FAST - Fastenal: Stock Will Probably Remain Under Pressure In 2023

Summary

- District and regional feedback from Fastenal Company leaders points to a challenging 2023.

- After it topped off at close to $63.50 per share on Dec. 2021, Fastenal Company has steadily dropped from there.

- Based upon management expectations and the recent trading pattern in Fastenal Company stock, the price has a ways to go before bottoming out.

- Some spot prices for inputs have fallen, such as fuel, transportation services, and steel, but it'll take several quarters before it has an impact in Fastenal's costs of goods.

For a business competing in the market it does, Fastenal Company ( FAST ) has had a nice run since August 2017, when it was trading at approximately $20.00 per share. It jumped to about $63.50 per share in December 2021 before falling to a 52-week low on October 14, 2022, and now trading at a little over $47.00 per share as I write.

{kind=link}

The company is now in its historically slow fourth quarter, and after getting feedback from district and regional managers, it looks like it's going to struggle to regain that momentum, based upon its customers telling them they aren't optimistic about their prospects for 2023.

They aren't pointing to a total economic collapse, but the lack of clarity has management in many companies tightening up spending because of the uncertain economic outlook for the next year or so.

As for its most recent earnings report, a decline in gross profit margins and an increase in the cost of sales, combined with management saying it was in preparation for a "softer" 2023, didn't immediately have an impact on the share price of the company to the downside. It began a temporary run after the earnings report from a little under $44.00 per share to close to $53.50 before pulling back.

While somewhat surprising, I don't see the tailwinds heading into 2023 that would justify the share price climbing on a sustainable basis, but rather heading back down after the expected weaker, seasonal fourth-quarter earnings report, and from there dropping further if the assumptions of weaker demand are how it plays out.

In this article we'll look at a few of its numbers from the last earnings report, the probable competitive environment in 2023, and how it's likely to affect Fastenal Company's share price based upon recent downward movements.

Some of the latest numbers

Revenue in the third quarter was $1.8 billion, compared to $1.55 billion in the third quarter of 2021. For the first nine months of 2022 revenue was $5.3 billion, compared to $4.5 billion in revenue for the first nine months of 2021.

Net earnings in the third quarter were $284.6 million or $0.50 per share, compared to $243.5 million or $0.42 per share in the third quarter of 2021. Increasing pricing on products from 550 to 580 basis points was the primary reason for the improvement in net earnings year-over-year.

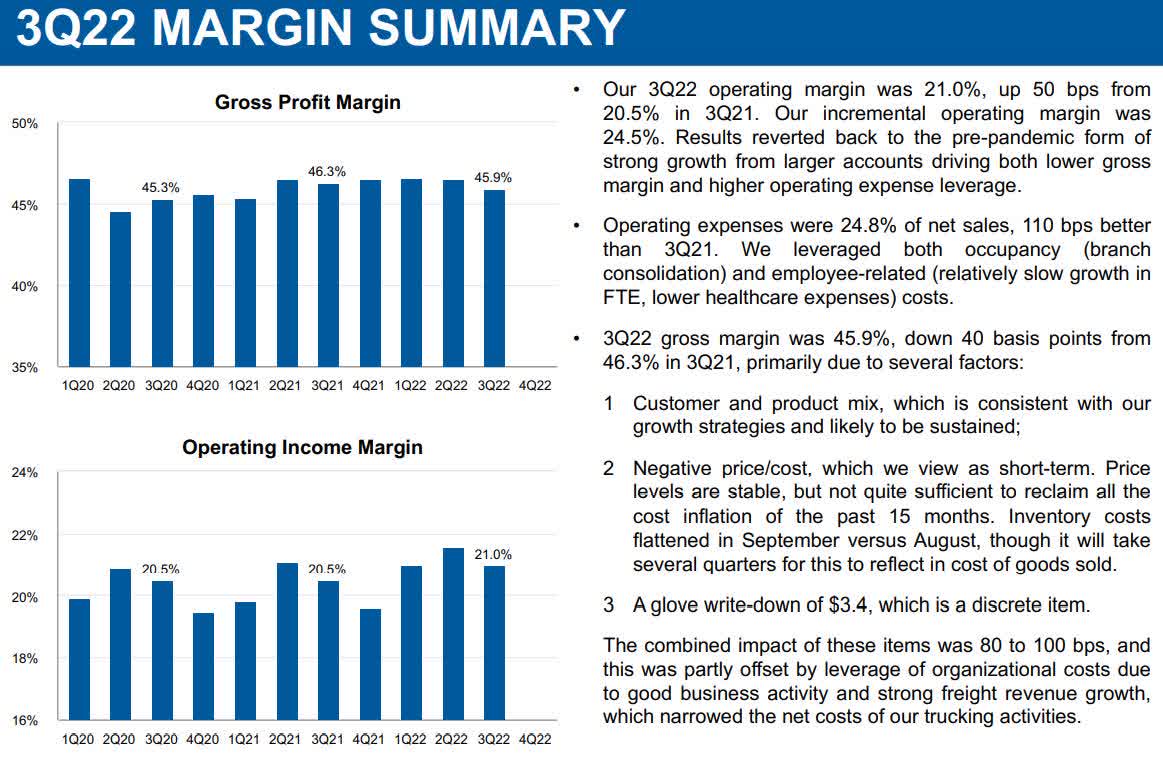

Gross margin in the reporting period was 45.9 percent, down 40 basis points from gross margin of 46.3 percent in the third quarter of 2021. Gross profit margin in the third quarter was 21 percent, up 50 basis points from 20.5 percent gross profit margin in the third quarter of 2021.

{kind=link}

Gross profit as a percentage of sales fell to 45.9 percent in the third quarter of 2022 from 46.3 percent in the third quarter of 2021. That was attributed to unfavorable product/customer mix, unfavorable price/cost, and writing down some of its gloves held in inventory.

Interest expense in the quarter was $3.9 million, compared to $2.3 million in the third quarter of 2021, primarily from an increase in debt and higher average interest rates in the reporting period. This will probably get worse before it gets better depending on the level of debt the company takes on going forward. We already know interest rates are going higher in 2023.

Cash and cash equivalents at the end of the third quarter of 2022 was $231.5 million, down from the $236.2 million in cash and cash equivalents it had at the end of calendar 2021. Long-term debt at the end of the third quarter was $404.7 million.

Softer 2023

I think the most important thing coming from the Q3 earnings call was the revelation from management that it is in preparation for a softer 2023.

The two major reasons are, first, the fourth quarter is historically its weakest, and coming off of that and heading into a weak 2023 will probably result in the share price of the company taking a hit because of expectations of the company's momentum slowing as it starts off in 2023.

Revenue from September to December normally runs 12 percent to 13 percent lower than other quarters, so if softness remains in the following quarters, it's going to cause some underperformance in the company's results.

The second and more important reason for the long term is after talking to its district and regional managers, the feedback they received from their customers was not encouraging, as they have little confidence in how business will be in 2023. Those customers said they are preparing for a weak economic environment in 2023, and are the result will be more of a defensive posture than an offensive one. This means spending is likely to be down, which will have an impact on the revenue of FAST. That means they're being much more cautious in their spending in order not to get ahead of themselves.

Because FAST has signed a significant number of Onsites in 2022, management feels it has some support for 2023. However, it's still making spending decisions, including in hiring, based upon what is visible to them and not what they aren't sure about.

Under that scenario, if the economy surprises to the upside, it'll take time to respond and take advantage of an improved economic environment.

As mentioned earlier, improvement in the cost of some inputs is going to probably take close to the end of 2023 before it has an impact on the performance of FAST.

Share price movement

Taking into account the probable softness of 2023 and the time it takes for lower costs to have an impact on the company's numbers, my expectations are that the share price of FAST is going to be under pressure until the economy shows signs of sustainable improvement.

And looking back over the last year, the price movement of its share have been very close to roughly $13.00 per share every time it corrected. If you look at the chart for the last year, you'll see that the three times the share price of the company took a dive, it did so at a predictable level. While that doesn't guarantee it'll happen that way again, it does provide a recent pattern that has a good chance of repeating itself because the movement of its share price reflects shareholder sentiment.

Most recently, it topped off at about $53.50 on December 13. If recent history repeats itself, we could see it test the $40.00 per share mark in the near term.

And if fourth quarter numbers come in lower as usual, and management commentary provides more caution for 2023 because of more clarity from its customers, the share price of FAST is going to fall a lot further in my opinion, as investors sell off to protect the downside.

On the other hand, if there is a more positive outlook from management going forward, it will provide a nice tailwind for the company, assuming it is the type of news that has the potential for sustainable improvement. If it doesn't, it could provide a temporary boost in its share price, but would pull back if there's nothing to support it over the long term.

Conclusion

The type of business Fastenal Company is in is one that is going to grow on an incremental basis long into the future, but it is definitely subject to volatility, as proven by the performance of Fastenal over the last year.

With the current visibility we have concerning the economy and actions by the Federal Reserve, I believe the chances of FAST facing a much slower 2023 are much higher than in facing one that is improving.

Based upon the price movement of Fastenal Company stock over the last year, that would mean more downward pressure, more than likely testing the $40.00 per share market based upon the corrections over the last year, and if economic news gets worse, it'll probably break significantly below $40.00 per share before it finds a bottom.

With investor jitters and the strong potential for economic momentum to slow down further in 2023, it looks like it's going to get worse for FAST before it gets better. The good news is it has been showing signs of improvement in some of its metrics, and when things are clearer and the economy starts to sustainably recover, it could be in for a prolonged upward growth trajectory.

For now, the best way to play Fastenal Company would probably be to wait for a good entry point and then take a position, using a dollar-cost averaging strategy and disciplined positioned sizing to get an attractive cost basis to take advantage of the inevitable return to growth.

Under these economic conditions, Fastenal Company should be considered a long-term holding that will reward shareholders over time.

For further details see:

Fastenal: Stock Will Probably Remain Under Pressure In 2023