LAND - Farmland Partners: Why The Strategy Is Not Working

2023-10-18 15:40:34 ET

Summary

- Farmland Partners Inc. is working through its interest rate challenges by selling farms and buying back stock.

- The company has completed several farm dispositions and acquisitions, resulting in solid gains.

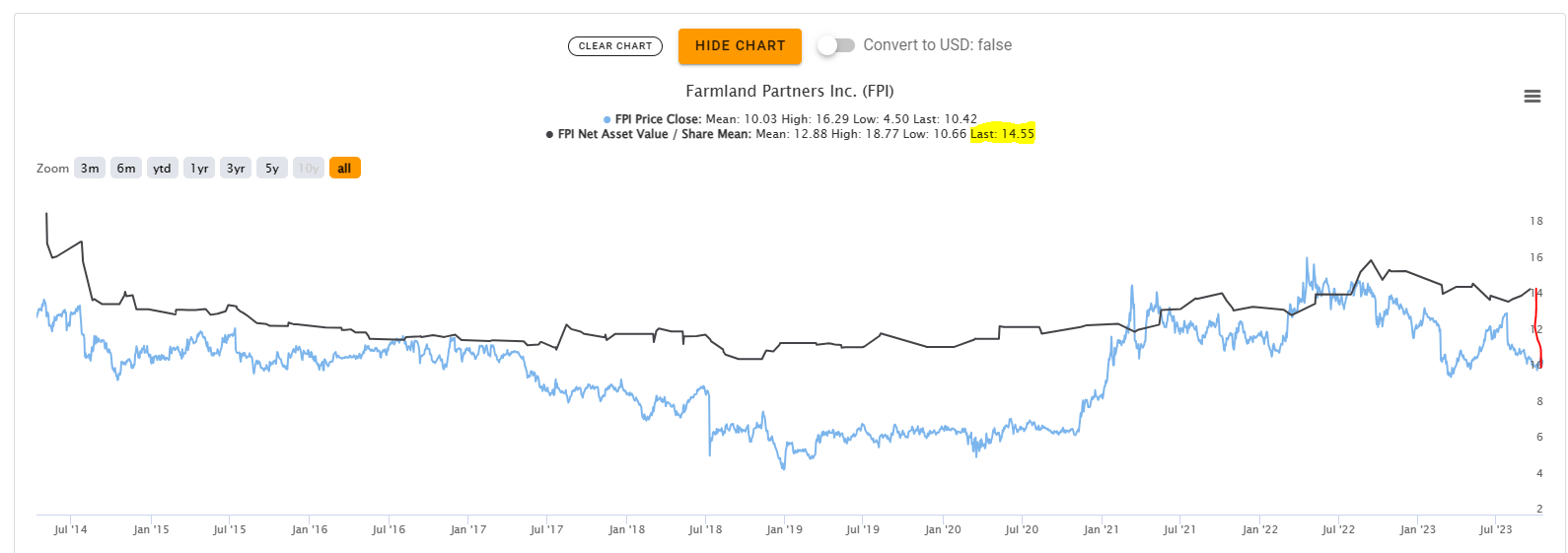

- Despite these efforts, the market does not respect the company, and the gap between its net asset value and stock price remains wide.

It is tough to make money in the REIT space and it is even harder to do so when you are really built for a low interest world. Farmland Partners Inc. (FPI) though, has got the right idea here and is working through its interest rate pains in the most methodical fashion. Will that be enough to defy the forces of gravity impacting REITs? Well, last time around, we suggested that the big decline likely would mark a buyable point.

That said, the current discount is looking modestly attractive. What is not looking attractive is the implied volatility on the stock. Generally, we tend to establish positions using a defensive approach and that requires aiming for the strike we like via options. The current implied volatility is pretty low considering the massive drop that just happened. We are looking to get involved near the $8.50-$9.50 area and this is on our watchlist.

Source: Approaching A Buy Point

The stock did a quick trip right below the upper end of our range (note the 52-week low) and bolted higher.

It has since come back down to almost the same point as when we last wrote about it.

The Current Strategy

FPI is in full discount compression mode. The firm strongly believes in the value of its properties and the strategy is to sell farms and buyback stock. In Q2-2023, we saw this:

Completed 17 farm dispositions for approximately $44.4 million in aggregate consideration and recognized an aggregate gain on sale of approximately $11.1 million;

Completed one farm acquisition for total consideration of $8.9 million;

Maintained access to liquidity of $131.9 million; and

repurchased 4,136,946 shares of its common stock at a weighted average price of $11.37 per share.

Source: FPI Q2-2023 Press Release

This was a marked acceleration from Q1-2023 where minimal amounts of land were sold. Q3-2023 results have not yet been released, but the capital market activity has been front and center.

FPI today announced that it finalized numerous transactions over the third quarter of 2023, including the disposition of more than 13,500 acres in California , Colorado , Georgia , Illinois , Louisiana , and Kansas , and the purchase of a 1,523-acre farm in Morehouse Parish, Louisiana .

The sales cumulatively totaled more than $70 million and represented a gain on sale of approximately 17%.

Through September 2023, FPI has disposed of more than $120 million of farmland, representing a total gain on sale of approximately $23 million. The Company’s currently projected asset sales for the year total $170 million.

Source: FPI

Through all of these activities, one thing remains abundantly clear. The market does not respect the company. The gap with the consensus net asset value or NAV remains rather wide, despite all of these transactions.

{kind=link}

In fact, in its entire history, FPI has seldom traded at a premium. Some of it was understandable as the malicious short-seller activities created a lot of unnecessary legal expenses for the company. But those have been resolved and the company continues to use a dollar of asset sales to buy stock trading at a 20%-30% discount. So what's the problem?

The problem is that the juice is just too little. The company is rather small and unless the commitment is to completely sell everything, value creation will be difficult. Sure you will boost up NAV by some of these asset sales and subsequent share buybacks.

But general and administrative expenses as a percentage of revenues will go up. A new purchaser of shares is likely to look at this in a negative manner and the discount to the higher NAV could widen. These are not small, to begin with.

Y-Charts

Let's zoom out to the wider space of REITs just to show you what FPI is dealing with in comparison.

We threw in a random assortment, using REITs we were most familiar with.

1) Realty Income Corp ( O ),

2) Agree Realty Corp ( ADC ),

3) Safehold Inc. ( SAFE ),

4) Vornado Realty Trust ( VNO )

5) Mid-America Apartment Communities Inc. ( MAA ),

6) Gladstone Land Corp ( LAND ).

Y-Charts

You can see the problem here. FPI towers over all of them including SAFE, one we have criticized for high expenses. LAND is a great direct comparative in this space and it too is way lower. The more traditional brick-and-mortar REITs are all way lower. You can expand this beyond the ones we have shown and it will get you to the same conclusion. These expense ratios don't work for this model.

Verdict

FPI can get to a smaller footprint and boost the NAV, but it will come at the cost of boosting the G&A expense line even higher. The problem is simply that the company is too small and the low-cap rates of the farmland asset class, make things worse. If that is not enough, FPI is likely to face even more challenges in a "higher for longer" environment.

FPI 10-Q

A lot of that debt maturing in the next three years will likely get repriced higher. Even the current interest rates on all of its debt (outside the first two lines shown above) are way higher than farmland cap rates. Now, there is value in the asset base and we think the NAV estimates are right around the ballpark. So despite all of these issues, we really cannot get bearish here. But for FPI to actually deliver this value, will require a firm commitment to sell the whole company. This can happen right away or even over two years. But that is the only way we can see some significant upside. Mind you, even that path is not guaranteed to produce results. We have seen quite a few REITs try this out (see here and here for two examples). Exploiting the differences between public and private market values often turns out to simply be an educational exercise in realizing that public values were right to begin with. At present we rate FPI as a hold and would stick to our $8.50-$9.50 range for a tactical buy.

For further details see:

Farmland Partners: Why The Strategy Is Not Working