% vacancy rate across its portfolio.

Figure 1 - FPI Overview (Farmland Partners)

{kind=link}

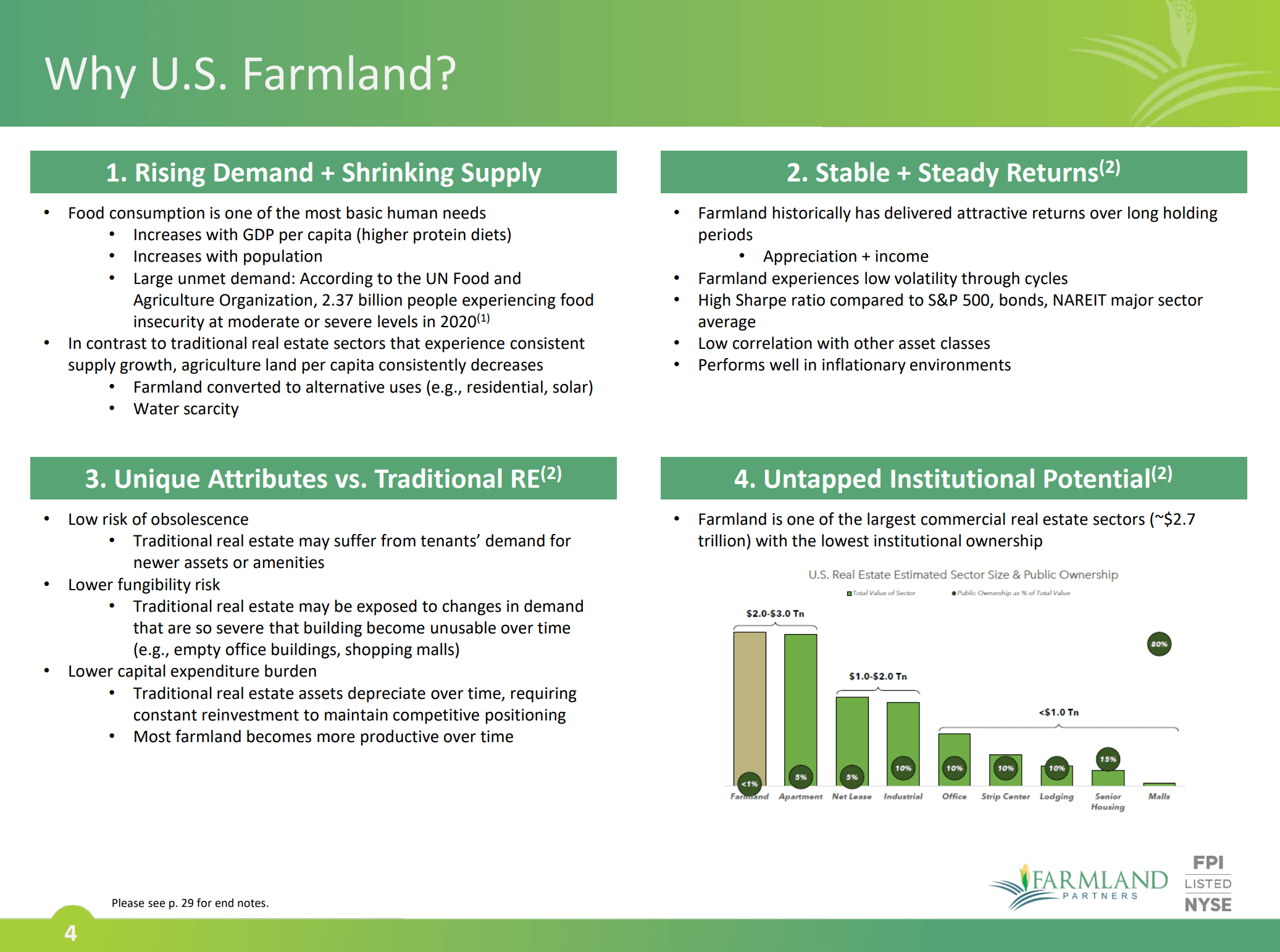

Farmland, for those not familiar, is one of the largest commercial real estate sectors, on par with apartments and ahead of industrial properties in terms of sector size (Figure 2). However, it has traditionally been the domain of institutional and high-net-worth ("HNW") investors, as retail investors lacked access.

Figure 2 - Farmland Basics (Farmland Partners)

{kind=link}

Farmland Partners gives retail investors convenient access to the farmland asset class. FPI is an internally managed real estate investment trust ("REIT") that has grown through acquisitions, to over $1.1 billion in real estate book value as of Q2/2022 (Figure 3).

Figure 3 - FPI gives investors access to farmland asset class (Farmland Partners)

{kind=link}

Look Beyond Unremarkable Cash Returns

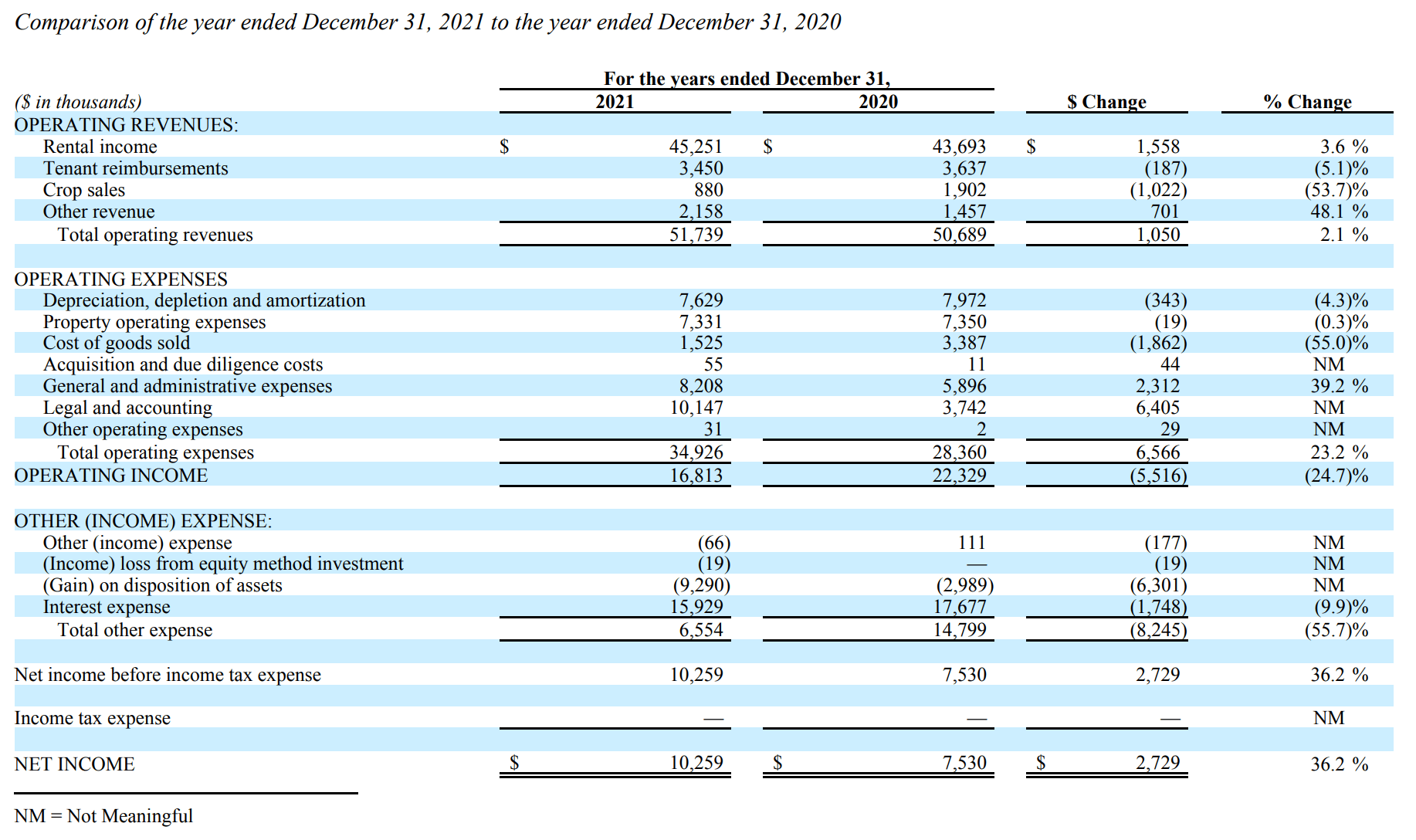

Farmland Partners' financials are not particularly remarkable on a cash yield basis. In 2021, FPI generated $52 million in revenues on $1.1 billion in real estate book value, or roughly 4.5% cash yield. After expenses, operating income in 2021 was $16.8 million and net income was $10.3 million, or 2.6% Return on Average Equity ("ROE").

Figure 4 - FPI 2021 financials (FPI 2021 10K)

{kind=link}

FPI's financials are not much different in the 2022. YTD Q2/2022 , FPI has generated $26.2 million in revenues and $3.3 million in adjusted net income.

Farmland Is A Long-Term Inflation Hedge

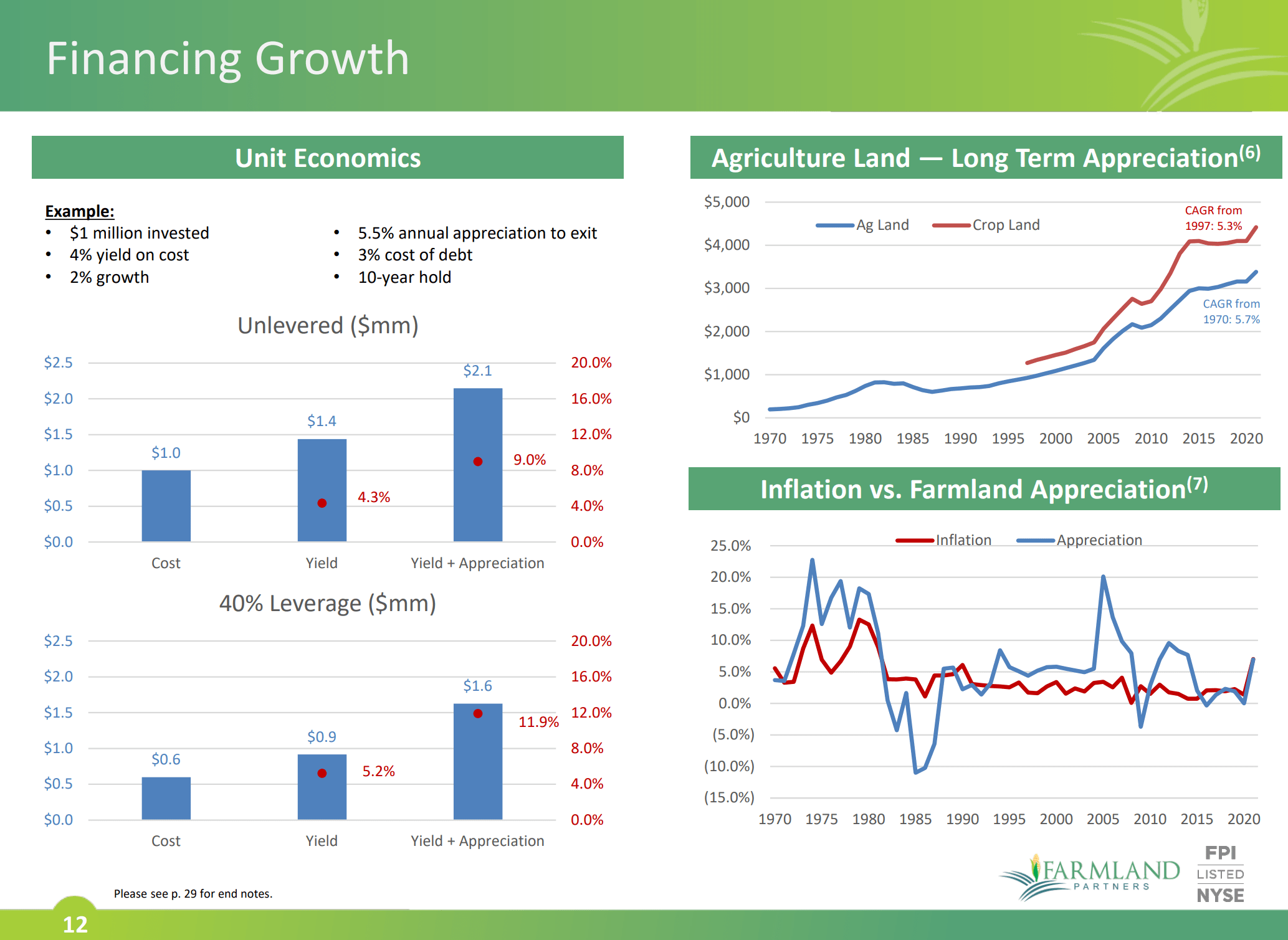

Investors are encouraged to look beyond the low cash yield and consider farmland's gradual appreciation in value due to land scarcity. Since 1970, agriculture land has increased in value at a 5.7% CAGR, while crop land has increased in value at a 5.3% CAGR since 1997 (Figure 5). Over the long run, farmland has been a good inflation hedge, as shown in the bottom right chart in Figure 5.

Figure 5 - Farmland values (Farmland Partners)

{kind=link}

FPI Had Been An Underperformer Until 2020

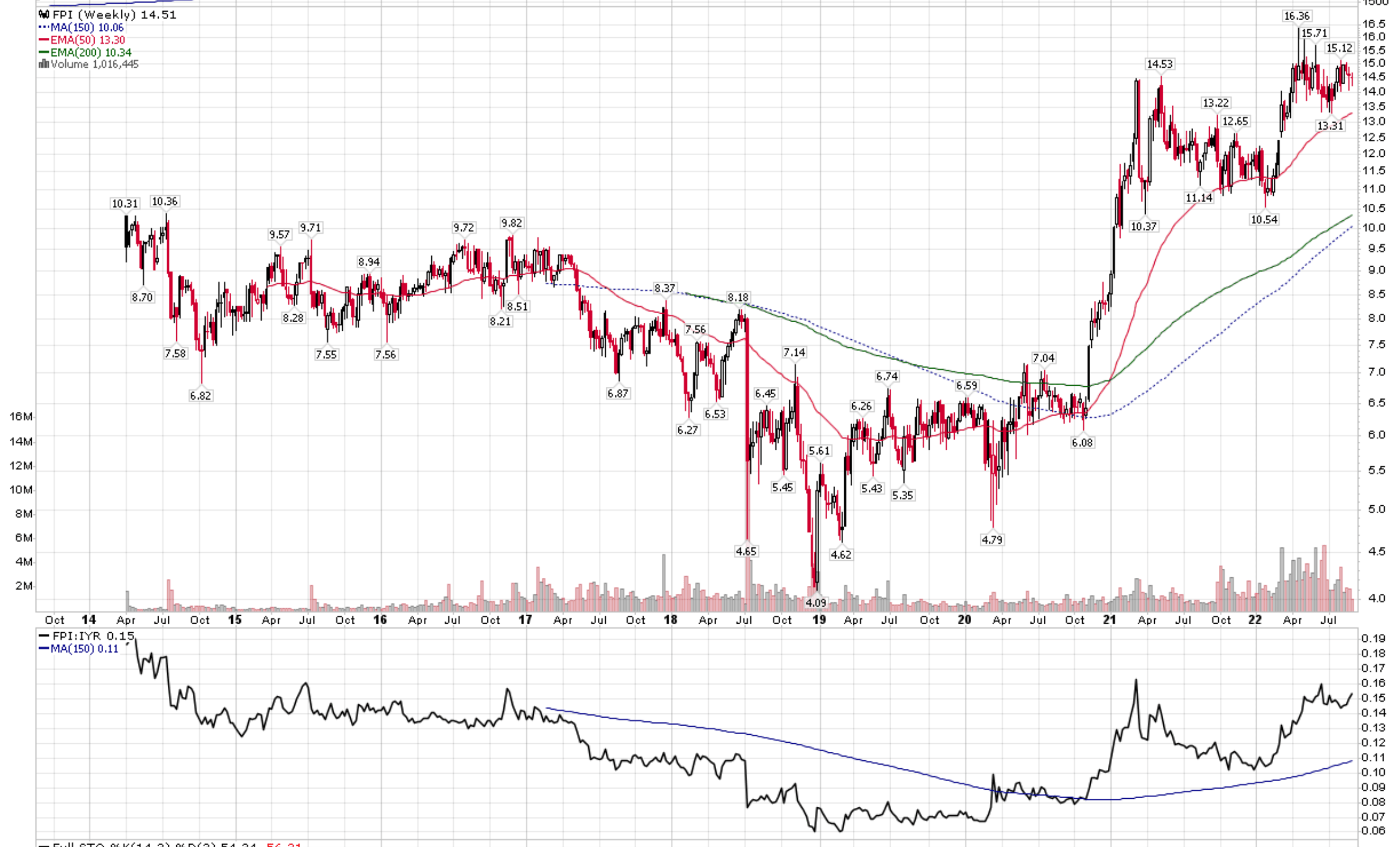

Looking at FPI's stock performance, we note that the stock had been an underperformer since it became public in 2014, lagging the iShares U.S. Real Estate ETF ( IYR ).

Figure 6 - FPI stock performance vs. IYR (Author created with price chart from stockcharts.com)

{kind=link}

Decade Of Abundance Led To Complacency

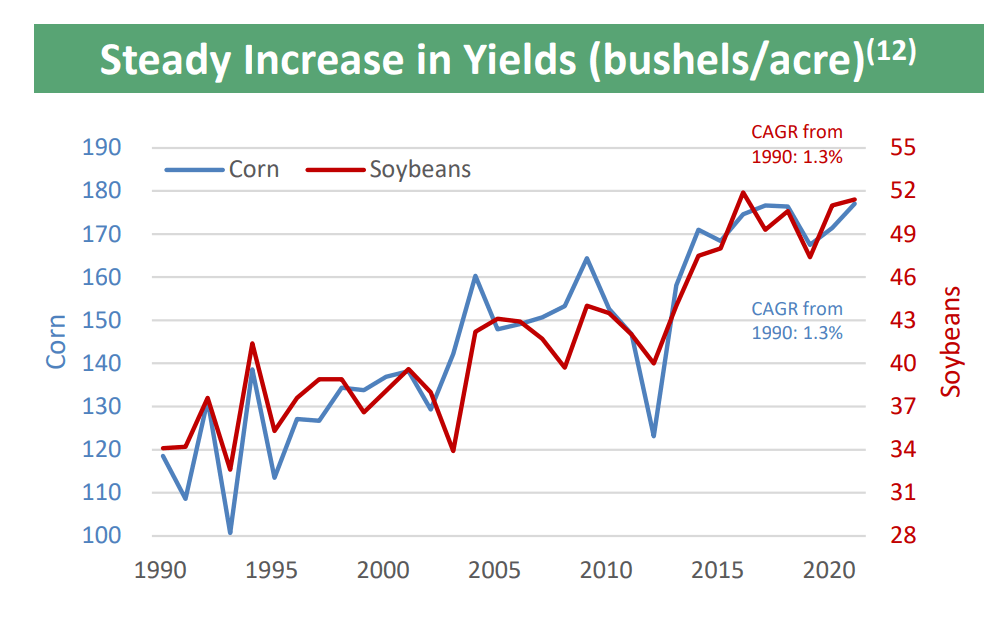

Although there are multiple reasons for the underperformance, including a shortseller attack in 2018, I believe a large part of the underperformance was due to what I call a "decade of abundance." As shown in Figure 7 below, the years from 2014 to 2020 saw increasingly high crop yields, which led to range bound agriculture prices and low inflation.

Figure 7 - Increasing crop yields (Farmland Partners)

{kind=link}

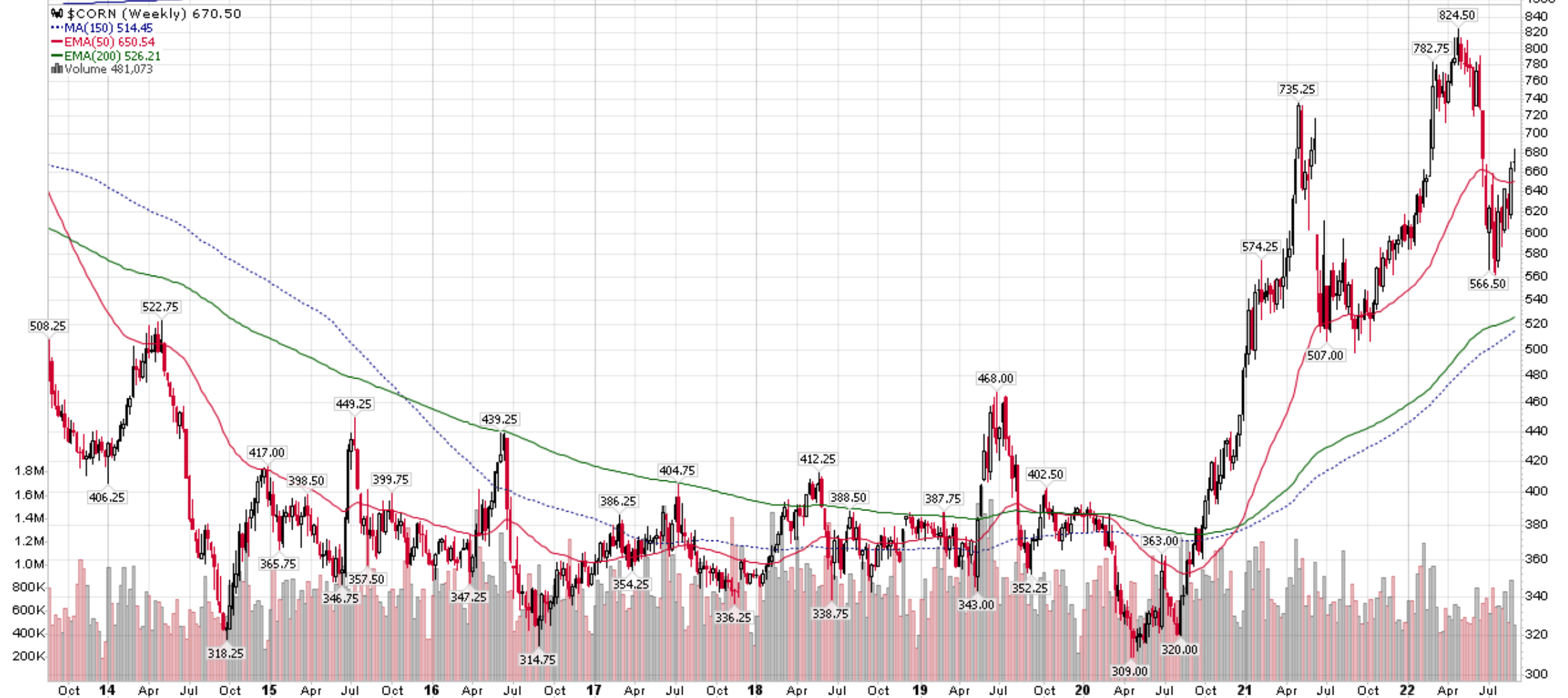

Corn prices, as shown in Figure 8, largely oscillated between $3.00 to $4.50 per bushel, and there was no urgency for investors to diversify into the farmland asset class.

Figure 8 - Corn prices (stockcharts.com)

{kind=link}

Decade Of Scarcity Calls For Tail Hedge

However, 2020 was a serious wake up call for many investors. First, we had the COVID-19 pandemic that paralyzed supply chains and caused many investors and governments to question their food security. Next, there was a historic drought in North America that began in the summer of 2020 and is still ongoing. It has been described as possibly the " most severe drought in modern history ." Finally, in early 2022, Russia invaded Ukraine (both large grain exporters), wreaking havoc with the global grain supply.

Agriculture products like corn skyrocketed in price (figure 8 above), and investor interest also picked up dramatically in FPI. Th stock went from a post-COVID low of $4.79 to recently trading as high as $16 / share.

Looking forward, I believe food prices are likely to remain high for the foreseeable future as the world grapples with severe weather events such as an epic drought in China , biblical floods in Pakistan , and the continuation of the North American drought that has caused Lake Mead to be at its lowest levels ever . Simply put, climate change is happening as we speak and it is leading to a global food crisis . Combined with the ongoing Russia/Ukraine conflict restricting export from Central Europe's breadbasket , arable farmland has suddenly become a tail hedge against both climate and man-made disasters.

Farmland As A Portfolio Diversifier

Viewed from the lens of a well diversified portfolio, we can see that an investment in farmland, represented by Farmland Partners, can both enhance returns and reduce risk.

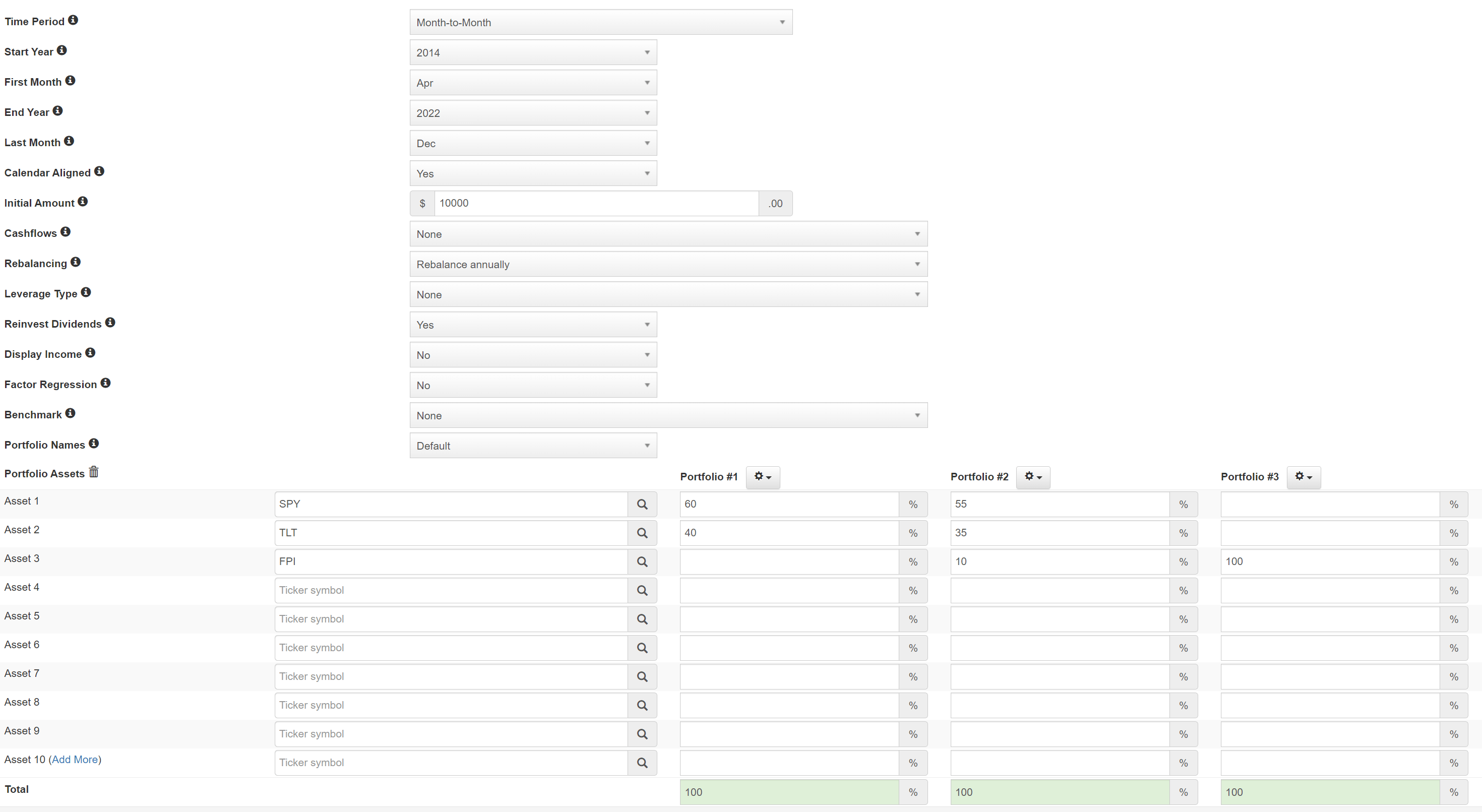

In the following Portfolio Visualizer analysis, we compare the returns between a 60/40 portfolio, a 55/35/10 portfolio that adds FPI as a diversifier, and FPI by itself (Figure 9).

Figure 9 - PV analysis (Author created with Portfolio Visualizer)

{kind=link}

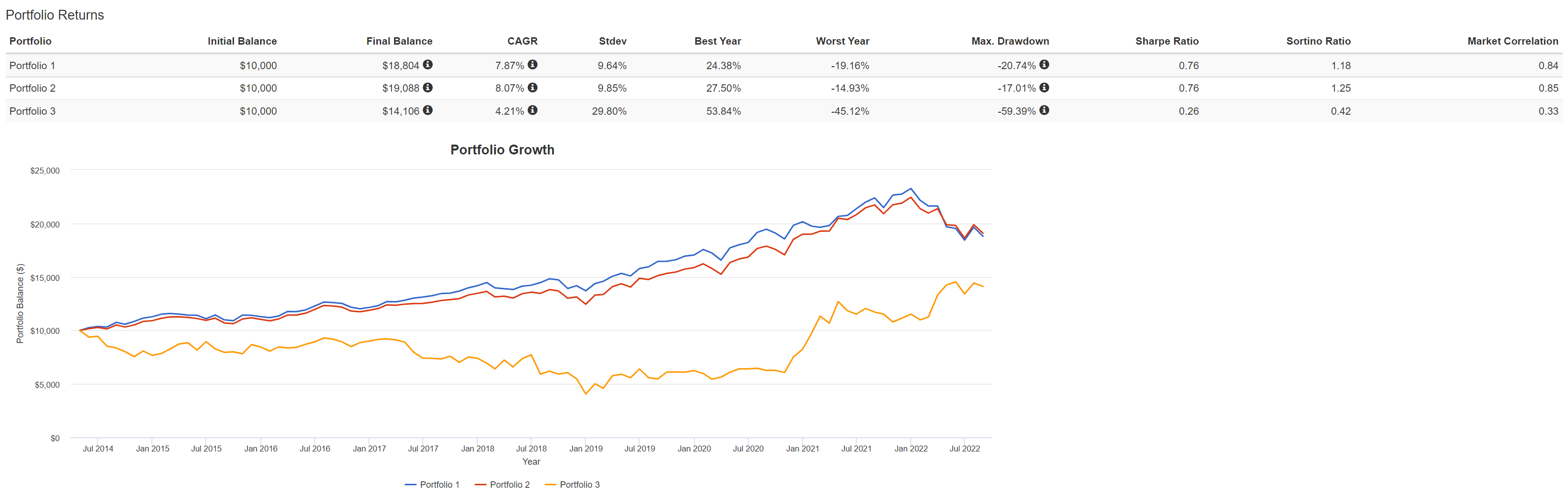

As can be seen in Figure 10 below, FPI (Portfolio 3) by itself is unremarkable. It has 4.2% CAGR return with a large max drawdown of 59%. However, when added to a balanced portfolio with a 10% weight (55% SPY, 35% TLT, 10% FPI), FPI's low market correlation shines through and the portfolio's CAGR returns are improved from 7.9% to 8.1%, while the max drawdown is reduced from 20.7% to 17.0%.

Figure 10 - Adding FPI to diversified portfolio (Author created with Portfolio Visualizer)

{kind=link}

Recent Addition Of Solar Is Icing On The Cake

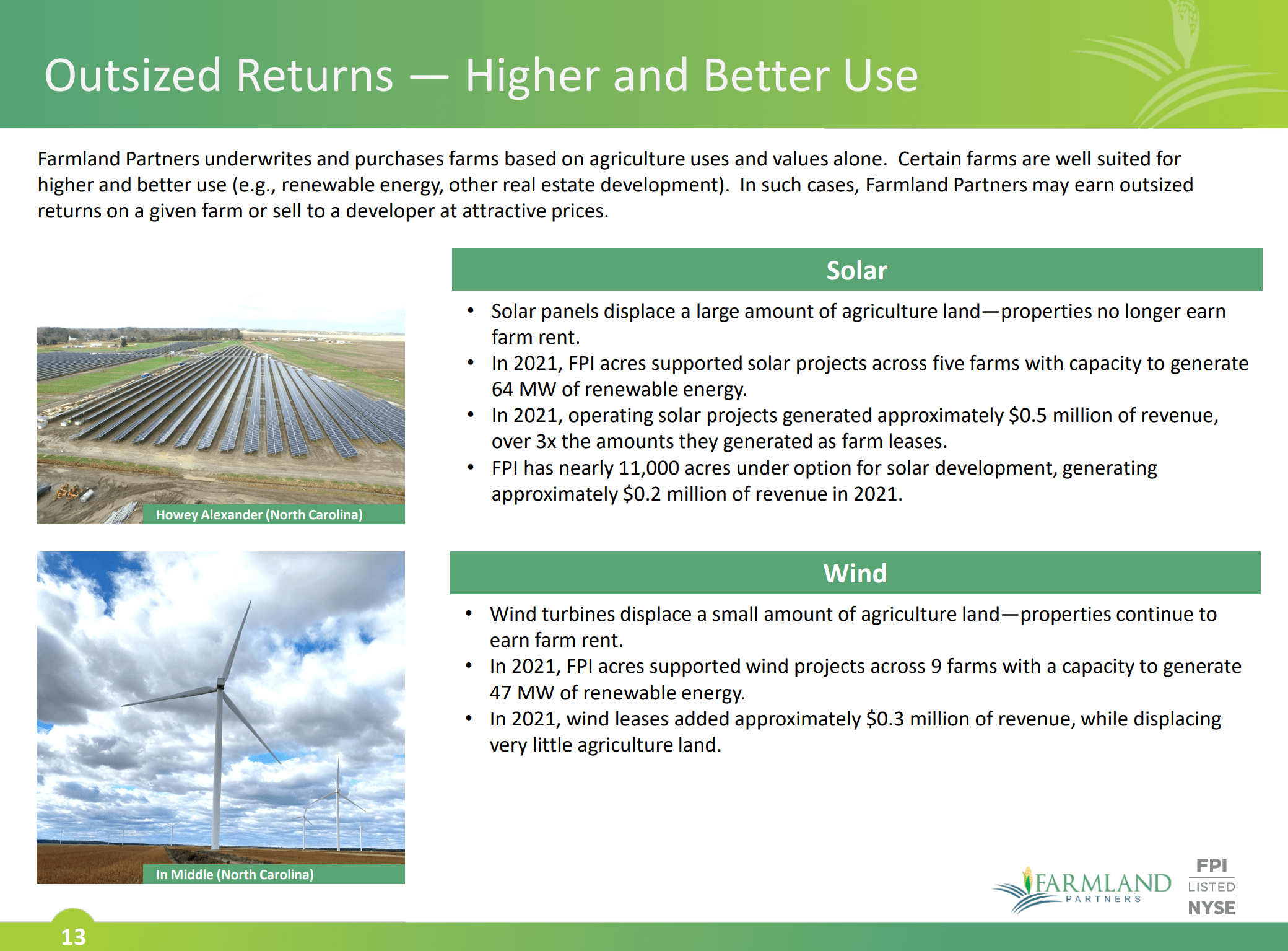

Recently, Farmland Partners have been highlighting the conversion of some agriculture land to other uses such as hosting solar and wind power generation (Figure 11). Cash revenues from these installations are often multiples of farm leases. While not core to our thesis, higher incremental revenues is icing on the proverbial cake.

Figure 11 - Some agriculture land can generate higher revenues from other uses (Farmland Partners)

{kind=link}

Conclusion

While FPI's cash returns are unremarkable, with 2021 cash yield of 4.5% and Equity ROE of 2.6%, I believe investors should consider an allocation to Farmland Partners as a tail hedge against adverse weather events and the ongoing conflict in Ukraine. Historically, farmland has also been a good inflation hedge. Finally, an allocation to FPI can potentially both enhance yield and reduce risk.

For further details see:

Farmland Partners: Portfolio Diversifier And Tail Hedge