FAT - Fat Brands: Treading The Line Between Expansion And Overreach

2023-11-08 08:36:51 ET

Summary

- Fat Brands Inc. has seen a 15.19% increase in stock value since December and has rewarded long-term investors with returns of 33.86%.

- The company's aggressive growth strategy and high leverage are becoming increasingly risky in an environment with rising interest rates and growing inflation.

- Fat Brands has widened its losses, has negative levered free cash flow, and a high amount of debt, making it a risky investment.

When I last evaluated Fat Brands Inc. ( FAT ), I decided to downgrade my position primarily due to concerns about the high debt, insufficient cash reserves, and rising expenses, particularly considering the current market conditions. However, since I wrote about it in December, the stock's value has surged by 15.19%, delivering an impressive return of 33.86% for long-term investors. Furthermore, the company has continued to acquire new brands .

{kind=link}

In its most recent Q3 2023 earnings, we saw an improving top line. However, the net loss has grown. Nevertheless, a key concern lies in Fat's rapid acquisition of brands through numerous securitisation facilities without assessing the debt, resulting in high-interest rate expenses . Additionally, the growth rate has notably decelerated over the past year. We're analysing a company offering dividends with a negative payout rate, escalating debt, and minimal cash reserves. This presents a considerable risk despite the low short interest of 2.39%. I'm choosing to maintain a hold position owing to the expanding losses and negative leveraged free cash flow.

Company updates

In my previous article , I discussed Fat's growth. It's impressive how Fat developed its asset-light business model into a substantial entity in the last three years, with a wide array of restaurants worldwide across eighteen food and restaurant brands. Most recently, it acquired Smokey Bones Bar and Fire Grill for $30 million, which is expected to increase annual adjusted EBITDA by approximately $10 million. Yet, the company's ambitious growth approach and high reliance on borrowing are becoming increasingly risky in a climate of rising interest rates. This economic scenario, coupled with uncontrolled inflation, is notably impacting how consumers make their purchasing decisions, which presents significant challenges for the company's future. We have seen the company increase its top-line. However, its bottom line has continued to decline.

Quarterly income statement (Marketscreener.com)

An evident trend emerges in the company's escalating annual interest expenses.

Annual interest expenses ( SeekingAlpha.com )

{kind=link}

Looking towards Fat Brands' future financial outlook, the recent recent earnings call didn't provide specific guidance for Q4 2023. However, there's a clear intention to sustain growth momentum through 2024. Even though there was a slight decrease in store openings this year, the company appears positive about achieving approximately 175 store openings in the upcoming year. Moreover, there's an encouraging sign with a robust pipeline of over 1,100 signed agreements for new units. This is anticipated to bolster adjusted EBITDA by approximately $60 million, offering a favourable financial contribution. Additionally, there's a plan to potentially take one of its brands, Twin Peaks, public in 2024 . Acquired for $300 million in 2021, this move could hold value for shareholders, potentially adding to the company's growth trajectory.

Financial updates

In Q3 2023, Fat Brands observed a 6% uptick in total revenue, reaching $109.4 million. However, there's been a concerning trend in the company's financials with losses widening from $23.44 million a year ago to $24.65 million in the most recent quarter. The growth in revenue was predominantly influenced by a 4.8% increase in royalties, a 2% climb in company-owned restaurant revenues, a notable 228.5% surge in franchise fees, and an 18.9% rise in revenues from its manufacturing facility. While the income from operations has shown growth, the company is facing significant and escalating interest expenses that are chipping away at its profits. This growing trend in losses over the quarter and the last nine months is an area of concern for the company.

Income statement Q3 2023 versus Q3 2022 (Investor presentation 2023)

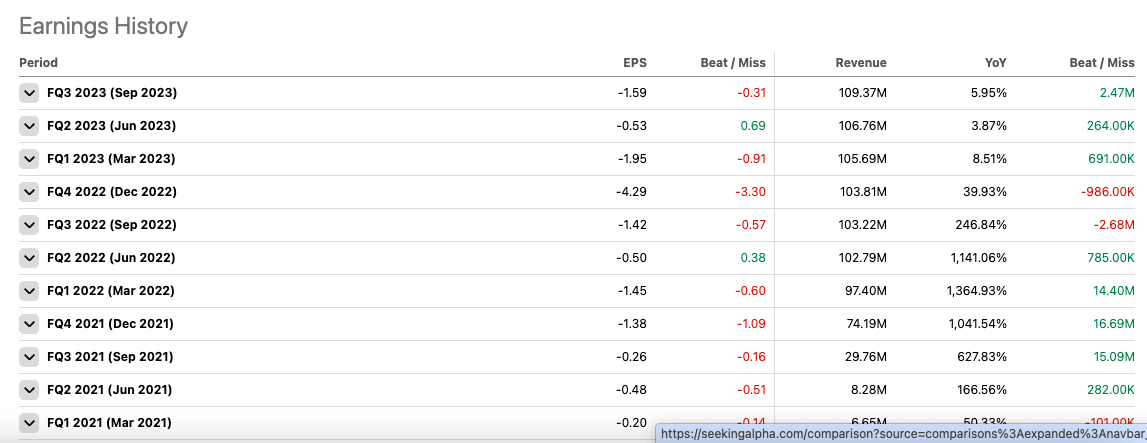

If we look at EPS over the last eleven quarters, we can see that the company has only beat expectations twice, and YoY earnings have worsened. Revenue has increased; however, the rate of growth has declined from a three-year CAGR of 193.29% to a YoY growth rate of 12.72%.

{kind=link}

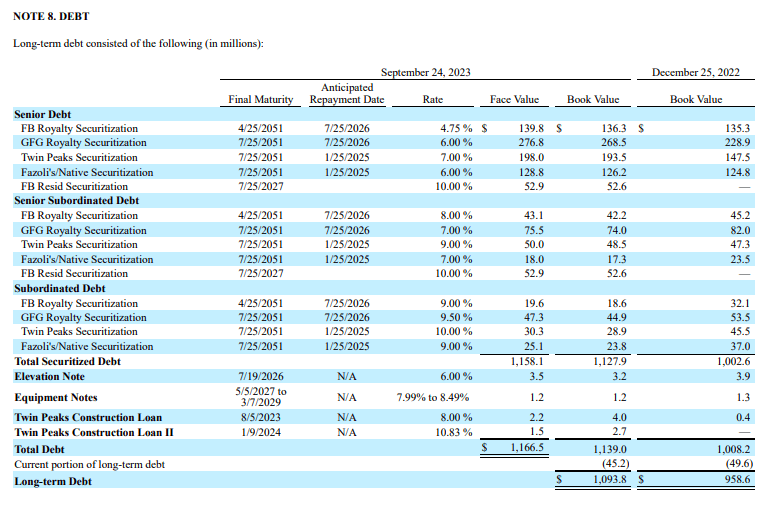

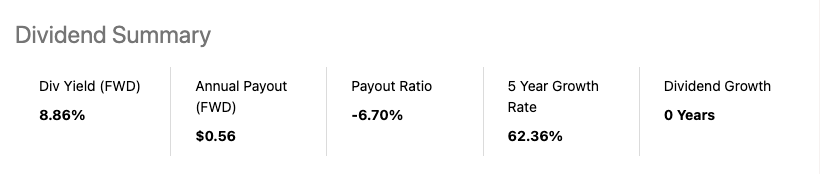

The company's financial situation appears less than ideal. While it holds around $87.99 million in total cash, the total debt has notably increased to $1.3 billion. There's an additional $200 million in available-for-sale securities , enhancing the cash reserves. The concerning point is the negative levered free cash flow of TTM $30.82 million. Moreover, the company is paying out a dividend with a negative payout ratio of 6.70%, suggesting that the dividend may not be adequately supported by the company's financial performance. This indicates a significant discrepancy between its cash position, debt, and financial obligations, which could pose challenges to its financial stability.

{kind=link}

{kind=link}

FAT has announced that it will be paying a quarterly dividend of $0.14 per share, which is the same as previous payouts. The forward yield is expected to be 8.56%. The payment is scheduled for December 1, and shareholders who are on record as of November 15 will be eligible to receive it. The ex-dividend date has been set for November 14.

{kind=link}

Risks and Final thoughts

Fat Brands has significantly expanded its brand portfolio over nearly three years, generating increased top-line benefits from these acquisitions. However, the YoY top-line growth has notably decelerated. The company has witnessed annual growth in net losses and maintains a negative EPS. Being a micro-cap company, there's a higher risk associated with investing, given its limited access to investment capital and susceptibility to market changes. While the potential for substantial growth exists, the stock's value can decrease as swiftly as it rises. As the company anticipates robust growth into FY2024 and announced a dividend payment, it has done so with a negative payout ratio, negative levered cash flow, and a substantial debt burden. It seems that FAT Brands may have overextended itself. Considering the escalating risks, disappointing EPS results in Q3 2023, and uncertain market conditions, despite the stock's 15.19% increase since my last article, I am not suggesting buying the stock and would recommend a Hold rating.

For further details see:

Fat Brands: Treading The Line Between Expansion And Overreach