FRCOF - Fast Retailing: The Dream Of Global Domination Is Very Much Alive

2023-03-21 07:44:55 ET

Summary

- The momentum behind Asia-led growth is considerable.

- But higher sales have not all translated into profits, at least not the bottom line kind.

- The stock, which looks fully priced at the moment, provides a good exposure to the fast-growing Asian apparel market.

Fast Retailing (FRCOY) began with UNIQLO close to forty years ago. Today the group is still defined by the brand synonymous with affordable everyday wear. What has changed is the geographical makeup of business. Halfway through its existence, UNIQLO became more international than purely Japanese, which had always been the intention of the founder and CEO Tadashi Yanai.

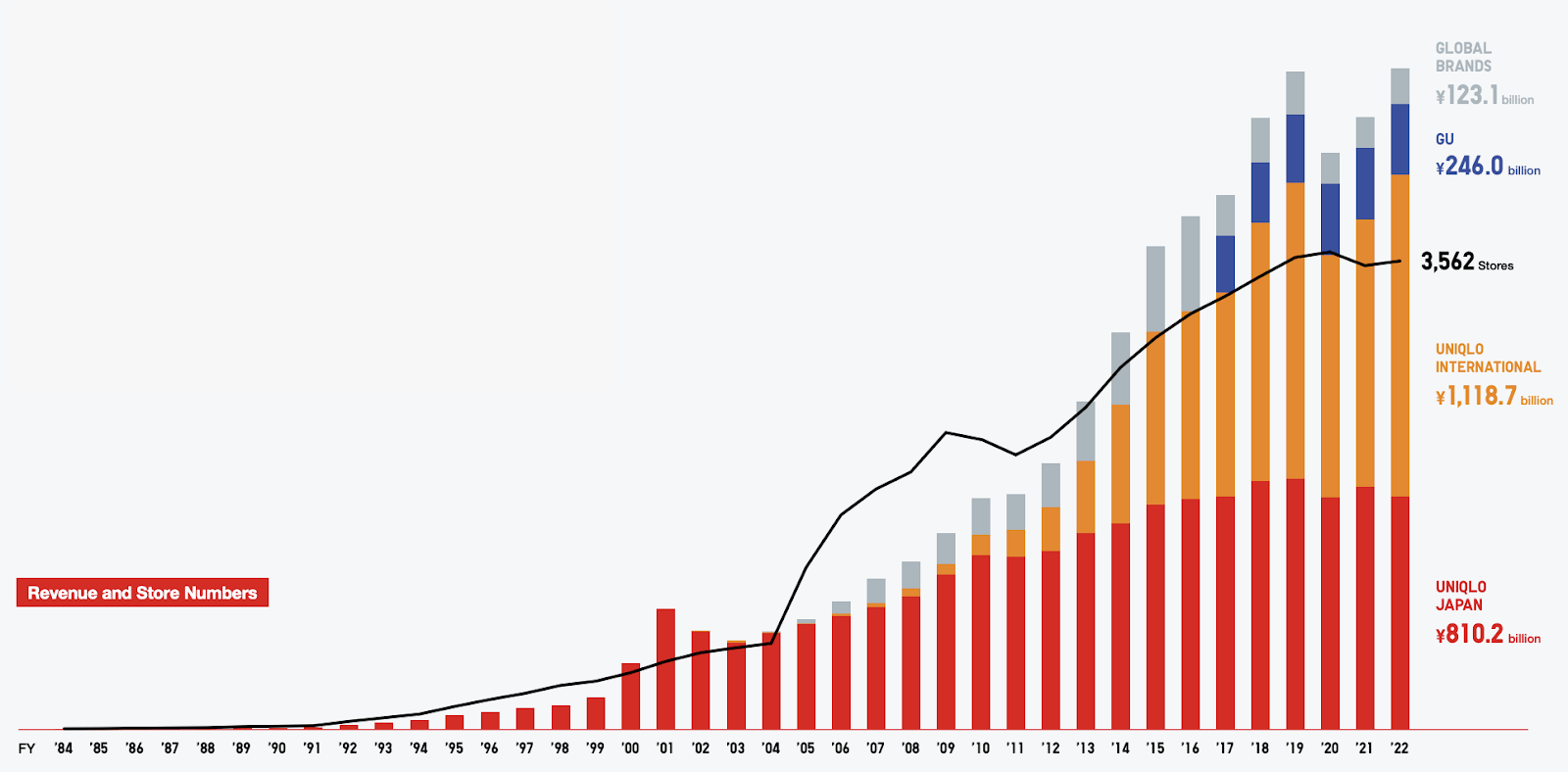

Among some two dozen countries where UNIQLO is present, Greater China (comprising mainland China, Hong Kong and Taiwan) has the most stores, 996 from a total of 2,394. Including South Korea and Southeast Asia, Asia has become the main driver of growth. Operations in the West lag behind but may finally be breaking new ground. In financial 2022, the North American division made a profit for the first time since opening shop 17 years ago.

{kind=link}

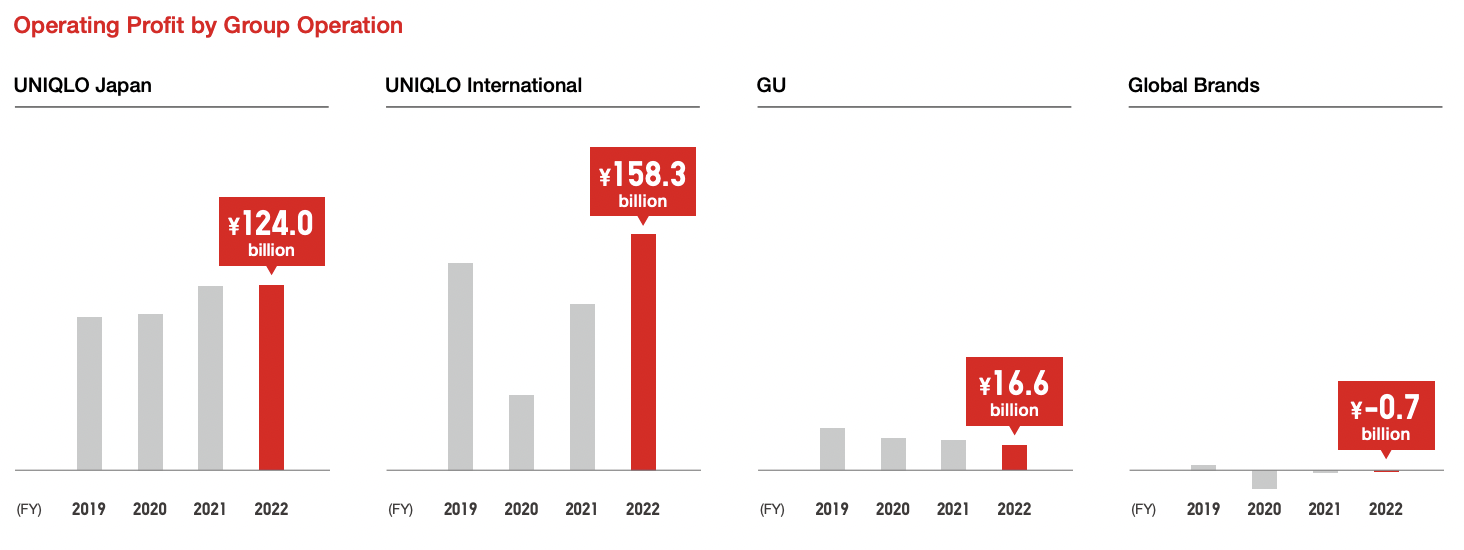

The group has been going from strength to strength, discounting Covid-related stumbles in 2020 and 2021. Only Greater China was still affected by movement restrictions in the latest financial year. Overall, UNIQLO International - that brings almost 50% of total revenue - has recovered to pre-pandemic levels thanks to gains in Southeast Asia, North America and Europe. But brands other than UNIQLO, the most notable being Japan-based GU which contributes 10% of sales, show more variable performance.

{kind=link}

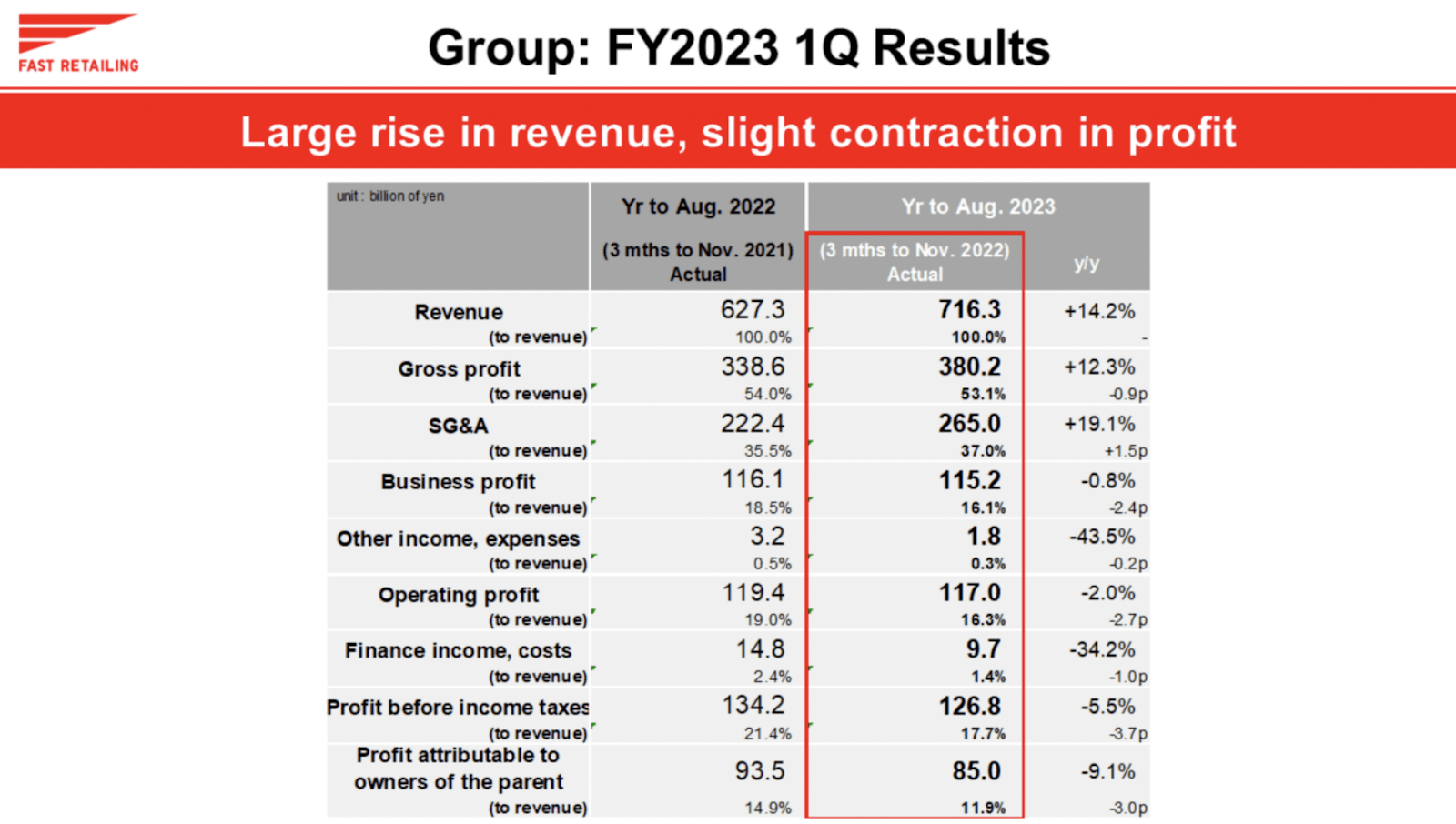

The forecast for FY2023 is modest and achievable. Revenue is expected to be lifted by 15%, operating profit by 17%. Concurrently, final profit is anticipated to fall by the same amount, although it grew without fail for the past five years , save for 2020. This bottom line effect might have to do with slowing economies and continuing inflationary pressures. So far Q1 results, from September to end-November, were broadly supportive of the forecast although they came slightly below target; better results from mainland China following its official reopening should help.

{kind=link}

The group's cash flows and cash balance have been robust. Cash and cash equivalents totaled ¥1.3582 trillion at the end of August 2022, equaling 4-5 months of short-term ¥3 trillion annual sales target, kept as ready liquidity to deal with unforeseen fluctuations and earmarked for growth investment. Capital expenditure will increase in coming years with many more new stores and automated warehouses in the pipeline. Fast Retailing is also fiscally sound; debt-to-equity at 23.2% is currently the lowest in a decade.

Strategy

The latest focus is on digital transformation of the supply chain - which in the fashion industry is a critical issue. Through the use of advanced information technologies in partner factories, warehouses and stores, the group hopes to achieve greater efficiency in manufacturing and inventory management. This, in turn, addresses two of the biggest grievances mounted against fast fashion companies (that Fast Retailing to its dismay is most often classified as): environmental waste and abuses of workers' rights.

To be sure, the intended changeover will not be absolute but it is definitely a step up, especially compared to the way fast fashion newcomers (such as online-only Shein and Asos) operate. In contrast to that definition of 'fast', Fast Retailing and its top brand UNIQLO promote their clothing lines as "today's classics" - affordable but still high-quality and hence durable. In this sense, the emphasis on sustainability is a natural extension of the LifeWear philosophy .

One reason why Fast Retailing is proactively reforming is its continual shift towards the global market. To build affinity with Western customers where UNIQLO is yet to make a mark, not only is the brand changing the way it manufactures but also the way it thinks up clothes. The American headquarters will soon be involved at every stage of product creation, which has till now been the exclusive domain of the Tokyo office. All in all, the group's organizational structure is turning less traditional and more collaborative, open to input from local managers.

Risks

Even through multiple operational reforms, Fast Retailing is staying cautious due to the downbeat macroeconomic environment. The global economy is expected to experience a noticeable slowdown in the next couple of years, with global GDP growth forecast to reach only 2.6% in 2023, down from 3.2% recorded in 2022. Japan, a material market for Fast Retailing, will be plodding at 1.4%. And inflation will remain on the radar in most places until the latter half of 2024. The good news is that much of the growth will be delivered by the emerging economies in Asia, where the group is heavily concentrated.

Stock

Fast Retailing is listed on the First Section of the Tokyo Stock Exchange and also offers depository receipts on the Main Board of the Hong Kong Stock Exchange. Traded in the US OTC market, FRCOY is an unsponsored ADR representing one-tenth of a common share.

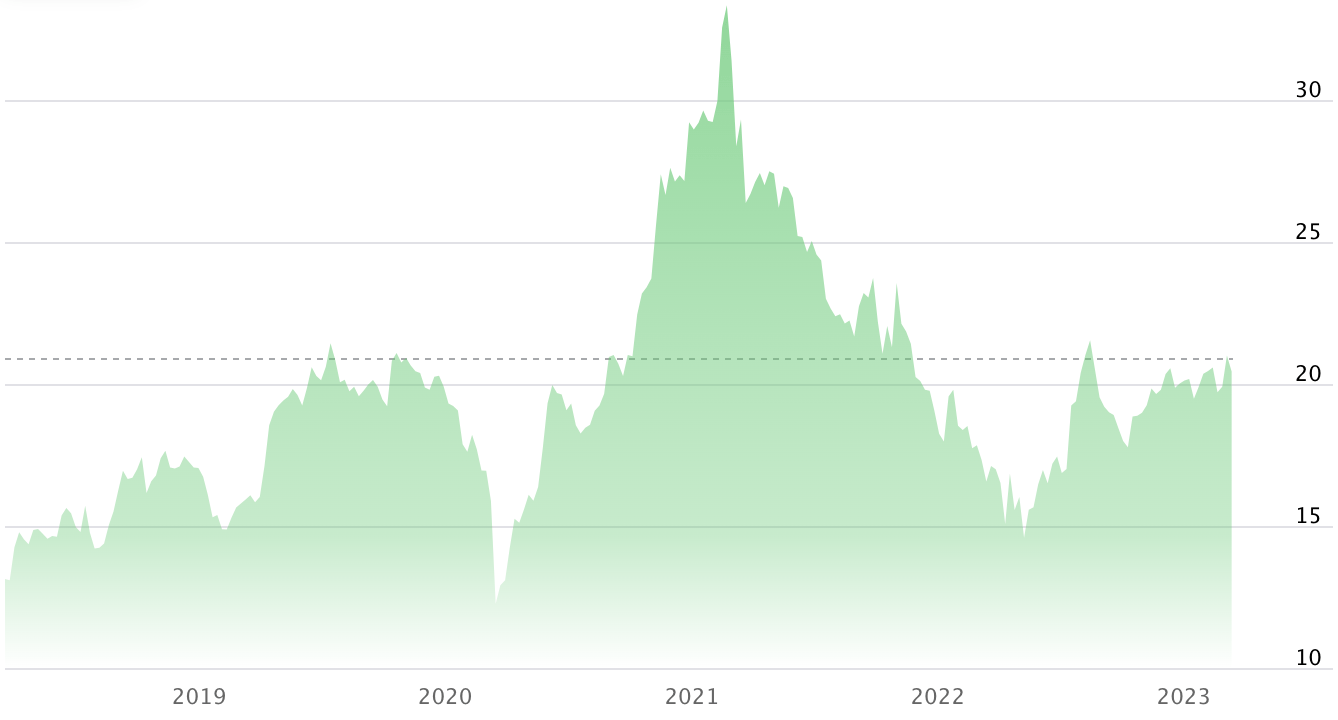

FRCOY closely follows TSE:9983 in price; over the last five years, the stock returned 112% (120% including dividends). The past year has been positive: 39% against median 24% of the Japanese specialty retail industry. The stock pays a smallish dividend yielding less than 1%, which translates to a payout ratio of 24%.

TSE:9983 vs FRCOY Stock Charts

{kind=link}

Compared to Japanese peers in specialty retail whose trailing P/E averages 11.1, Fast Retailing at 32.4 is definitely expensive. But it is also in between Western rivals Inditex (that owns Zara) and Swedish H&M that currently trade at 21.6 and 56.1 respectively. The 12-month target price for the Tokyo listing is just 7% above ¥27.99k per share as of March 19. It is safe to suggest that the stock is close to its fair value at the moment.

Conclusion

Fast Retailing seems underrated, unbefitting for the world's third-largest maker of private-label apparel by revenue. However, it is already the number one brand in Greater China , a fact unbeknown to many outside the region. And the Chinese apparel market has already leveled up to the American, the global leader. It is partly because of such fortuity that Tadashi Yanai has not given up on his long-harbored ambition of turning Fast Retailing into the world's top fashion group. More fundamentally though, it is about the principles that UNIQLO espouses that seem to do well in today's environment of high uncertainty.

For further details see:

Fast Retailing: The Dream Of Global Domination Is Very Much Alive