FAT - FAT Brands: Some Stiff Headwinds Could Ruin Its Growth Party

2023-03-21 12:42:09 ET

Summary

- CEO stepping down could be a disruptive factor as the company attempts to ramp up growth initiatives.

- Revenue should maintain momentum on organic growth and acquisitions.

- Profitability remains a big concern as expenses rise and debt payment rates jump.

- An economic downturn would likely hit the company hard because of consumers reprioritizing spending and cutting back on eating out.

Since FAT Brands Inc. ( FAT ) took off in August 2020, the company enjoyed a rapid growth trajectory in its share price, reaching a high of a little over $14.00 per share, and has since struggled to maintain momentum, even after making numerous acquisitions and opening many more stores.

While the company has made progress on the revenue side, it has underperformed the sector in a number of profitability metrics, and with the ongoing plans to grow at a rapid pace, along with the rising cost of capital, means it's probably going to continue to struggle for some time before it turns a profit.

On the organic side of the business, it has plans in place to build over 1,000 more restaurants over the next several years, which have signed agreements already in place.

Taken together with acquisitions, the company should continue to grow revenue, but I see it coming under even more earnings pressure in light of interest rates that are expected to remain high for a substantial period of time.

In this article, we'll look at its most recent numbers, its growth strategy, the implications of changing CEOs at a vital time for the company, and what the future potentially holds for the company.

{kind=link}

Some of the numbers

Revenue in the fourth fiscal quarter of 2022 was $103.8 million, compared to revenue of $74.2 million in the fourth fiscal quarter of 2021, a gain of 39.9 percent. Full year revenue for fiscal 2022 was $407.2 million, compared to full year fiscal 2021 revenue of $118.9 million.

The improvement in revenue came primarily from acquisitions made in the fourth quarter of 2021, and the ongoing recovery of royalties from the effects of COVID-19 on the performance of its businesses.

On a same-store basis, revenue was up 2.7 percent year-over-year.

Adjusted EBITDA in the fourth fiscal quarter was $19.6 million, compared to $10.4 million in the fourth fiscal quarter of 2021. Adjusted EBITDA for full year 2022 was $88.8 million, compared to adjusted EBITDA of $21.1 million for full year 2021.

Net loss in the reporting period was -$(70.8) million, or -$(4.29) per diluted share, compared to -$(19.6) million, or a net loss of -$(1.38) per diluted share in the fourth quarter of fiscal 2021. Net loss for full year 2022 was -$(126.2) million, or -$(7.66) per share, compared to a net loss of -$(31.6) million, or -$(2.15) per share for full year 2021.

As of December 25, 2022, the company had cash-on-hand of $28.7 million, with an additional $25.4 million in restricted cash. It had long-term debt of close to $50.00 million.

Two major catalysts

As mentioned above, a big part of the boost in revenue in the fourth quarter was acquisitions. The company acquired Twin Peaks in October 2021, and Fazoli's and Native Grill & Wings in December 2021.

The other major catalyst was organic growth, with the company opening more than 140 new units during 2022; 44 of them were opened in the fourth fiscal quarter. That momentum is expected to continue in 2023, with another 150 to 175 new stores scheduled to be opened during the year.

As for the long-term pipeline, the company has a goal of building over 1,000 more restaurants, with signed agreements for them already in place. Over the next several years, the company estimates they'll be worth another $60.00 million in adjusted EBITDA, bringing the total from about $90.00 million today to $150.00 million within several years.

If adjusted EBITDA achieves that level, management is guiding for its leverage ratio to drop to about 7x its securitized debt. While it's an improvement, I think the company is trying to grow too fast, and it's going to struggle to generate a profit as expenditures and interest payments continue to climb. Management believes scaling will take care of that, but it has yet to prove it.

There is also a strong likelihood of the economy getting worse in 2023. Under that scenario, consumers will reprioritize their spending, and one of those will be to cut back on going out to restaurants, which I believe would hit FAT hard. It would also disrupt their pace of growth, pushing it further out into the future.

I think the market is pricing that in now, in spite of the company's big growth plans. It is trading at about $7.31 per share as I write, almost exactly where it was trading at in April 2021.

Growth and profitability

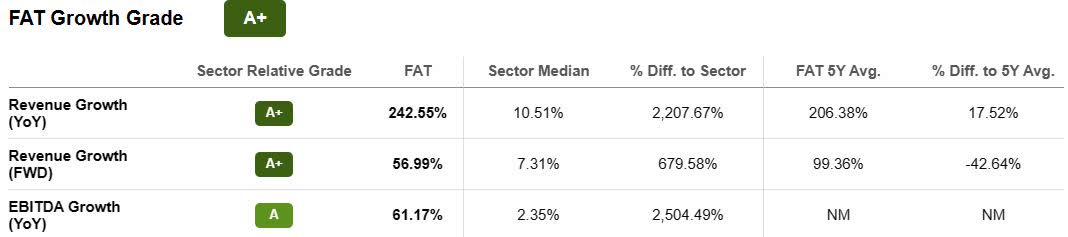

In regard to growth , the company has easily surpassed the sector median, with year-over-year revenue growth soaring by 242.55 percent, compared to the sector median of 10.51 percent, higher by 2,207.67 percent.

Revenue growth ('FWD') is projected to be 56.99 percent, as measured against the sector median of 7.31 percent, up by 679.58 percent.

Year-over-year EBITDA growth was 61.17 percent, compared to the sector median of 2.35 percent, up 2,504.49 percent.

{kind=link}

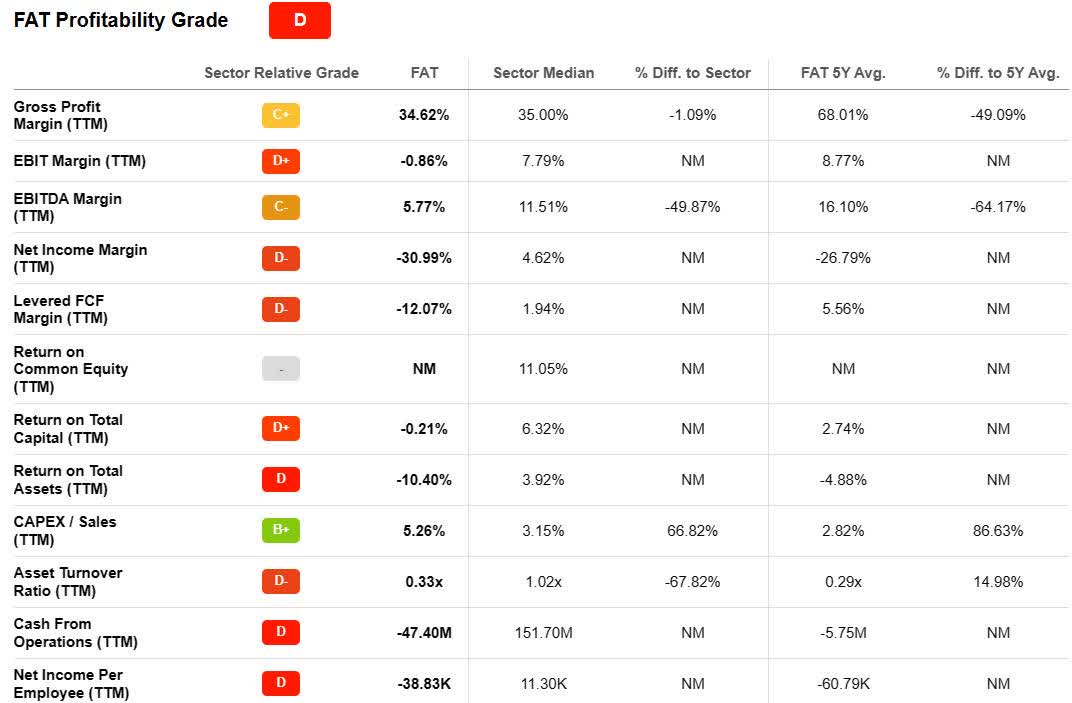

While the company has grown sales organically and via acquisitions, it has come at the cost of profitability, with the firm underperforming the sector in most categories.

Gross profit margin ('TTM') was 34.52 percent, compared to the sector median of 35.00 percent; EBIT margin ('TTM') was -(0.86) percent, compared to the sector median of 7.79 percent; EBITDA margin ('TTM') was 5.77 percent, compared to the sector median of 11.51 percent, down -49.87 percent; and net income margin ('TTM') was -(30.99) percent, compared to the sector median of 4.62 percent.

Other profitability metrics such as return on total capital, return on total assets, cash from operations, and net income per employee, as the chart below shows, all significantly underperformed the sector median.

{kind=link}

A major expense to consider now and in the future is interest expense. In the fourth fiscal quarter, it was $24.2 million, compared to $17.1 million last year in the same reporting period. That will increase in the future as the company continues to spend on organic growth and growth via acquisitions. I draw that conclusion from the high interest rates environment that should remain in place for the next couple of years, and possibly longer.

CEO stepping down

FAT announced that CEO Andy Wiederhorn would be stepping down from his role as CEO and taking on the role of an outside consultant. Wiederhorn will remain as CEO until the time an interim CEO is announced, which will be before the official transition date of May 5, 2023.

Wiederhorn is likely leaving in order to avoid the distraction from his connection to a government investigation he has ties to.

The significance there is, at a time when the company is significantly ramping up its growth trajectory, it's going to have to transition to a new head of the company.

There's no way of knowing how the interim CEO will perform or how the permanent CEO will do once installed into leadership.

A potential positive here is the company could decide on a candidate that has the proven ability and history to lower costs while implementing growth plans. That, in my opinion, would be a big plus for the company and could result in consistent, sustainable growth in the stock over the long term.

Conclusion

FAT gives me the impression it's attempting to grow at all costs, and if I'm right in that assessment, it is in fact growing at all costs, as expenses continue to rise, capital gets more expensive, and uncertainty surrounding consumer spending habits in 2023 weigh on the potential performance of the company.

I think the headwinds the company faces are stronger than current management thinks, and it will probably get disrupted in 2023 if consumers start to cut back on going out and spending at restaurants, which I think is a very high probability.

Under that scenario, the company's growth plans would be significantly slowed down and pushed out further into the future, which would probably result in the share price taking a big hit if both revenue and earnings underperform.

Since it has bounced big off its 52-week low of $4.73 on December 30, 2022, I see it being poised for a correction, especially when considering the continual pressure on its earnings and the need to spend a lot more to meet its organic and inorganic growth plans. Based upon the way investors have responded to the moves of the company over the last couple of years, I believe the stock is likely to come under further pressure in 2023, which could provide a very attractive entry point, and a good dividend yield if the company keeps it where it's at.

For further details see:

FAT Brands: Some Stiff Headwinds Could Ruin Its Growth Party