FAST - Fastenal Company Is On Sale Again

2023-11-21 10:16:24 ET

Summary

- Fastenal Company has had a strong track record of performance, outperforming the S&P 500 over the past decade and a half.

- The company is engaged in the wholesale distribution of industrial and construction supplies, serving various markets including manufacturing and non-residential construction.

- Fastenal's balance sheet, revenue growth, and earnings growth all meet positive criteria, indicating a favorable outlook for the company.

Introduction

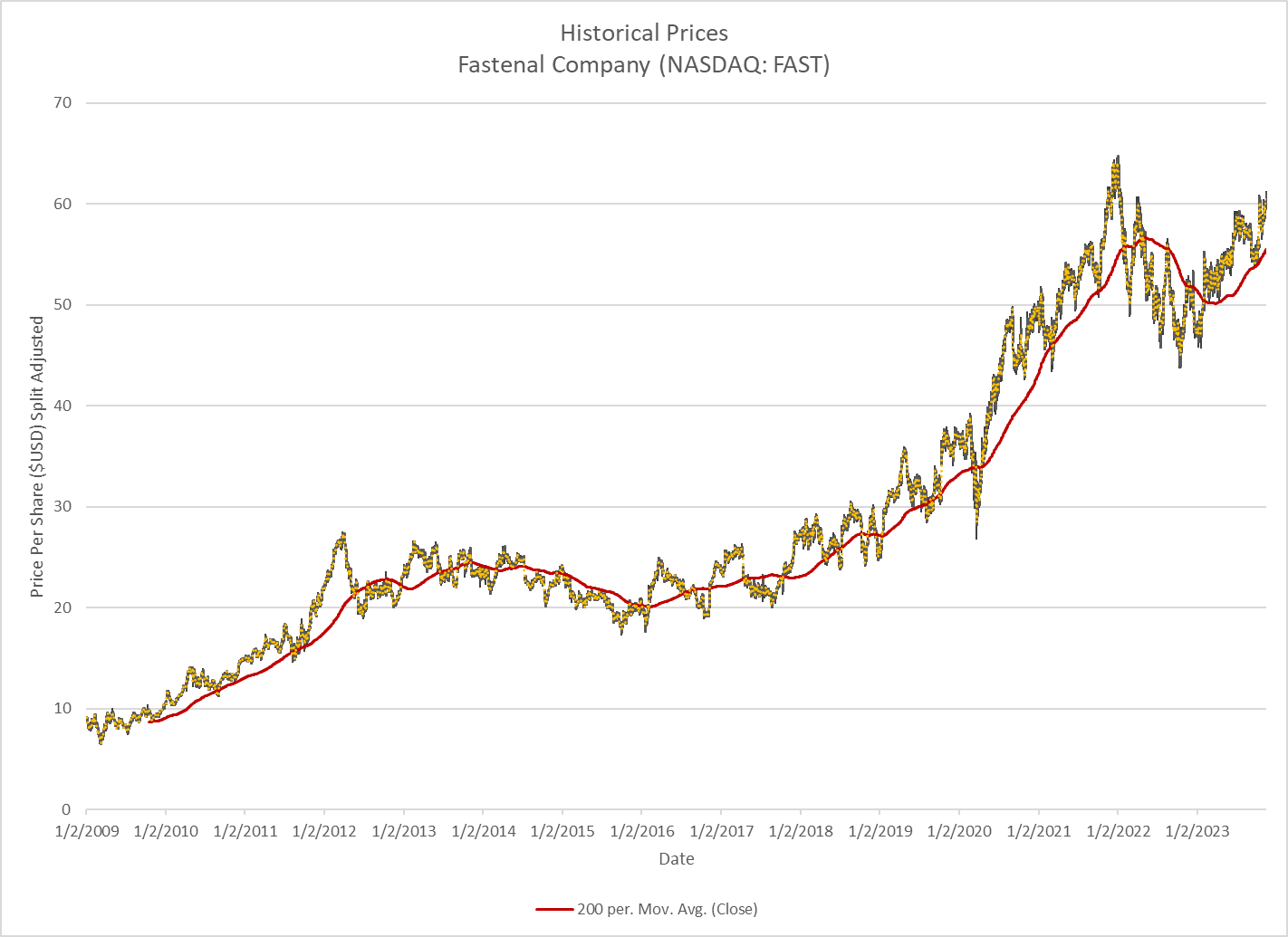

Fastenal Company ( FAST ) is one of my favorite companies to follow. It feels like a little train that keeps chugging along. Since the beginning of 2009 when it first hit my screens, it has had a total return of an annualized 16.49% (±25.70%). This is a far better return than what one would have expected from the S&P 500’s return of 13.32% (±15.28%). As the chart clearly shows, it has been a good run for Fastenal for the last decade and a half.

FAST Historical Prices (Author)

{kind=link}

According to Reuters , "Fastenal Company is engaged in the wholesale distribution of industrial and construction supplies." The Company distributes threaded fasteners, bolts, nuts, screws, studs, and related washers, as well as miscellaneous supplies and hardware. Their main customers are construction workers, but they also distribute their products to farmers, truckers, and railroads. Those companies engaged in oil exploration, production, and refining also are part of Fastenal's customer base. They are also a supplier to mining operators and various government entities.

This is how others rate Fastenal Company:

- Morningstar – Buy

- Zacks – Buy

- The Street – Buy

- HSBC Securities—Hold

- Consensus – Hold

After Fastenal came out with their third-quarter earnings, this is what was said :

- “The results look OK, and investors are relieved.”

- The quarter was, “solid with continuing themes of overall slow growth.”

- “There are signs of improvement in the numbers.”

Methodology Disclosure

I am a quantitative analyst. I put little stock in making future predictions about what a company will or will not do. My preference is to analyze the revenue of a company over the last five years and make determinations for earnings and free cash flow from there. I contend that most financial results for a company are the function of sales. The direction of sales dictates everything else for a corporation and one will that is the basis of all analysis I do.

Balance Sheet

Any passing company must have a clean balance sheet. These are my criteria, and how FAST compares. All criteria are a modified screen that I adopted from Harry Domash's "Bulletproof Stocks" method. I consider Harry a mentor.

- Debt-to-Equity is 0.16

- Must be less than 0.4.

- The current Ratio is 4.71

- Must be greater than 1.5.

- Altman-Z is 22.62

- Must be greater than 3.0.

- Free Cash Flow is $7.28B

- Must be positive.

All the metrics have a passing grade.

Revenue Analysis

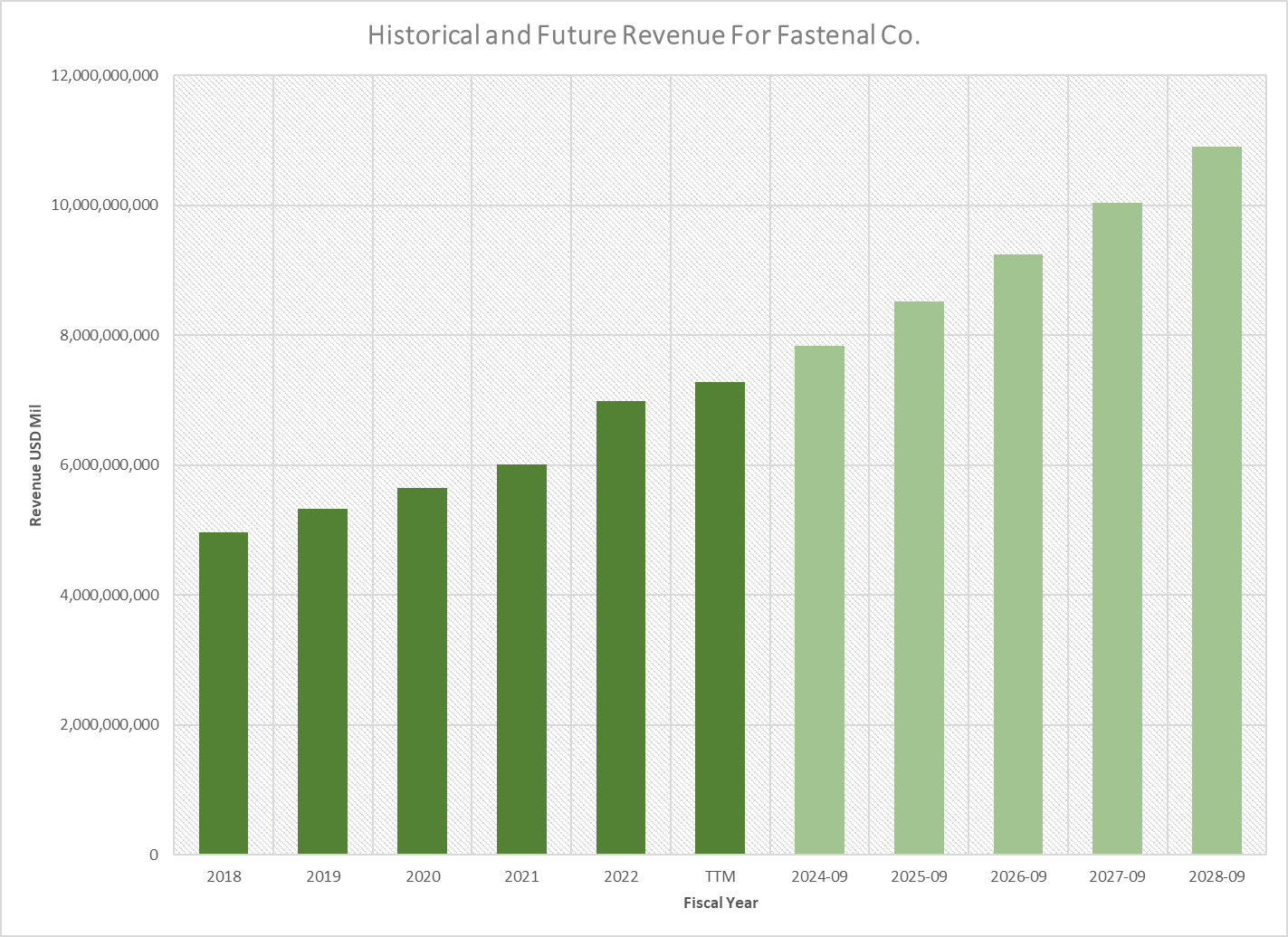

FAST has seen its revenue grow at an annual rate of 7.60% since 2018, and it has a regressed growth rate of 8.41%. Its historical price-to-sales ratio has been as low as 3.95 and as high as 5.96. Its five-year average is 4.78.

FAST Historical Revenue (Author)

{kind=link}

FAST has a historical beta of 0.86 which gives me a required rate of return of 9.30%. Based on historical metrics, these are the present values for FAST determined by revenue growth:

- Bearish Case: $55.75/share

- Bullish Case: $78.19/share

- Fair Value: $65.01/share

Earnings Analysis

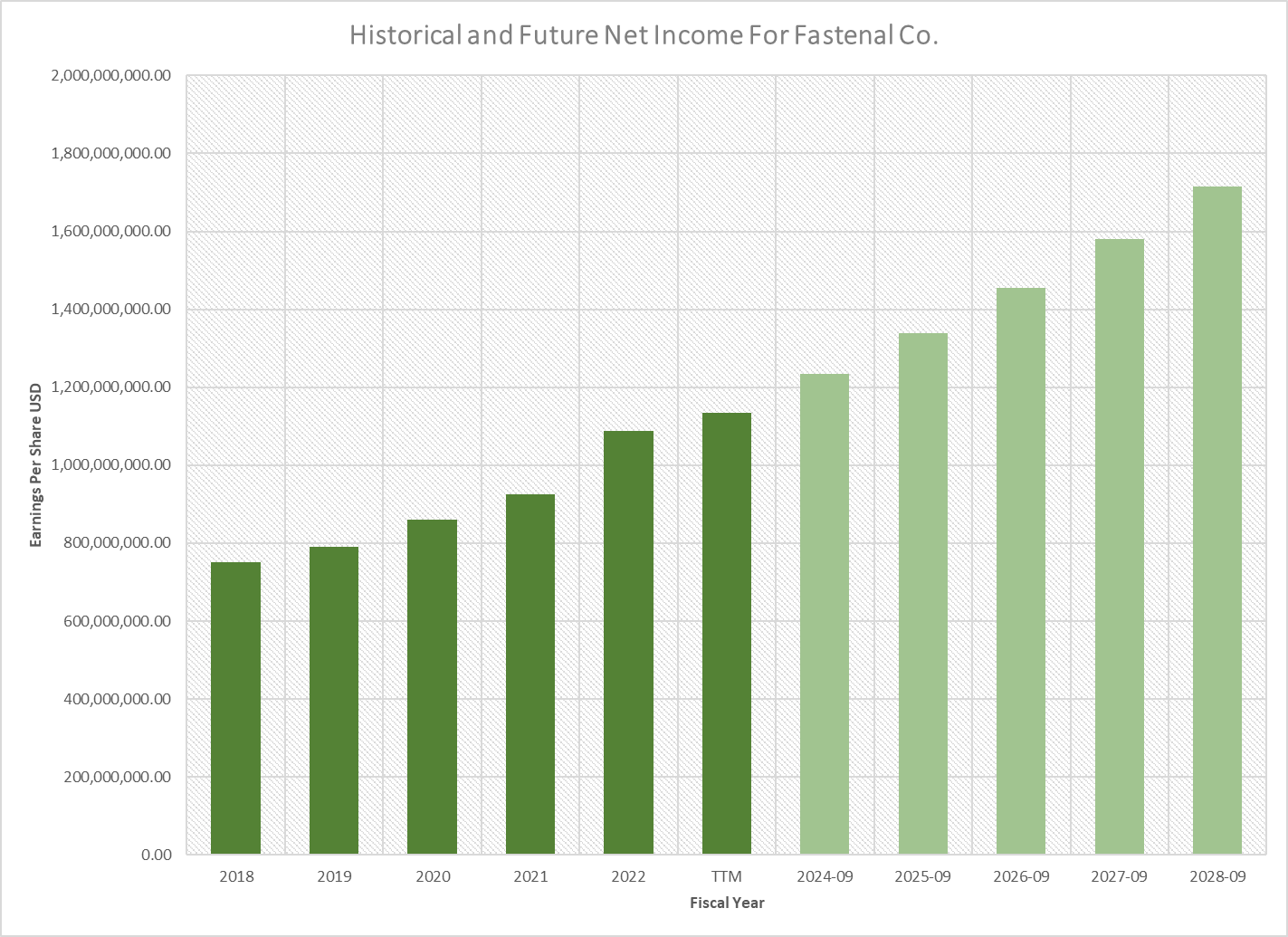

FAST is in a high-growth industry where earnings growth averages 23.89%, while its earnings per share have grown a more mundane 9.59%. Gross margins do average around 45% and net income from continuing operations averages around 16%. Those numbers have been consistent over the last five years. Due to better efficiencies in their operations, I see future EPS growth at 10.08%

FAST Historical Earnings (Author)

{kind=link}

Historically, Fastenal's Price/Earnings ratio ran from a low of 20.35 to a high of 41.52. The five-year average for the P/E ratio is 29.07. Here is how I see the value of FAST as determined by earnings growth:

- Bearish Case: $47.39/share

- Bullish Case: $84.57/share

- Fair Value: $62.70/share Free

Cash Flow Analysis

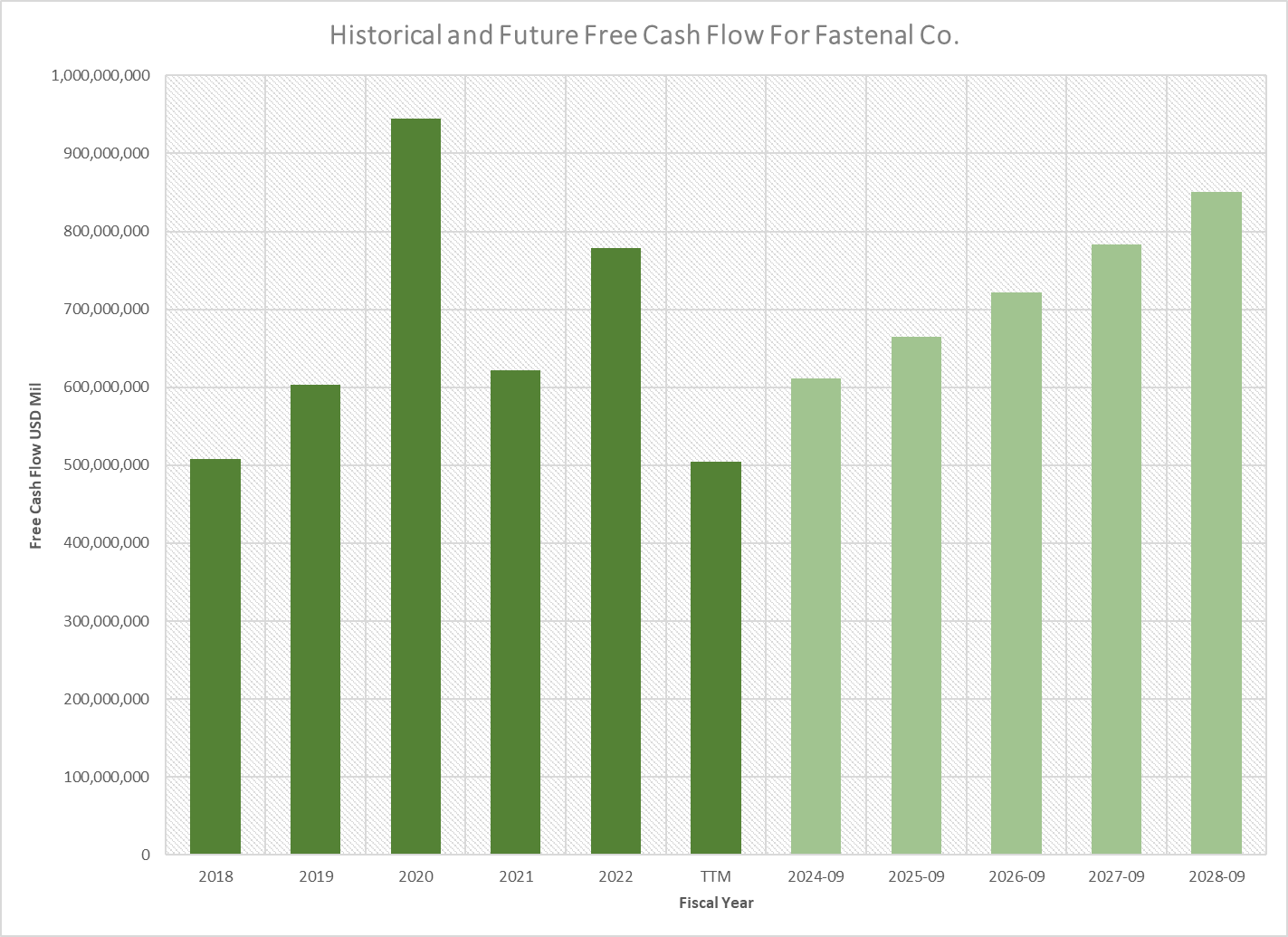

FAST had choppy free cash flow over the last five years. For me, I only want surety that it will remain positive over the next few years, and it will. While that is important, I also do not want to overpay for the positive outcomes.

FAST Historical Free Cash Flow (Author)

{kind=link}

I see the company’s cost of debt at 6.21% and its WACC at 9.30%. When I conduct my sensitivity tests, I usually assume an assumed long-term growth rate of 1%-3%. I wish my trends from the past were smoother, but I do like the consistently positive results. With my head slightly covered due to embarrassment, here is the present value of FAST based on free cash flow:

- Bearish Case: $19.38/share

- Bullish Case: $26.23/share

- Fair Value: $22.21/share

Growth Rating

We now have three net present values for Fastenal and are now able to give it a growth rating.

So here is how Fastenal rates:

- The minimum is one point

- Financial Health: Safe

- Add one point

- Revenue Analysis

- Present Value Based on Revenue > Current Price

- Add one point

- Earnings Analysis

- Present Value Based on Earnings > Current Price

- Add one point

- Free Cash Flow Analysis

- Present Value Based on Free Cash Flow < Current Price

- Zero points

- Growth Rating: 4-Star ((BUY))

Dividend Analysis and Rating

Fastenal popped up on my GARP screen, so I certainly was not looking for a dividend payer. Yet, it does pay a nice distribution, so I consider it a GARP stock with a dividend kicker.

- The current yield is 2.33% and the historical yield is 2.22%.

- Must be greater than 2%

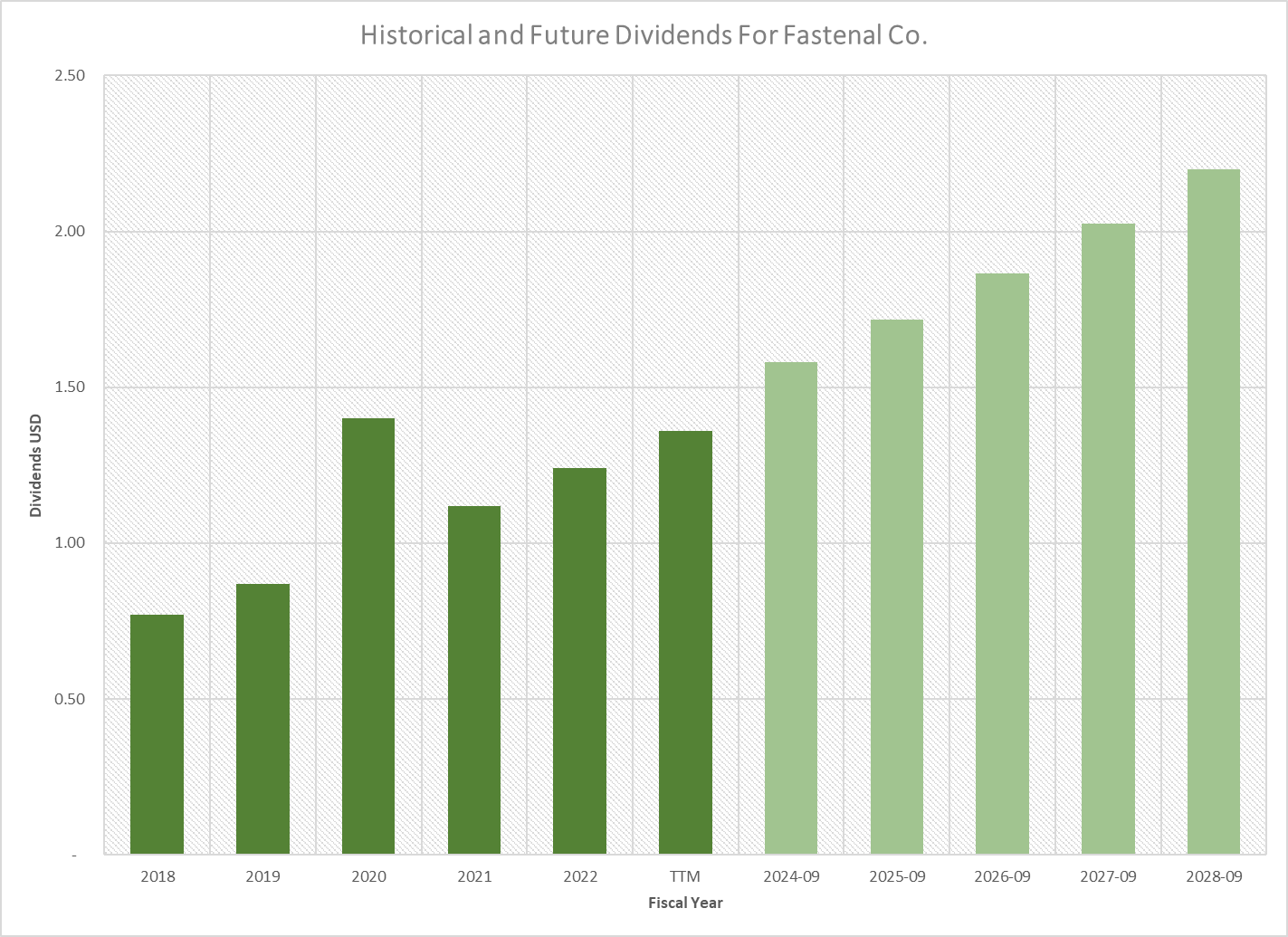

- Annual dividend increases do not always occur, and even decrease instead. This occurred during uncertain periods such as 2008 and 2020. That is a sign of Fastenal’s fiscal prudence. I do like the fact that dividends have increased at an annualized rate of 15.28% per year. I anticipate dividends to continue to increase barring any economic catastrophes.

- Must increase for at least ten consecutive years.

FAST Historical Dividends (Author)

{kind=link}

I am assuming a future dividend growth rate to be in line with the EPS growth rate of 10.08%. Based on a constant growth model, I see this as $66.97/share stock, and based on a non-constant growth model, it is worth a present value of $69.70/share.

Here are my ratings of FAST based on its dividend history:

- The minimum is one point

- Financial Health: Safe

- Add one point

- Current Yield > 2%: Pass

- Add one point

- Free Cash Flow Analysis

- Present Value Based on Free Cash Flow < Current Value

- 0 points

- Discounted Dividend Analysis

- Present Value Based on Dividends > Current Value

- 0 points

- This is because of its lack of annual dividend increases for the last ten years.

- Income Rating: 3-Star (Hold)

My Take

Periodically, I do recommend Fastenal to beginning investors. It has a wonderful history of appreciation over the years that did not lead to demoralizing feelings one can realize in the investment markets. Its classification as an income stock will depend on whether it can maintain annual dividend increases.

For further details see:

Fastenal Company Is On Sale Again