FATE - Fate Therapeutics: Yes For Speculators No For Defensive Investors

Summary

- Fate Therapeutics has potential inflection points stemming from clinical trial and regulatory momentum in the next 6-12 months.

- For those taking speculative positions within healthcare, this could present with potential upsides post-event(s).

- Those investors looking for a defensive overlay within healthcare might find weakness in FATE's measures of corporate value.

- With these points in mind, we rate FATE a hold with a $21 per share valuation.

Investment summary

There are selective opportunities located within the healthcare universe for investors taking both speculative and defensive positions. In either sense, factor rotations in H2 FY22 corroborate that value remains a thematic favorite for investors, adding a layer of resiliency to portfolios. Measures examining corporate value are therefore of upmost importance for equity investors looking ahead, in order to decipher the quality of earnings and business model one is allocating to.

With this in mind, we examined Fate Therapeutics, Inc. ( FATE ) and found that it offers potential upsides from clinical trial and regulatory momentum over the next 6-12 months. For those on the speculative side, this is ideal. However, we also noted that for those seeking a defensive beta name in healthcare, FATE might not be the best choice, due to lack of profitability and unsupportive valuations from forward earnings. With opportunity costs front of mind, but also acknowledging the strengths in FATE's wider offering, we rate FATE a hold with a price target of $21.

Exhibit 1. FATE 6-month price action

{kind=link}

Q2 earnings indicative of regulatory, fundamental momentum

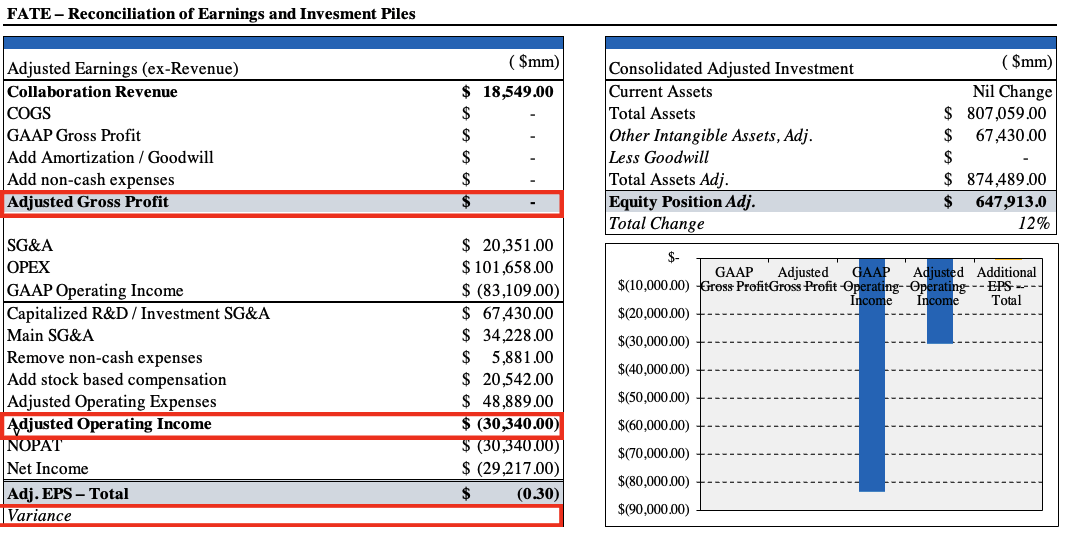

Fundamental momentum is creeping up alongside regulatory momentum for FATE. Despite this, its earnings do need some cleaning up to reflect a more accurate snapshot. Revenue obtained via collaborations with Janssen and Ono Pharmaceutical (OPHLY) rose to $18.5 million in Q2 FY22, a 38% growth YoY. Meanwhile, the company saw a ~67% YoY headwind at the G&A line with expenditures increasing to $20.4 million. However, breaking down the increase in G&A, ~34% or $6.9 million ($0.07/share) was attributed to stock based compensation ("SBC"), up $4.3 million from this time last year. Operating expenses were also comprised of $81.3 million in R&D spend, that we argue should be capitalized and treated as an investment on the balance sheet [discussed later]. All in, SBC comprised $20.5 million of the $101.6 million in operating spend for the quarter.

On the regulatory front, FATE achieved its first clinical milestone in its CAR T-cell product candidate, FT819. This is under an amended license agreement with Memorial Sloan Kettering Cancer Centre ("MSK"). The first milestone payment to MSK was activated following this milestone. This is important as there could be an additional 2 milestone payments obliged to MSK that are based on trading volumes of the company's stock in ranges of $100-$150/share. Changes in the fair value of these instruments is booked as income or expenditure by FATE and is therefore worth keeping an eye on from period to period and make necessary adjustments if necessary.

Exhibit 2. FT819 descriptive overview

Data: Fate Therapeutics Website

{kind=link}

Meanwhile, the Phase 1 trial of FATE's FY596 in combination with rituximab exhibited favorable safety data in both the single dose and dual-dose cohorts. Safety data held up well up to 900 million cells per dose, and the higher-dose regime could well be the protocol looking ahead, by estimate. From here FATA will continue to evaluate dosages for maximal therapeutic effect, with the next moves being a 3-dose cohort at a dose of 1.8 billion cells. We are intrigued to observe the outcome of the increased cellular load, particularly as the clinical protocol permits further dose escalation

In terms of regulatory catalysts, investors should keep an eye out for the company's FT516 RMAT Type-B multidisciplinary meeting with the FDA this coming quarter. From here we'll have better understanding on the registrational pathways for the off-shelf programs against refractory aggressive B-cell lymphoma. Patients will include those whose disease is refractory or relapsed after previous treatment from other CD19 targeted CAR T-cell therapies.

Reconciliations for accurate valuation

We've identified a number of adjustments that need to be made in order to accurately value FATE, in order to understand exactly what it is we're buying. Firstly, R&D expenditure came in at $81 million for the quarter, up from $48 million YoY. We argue that R&D expenditure should be capitalized and amortized as an intangible asset, as it is an investment set to create future economic value. This has implications to earnings and investment for the company. However, we also found we can't capitalize FATE's entire R&D spend.

Notably, the $33 million YoY increase in R&D stemmed from:

- $4.9 million increase in employee SBC expense to $13.57 million

- $9 million increase in spend to third-party professional consultants

- $8.6 million increase in expenditures for laboratory materials and supplies relating to the manufacture of product candidates and conduct of research activities.

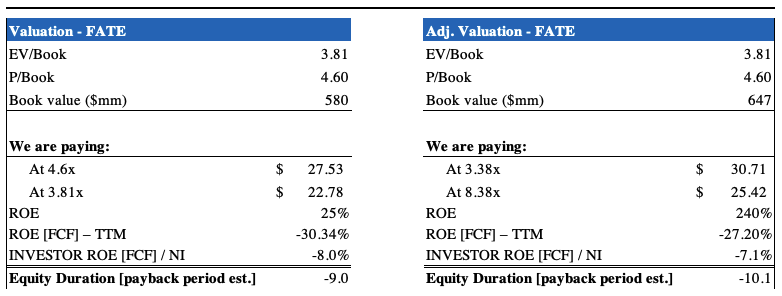

Therefore, we can only advocate to capitalize $67.4 million of R&D as an investment, seeing as SBC is an expense in our eyes. This has implications for both earnings and valuation, as discussed below. In addition, the company's drug product manufacturing facility in California has now opened with engineering runs underway. This is a tangible source of value that will supply drug products for companies conducting pivotal trials. In all, the company has $580 million in tangible book value with this included.

Exhibit 3.

{kind=link}

Valuation

Being a clinical stage biopharma company, valuation ideally comprises a number of factors to obtain a corporate value for the company. However, we aren't confident on the predictability of estimating the prospective value of FATE's pipeline or working in terms of what's 'possible'. Instead, what's real and 'probable' are better terms to work by. With that, we observe corporate valuation in terms of earnings and investment; what's real and what's expected. We record this in shorthand with multiples of book value and earnings estimates. Instead, we are focusing on what we'd be buying today in FATE.

Keeping this mantra in mind, with respect to the investment pile, we note shares appear to be richly priced after reorganizing for adjustments as in Exhibit 3. As seen in the Exhibit below, shares are priced at ~4.6x book value, and 3.8x enterprise value ("EV") to book value. Post-adjustment, at these multiples, we are paying an implied value of $25-$30.71 [prior, shares looked to be fairly priced]. The question is if this presents as compelling value or if we'd be overpaying. Given its lack of profitability, return on equity measures are negligible for the company.

Exhibit 4. Post-adjustment valuations look pricey

Data: HB Insights Estimates. Image: HB Insights

{kind=link}

In this vein, we have to project the future cash flows on offer for the company. We see this best represented at the top line for FATE in its collaborative revenue. As seen in Exhibit 5, the valuation model prescribed delivers a valuation of just $21 for the company, suggesting we'd be overpaying at current prices. Investors are asked to pay ~$25-$30 in implied value to receive a potential downside of 30% at the upper end.

Exhibit 5. Fair value distribution values FATE with a value gap to the downside

Lack of profitability and lack of predictability in estimating the company's future cash flows are key factors in the valuation debate

Data: HB Insights Estimates. Image: HB Insights

With the culmination of these factors in mind - valuations in particular - we rate FATE a hold and look forward to observing potential inflection points from the clinical trial and regulatory momentum listed above.

For further details see:

Fate Therapeutics: Yes For Speculators, No For Defensive Investors