FAST - Fastenal: Intriguing Story But Too Steep Price

2023-09-19 16:30:12 ET

Summary

- Fastenal Company manufactures and sells industrial and construction supplies to businesses.

- The company has demonstrated impressive long-term financial performance with stable growth and margins.

- The current valuation of the stock is excessively high with a significant DCF model downside, leading to a sell-rating at the current price.

Fastenal Company ( FAST ) manufactures and sells industrial and construction supplies to businesses. The company has demonstrated very impressive long-term financials. As the company’s valuation reflects an excessively good performance from the company, though, I have a sell-rating for the stock at the current price.

The Company

Fastenal provides industrial supplies – the company’s offering includes products such as screws, safety gloves, and electrical tools:

Fastenal's Offering (fastenal.com)

{kind=link}

The company sells these products mostly in the United States, Canada, and Mexico, but does also sell internationally.

Fastenal’s stock price has risen by around 122% in the past ten years, translating to a CAGR of 8.3%:

10-Year Stock Chart (Seeking Alpha)

{kind=link}

In addition, the company pays out a quarterly dividend , with an estimated forward yield of 2.54%.

Financials

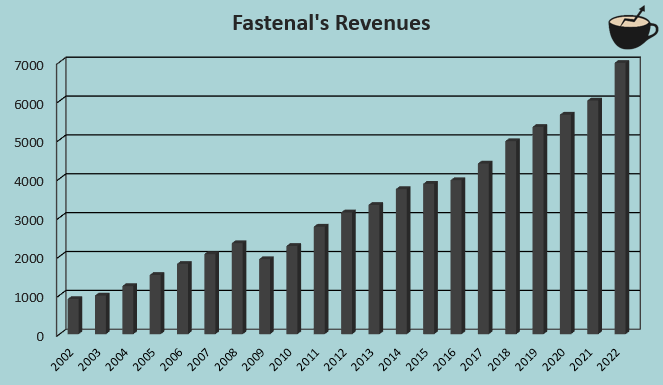

The company has achieved a very good compounded annual growth of 10.8% from 2002 to 2022 in a very stable manner.

Author's Calculation Using TIKR Data

{kind=link}

Impressively, the growth has been mostly achieved organically – Fastenal has less than $300 million in cash acquisitions from 2013 to 2023. Compared to the company’s current market capitalization of around $32 billion, the acquisitions seem to play a very minimal part in Fastenal’s story.

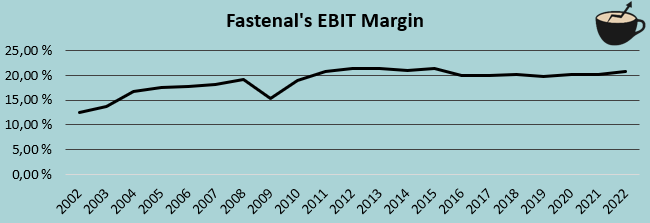

More than just a good growth rate, Fastenal has achieved a stable and high EBIT margin. The company’s trailing margin stands at 20.7%, a very healthy rate around the company’s medium-term average:

Author's Calculation Using TIKR Data

{kind=link}

Demonstrating Fastenal’s margin stability, from 2012 to Q2/2023, the company’s margin has fluctuated between a very tight range on a quarterly basis – in the period, the company’s lowest margin is 18.68% and highest is 22.65%; very few companies are able to keep such a stable margin.

Many of the companies that I’ve recently written about have recently seen declining earnings as interest rates have risen and as the economy’s having some turbulence – Fastenal on the other hand has only reported growing earnings. In the first half of 2023, Fastenal’s EBIT rose by 6.3% from the previous year’s period. In the company’s Q2 earnings presentation , the company commented the quarter to have been challenging – I don’t see such challenges in the achieved financials.

Fastenal’s balance sheet is quite non-threatening – the company has around $350 million in long-term debt, a very low amount compared to the company’s size and its earnings. Of the debt, $150 million is in current portions. The company has kept its debt level very low for a long period. Although this decreases the risk level for investors, I believe a higher amount of debt would provide Fastenal with a cheaper financing alternative, creating shareholder value for investors. Fastenal also has a healthy cash balance of around $244 million.

Valuation

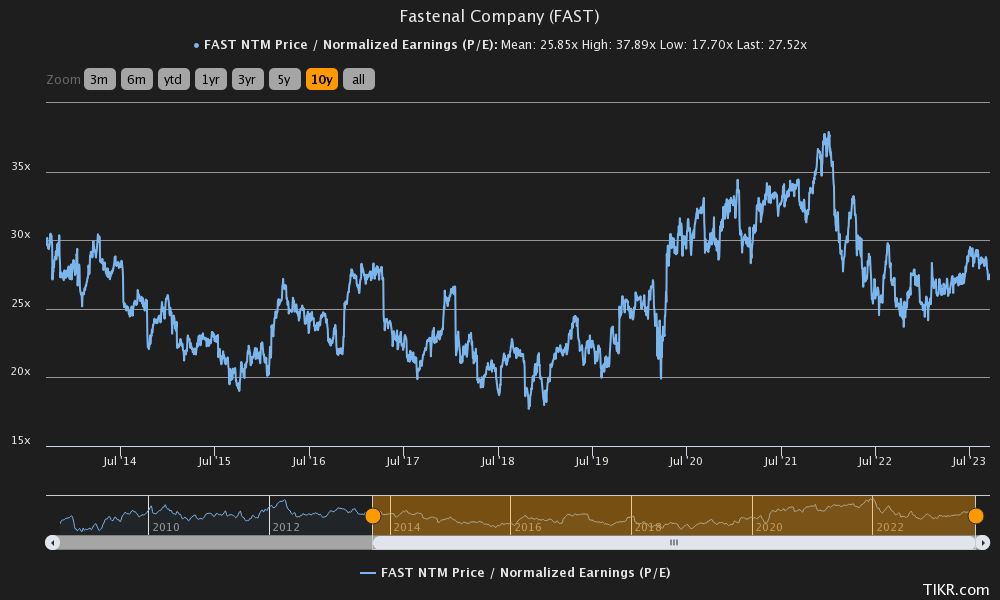

Although the company has very impressive financials, I am not so optimistic about Fastenal’s valuation. Fastenal currently trades at a forward price-to-earnings ratio of 27.5, around the company’s ten-year average of 25.9.

{kind=link}

As interest rates are currently higher than in the period, a higher required rate of return should be expected – I don’t see the current price as a good opportunity looking through this lens.

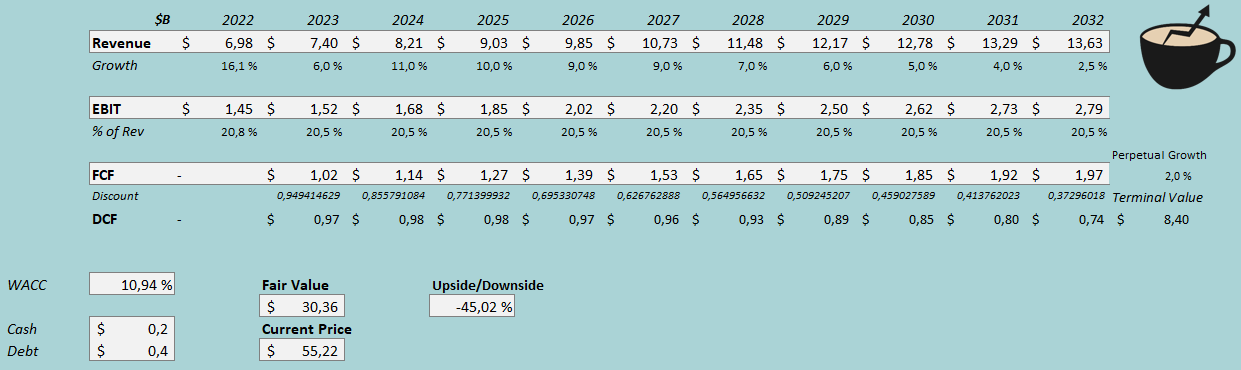

To get a better grasp of the valuation, I constructed a discounted cash flow model in my usual manner. In the model, I estimate a slightly lower growth for 2023 than the company’s historical rate, as in H1 the company only had a growth of 7.5% - I conservatively estimate a growth of 6% for the year. Going forward, I estimate Fastenal to accelerate the growth from 2023 with a growth of 11% in 2024. After the year, I estimate the company’s growth to slow down in steps into a perpetual growth of 2%. The DCF model’s estimates amount to an estimated revenue CAGR of 6.9% from 2022 to 2032.

As for Fastenal’s margin, I estimate further stability – I have a stable margin of 20.5% in 2023 as well as the company’s entire future. I don’t see any catalysts to estimate a varying margin from Fastenal’s medium-term history. These estimates along with a cost of capital of 10.94% crafts the following DCF model, with an estimated fair value of $30.36, around 45% below the stock’s current price, signifying a substantially overvalued stock:

DCF Model (Author's Calculation)

{kind=link}

Fastenal could potentially surprise the DCF model's estimates to the upside, creating a fair value that's closer to the current price; for example, the company could expand its margin or have a growth that's greater than in my estimates - the CAGR of 6.9% is lower than Fastenal's historical rate.

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Fastenal had $2.9 million in interest expenses. With the company’s current amount of interest-bearing debt, Fastenal’s interest rate would be 3.31% - the company seems to have managed to keep a very good interest rate. Fastenal’s debt-to-equity ratio has been historically very low though – in the model, I estimate a long-term debt-to-equity ratio of only 5%.

For the risk-free rate, I use the United States’ 10-year bond yield of 4.34%. The used equity risk premium estimate of 5.91% is Professor Aswath Damodaran’s latest estimate .

Yahoo Finance estimates Fastenal’s beta to be 1.15 – the company has kept a very good earnings level despite a turbulent current economy, and in the financial crisis Fastenal’s operating income only fell by 34% for a single year. I believe the beta could be significantly lower in the future, as Fastenal has demonstrated stabile earnings throughout economic turbulence with very little debt, but for the time being, I use Tikr’s estimate in my CAPM.

Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 11.39% and a WACC of 10.94%, used in the DCF model.

Takeaway

Fastenal is an amazing company with a very impressive past. Unfortunately, though, I have to have a negative view of the stock as an investment at the current price – the price seems to price in way too much from the company as my DCF model estimates a downside of 45%. Even with a lower beta of 0.8, that could be theoretically argued for the stock, the DCF model would point towards a downside of 29% - with a beta of 0.46 the stock would be correctly priced with my DCF model estimates, a figure around Walmart’s beta of 0.49. I don’t see such a beta as reasonable.

If the stock price falls, I would be ready to change my view of the investment opportunity. For the time being, though, I have a sell-rating for the stock.

For further details see:

Fastenal: Intriguing Story But Too Steep Price