FATBB - FAT Brands: Why I Got Out Of The Preferreds

2023-11-09 10:32:15 ET

Summary

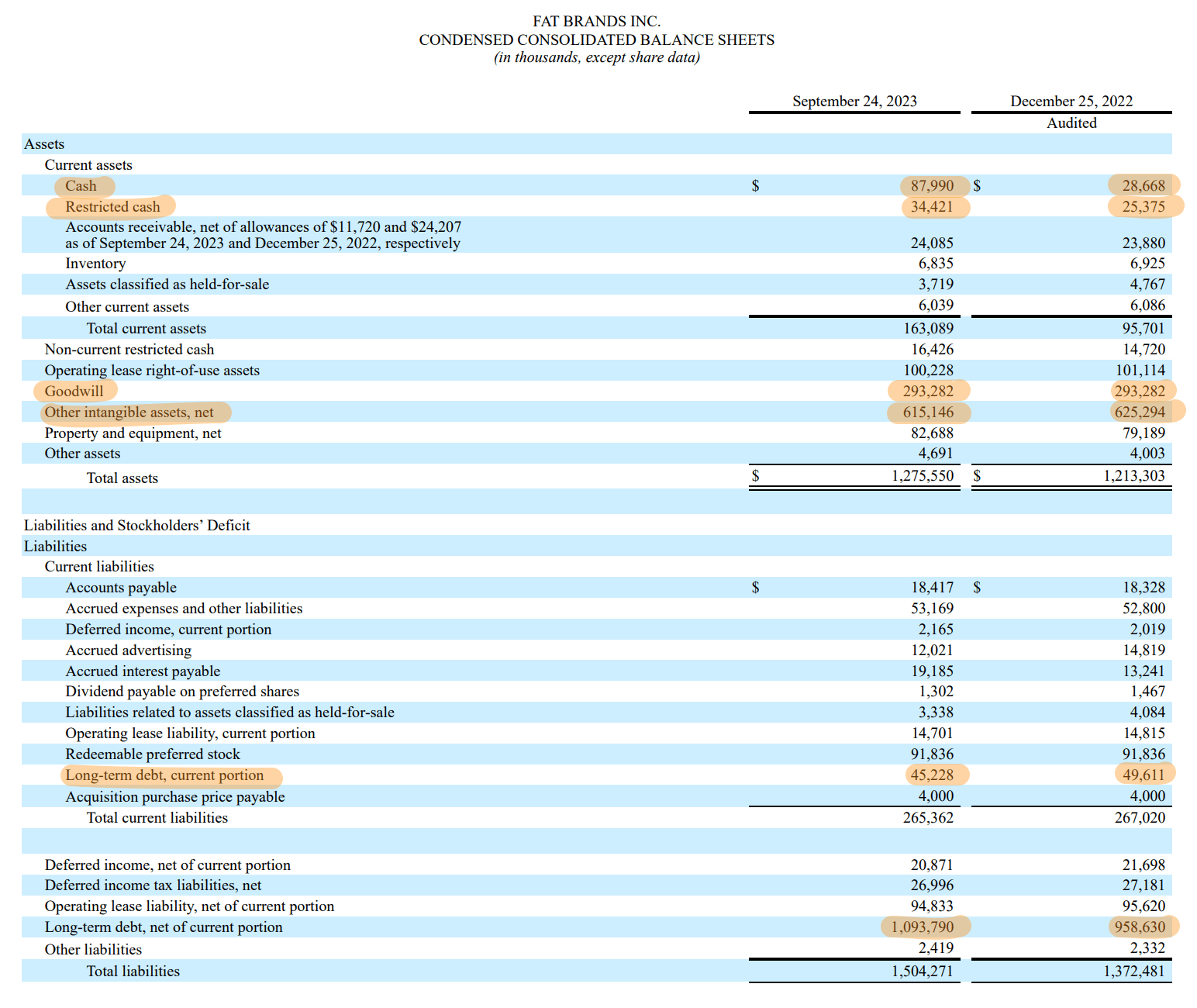

- FAT's total debt balance has risen to a record high with interest expenses as a percent of revenue jumping to 27% during its fiscal 2023 third quarter.

- The company continues to layer on debt ahead of a still uncertain IPO of its Twin Peaks restaurant.

- Common equity is negative and deteriorating every quarter as free cash burn continues to stack up.

I'm out of FAT Brands' ( FAT ) ( FATBB ) preferred shares ( FATBP ) with a small total return from both capital uplift and dividends. The decision to divest the ticker after a few months of holding came on the back of bearish indicators that were flashing red. At the core of the company's loss of investability is a steadily expanding debt balance, declining liquidity, and a still uncertain backdrop for the IPO of its flagship Twin Peaks in calendar 2024. Initial optimism that the IPO of Arm would pry open the capital market has now turned into deep uncertainty around the impact of interest rates remaining higher for longer even with the Fed highly likely set to end rate hikes. There are reasons for both common and preferred shareholders to be worried as cumulative net losses stack up.

The company last declared a quarterly cash distribution of $0.14 per share , unchanged from its prior payment for what's currently an 8.7% annualized forward dividend yield. Critically, FAT's continuation of a common share dividend distribution policy against fiscal 2023 third-quarter cash and equivalents balance that at $88 million formed a cash runway of just six quarters is odd and fundamentally destructive to its shareholders. It raises the specter of material losses as continued free cash burn aggregates and the proposed capital raising IPO looks uncertain under current capital market conditions. The preferreds are down 11% year-to-date, are currently swapping hands for 60 cents on the dollar, and come with a 13.6% yield on cost. These factors are attractive if you ignore the fast deteriorating balance sheet.

{kind=link}

Losses, Free Cash Burn, And Total Debt

{kind=link}

FAT's long-term debt stood at $1.09 billion at the end of its third quarter. There is another $45.2 million of current debt that places its total debt position at $1.14 billion. This drove $29.7 million in quarterly interest expenses during the third quarter, up 22% from the year-ago period. Total common equity is negative and has been deepening in recent quarters. This was negative $272 million in the third quarter, a deterioration from $133 million a year ago as continued net losses drove FAT to take on more debt to fund its operations. Further, the bulk of common equity value is being driven by goodwill and other intangible assets.

The company's cash balance at $88 million was up $57.4 million sequentially, helping expand a cash runway that had dropped to less than four quarters. The rise in cash was driven by FAT's continued strategy of layering on debt ahead of the possible IPO to fund its operations and to pay a dividend even against a free cash burn of $8.2 million. Whilst this dropped by $2.9 million from $11.1 million in the year-ago period, the outlook for profitability is still poor and the company stated during its third-quarter earnings call that it's banking on the IPO of Twin Peaks to help with the repayment of debt. How does this end? Two scenarios. The company continues operations as it is by the continued build-up of debt and is then able to IPO Twin Peaks at a significant valuation next year. In this scenario, the dividends to both common and preferred shareholders are maintained.

The Dividend Is At Risk

The bearish scenario would see FAT be forced to delay the IPO of Twin Peaks with continued tepid stock market conditions pushing the company to delay the IPO into 2025 or 2026 when interest rates could be lower and market appetite for risk would be higher. This would still come with what's been a rapidly eroding equity base. FAT is notching some operational momentum with revenue of $109.37 million growing 6% over its year-ago comp and beating analyst consensus by $2.47 million. However, system-wide sales only notched growth of 0.8% versus the year-ago period with FAT also opening 30 new stores during the period.

The continued accumulation of losses which came in at $24.7 million, or $1.59 per share, was a deterioration from the year-ago period. Hence, it's hard to point to a substantial near-term positive for FAT. Shareholders are now just holding a security where the losses are stacking up, the debt is increasing and the equity base is inverting further into negative territory. There could come a critical point where the continued layering of debt becomes a Sisyphean undertaking under the pressure of interest expenses which formed 27% of FAT's revenue for the third quarter. This was up from 23.7% in the year-ago period and highlights the pressure the company will face as its debt expands and losses continue to get aggregated. Both the commons and preferreds are a sell against this more likely bearish scenario.

For further details see:

FAT Brands: Why I Got Out Of The Preferreds