FARO - FARO: Risky But Cloud Integration May Push The Price Up

2023-06-01 15:09:42 ET

Summary

- FARO Technologies, a global technology company specializing in 3D scanning, has recently received more debt financing and announced an integration plan, which may lead to an increase in demand for its stock and FCF margin generation.

- The company is expected to benefit from the growth of the global 3D scanning market, which is projected to grow at a CAGR of 13.11% from 2022 to 2032.

- Despite risks from lack of financing and issues with third-party manufacturers, the stock price appears undervalued, and I believe recent consolidation in the 3D printing industry may push FARO to merge with another company, benefiting shareholders.

FARO Technologies, Inc. ( FARO ) recently received more debt financing, which led to an increase in the total amount of assets, and may bring demand for the stock. I also believe that the recent integration plan announced and the consolidation of the cloud-based offerings could bring substantial FCF margin generation. Finally, I think that the new merger announced in the 3D printing market may push Faro to merge too, which could benefit shareholders. Even considering the risks from lack of financing or problems with third-party manufacturers, in my view, Faro’s shares are undervalued.

Faro Will Likely Benefit From The Growth Of The Global 3D Scanning Market

Faro is a global technology company specializing in measurement, imaging, and three-dimensional realization solutions for diverse industries including metrology, architecture, engineering and construction, and operations and maintenance.

In my view, the most interesting is how diversified is the business model. The company serves various industries such as automotive, aerospace, metal fabrication, surveying, and architecture. The following image was taken from the corporate website. It offers information about the industries served as well as the products and hardware sold.

{kind=link}

Its broad set of technology enables customers to capture and share 3D and 2D data from the physical world in a virtual environment. With a range of 3D capture technologies, including ultra-high-precision laser scanners and photogrammetry, FARO's software products and solutions are used for inspection, prototyping, high-volume documentation or 3D structures, surveying, and construction management.

I believe that it is worth noting the most well-known clients reported by Faro. Amazon (AMZN), Volvo, and the University of Yale found a lot of uses for the technologies offered by the company. In my view, after knowing these names working with Faro, other international players will most likely be willing to try the new 3D capture technologies.

{kind=link}

I believe that investors will likely appreciate conducting research about the global 3D scanning market growth. Experts in the assessment of market growth believe that the Global 3D Scanning Market could grow at a CAGR of close to 13%. I used some of this information for my financial model.

The Global 3D Scanning Market Size is to grow from USD 3.91 billion in 2022 to USD 65.79 billion by 2032, at a Compound Annual Growth Rate of 13.11% during the projected period. Source: Global 3D Scanning Market Size To Surpass USD 65.79 Billion

The Total Amount Of Assets Increased Significantly In The Last Quarter

After having a look at the most recent quarterly earnings report, I am quite optimistic about the evolution of the financial figures. The balance sheet showed an increase in assets driven by an increase in cash and cash equivalents and short term investments.

The total amount of liabilities also increased due to a new convertible loan received in the last months. I understand that perhaps certain investors don't like convertible debt, but I believe that it is beneficial that new investors are giving money to the company.

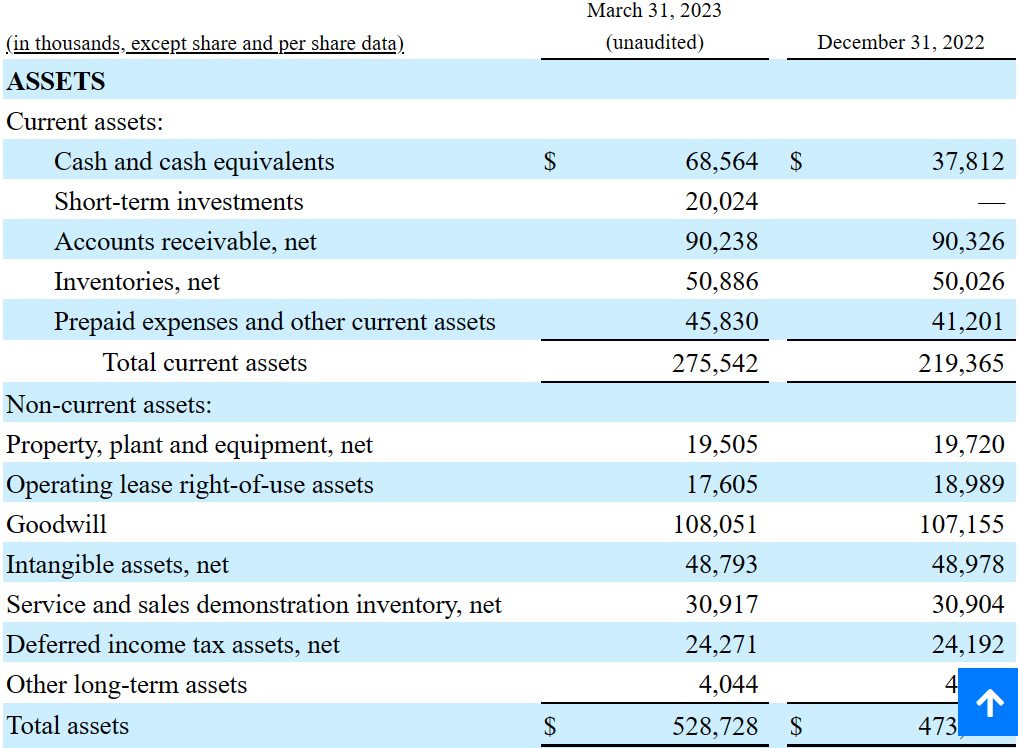

As of March 31, 2023, Faro reported cash and cash equivalents worth $68 million with short-term investments of $20 million, which I also included for the equity calculation. Also, with accounts receivable of $90 million, inventories close to $50 million, and prepaid expenses and other current assets of about $45 million, total current assets are equal to $275 million. The ratio of current assets/current liabilities is close to 2.7x, so I believe that the balance sheet appears quite solid.

The list of non-current liabilities includes property, plant and equipment worth $19 million, operating lease right-of-use assets of about $17 million, goodwill close to $108 million, intangible assets of $48 million, and total assets of $528 million. The asset/liability ratio is close to 2x, so I believe that the balance sheet stands in a very good position.

{kind=link}

In the last quarterly report, the company noted accounts payable of $22 million, accrued liabilities of about $26 million, and current portion of unearned service revenues worth $36 million.

I am not very concerned about the total amount of debt as management reported only 5.50% convertible senior notes worth $72 million. Finally, with lease liabilities worth $13 million, total liabilities are equal to $232 million.

{kind=link}

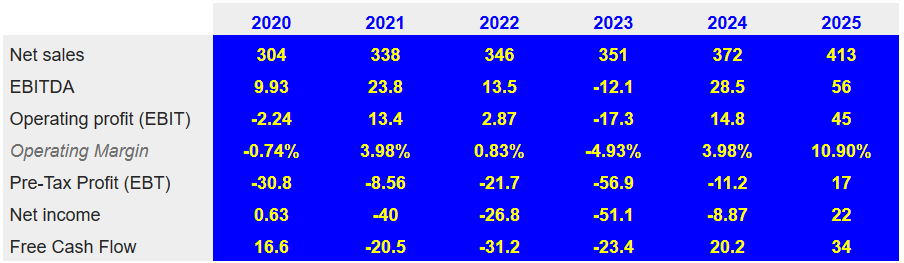

Market Expectations Include Net Sales Growth, Growing Operating Margin, And Growing FCF In 2024 And 2025

I believe that investors will likely benefit from having a look at the expectations for the year 2024, which include growing EBITDA and FCF growth. Other market analysts are expecting 2024 sales of $372 million and 2025 sales of $413 million. The operating margin would grow from 3.9% in 2024 to 10.9% in 2025. Finally, 2025 EBITDA would be close to $56 million with 2025 FCF close to $34 million.

{kind=link}

Considering the expectations of market participants, I believe that we may see an increase in the stock valuation as the new numbers come out in 2024 and 2025.

I also believe that investors should read carefully the new initiatives included in the integration plan announced in February. I hope that the consolidation of the cloud-based offerings does not damage the quality of the services provided.

On February 7, 2023, our Board of Directors approved an integration plan. Key activities under the Integration Plan include a planned decrease in headcount, consolidation of our cloud-based offerings from 3 platforms (2 acquired, 1 organic) into a single customer offering, and the optimization of our facility assets to align with current and expected future utilization. Source: 10-Q

My Financial Model

My DCF model includes several assumptions that could lead to FCF margin improvement in the future. I assumed that strengthening the understanding of customer applications and workflows, developing high-value solutions, and optimizing the lead generation process will likely benefit Faro. Additionally, new strategic partnerships to improve efficiencies and reduce costs, such as the manufacturing services contract with Sanmina Corporation, will most likely enhance the cash flow statement.

Faro recently reported a global restructuring plan, which intends to optimize resources and achieve significant annual savings. The plan includes simplification of the product portfolio, the sale of certain businesses, and the reduction of the workforce. Under my financial model, I assumed that successful execution of this strategy will likely bring FCF growth in the coming years.

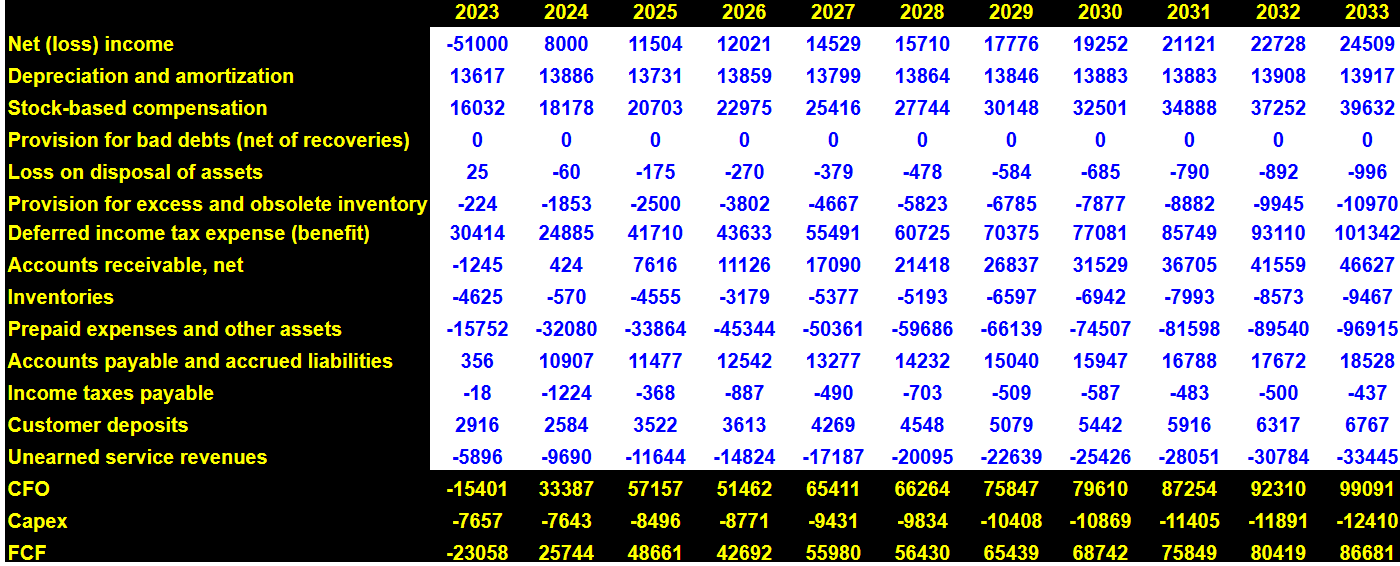

My financial model includes net income close to $24.509 million, depreciation and amortization of around $13.916 million, stock-based compensation of $39.631 million, and changes in deferred income tax expense close to $101.342 million.

I also included changes in accounts receivable of about $46.627 million, changes in inventories worth -$9.468 million, and changes due to prepaid expenses and other assets of -$96.915 million. Finally, with accounts payable and accrued liabilities worth $18.527 million and income taxes payable of -$0.438 million, 2033 CFO would be close to $99.091 million, and with capex of -$12.411 million, 2033 FCF would be $86.680 million.

{kind=link}

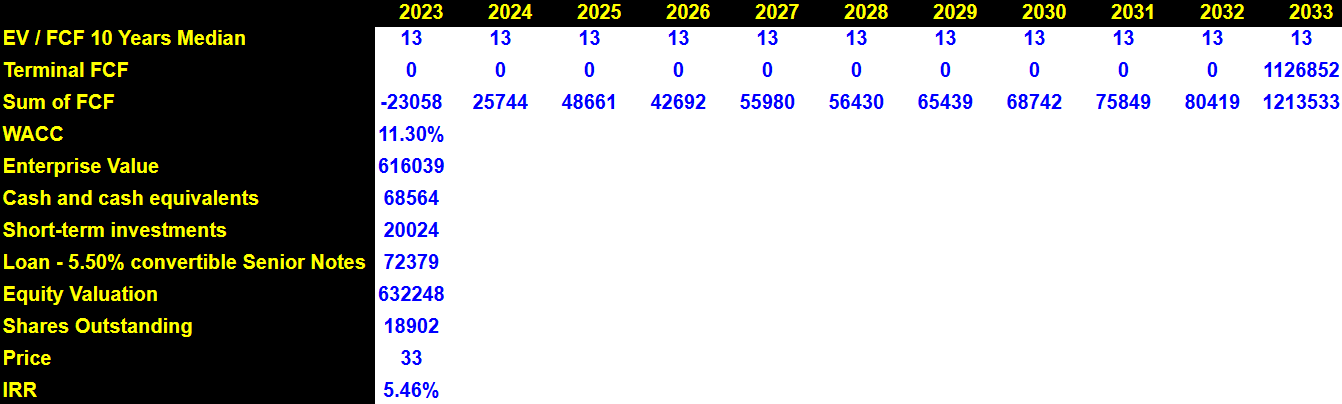

Taking into account that the median EV/FCF in the last 10 years stands at 13x, the terminal FCF would be $1126.852 million. I also assumed a WACC of 11%, which would imply an enterprise value close to $616 million.

{kind=link}

Adding cash and cash equivalents worth $68.564 million and short-term investments of around $20.024 million, and subtracting the 5.50% convertible senior notes worth $72.379 million, the equity valuation would be close to $632.247 million. If we assume a share count of 18.902 million, the implied price would be $33 per share, and the IRR would be close to 5.4%.

{kind=link}

Considering the current stock price and the fair value that I obtained in my DCF model, I believe that we may see stock price increases soon. Among the stock catalysts mentioned in this article, it is worth mentioning that the company has a stock repurchase agreement, which may bring stock demand to the market.

Acquisitions for the share repurchase program may be made from time to time at prevailing prices, as permitted by securities laws and other legal requirements, and subject to market conditions and other factors. Source: 10-Q

Risks From Lack Of Financing, Problems With Third Parties, Or Lack Of Innovation

Taking into account the stage of development reported by Faro, I believe that lack of financing would be terrible for the business model. According to the most recent quarterly report, Faro may suffer from further consolidation in the banking sector. In addition, more banks like Silicon Valley Bank (SIVBQ) may become insolvent. In this regard, management made the following comments.

First Republic Bank was also placed into receivership with the FDIC, and substantially all of its assets were sold to JPMorgan Chase Bank (JPM), National Association. If other banks and financial institutions with whom we have banking relationships enter receivership or become insolvent in the future, we may be unable to access, or we may lose, some or all of our existing cash, cash equivalents. Source: 10-Q

I also believe that the current small public float may significantly affect the valuation obtained in the DCF model. A sudden increase in volatility driven by low trading volume may lead to an increase in the cost of equity, which may bring the stock valuation down.

Our relatively small public float and daily trading volume have in the past caused, and may in the future result in, significant volatility in our stock price. Source: 10-Q

Finally, Faro may not obtain future sales growth expected by analysts, which would most likely lower the stock valuation. Besides, if third-party manufacturing facilities that the company works with try to renegotiate terms or lower production levels due to supply chain issues or transportation issues, FCF margins may also decline. For instance, issues could arise in the production of FARO Quantum Max Arm, FARO Focus Laser Scanner, FARO Laser Tracker, and FARO Laser Projector products, which are manufactured in Thailand.

Sanmina currently manufactures our FARO Quantum Max Arm, FARO Focus Laser Scanner, FARO Laser Tracker and our FARO Laser Projector products in their facility located in Thailand. Source: 10-Q

Competitors And Recent Consolidation

It seems to me that the company faces intense competition in the manufacturing and industrial measurement device market. Its products, such as articulating arms, laser trackers, and 3D scanners, compete with companies such as Hexagon Manufacturing Intelligence, Automated Precision Inc., Artec Europa, Leica Geosystems, Creaform, and Trimble Inc. (TRMB).

FARO seeks to maintain and expand its technological advantage through continued investments in technology and product development, but in my view, there are obvious risks of industry evolution and the emergence of additional competitors in the expanding market for measurement systems.

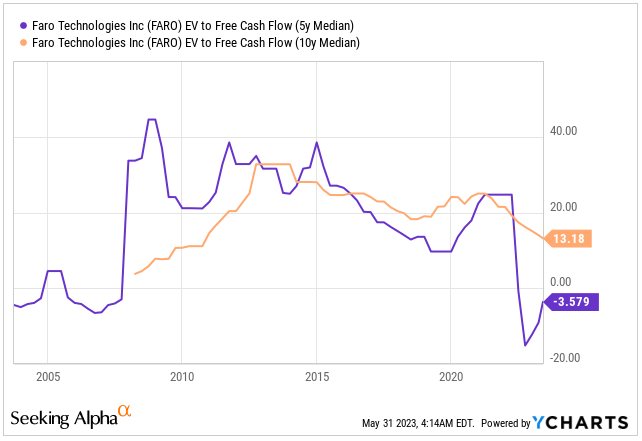

Finally, I think that readers may want to follow the recent news about consolidation in the 3D printing industry. On May 25, 2023, Stratasys ( SSYS ) entered into a definitive agreement to combine with Desktop Metal (DM), and recently Nano Dimension offered $18 per share in cash for SSYS. As shown by YCharts in the image below, there are a number of other players in the 3D printing industry, which may be willing to consolidate like DM, SSYS, and Nano Dimension. In my opinion, a wave of consolidation may affect Faro. The company may try to acquire other competitors, which may benefit shareholders in the long term.

{kind=link}

Conclusion

Faro reported an increase in the total amount of assets, successfully received new debt, and announced an integration plan. In my view, if the consolidation of the cloud-based offerings does not compromise the quality of the products offered by Faro, the efforts may lead to FCF margin expansion. I also think that Faro may benefit substantially from the global 3D scanning market growth, which is expected to bring double digit growth. Finally, I believe that the recent consolidation noted by Stratasys Desktop Metal and Nano Dimension may push the company to merge too. As a result, shareholders may benefit from FCF margin growth. In sum, I do see risks from lack of cash, new investments, and issues with third-party manufacturers, however I believe that the stock price appears quite undervalued.

For further details see:

FARO: Risky, But Cloud Integration May Push The Price Up