FAT - FAT Brands: Growing Number Of Restaurants But Short On Cash

Summary

- FAT Brands is a micro-stock but with an enterprise value of $1.29 billion; huge potential but high debt intake for acquisitions is proving costly as interest expenses soar.

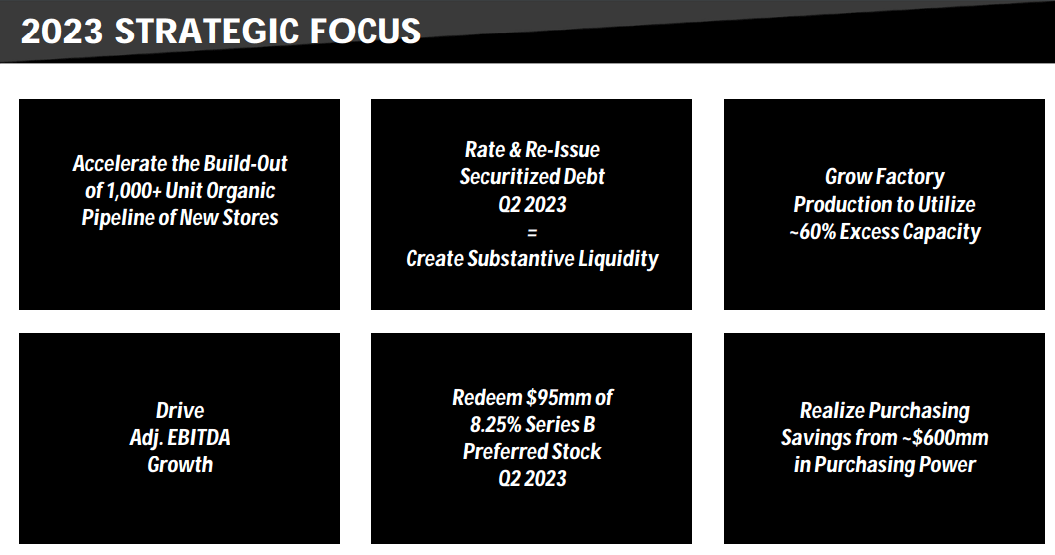

- FAT Brands missed earnings expectations but is on target to open 125 new restaurants in fiscal 2022, with a robust pipeline of over 130 new restaurants for 2023.

- The company recently withdrew an intention for a common stock offering, both actions were poorly received by the market.

- I'm cautious due to the challenging operating environment, cancelled and closed restaurants, interest rates at 15-year high and reduced consumer spending.

FAT Brands Inc. ( FAT ) is an exciting franchising company with tremendous upside potential at a market cap of only $90.98 million, while its enterprise value is a whopping $1.29 billion. FAT grew its asset-light business model into a massive entity over the last two years, with a significant number of restaurants across the globe through its portfolio of seventeen food and restaurant brands.

{kind=link}

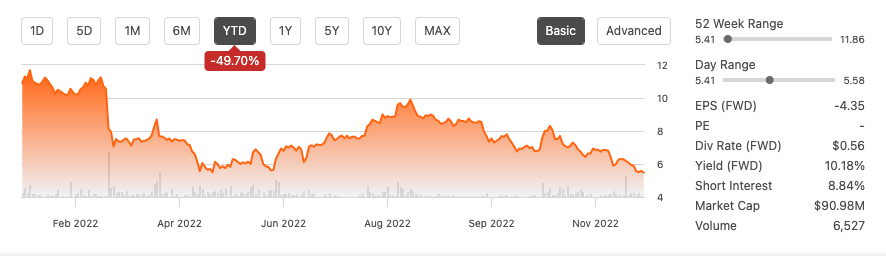

However, its aggressive growth strategy and high leverage is looking increasingly risky in an environment with rising interest rates that have yet to control growing inflation and are impacting consumer buying decisions. The stock has lost 49.70% in value year to date, and recently it withdrew an intention t o a common stock offering . The market poorly received both actions. Furthermore, the Q3 results missed EPS expectations by $0.57 and showed increasing cost pressures and a severe lack of cash from operations. Although I believe in the FAT journey, the high debt, the insufficient cash funds and growing expenses under the current market conditions are too high to maintain my Buy status and downgrade the stock to a Hold position.

The Company

FAT is a multi-brand restaurant franchising company that has been public for five years. It has grown from a single branded company to a portfolio of seventeen brands with over 2,350 locations and 760 franchisees, of which more than 325 are multi-unit operators across forty countries. The company acquired multiple brands by raising debt through issuing securitisation facilities. The company has radically changed since 2019.

{kind=link}

The primary revenue generation is through the upfront franchisee fee and recurring royalties. The company is growing through acquisitions but also heavily through organic growth. Year to date, the company has opened more than 100 restaurants and targeting a year-end total of at least 125.

The fast food industry is expected to grow to $802.62 billion in 2026 at a CAGR of 6.3% and FAT is taking on this potential. It has set agreements for more than 1,000 new franchise restaurants which will provide the company with organic growth of an incremental $60 million in adjusted EBITDA. It is also looking into non-traditional locations for expansions such as universities, airports and stadiums.

{kind=link}

Another exciting part of the business is its pretzel and cookie dough manufacturing facility which is only at 33% capacity and has EBITDA margins of 40%, thus a very profitable business that can scale. Year to date, it has generated close to $25 million in sales.

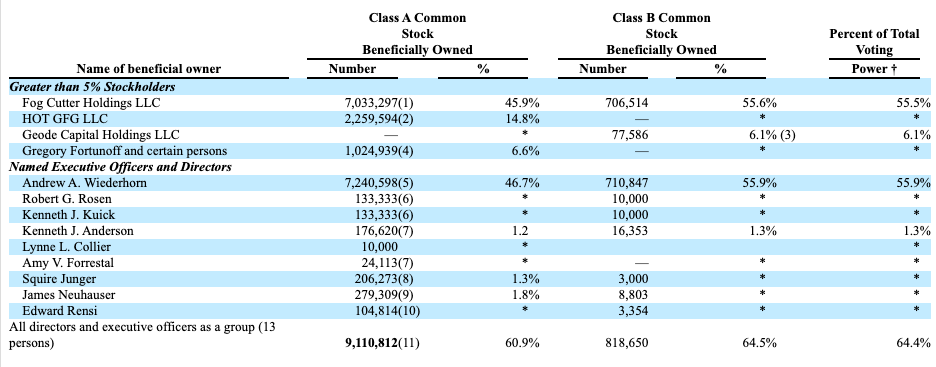

If we look at ownership, we can see that the CEO has a huge stake in the company, which is good to know as it would mean that his needs are more aligned with shareholders, although this should not be the main reason to invest in a company, it is positive to see.

{kind=link}

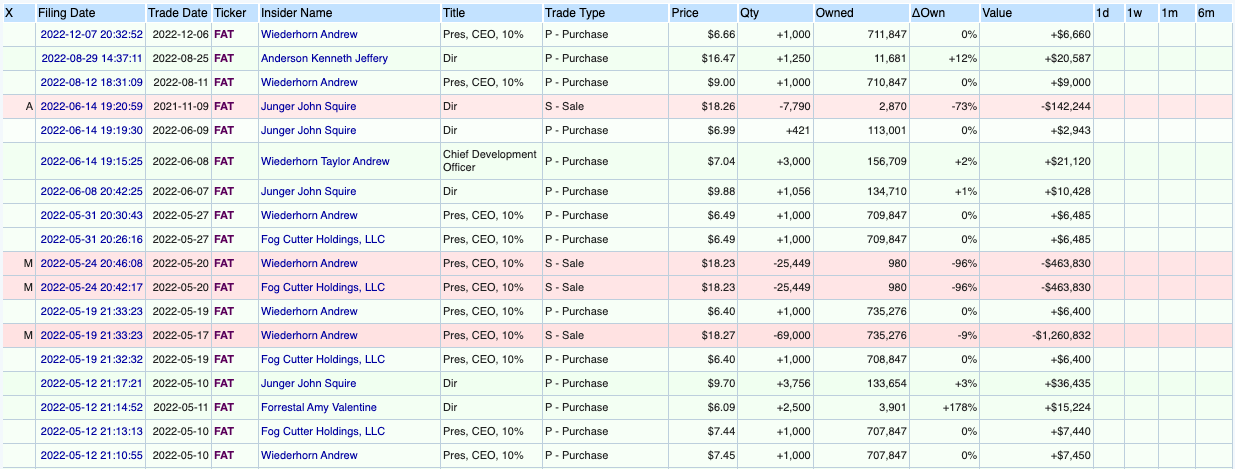

Furthermore, there has been ongoing insider buying activity, most recently this month by the CEO.

{kind=link}

The pressing problem is that FAT wanted to acquire brands quickly and did so by issuing many securitisations facilities without rating their debt first, which has left them with high-interest rates. It acquired four deals totalling $900 million on 30-year bonds at a fixed interest rate only for five years. FAT needs to rate its debt to lower interest-rate expenses. However, interest rates have increased at incredible rates. Only last week, another hike was made by the feds. This is a considerable worry.

Financials

If we look at the revenue, we can see a significant growth curve due to the number of acquisitions that have taken place and the organic growth through several new restaurants over the last few years.

{kind=link}

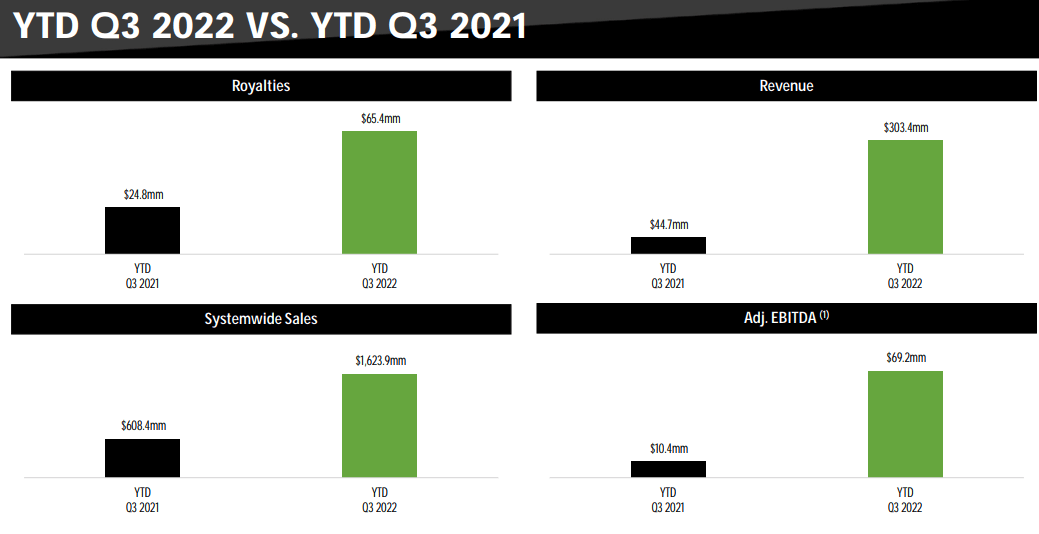

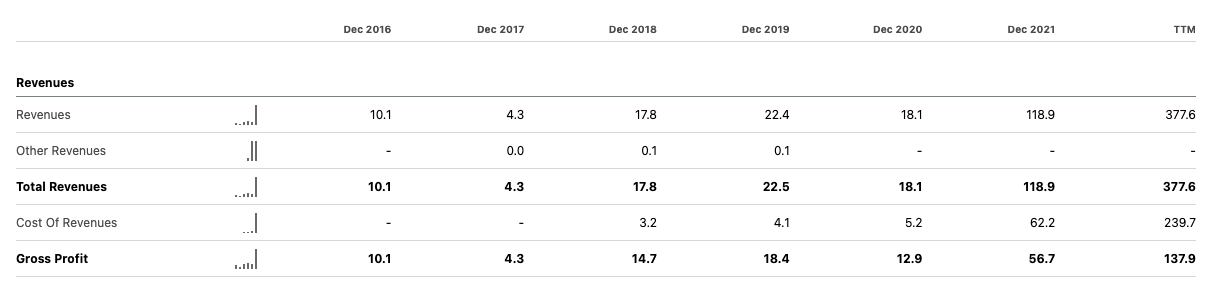

Over five years, we have seen revenue grow from $4.3 million to $118.9 million. Twelve months trailing, we see a record high of $377.6 million. In Q3 2022, there was a year-on-year revenue increase of 247% to reach $103.2 million. The company is also increasing its foreign sales, adding to its diverse revenue streams. The main reason is acquisitions and post-COVID-19 pandemic recovery.

{kind=link}

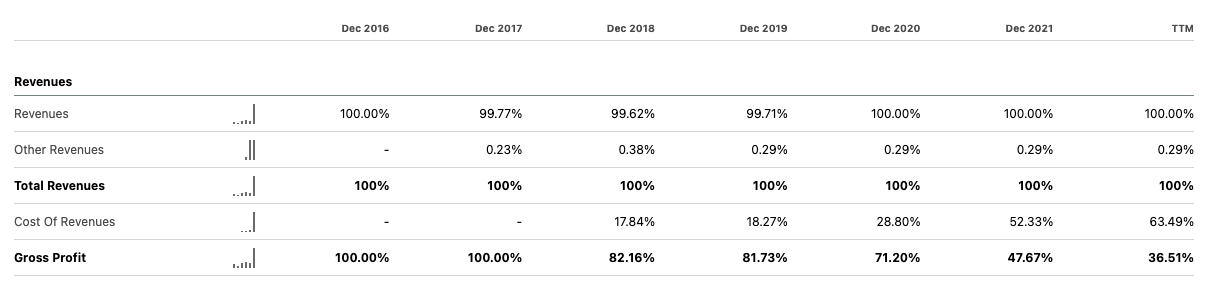

However, we can see that the company is impacted by the inflationary environment impact on increased costs and operational expenses, with gross profit margins decreasing to 36.51% TTM.

{kind=link}

The company's net income has also been negative. However, this is impacted mainly by the number of acquisitions that have taken place. Although this last quarter, the company missed earnings expectations by $0.57 by posting a loss of -$1.42 per share.

Annual net income (SeekingAlpha.com)

The EBITDA has been increasing upward, which is positive to see. In Q3 2022, it grew to $24.6 million (adjusted). The expectation is for adjusted EBITDA to be similar to this past quarter and for year-end results to come in around $90 million.

Annual EBITDA (SeekingAlpha.com)

The company has had positive upward levered cash flow for the last three years. Its twelve-month trailing cash flow is currently negative $12.0 million.

Annual levered cash flow (SeekingAlpha.com)

Cash is a pressing issue. It recently redeemed the value of $43.2 million of its Series B Preferred stock ( FATBP ) from an affiliate of Garnett Station Partners for $23.69 per share in addition to unpaid dividends, which helps with cash flow. Below we see the increasing total liabilities.

Quarterly total liabilities (SeekingAlpha.com)

And below, we see the increasing interest rate expenses that have come along with the debt intake for the acquisitions.

TTM Net interest rate expense (SeekingAlpha.com)

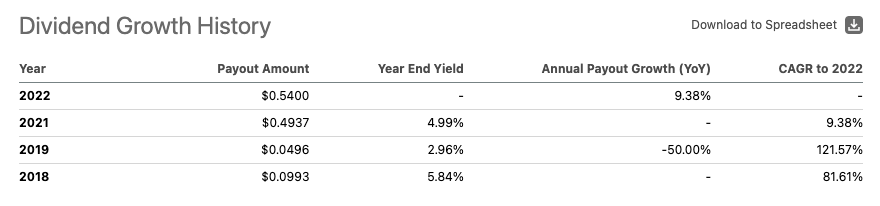

FAT Brands has a handsome dividend for such a small stock and is well above the industry average, with an annual payout growth of 9.38%. However, as it currently stands with negative earnings, the company cannot cover their dividend payment which is a big red flag.

{kind=link}

Final thoughts

FAT has an attractive asset-light business with popular restaurant brands and a proactive approach to growing restaurants and franchisees through events and incentives, and this is paying off if we look at the pipeline for the following year. It is exciting to see the published updates on new restaurants opening across the globe. Furthermore, it has a profitable manufacturing facility currently only utilised at around 30%. There is a lot of upside potential if the company improves its cash from operations. However, in the current environment, the company has negative cash flow and massive debt at high-interest rates that are hugely impacting the company's potential profit margins. It feels like FAT may have bitten off more than it can chew. Due to the increasing risks, poor EPS results in Q3 and uncertain market conditions, I'm downgrading FAT to Hold.

For further details see:

FAT Brands: Growing Number Of Restaurants, But Short On Cash