FRCOY - Fast Retailing: Quality At A Steep Premium

2023-06-09 15:24:30 ET

Summary

- Fast Retailing followed up solid April sales numbers with an even more impressive sales report in May.

- With contribution from China also set to accelerate post-earnings in the upcoming quarters, the company appears poised for another beat-and-raise.

- But the lofty valuation has already priced in a lot of optimism, and I would exercise caution here.

Japanese casual clothing retailer Fast Retailing ( FRCOY ), operating the Uniqlo and GU brands, posted another set of solid sales numbers in May, with same-store sales (including online) in Japan up 4.4% YoY. The domestic outperformance comes on the heels of April same-store sales growth of +1.7% YoY, led by per-customer spending of +7.5% (vs. a decline in traffic) despite temperature-related headwinds toward the back half of the month. Going forward, expect the domestic strength to be complemented by expansion at Uniqlo International as well, particularly in Greater China, where a post-reopening recovery is underway. And even with limited long-term growth potential for Uniqlo Japan, given its already high market share, Fast Retailing will benefit from an extensive mid to long-term runway in Europe, North America, and Southeast Asia.

As attractive as the company's fundamentals may seem, however, the valuation is a major hurdle at ~37x P/E. Having re-rated this year alongside broader Japanese indices on TSE reform-driven optimism , the relative valuation premium vs. peers like Ryohin Keikaku ( RYKKF ) seems too wide. While this is a stock that could well grow into its valuation over time, there isn't a lot of safety margin here; pending a meaningful pullback, I would remain sidelined.

An Impressive Domestic Sales Acceleration in May

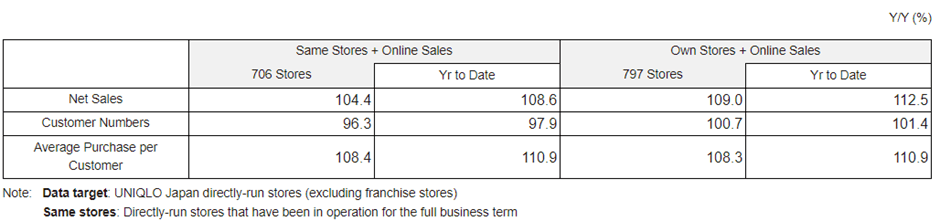

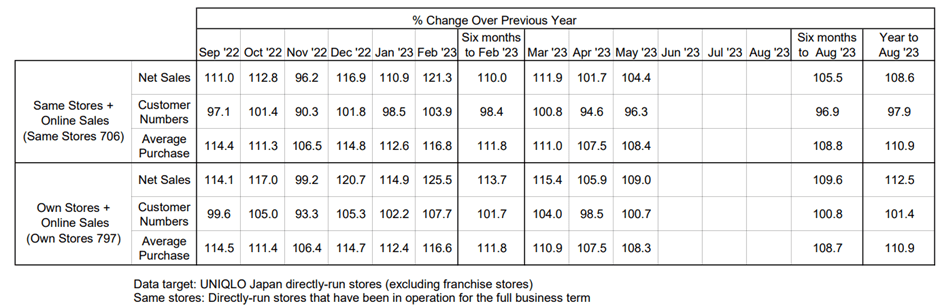

Japanese apparel retail sales have surprised positively over the last month, with numbers in recent months reflecting a post-COVID recovery in mobility and demand. The extent of Fast Retailing's outperformance over the last two months, though, has been impressive. Last week's May sales report was a case in point - Uniqlo Japan saw its same-store sales and online sales up 4.4% YoY, with sales from own stores and online outpacing the broader group at +9.0% on the success of its summer merchandise and in-fashion products. Of note, the strong May print also comes on the heels of price hikes in April (same-store and online sales for Uniqlo Japan rose +1.7% YoY), highlighting the company's domestic pricing power.

{kind=link}

Digging deeper into the numbers , the MoM acceleration was perhaps no surprise, given April sales had been impacted by weather-related headwinds in the back half of the month. But while customer traffic was down, the rise in per-customer spending more than offset the impact, led by price hikes across high-ticket merchandise and on-trend releases of new Spring/Summer products. The momentum from its Summer product line continued into May, again driving a YoY rise in average spending. Despite the higher prices, traffic appears to have been resilient - excluding the seasonal headwind from the fewer holidays vs. last year, the same-store traffic decline would have been much less steep than the -3.7% YoY headline release. With the April/May reports implying a mid to high-single-digits percentage YoY same-store and online sales growth algorithm for the domestic business on a trailing H2 basis, the company appears poised for another beat-and-raise.

{kind=link}

Leaning on International for the Next Leg of Growth

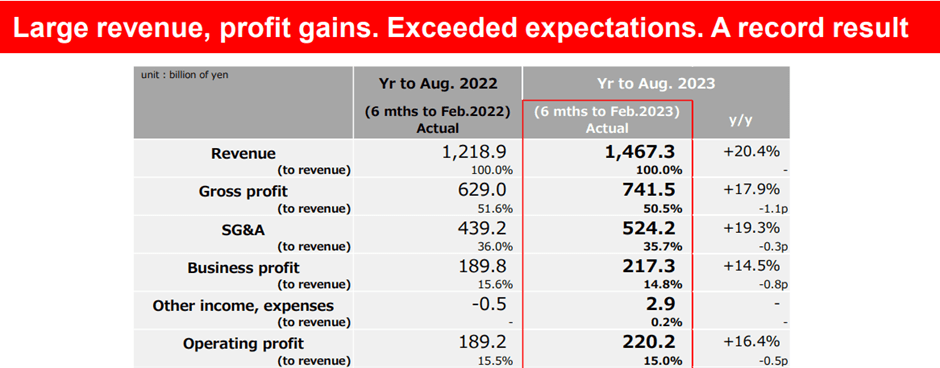

While the domestic sales updates were encouraging, the key highlight of Fast Retailing's H1 results (+14% YoY business profits) was the growth in South Asia, Southeast Asia and Oceania, North America, and Europe (ex-Russia). Performance in these growth regions more than offset weakness at Uniqlo Japan, which suffered a contraction in gross margins due to higher procurement costs. Revenue in China was also a weak point - despite being up 5% YoY for the period, FX headwinds (19.8 JPY/RMB in H1 2023 from 17.7 JPY/RMB in the prior year) wiped out much of the gains. Given China's sales numbers were impacted by COVID, though, the performance was commendable. And with management also citing same-store sales in mainland China rising strongly in March (+40% YoY), I expect an outsized P&L contribution from the region in the upcoming quarter. Alongside the growth in the rest of Uniqlo International, which typically commands higher margins vs. the domestic business, the company appears poised for significant expansion over the mid to long term.

{kind=link}

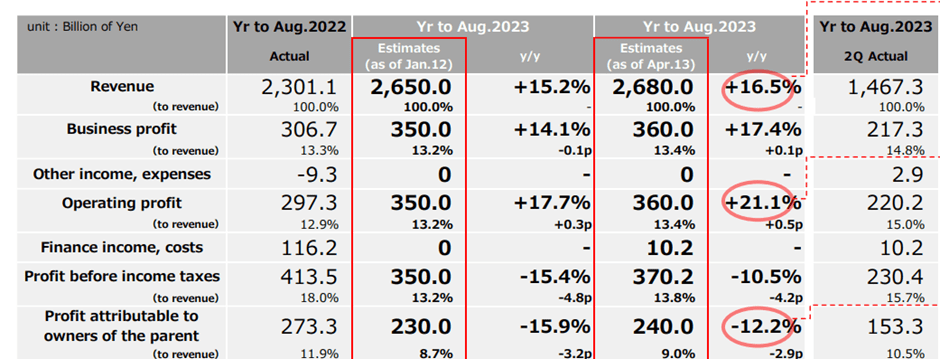

In tandem, management revised its guidance higher post-H1 - the full-year fiscal outlook for sales now stands at JPY2.68tn (from JPY2.65tn prior), JPY360bn for business profit (from JPY350bn prior), and JPY360bn for operating profit (from JPY350bn prior). The key driver for the guidance raise was a better outlook for Uniqlo Japan, though at an expected same-store sales growth of +2% YoY (vs. +4.4% YoY in May), more upward revisions are likely on the horizon. Uniqlo International is guided to come in strongly as well, offsetting weakness in the GU format (i.e., the Uniqlo sister brand with lower price points) and its ex-Uniqlo/GU brands (e.g., Comptoir des Cotonniers and Theory).

{kind=link}

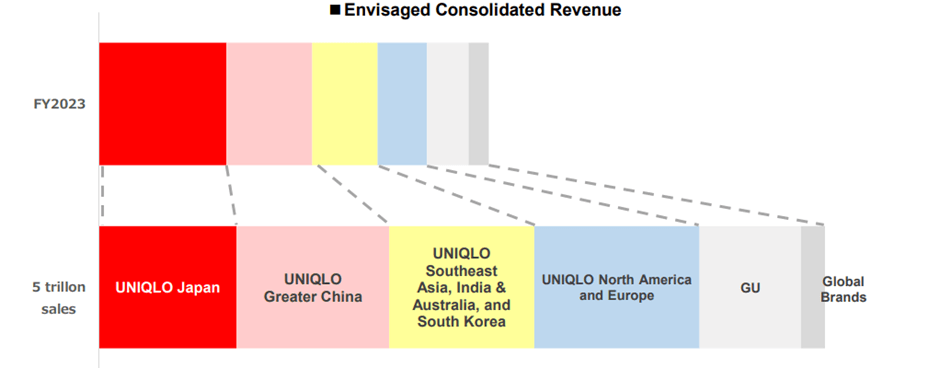

While the domestic strength will likely be the main near-term driver, Uniqlo Japan already has a high market share, and thus, the mid to long-term growth potential is limited here. Instead, I would focus on the margin expansion progress at Uniqlo International, particularly in the higher-margin China business (note segment margins deteriorated through H1), along with new concepts like LifeWear (i.e., a more environment and socially conscious brand), where uptake appears to be gaining traction globally. With the stock already re-rated to 37x P/E, though, there isn't a lot of room for execution missteps on the path to reaching its JPY5tn/year midterm sales target.

{kind=link}

Quality at a Steep Premium

Fast Retailing looks set for another beat-and-raise quarterly report, with monthly Uniqlo Japan sales numbers coming in well ahead of expectations yet again. Same-store sales growth for Uniqlo Japan came in at an impressive +4.4% YoY (+9.0% YoY for own stores and online sales), accelerating from the +1.7% YoY growth in April on the back of improved per-customer spending and traffic. Supported by reopening tailwinds in China, Uniqlo International should also deliver strong sales and profit numbers in the upcoming quarter. Alongside emerging growth markets like Europe, North America, and Southeast Asia, the growth runway for Fast Retailing is attractive, more than offsetting any potential slowdown for Uniqlo Japan in the mid to long term. Like all great fundamental stories, however, the catch is the valuation - at the current valuation premium, the stock has priced in a lot of optimism and could de-rate on any growth disappointments ahead.

For further details see:

Fast Retailing: Quality At A Steep Premium