BALDF - Fastighets Balder: An Under-Covered European Real Estate Company For Long-Term Investors

Summary

- Balder is a Swedish real estate developer, focused on the residential and commercial segments.

- It has a strong growth track record, showing that its business strategy is sound, but current market conditions are more challenging.

- While its valuation is cheap, its refinancing needs should not be overlooked and for the time being investors should keep out of its stock.

Fastighets Balder ( BALDF ) has a very good growth track record on the Nordic real estate market, showing that its business model is sound over the long term, but its significant refinancing needs in the short term are a key risk for its investment case.

Company Description

Fastighets Balder is a Swedish real estate company, focused on the housing, commercial properties, and new construction projects in several Scandinavian countries, plus Germany and in the U.K. The company was founded in 2005, has a market value of about $5.3 billion and trades in the U.S. on the over-the-counter market. However, it has much more liquidity in its main listing in Sweden, and this is the preferred way for investors to trades its shares.

At the end of September 2022, its asset portfolio was valued at some $20 billion, being one of the largest real estate companies in Sweden. Its business model is to be a long-term owner, generating value through a high level of activity and efficient management, aiming to provide stable cash flows over the economic cycle.

At the end of Q3 2022, the majority of its properties were residential (57% of total), followed by office, retail, and industrial/logistics, which altogether can be considered commercial real estate assets. Its most important regions are Stockholm and Gothenburg in Sweden, and Helsinki in Finland.

Asset portfolio (Balder)

Balder’s major shareholders are Erik Selin (the company’s founder and CEO), who owns 35.1% of the capital and 48.8% of its voting rights, given that as usual with Swedish companies Balder has both A-class and B-class shares with different voting rights (class A carries one vote, each class B share carries one tenth of one vote). Another large shareholder is Arvid Svensson, who holds 7.7% of the company’s capital, thus insiders hold the majority of voting rights, which theoretically should lead to a good alignment between management and shareholders’ interests over the long term.

Business Profile

Balder’s business model is to invest in properties in capital and major cities across Nordic and other developed European countries, having a good diversification regarding property type and geography. Its main goal is to increase the profit from property management per share over the long term, which it has been able to achieve over the past few years.

Indeed, in the past five years, Balder’s profit from property management has increased by some 20% per year, and its net asset value ((NAV)) increased by about 23% annually, which are very good growth rates within the European real estate sector.

Due to this strong track record, the company’s strategy is to reinvest profits in the business, through acquisitions, new construction, and renovation of its existing assets, to generate further growth. Due to this approach, the company does not distribute dividends, which is quite unusual in the real estate market. Thus, its share is not attractive for investors who seek income, being a better match for growth investors who seek capital appreciation over the long haul.

Regarding its growth strategy, Balder has grown historically through acquisitions and new developments, both for its management and developments for sale to private individuals. This means that its capital expenditures are usually quite high compared to its revenue stream, which is also another reason why its management likely prefers to reinvest earnings in the business rather than distributing it to shareholders.

For instance, in the last year Balder’s capex amounted to $2.9 billion, while its rental income was only $1 billion, which means that Balder has invested aggressively in new developments, with the aim of generating value through asset sales. As property markets in the Nordic countries have experienced a slowdown in recent months, Balder is adapting its growth strategy and expects to invest less in 2023 and 2024, to maintain important financial metrics at sound levels.

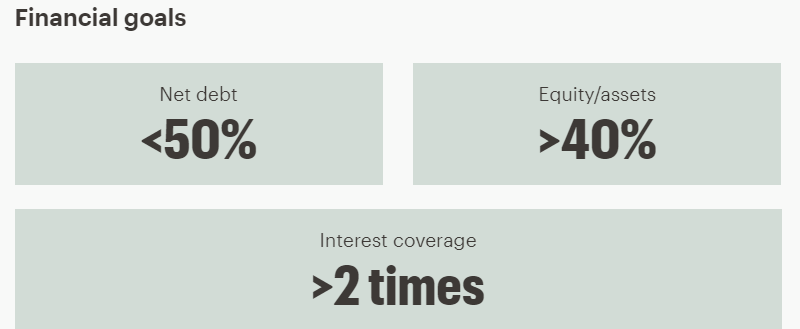

Regarding its main financial targets , its main goal is to maintain a sound financial position and an investment grade credit rating, measured by a net debt-to-assets ratio below 50%, equity-to-assets ratio above 40% and an interest coverage ratio of at least 2x. At the end of Q3, Balder was well within its targets, given that its net debt was 47% of total assets, the equity ratio was 40.4%, and its interest coverage ratio was above 5x. This shows that Balder’s financial position is strong and does not need to reduce financial leverage in the short term, which is positive considering the current down cycle in the property sector.

{kind=link}

Financial Overview & Balance Sheet

Regarding its financial performance, Balder has reported a positive operating backdrop over the past few years, supported by a strong housing segment in Nordic countries and its new development initiatives. Its track record is quite positive, considering that its NAV has increased consistently since 2015, showing that Balder’s growth strategy has delivered good results (NAV of $8.75 per share in Q3 vs. $2 in 2015).

NAV growth (Balder)

During the first nine months of 2022 , Balder has maintained a positive operating momentum, even though economic conditions have deteriorated and property values in Nordic countries are experiencing a correction after many years of rising values.

Nevertheless, Balder’s rental income amounted to $733 million, an increase of 18% YoY, while like-for-like rental income increased by 2.5% YoY. Its profit from property management was $437 million (up by 17% YoY). Due to its active management of properties, its net profit was $886 million in the period, a level that is higher than its revenues due to capital gains from asset sales.

Despite these good financial figures, the negative impact of higher interest rates is already reflected in property values, which have declined and will lead to much lower capital gains in the near future. While Balder’s new developments are mainly at fixed construction costs, new developments will reflect higher costs, while on the other hand prices are down. This means that new construction is much less profitable for developers, which naturally will lead to much lower activity in the coming quarters compared to the past few years.

Regarding its balance sheet, Balder has a sound position right now, but the company has significant debt maturities over the next two years (2023-24), given that about 27% of its total liabilities mature during this period. At the end of Q3, Balder’s liquidity position was only enough to refinance its 2023 maturities, thus the company needs to refinance debt during the coming year to not run out of cash.

Debt maturity profile (Balder)

As current conditions on the capital markets are not particularly good for real estate companies, given that in practice capital markets have been shut for these companies during the past few months due to rising interest rates and declining property values, leading to negative investor sentiment towards the sector, Balder may have some difficulty to refinance coming debt maturities.

This means that the company is likely to resort to secured bank financing in the short term, which will much likely have a higher cost than its current bonds. Therefore, higher funding costs should represent another headwind for earnings growth in the coming years, even though I’m not expecting many issues to refinance debt through Nordic banks as Balder’s credit profile is sound and has an investment grade credit rating (BBB by S&P).

Nevertheless, its refinancing needs are a significant risk in the short term and a factor that investors should monitor closely, as the company does not have enough liquidity to pay its maturing debts over the next couple of years.

Conclusion

Balder is an interesting growth play within the European real estate sector, but its refinancing needs over the next couple of years are quite substantial and may become an issue if the company struggles to raise new debt.

While the company’s valuation is currently quite low, trading at only 0.53x NAV, to become a buyer I would need some positive developments regarding its debt management, which may happen during 2023 if Balder is able to raise bank, or debt, financing.

For further details see:

Fastighets Balder: An Under-Covered European Real Estate Company For Long-Term Investors