FAST - Fastenal Q4 Earnings: Softer Manufacturing Environment Shares Adequately Priced

2024-01-18 09:15:49 ET

Summary

- Fastenal Company, the wholesale distributor of industrial and construction supplies, just reported its Q4 financial results.

- Heading into the release, shares have outperformed over the past one year, up over 30%.

- The share price strength is despite weaker operational performance with respect to the company’s overall growth in daily sales.

- I also view the softer manufacturing end market as a key consideration for the future outlook.

- At current trading levels following the release of Q4 results, I view Fastenal Company shares as adequately priced.

Shares in industrial wholesale distributor, Fastenal Company (FAST) have outperformed over the past year. The stock price has gained over 30% during this period. This compares to a more modest gain of about 11.5% in the broader Vanguard Industrials ETF ( VIS ).

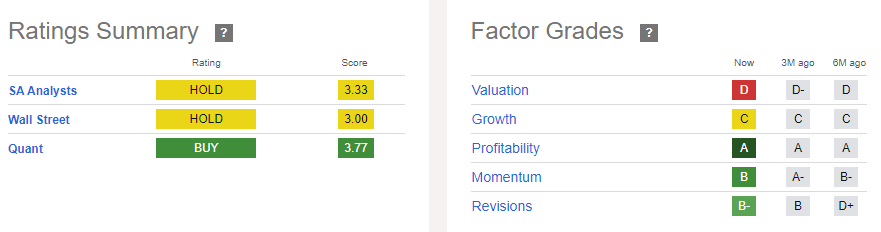

The positive momentum, as well as FAST's strong profitability and cash flow profile, are but a few factors that are contributing to the continued "buy" rating by Seeking Alpha's ("SA") Quant Factor Grades .

Seeking Alpha - Ratings Summary Of FAST Stock

{kind=link}

Wall Street and the broader SA community , including me, are less bullish on FAST's prospects. In prior coverage, I've cited the softer manufacturing environment and the company's declining daily sales rate ("DSR") growth as factors to consider prior to new or further initiation in the stock. My more neutral stance hasn't aged well, as the stock is up about 13% since my last update .

At this point following Q4 results , which came in ahead of expectations, I still believe a neutral position is warranted on Fastenal, given the stall in economic activity and the overall high bar for continued outperformance in the company's stock.

Macroeconomic Considerations For FAST Stock

Industrial production activity, as measured by monthly PMI, is a key metric associated with FAST's operational performance; and more specifically to the company's OEM-oriented fasteners. Through the 2023 fiscal year, softer readings in the metric have correlated with a decline in DSR growth.

While U.S. industrial production ticked higher in December, overall PMI still remains in contractionary territory. And in the Federal Reserve's most recently released Beige Book survey of regional business contacts, nearly all districts reported decreases in manufacturing activity over the reportable period.

In the periods ahead, the weakness in activity would most likely be felt within FAST's product categories that are more heavily oriented toward production of final goods, such as fasteners, which are more susceptible to weaker manufacturing end markets.

FAST Stock Q4 Headline Results

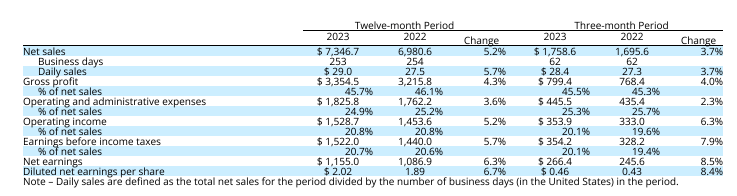

In the final quarter of the fiscal year, FAST grew YOY net sales by 3.7% and reported overall EPS of $0.46/share. Both came in ahead of consensus estimates. For the full fiscal year, YOY net sales grew 5.2%, driving overall EPS growth of 6.7%.

FAST Q4 Earnings Release - Snapshot Of Q4 And Full Fiscal Year Operating Performance

{kind=link}

During the fiscal year, FAST benefitted from incremental pricing actions taken over the past twelve months, as well as by growth in the number of Onsite locations. This was offset in part by a continued divergence in the sale of fasteners, which are core to FAST, and non-fastener product lines. The divergence, in turn, negatively impacted the company's DSR growth and held back overall margin performance.

Key Takeaways From FAST Q4 Results

Continued Weakness In DSR: Weaker manufacturing end markets have negatively impacted FAST's DSR growth through the fiscal year. In Q4, DSR increased 3.7%, down from 4% growth in the quarter prior and 10.7% in the same period last year.

FAST Q4 Supplemental Presentation - Recent Quarterly Snapshot Of FAST DSR Growth

This is largely reflective of the softer overall industrial environment. In Q4, for example, U.S. PMI averaged 46.9, representing 14 consecutive months of contracting manufacturing activity.

In a more promising angle, the declining growth rate appears to be reaching a bottom. In December, DSR grew 5.3%, which was above normal sequential seasonality, according to the company's quarterly presentation .

Onsite Signings Shy Of Estimates: An important growth driver for FAST is increasing the number of their in-market locations. These include traditional branches, international brands, and Onsites, all of which enable FAST to operate closer to their customers. The most in-focus of the three are Onsite signings. In 2015, Onsites were 9.1% of FAST's in-market locations. By 2023, its share had risen to over 50%.

In 2023, the company reported 326 signings, including 58 during Q4. This builds upon gains from prior quarters. While positive, the total did fall below expectations. During the Q3 conference call , FAST President and CEO, Dan Florness, did guide for ending the year at 350 signings. The guide was already lower than the 375 to 400 range provided at the end of 2022. In missing the target for FY23, I am less confident that FAST can hit the current goal outlined for 2024 - 375 to 400 locations.

Continued Strength In Margin And Cash Flow Profile: Despite weakness elsewhere in the business, FAST has benefitted from incremental pricing actions. In Q4, gross margins held in the mid-40% range and were up slightly YOY. Though operating margins exhibited a sequential decline, they were still up YOY despite lower DSR growth.

FAST also reported record operating cash flow in 2023. This was primarily due to reduced working capital needs, as well as greater inventory efficiency. The stronger cash flow profile likely contributed to the company's recently announced special dividend of $0.38/share, a healthy complement to the reoccurring quarterly payout, which itself was just increased to $0.39/share.

Is FAST Stock A Buy, Sell, Or Hold?

Over the past 52 weeks, shares in Fastenal have reached new highs. The stock, moreover, continues to trade near the upper boundaries of its yearly share price range. This is despite the company's operational performance in a challenged macroeconomic environment. The growth rate in daily sales, for one, have continued to decline. And industrial data remains soft, with PMI readings still below the 50.0 mark. Barring a reversal in these metrics, I believe shares in FAST should remain on "hold."

Existing investors who are long-time shareholders in Fastenal Company could celebrate cashing in on the company's reliable dividend payouts. In 2023, the reoccurring payout was increased by nearly 13%. The company also had ample flexibility in declaring a special dividend at year end. This was made possible due to Fastenal's reduced working capital needs and the stronger resulting cash flow profile.

But for new investors or those looking to add to their current positioning, Fastenal Company stock lacks sufficient appeal at current trading levels. Shares are up over 30% in the last year, and they are currently trading about 6% above Wall Street's target price. While I don't view shares as a sell, I believe investors could benefit by waiting for a better buy-in price, perhaps near the $55/share mark. Until then, I would view shares as a continued "hold."

For further details see:

Fastenal Q4 Earnings: Softer Manufacturing Environment, Shares Adequately Priced